Download as docx, pdf, or txt

You might also like

- Task 3 - DCF ModelDocument10 pagesTask 3 - DCF Modeldavin nathan0% (1)

- T24 Account Additional Features R17 PDFDocument56 pagesT24 Account Additional Features R17 PDFTes Tesfu100% (1)

- Internship Report On Js Bank LimitedDocument58 pagesInternship Report On Js Bank Limitedbbaahmad8973% (11)

- Unsealed - The 666 Mystery (Rev03)Document33 pagesUnsealed - The 666 Mystery (Rev03)Pablo Jr Agsalud100% (1)

- Distressed Debt PrezDocument32 pagesDistressed Debt Prezmacondo06100% (2)

- Assessment of Cash Management in CBEDocument44 pagesAssessment of Cash Management in CBEEfrem Wondale88% (8)

- 3 5 Profitability and Ratio AnalysisDocument2 pages3 5 Profitability and Ratio AnalysisKANAK KOKARENo ratings yet

- FA M8 NotesDocument22 pagesFA M8 Noteslim hwee lingNo ratings yet

- Ratio Analysis: It Is Concerned With The Calculation ofDocument19 pagesRatio Analysis: It Is Concerned With The Calculation ofsajithNo ratings yet

- BFA103 Accounting and Financial DecisionDocument2 pagesBFA103 Accounting and Financial DecisionismailNo ratings yet

- A2 Business Formula SheetDocument2 pagesA2 Business Formula SheetThana YoyoNo ratings yet

- Ratio Analysis Chart Complete 262tqvpDocument2 pagesRatio Analysis Chart Complete 262tqvpCA Manoj Kumar SabatNo ratings yet

- Strategic Management (The Strategy Framework)Document19 pagesStrategic Management (The Strategy Framework)Charles CagaananNo ratings yet

- Notes On Ratio AnalysisDocument12 pagesNotes On Ratio AnalysisVaishal90% (21)

- Business Analysis Project: Session 8 Assignment Guidelines 2018 19 Andre Samuel SAM TrinidadDocument21 pagesBusiness Analysis Project: Session 8 Assignment Guidelines 2018 19 Andre Samuel SAM TrinidadFederica FreddiNo ratings yet

- Finance 1665265099Document19 pagesFinance 1665265099hicham ABOUYOUBNo ratings yet

- Ratio Formula Analysis and InterpretationDocument5 pagesRatio Formula Analysis and InterpretationGalib Hossain50% (2)

- Ratio AnalysisDocument10 pagesRatio AnalysisUdayan KarnatakNo ratings yet

- Final Cheat Sheet FA ML X MM UpdatedDocument8 pagesFinal Cheat Sheet FA ML X MM UpdatedIrina StrizhkovaNo ratings yet

- Ederlyn Barrantes Rosemarie Gumopas: Mcgraw-Hill/IrwinDocument38 pagesEderlyn Barrantes Rosemarie Gumopas: Mcgraw-Hill/IrwinMary Joyce Anne AlejoNo ratings yet

- Ratio Analysis: Interpretation of Financial Statements: 1) Profitability RatiosDocument4 pagesRatio Analysis: Interpretation of Financial Statements: 1) Profitability RatiosCollen MahamboNo ratings yet

- Understanding Financial Ratios AnalysisDocument6 pagesUnderstanding Financial Ratios AnalysismanuNo ratings yet

- The City School: Ratio Analysis and InterpretationDocument9 pagesThe City School: Ratio Analysis and InterpretationHasan ShoaibNo ratings yet

- 15 FINANCIAL Performance MeasurementDocument8 pages15 FINANCIAL Performance MeasurementJack PayneNo ratings yet

- Economics 24Document106 pagesEconomics 24suranains7No ratings yet

- Ratio Analysis NotesDocument7 pagesRatio Analysis NotesabdullahzaheersheikhoNo ratings yet

- Ratio AnalysisDocument13 pagesRatio Analysismuralib4u5No ratings yet

- ACCOUNTING RATIOS-notesDocument5 pagesACCOUNTING RATIOS-notesMohamed MuizNo ratings yet

- Gross Profit - Margin RatioDocument16 pagesGross Profit - Margin RatioaaronNo ratings yet

- Ratio Analysis ParticipantsDocument17 pagesRatio Analysis ParticipantsDeepu MannatilNo ratings yet

- Quantitative Competitive Analysis Org PerformanceDocument29 pagesQuantitative Competitive Analysis Org PerformanceFederica FreddiNo ratings yet

- TIFA CheatSheet MM X MLDocument10 pagesTIFA CheatSheet MM X MLCorina Ioana BurceaNo ratings yet

- Fa Cheat Sheet MM MLDocument8 pagesFa Cheat Sheet MM MLIrina StrizhkovaNo ratings yet

