Incentives-GST Implications - Taxguru - in PDF

Incentives-GST Implications - Taxguru - in PDF

You might also like

- PFRS 15 Revenue From Contracts With CustomersDocument7 pagesPFRS 15 Revenue From Contracts With Customerspanda 1100% (2)

- Circuit City Accounting CaseDocument4 pagesCircuit City Accounting CasePookguyNo ratings yet

- VAT CONFIGURATION For SADocument28 pagesVAT CONFIGURATION For SAMohammed Nawaz Shariff100% (1)

- Discounts Incentives GST ImplicationsDocument12 pagesDiscounts Incentives GST ImplicationsVrajesh PatelNo ratings yet

- Treatment of Discounts Offers Free Samples in GSTDocument5 pagesTreatment of Discounts Offers Free Samples in GSTnaren.invincible244No ratings yet

- LB Decision in Aggarwal Color Case On Notification No. 12/2003-An AnalysisDocument5 pagesLB Decision in Aggarwal Color Case On Notification No. 12/2003-An AnalysisShrenikNo ratings yet

- Tax IshritaDocument15 pagesTax IshritaManeesh ReddyNo ratings yet

- Various Issues Relating To Works ContractDocument5 pagesVarious Issues Relating To Works ContractApoorvnujsNo ratings yet

- Chapter 6 ValueofTaxableSupplyDocument21 pagesChapter 6 ValueofTaxableSupplyDR. PREETI JINDALNo ratings yet

- Article On Supplementary Invoices Under GST Dated March 25 - 2019Document2 pagesArticle On Supplementary Invoices Under GST Dated March 25 - 2019deepak kumarNJNo ratings yet

- Aa 3 Mo-Chc-VagraDocument4 pagesAa 3 Mo-Chc-Vagraomkar daveNo ratings yet

- Revenue Revisited: Student Accountant Hub PageDocument4 pagesRevenue Revisited: Student Accountant Hub PageNozimanga ChiroroNo ratings yet

- IFRS 15-1 Five Steps ModelDocument59 pagesIFRS 15-1 Five Steps ModelJIAYING LIUNo ratings yet

- GeM - Terms & ConditionsDocument6 pagesGeM - Terms & ConditionsPriyankaNo ratings yet

- GST Impact On Free Issues and Samples ArticleDocument4 pagesGST Impact On Free Issues and Samples ArticleKantiSutharNo ratings yet

- Corporate Reporting Homework (Day 1)Document9 pagesCorporate Reporting Homework (Day 1)Sara MirchevskaNo ratings yet

- TMP 10202-Decoding The Draft GST Law-Impact On The Pharma Sector170599877Document7 pagesTMP 10202-Decoding The Draft GST Law-Impact On The Pharma Sector170599877mad13boyNo ratings yet

- PFRS 15 Summary NotesDocument4 pagesPFRS 15 Summary NotesDaniel Nichole MerindoNo ratings yet

- Revenue Revisited: The Global Body For Professional AccountantsDocument3 pagesRevenue Revisited: The Global Body For Professional AccountantsPANTUGNo ratings yet

- Vendor AgreementDocument10 pagesVendor AgreementyhNo ratings yet

- IFRS 15 Revenue From Contracts With CustomersDocument5 pagesIFRS 15 Revenue From Contracts With CustomersADEYANJU AKEEMNo ratings yet

- Making Sense of A Complex WorldDocument16 pagesMaking Sense of A Complex WorldciaranharronNo ratings yet

- Supply GSTDocument4 pagesSupply GSTnavoditakm04No ratings yet

- Pfrs 15 Summary NotesDocument5 pagesPfrs 15 Summary NotesSHARON SAMSONNo ratings yet

- Latest Updates in Indirect Tax Law For May 2015 Exams A. Central ExciseDocument21 pagesLatest Updates in Indirect Tax Law For May 2015 Exams A. Central Excisesivanpillai ganesanNo ratings yet

- The Company FinalDocument6 pagesThe Company FinalMavambu JuniorNo ratings yet

- IFRSDocument8 pagesIFRSrahulhsharmaNo ratings yet

- Chapter 1. Overview of Service Tax: Constitutional Validity and ConceptsDocument38 pagesChapter 1. Overview of Service Tax: Constitutional Validity and ConceptsPrateek UpadhyayNo ratings yet

- Value of SupplyDocument16 pagesValue of Supplyhariom bajpaiNo ratings yet

- TCS Refund Under GST - A Navigation Through Its Impact On E-Commerce and Other BusinessesDocument9 pagesTCS Refund Under GST - A Navigation Through Its Impact On E-Commerce and Other BusinessesMohammed SadiqhNo ratings yet

