Download as xlsx, pdf, or txt

You might also like

- Eva H. Hanks, Michael E. Herz and Steven S. Nemerson - Elements of Law, 2nd EditionDocument519 pagesEva H. Hanks, Michael E. Herz and Steven S. Nemerson - Elements of Law, 2nd EditionTaegeun Kim100% (1)

- HO 2 - Qualified Audit ReportDocument3 pagesHO 2 - Qualified Audit ReportRheneir Mora100% (1)

- JFC Consolidated Financial Statements 2018 PDFDocument132 pagesJFC Consolidated Financial Statements 2018 PDFPHILLIP PACLEBNo ratings yet

- Audit Report AssignmentDocument2 pagesAudit Report AssignmentShafayet ShihabNo ratings yet

- Financial Statements For The Year 2019Document174 pagesFinancial Statements For The Year 2019MD. ISRAFIL PALASHNo ratings yet

- Audit ReportDocument30 pagesAudit Reportmiam67830No ratings yet

- Financial Statements 201819 PDFDocument133 pagesFinancial Statements 201819 PDFRobinsNo ratings yet

- Robi Axiata Limited: Report and Financial Statements As at and For The Year Ended 31 December 2019Document97 pagesRobi Axiata Limited: Report and Financial Statements As at and For The Year Ended 31 December 2019Anika hossainNo ratings yet

- Auditor' Report.Document8 pagesAuditor' Report.Johan GutierrezNo ratings yet

- Illustrative Audit OpinionDocument6 pagesIllustrative Audit OpinionCaleb NewquistNo ratings yet

- BWCL - 2020 Bestway Cement Limited - OpenDoors - PKDocument142 pagesBWCL - 2020 Bestway Cement Limited - OpenDoors - PKzainNo ratings yet

- LG Chem 2020 Contingent Financial StatementsDocument102 pagesLG Chem 2020 Contingent Financial StatementsAyushika SinghNo ratings yet

- Ashbourne Industries Audit OpinionDocument4 pagesAshbourne Industries Audit OpinionFanix Yostina DaelyNo ratings yet

- Optiva Inc. Q4 2021 Financial Statements FinalDocument63 pagesOptiva Inc. Q4 2021 Financial Statements FinaldivyaNo ratings yet

- LG Chem, LTD.: Separate Financial Statements and Internal Control Over Financial Reporting December 31, 2019 and 2018Document97 pagesLG Chem, LTD.: Separate Financial Statements and Internal Control Over Financial Reporting December 31, 2019 and 2018Ayushika SinghNo ratings yet

- Sleep Country Canada Holding IncDocument44 pagesSleep Country Canada Holding IncSunira PaudelNo ratings yet

- Chapter 29 Procedures and Reports On Special Purpose Audit EngagementsDocument30 pagesChapter 29 Procedures and Reports On Special Purpose Audit EngagementsClar Aaron BautistaNo ratings yet

- Singapore Standard On AuditingDocument14 pagesSingapore Standard On AuditingbabylovelylovelyNo ratings yet

- 2023 Con Quarter04 AllDocument87 pages2023 Con Quarter04 AllMohammad Hyder AliNo ratings yet

- Smc-Sec Form 17-A (04.17.2023) Part2-FinalDocument305 pagesSmc-Sec Form 17-A (04.17.2023) Part2-FinalRenneth Ena OdeNo ratings yet

- Audited ReportDocument36 pagesAudited ReportverdeepNo ratings yet

- Latest Sample Auditors ReportDocument5 pagesLatest Sample Auditors ReportABDUL REHMAN WARRIACHNo ratings yet

- Standalone Financial StatementsDocument68 pagesStandalone Financial StatementsMaaz ShamsherNo ratings yet

- 2022년 영문연결감사보고서Document92 pages2022년 영문연결감사보고서Thu HồngNo ratings yet

- Consolidated Financial Statements of Samsung Electronics Co., Ltd. and Its Subsidiaries Index To Financial StatementsDocument103 pagesConsolidated Financial Statements of Samsung Electronics Co., Ltd. and Its Subsidiaries Index To Financial StatementsAlen Vincent JosephNo ratings yet

- Dongyue Report 2023 + UpdateDocument85 pagesDongyue Report 2023 + UpdateRobert ManjoNo ratings yet

- Unqualified Audit Report SpecimenDocument1 pageUnqualified Audit Report SpecimenFahmida AkhterNo ratings yet

- Financial Statements PDFDocument79 pagesFinancial Statements PDFRahul Kumar PatelNo ratings yet

- Principals of Auditing CH 17 PowerpointDocument32 pagesPrincipals of Auditing CH 17 Powerpointl2thez100% (1)