- Intro To Financial RatiosDocument2 pagesIntro To Financial Ratiosmuhammadtaimoorkhan100% (3)

- Financial Ratios SummaryDocument8 pagesFinancial Ratios SummaryHany BadrNo ratings yet

- KPI's For Accounts & Finance DeptDocument1 pageKPI's For Accounts & Finance DeptShaheryar ShahidNo ratings yet

- Financial Ratio Analysis Dec 2013 PDFDocument13 pagesFinancial Ratio Analysis Dec 2013 PDFHạng VũNo ratings yet

- Strategic Cost ManagementDocument8 pagesStrategic Cost Managementneha chodryNo ratings yet

- ACCCDocument6 pagesACCCAynalem KasaNo ratings yet

- Accounting KpisDocument6 pagesAccounting KpisHOCININo ratings yet

- Lesson 3 Analysis and Interpretation NotesDocument8 pagesLesson 3 Analysis and Interpretation NotesoretshwanetsemosielengNo ratings yet

- Week 7 Formula SheetDocument1 pageWeek 7 Formula SheetHarsahej MokhaNo ratings yet

- About Financial RatiosDocument6 pagesAbout Financial RatiosAmit JindalNo ratings yet

- Profitability Ratios: (Opening Inventory + Closing Inventory) ÷ 2Document1 pageProfitability Ratios: (Opening Inventory + Closing Inventory) ÷ 2AnNo ratings yet

- Imp RatioDocument6 pagesImp RatiofejalNo ratings yet

- 09 Ratio AnalysisDocument26 pages09 Ratio Analysisrjtrainor14No ratings yet

- Ratio Analysis:: Liquidity Measurement RatiosDocument8 pagesRatio Analysis:: Liquidity Measurement RatiossammitNo ratings yet

- 6.financial RatiosDocument13 pages6.financial RatiosYousab KaldasNo ratings yet

- 3.5 Profitability and Liquidity Ratio Analysis. - IB Business 2023Document82 pages3.5 Profitability and Liquidity Ratio Analysis. - IB Business 2023qdxtcmvzgzNo ratings yet

- Financial Ratio AnalysisDocument5 pagesFinancial Ratio AnalysisPhuoc TruongNo ratings yet

- Ms & Oracle Project Ex DDocument53 pagesMs & Oracle Project Ex DA.D. Home TutorsNo ratings yet

- Manajemen Strategis - Pertemuan 4Document18 pagesManajemen Strategis - Pertemuan 4Ferdian PratamaNo ratings yet

- 9960 FinancialratiosDocument2 pages9960 FinancialratiosGhelyn GimenezNo ratings yet

- 1081 A1 Profits CA 02 FA Combined With NAVDocument38 pages1081 A1 Profits CA 02 FA Combined With NAVLyfe SpanNo ratings yet

- ProfitabilityDocument6 pagesProfitabilityVidaisbae 12No ratings yet

- Unit 3b Ratio AnalysisDocument52 pagesUnit 3b Ratio AnalysisKashish JainNo ratings yet

- Kpi 1713958219Document1 pageKpi 1713958219omji5177No ratings yet

- 50 Finance KPIsDocument1 page50 Finance KPIsDIPEN ASTIKNo ratings yet

- HO 4 - Telecoms - Industry - and - Operator - Benchmarks - by - Key - Financial - Metrics - 4Q13Document28 pagesHO 4 - Telecoms - Industry - and - Operator - Benchmarks - by - Key - Financial - Metrics - 4Q13Saud HidayatullahNo ratings yet

- Fatema NusratDocument10 pagesFatema NusratFatema NusratNo ratings yet

- Analysis of Financial StatementsDocument19 pagesAnalysis of Financial StatementsGautam MNo ratings yet

- Strategic Control Mechanism 1Document38 pagesStrategic Control Mechanism 1John Patrick Lazaro Andres80% (5)

- PM - Decision Making Techniques: Cost-Volume-Profit AnalysisDocument14 pagesPM - Decision Making Techniques: Cost-Volume-Profit AnalysisBhupendra SinghNo ratings yet

- CPA Review Notes 2019 - BEC (Business Environment Concepts)From EverandCPA Review Notes 2019 - BEC (Business Environment Concepts)Rating: 4 out of 5 stars4/5 (9)

- Y10 English Language Remote Learning 25.1.2021Document14 pagesY10 English Language Remote Learning 25.1.2021Elllie TattersNo ratings yet

- Y10 English Language Remote Learning 01.02.2021Document8 pagesY10 English Language Remote Learning 01.02.2021Elllie TattersNo ratings yet

- Y10 English Language Remote Learning 08.02.2021Document10 pagesY10 English Language Remote Learning 08.02.2021Elllie TattersNo ratings yet

- Y10 English Language Remote Learning 22.02.2021Document8 pagesY10 English Language Remote Learning 22.02.2021Elllie TattersNo ratings yet