- Module 1 - PDFDocument4 pagesModule 1 - PDFMelanie SamsonaNo ratings yet

- RCM On Renting of Motor Vehicle Under GST - Taxguru - inDocument3 pagesRCM On Renting of Motor Vehicle Under GST - Taxguru - invneha0707No ratings yet

- Tax Refund On Rescinded Contracts - RSC 4 12 17Document3 pagesTax Refund On Rescinded Contracts - RSC 4 12 17Mikee Baliguat TanNo ratings yet

- Tax ProjectDocument7 pagesTax Projectipant2884No ratings yet

- Confirm Vat Audit ProjectDocument33 pagesConfirm Vat Audit ProjectkennyajayNo ratings yet

- RCM ChargesDocument9 pagesRCM Chargesnallarahul86No ratings yet

- Acca Ifrs 15Document19 pagesAcca Ifrs 15Ittihadul islamNo ratings yet

- GST CircularDocument5 pagesGST Circularanju shuklaNo ratings yet

- Transfer PricingDocument111 pagesTransfer PricingMamun0% (1)

- Vat Audit by Chetan SarafDocument33 pagesVat Audit by Chetan Sarafchetan saraf100% (1)

- Value of SupplyDocument5 pagesValue of SupplyMohanNo ratings yet

- Compliance Barriers On The Road To GST An Analysis of Model GST LawDocument6 pagesCompliance Barriers On The Road To GST An Analysis of Model GST LawTaxmann PublicationNo ratings yet

- Circular 92 ExplainedDocument2 pagesCircular 92 ExplainedaekurnoolNo ratings yet

- Iv Sem Tax ProjDocument9 pagesIv Sem Tax ProjVagisha SharmaNo ratings yet

- Morgan Stanley Case LawDocument2 pagesMorgan Stanley Case LawakshNo ratings yet

- Transfer Pricing CasesDocument6 pagesTransfer Pricing CasesShreya SinghNo ratings yet

- ISD Vs Cross Charge The Saga Continues 1693273129Document3 pagesISD Vs Cross Charge The Saga Continues 1693273129onkar_gnlu8745No ratings yet

- 3A2013s2WK5 - RevenueDocument8 pages3A2013s2WK5 - RevenueAngela AuNo ratings yet

- The Regalia Group Corporation: BIR RULING (DA-295-08)Document4 pagesThe Regalia Group Corporation: BIR RULING (DA-295-08)Johnallen MarillaNo ratings yet

- A Global Guide To M&A - India: by Vivek Gupta and Rohit BerryDocument14 pagesA Global Guide To M&A - India: by Vivek Gupta and Rohit BerryvinaymathewNo ratings yet

- Judicial Snippets: /idt /service TaxDocument4 pagesJudicial Snippets: /idt /service Taxswami_ratanNo ratings yet

- IFRS 15 Revenue From Contracts With Customers-2Document8 pagesIFRS 15 Revenue From Contracts With Customers-2abbyNo ratings yet

- Ifrs 15: Revenue From Contracts With CustomersDocument8 pagesIfrs 15: Revenue From Contracts With CustomersAira Nhaira MecateNo ratings yet

- The New Revenue Recognition Rules: What Is The Impact For Franchisors?Document25 pagesThe New Revenue Recognition Rules: What Is The Impact For Franchisors?Tag SenNo ratings yet

- Cir Vs San Roque PowerDocument3 pagesCir Vs San Roque PowerHa MisNo ratings yet

- IFRS 15 (IAS) - Revenue From Contracts With CustomersDocument10 pagesIFRS 15 (IAS) - Revenue From Contracts With CustomersAngie MagnayeNo ratings yet

- 28548vol3stvatcp14 PDFDocument5 pages28548vol3stvatcp14 PDFNaveed AnsariNo ratings yet

- Jagran Prakashan (All HC)Document38 pagesJagran Prakashan (All HC)Priyank GalaNo ratings yet

- MFRS 15 Implementation Issues and Challenges in For The Construction, TelecommunDocument6 pagesMFRS 15 Implementation Issues and Challenges in For The Construction, TelecommunNik RubiahNo ratings yet

- Judgments On Input Tax CreditDocument3 pagesJudgments On Input Tax CreditANUJ VISHWAKARMANo ratings yet

- Consumer Protection in India: A brief Guide on the Subject along with the Specimen form of a ComplaintFrom EverandConsumer Protection in India: A brief Guide on the Subject along with the Specimen form of a ComplaintNo ratings yet

- ANPC v. BIR and CIR v. PAGCORDocument2 pagesANPC v. BIR and CIR v. PAGCORDerek C. Egalla100% (2)