- Pas 510Document10 pagesPas 510georbert abieraNo ratings yet

- 2021 Audit ReportDocument79 pages2021 Audit ReportvishalNo ratings yet

- ACC 3250 Milestone 1Document5 pagesACC 3250 Milestone 1Akhuetie IsraelNo ratings yet

- 2020 Bao Cao TCDocument93 pages2020 Bao Cao TChienys huynhNo ratings yet

- Year End Financial Statements PDFDocument38 pagesYear End Financial Statements PDFCasualKillaNo ratings yet

- Singapore Standard On AuditingDocument28 pagesSingapore Standard On AuditingbabylovelylovelyNo ratings yet

- Dino Polska Group 2019 Audit ReportDocument10 pagesDino Polska Group 2019 Audit ReportfiohdiohhodoNo ratings yet

- Natura 2016 AR Engl PDFDocument140 pagesNatura 2016 AR Engl PDFManuel CámacNo ratings yet

- Example New Auditors ReportDocument4 pagesExample New Auditors ReportHhaNo ratings yet

- Auditors Report StandaloneDocument12 pagesAuditors Report StandalonezendeexNo ratings yet

- 2021 June Tutorial Set Questions - AuditDocument10 pages2021 June Tutorial Set Questions - AuditakpanyapNo ratings yet

- Financial StatementsDocument198 pagesFinancial StatementsRK15 21100% (1)

- 7eleven 2021 AFSDocument99 pages7eleven 2021 AFSjessellejeanenot21No ratings yet

- 2964 0 2023-03-19 18-44-08 enDocument55 pages2964 0 2023-03-19 18-44-08 enabdullah.h.aloibiNo ratings yet

- February 12, 2021: Consolidated Financial Statements and NotesDocument77 pagesFebruary 12, 2021: Consolidated Financial Statements and NotesAnujaNo ratings yet

- Ch6 Audit ReportDocument26 pagesCh6 Audit Reportkitababekele26No ratings yet

- ISA 700 705 706 Audit Report UpdatedDocument28 pagesISA 700 705 706 Audit Report UpdatedAshraf Uz ZamanNo ratings yet

- Philippine Savings BankDocument120 pagesPhilippine Savings BankLyn RNo ratings yet

- Consolidated Financials 2020 21Document116 pagesConsolidated Financials 2020 21Tuhin SenNo ratings yet

- Substantive Test of LiabilitiesDocument42 pagesSubstantive Test of LiabilitiesAldrin John TungolNo ratings yet

- OriginalDocument136 pagesOriginalShifa NazNo ratings yet

- SESI 10 ch17 - External Auditing Function - LectureDocument109 pagesSESI 10 ch17 - External Auditing Function - LecturekimkimberlyNo ratings yet

- Unilever Financial StatementDocument77 pagesUnilever Financial StatementIrene CapilitanNo ratings yet

- JG Summit Annual - FS 2019 PDFDocument210 pagesJG Summit Annual - FS 2019 PDFZo ThelfNo ratings yet

- Reporte Auditoría PWC Kruk 2023Document8 pagesReporte Auditoría PWC Kruk 2023pablo.i.torradoNo ratings yet

- Module - 2 Auditor'S Report: Objectives of The AuditorDocument20 pagesModule - 2 Auditor'S Report: Objectives of The AuditorVijay KumarNo ratings yet

- To The Directors and Shareholders of Conay Company, Inc.: Independent Auditor'S ReportDocument3 pagesTo The Directors and Shareholders of Conay Company, Inc.: Independent Auditor'S Reporthanie vine lirayNo ratings yet

- A Comparison of Auditor's ReportsDocument4 pagesA Comparison of Auditor's ReportsErdene BolorNo ratings yet

- Grameenphone Accounts 2020Document62 pagesGrameenphone Accounts 2020JUNAYED AHMED RAFINNo ratings yet

- Financial Statements - 2Document199 pagesFinancial Statements - 2Liliana MNo ratings yet

- Financial Accounting - Want to Become Financial Accountant in 30 Days?From EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Rating: 3.5 out of 5 stars3.5/5 (2)

- Engagement Essentials: Preparation, Compilation, and Review of Financial StatementsFrom EverandEngagement Essentials: Preparation, Compilation, and Review of Financial StatementsNo ratings yet

- Final ITO 1984 FA 2018Document176 pagesFinal ITO 1984 FA 2018Sarowar AlamNo ratings yet

- Disclosure Checklist-Companies ActDocument7 pagesDisclosure Checklist-Companies ActSarowar AlamNo ratings yet

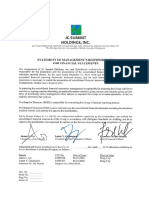

- Format of Management Representation LetterDocument6 pagesFormat of Management Representation LetterSarowar AlamNo ratings yet