- Y10 English Language Remote Learning 01.03.2021Document12 pagesY10 English Language Remote Learning 01.03.2021Elllie TattersNo ratings yet

- Application of Knowledge QuestionsDocument16 pagesApplication of Knowledge QuestionsElllie TattersNo ratings yet

- Blue Zone Higher Questions Lockdown WorkDocument7 pagesBlue Zone Higher Questions Lockdown WorkElllie TattersNo ratings yet

- Higher Exam QuestionsDocument7 pagesHigher Exam QuestionsElllie TattersNo ratings yet

- Component Characteristics Questions - Physics GCSEDocument10 pagesComponent Characteristics Questions - Physics GCSEElllie TattersNo ratings yet

- Economics of Money and BankingDocument196 pagesEconomics of Money and BankingDenisse Garza100% (3)

- Unit 4 - IAPMDocument17 pagesUnit 4 - IAPMPRAGASM PROGNo ratings yet

- Statement of Cash FlowsDocument12 pagesStatement of Cash Flowsnot funny didn't laughNo ratings yet

- Economics Preliminary SyllabusDocument3 pagesEconomics Preliminary Syllabusசுப.தமிழினியன்100% (2)

- Chapter 15 Test BankDocument31 pagesChapter 15 Test BankNadi HoodNo ratings yet

- Name: Nguyễn Hoàng Phương Linh - 10190547Document1 pageName: Nguyễn Hoàng Phương Linh - 10190547Linh Nguyễn Hoàng PhươngNo ratings yet

- Quiz 4 Fa ReviewerDocument3 pagesQuiz 4 Fa ReviewerKristine Jewel PacursaNo ratings yet

- Coca Cola Company Is A Global Soft Drink Beverage Company TickeDocument3 pagesCoca Cola Company Is A Global Soft Drink Beverage Company TickeAmit PandeyNo ratings yet

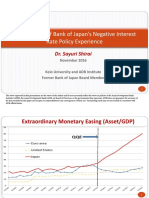

- An Overview of Bank of Japan Negative Interest Rate Policy ExperienceDocument12 pagesAn Overview of Bank of Japan Negative Interest Rate Policy ExperienceADBI Events100% (1)

- CH 6 13Document148 pagesCH 6 13林韋丞No ratings yet

- Project On Sbi Retail Banking by Vivek Kumar, DarbhangaDocument47 pagesProject On Sbi Retail Banking by Vivek Kumar, Darbhangavivekkumar883377% (30)

- Short Term Budgeting Lecture Notes 3 CompressDocument30 pagesShort Term Budgeting Lecture Notes 3 CompressGwyneth TorrefloresNo ratings yet

- The Asian Currency Crisis: A Case StudyDocument7 pagesThe Asian Currency Crisis: A Case StudyTantanLeNo ratings yet

- Cash Flow Statement Examples As Per Direct Method: Report Name Sap Report T-CodeDocument6 pagesCash Flow Statement Examples As Per Direct Method: Report Name Sap Report T-Codejainendra100% (1)

- 2468 - EstimDocument2 pages2468 - EstimTariq MahmoodNo ratings yet

- 9 Capital BudgetingDocument55 pages9 Capital BudgetingAlperen KaragozNo ratings yet

- Welete Weldu 1Document19 pagesWelete Weldu 1Kalayu KirosNo ratings yet

- Exercise 1-Use Built-In Functions: Sales May June July August Sum: Average: Min: Max: Today's DateDocument15 pagesExercise 1-Use Built-In Functions: Sales May June July August Sum: Average: Min: Max: Today's DateAmrit Pal SinghNo ratings yet

- Mengenal Bitcoin Dan Cryptocurrency by Taufik KurniawanDocument69 pagesMengenal Bitcoin Dan Cryptocurrency by Taufik KurniawanMuhamad Urip MauluddinNo ratings yet

- Instructors Manual/ Corporate Finance/ Ross, Westerfield, Jaffe & Kakani/ 8 Edition/ Special Indian Edition/ Mcgraw Hill /2009Document2 pagesInstructors Manual/ Corporate Finance/ Ross, Westerfield, Jaffe & Kakani/ 8 Edition/ Special Indian Edition/ Mcgraw Hill /2009Kunal Kumar100% (1)

- Analyzing A Bank's Financial Statements: by Hans WagnerDocument6 pagesAnalyzing A Bank's Financial Statements: by Hans WagnerMustafaNo ratings yet

- 10 Emh (FM)Document4 pages10 Emh (FM)Dayaan ANo ratings yet

- Reformulated Chatbot Framework: 1. Account ManagementDocument2 pagesReformulated Chatbot Framework: 1. Account Managementakash paulNo ratings yet

- Daftar 231 Fintech P2P Lending IDocument11 pagesDaftar 231 Fintech P2P Lending Irekky andryNo ratings yet