- GST Aftab 2.0Document76 pagesGST Aftab 2.0AFTAB PIRJADENo ratings yet

- Taxation of Electricity in India: Prepared by Abhay Kumar Singh 16SBSBA11046 BBA Sem-5 Under Guidance-Hetal UpadhayaDocument17 pagesTaxation of Electricity in India: Prepared by Abhay Kumar Singh 16SBSBA11046 BBA Sem-5 Under Guidance-Hetal UpadhayaKRUPALI RAIYANINo ratings yet

- Curriculum Vitae: Sonal Sujay Patil. 4/2, Yashoda Kunj, Mohili Village, Pipeline Sakinaka, Mumbai-400072. ObjectiveDocument4 pagesCurriculum Vitae: Sonal Sujay Patil. 4/2, Yashoda Kunj, Mohili Village, Pipeline Sakinaka, Mumbai-400072. ObjectiveGayatri GowdaNo ratings yet

- Draft Invoice Cyprus LLC MigrationDocument7 pagesDraft Invoice Cyprus LLC MigrationShehryar KhanNo ratings yet

- In Partial Fulfilment For The Award of The Degree ofDocument15 pagesIn Partial Fulfilment For The Award of The Degree ofnithyaNo ratings yet

- Proposed Tax Changes Under The Finance Bill 2022 ALN Kenya Legal Alert April 2022Document24 pagesProposed Tax Changes Under The Finance Bill 2022 ALN Kenya Legal Alert April 2022yomak94018No ratings yet

- Tender Document - 1 - 2 - 3 PDFDocument60 pagesTender Document - 1 - 2 - 3 PDFsunikesh shuklaNo ratings yet

- RR No. 8-2018Document27 pagesRR No. 8-2018deltsen100% (1)

- Bottled Water Market in MexicoDocument18 pagesBottled Water Market in MexicofuentenaturaNo ratings yet

- Chapter OneDocument48 pagesChapter OneChigozieNo ratings yet

- Invoice 40 Palmeto MulesoftDocument6 pagesInvoice 40 Palmeto MulesoftSrinivasa HelavarNo ratings yet

- VAT RulesDocument11 pagesVAT RulesamrkiplNo ratings yet

- Intl FormsDocument3 pagesIntl FormsRS ENTERPRISESNo ratings yet

- Guide To Publishing ContractsDocument17 pagesGuide To Publishing ContractsreadalotbutnowisdomyetNo ratings yet

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Syed SameerNo ratings yet

- Comparative Analysis Real Estate MEX USDocument40 pagesComparative Analysis Real Estate MEX USquijote82No ratings yet

- Maharashtra Value Added Tax Act 2Document27 pagesMaharashtra Value Added Tax Act 2Minal ShethNo ratings yet

- Place of Supply of Goods or Services or BothDocument38 pagesPlace of Supply of Goods or Services or BothHarshit GuptaNo ratings yet

- Liyu - 2021 G.CDocument8 pagesLiyu - 2021 G.CElias Abubeker AhmedNo ratings yet

- Finance Act 2020:: Key Changes and ImplicationsDocument5 pagesFinance Act 2020:: Key Changes and ImplicationsAdebayo Yusuff AdesholaNo ratings yet

- Taxation Cases On Remedies (1) DigestDocument77 pagesTaxation Cases On Remedies (1) DigestGuiller MagsumbolNo ratings yet

- B. O Q For BuildingDocument37 pagesB. O Q For Buildingalinaitwe shalifuNo ratings yet

- IM ACCO 20173 Business and Transfer Taxes Module 5 PDFDocument5 pagesIM ACCO 20173 Business and Transfer Taxes Module 5 PDFMakoy BixenmanNo ratings yet

- Rural and Urban DevelopmentDocument14 pagesRural and Urban DevelopmentChatleen Pagulayan TumanguilNo ratings yet

- FAR 100 Merchandising Quiz Answer KeyDocument4 pagesFAR 100 Merchandising Quiz Answer KeyclaudellerosetteNo ratings yet

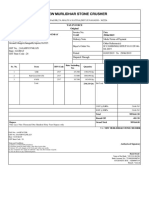

- New Murlidhar Stone Crusher: Tax Invoice OriginalDocument1 pageNew Murlidhar Stone Crusher: Tax Invoice OriginalrajendranrajendranNo ratings yet

- 04-Duty Free Phils. v. Bureau of Internal Revenue. GR No 197228Document6 pages04-Duty Free Phils. v. Bureau of Internal Revenue. GR No 197228ryanmeinNo ratings yet