- Financial Statements FormatDocument80 pagesFinancial Statements FormatSarowar AlamNo ratings yet

- Letter From Empower Oversight To U.S. Office of Special CounselDocument6 pagesLetter From Empower Oversight To U.S. Office of Special CounselThe FederalistNo ratings yet

- Environmental Law NotesDocument72 pagesEnvironmental Law NotesNenz Farouk100% (1)

- Suntex340 Awta 2023Document4 pagesSuntex340 Awta 2023MOHAMEDNo ratings yet

- Public Works Bill FormDocument4 pagesPublic Works Bill FormvoccubdNo ratings yet

- Letter To Tioga Borough Council President Frmo AG ShapiroDocument1 pageLetter To Tioga Borough Council President Frmo AG ShapiroCarl AldingerNo ratings yet

- 14 Yngson v. Philippine National BankDocument12 pages14 Yngson v. Philippine National Bank149890No ratings yet

- The Competition Commission of PakistanDocument10 pagesThe Competition Commission of Pakistanranag28No ratings yet

- Taxation 2nd PreboardDocument17 pagesTaxation 2nd PreboardJaneNo ratings yet

- 01 Quiz 1aDocument3 pages01 Quiz 1aJoffrey MellamaNo ratings yet

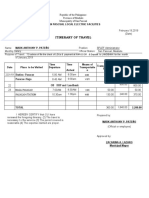

- Iterenary Travel FormDocument3 pagesIterenary Travel Formsplef lguNo ratings yet

- Traffic CountDocument32 pagesTraffic Countobrkh 07No ratings yet

- California Judicial Conduct Handbook Excerpt: David M. Rothman California Judges Association - California Commission On Judicial Performance - California Supreme CourtDocument24 pagesCalifornia Judicial Conduct Handbook Excerpt: David M. Rothman California Judges Association - California Commission On Judicial Performance - California Supreme CourtCalifornia Judicial Branch News Service - Investigative Reporting Source Material & Story Ideas100% (1)

- Week 1 Overview of Forensic Science PDFDocument6 pagesWeek 1 Overview of Forensic Science PDFShirsendu MondolNo ratings yet

- The Relationship Between School Regulations Awareness and Effective Management of Student Discipline in Secondary Schools in RwandaDocument49 pagesThe Relationship Between School Regulations Awareness and Effective Management of Student Discipline in Secondary Schools in RwandaRyan AustriaNo ratings yet

- Republic of The Philippines National Capital Judicial Region Regional Trial Court Manila, Branch 29Document7 pagesRepublic of The Philippines National Capital Judicial Region Regional Trial Court Manila, Branch 29Kaye RabadonNo ratings yet

- ALMANCO1Document2 pagesALMANCO1Diseños GarzotaNo ratings yet

- An Application For Restoration of A SuitDocument2 pagesAn Application For Restoration of A SuitSawda Ghojariya100% (1)

- Professional Ethics and Human Values Engineering As Social ExperimentationDocument11 pagesProfessional Ethics and Human Values Engineering As Social Experimentationceloso5409No ratings yet

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document2 pagesTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Sachin ChadhaNo ratings yet

- United States Court of Appeals, Third CircuitDocument1 pageUnited States Court of Appeals, Third CircuitScribd Government DocsNo ratings yet

- International Law Obligations On Climate Change Mitigation Benoit Mayer Full ChapterDocument67 pagesInternational Law Obligations On Climate Change Mitigation Benoit Mayer Full Chapterdixie.brewer931100% (7)

- McGhee V NCBDocument13 pagesMcGhee V NCBBernice Purugganan AresNo ratings yet

- Significance of International Organizations Have Enriched International LawDocument4 pagesSignificance of International Organizations Have Enriched International LawUtchas GaniNo ratings yet

- A Caricature Grievances Speech AquinoDocument39 pagesA Caricature Grievances Speech AquinoJessa CañadaNo ratings yet

- Research Paper Final Aditya MediaDocument76 pagesResearch Paper Final Aditya MediaAdityaSharma100% (1)

- KIIFB Manual of Business ProceduresDocument186 pagesKIIFB Manual of Business ProceduresSharat GopalNo ratings yet

- Bluebook (19th Ed.) Citation Format ExamplesDocument1 pageBluebook (19th Ed.) Citation Format ExamplesSweta Rao100% (1)

- SAM Tentative RulingDocument73 pagesSAM Tentative RulingJohn UllomNo ratings yet

- Res-020790.HTML Contract of ServicesDocument4 pagesRes-020790.HTML Contract of ServicesLala LanibaNo ratings yet