- S.No Procedure NAMEDocument22 pagesS.No Procedure NAMEMithun NNo ratings yet

Download as pdf or txt

You might also like

- PFRS 15 Revenue From Contracts With CustomersDocument7 pagesPFRS 15 Revenue From Contracts With Customerspanda 1100% (2)

- Circuit City Accounting CaseDocument4 pagesCircuit City Accounting CasePookguyNo ratings yet

- VAT CONFIGURATION For SADocument28 pagesVAT CONFIGURATION For SAMohammed Nawaz Shariff100% (1)

- Discounts Incentives GST ImplicationsDocument12 pagesDiscounts Incentives GST ImplicationsVrajesh PatelNo ratings yet

- Treatment of Discounts Offers Free Samples in GSTDocument5 pagesTreatment of Discounts Offers Free Samples in GSTnaren.invincible244No ratings yet

- LB Decision in Aggarwal Color Case On Notification No. 12/2003-An AnalysisDocument5 pagesLB Decision in Aggarwal Color Case On Notification No. 12/2003-An AnalysisShrenikNo ratings yet

- Tax IshritaDocument15 pagesTax IshritaManeesh ReddyNo ratings yet

- Various Issues Relating To Works ContractDocument5 pagesVarious Issues Relating To Works ContractApoorvnujsNo ratings yet

- Chapter 6 ValueofTaxableSupplyDocument21 pagesChapter 6 ValueofTaxableSupplyDR. PREETI JINDALNo ratings yet

- Article On Supplementary Invoices Under GST Dated March 25 - 2019Document2 pagesArticle On Supplementary Invoices Under GST Dated March 25 - 2019deepak kumarNJNo ratings yet

- Aa 3 Mo-Chc-VagraDocument4 pagesAa 3 Mo-Chc-Vagraomkar daveNo ratings yet

- Revenue Revisited: Student Accountant Hub PageDocument4 pagesRevenue Revisited: Student Accountant Hub PageNozimanga ChiroroNo ratings yet

- IFRS 15-1 Five Steps ModelDocument59 pagesIFRS 15-1 Five Steps ModelJIAYING LIUNo ratings yet

- GeM - Terms & ConditionsDocument6 pagesGeM - Terms & ConditionsPriyankaNo ratings yet

- GST Impact On Free Issues and Samples ArticleDocument4 pagesGST Impact On Free Issues and Samples ArticleKantiSutharNo ratings yet

- Corporate Reporting Homework (Day 1)Document9 pagesCorporate Reporting Homework (Day 1)Sara MirchevskaNo ratings yet

- TMP 10202-Decoding The Draft GST Law-Impact On The Pharma Sector170599877Document7 pagesTMP 10202-Decoding The Draft GST Law-Impact On The Pharma Sector170599877mad13boyNo ratings yet

- PFRS 15 Summary NotesDocument4 pagesPFRS 15 Summary NotesDaniel Nichole MerindoNo ratings yet

- Revenue Revisited: The Global Body For Professional AccountantsDocument3 pagesRevenue Revisited: The Global Body For Professional AccountantsPANTUGNo ratings yet

- Vendor AgreementDocument10 pagesVendor AgreementyhNo ratings yet

- IFRS 15 Revenue From Contracts With CustomersDocument5 pagesIFRS 15 Revenue From Contracts With CustomersADEYANJU AKEEMNo ratings yet

- Making Sense of A Complex WorldDocument16 pagesMaking Sense of A Complex WorldciaranharronNo ratings yet

- Supply GSTDocument4 pagesSupply GSTnavoditakm04No ratings yet

- Pfrs 15 Summary NotesDocument5 pagesPfrs 15 Summary NotesSHARON SAMSONNo ratings yet

- Latest Updates in Indirect Tax Law For May 2015 Exams A. Central ExciseDocument21 pagesLatest Updates in Indirect Tax Law For May 2015 Exams A. Central Excisesivanpillai ganesanNo ratings yet

- The Company FinalDocument6 pagesThe Company FinalMavambu JuniorNo ratings yet

- IFRSDocument8 pagesIFRSrahulhsharmaNo ratings yet

- Chapter 1. Overview of Service Tax: Constitutional Validity and ConceptsDocument38 pagesChapter 1. Overview of Service Tax: Constitutional Validity and ConceptsPrateek UpadhyayNo ratings yet

- Value of SupplyDocument16 pagesValue of Supplyhariom bajpaiNo ratings yet

- TCS Refund Under GST - A Navigation Through Its Impact On E-Commerce and Other BusinessesDocument9 pagesTCS Refund Under GST - A Navigation Through Its Impact On E-Commerce and Other BusinessesMohammed SadiqhNo ratings yet

- Module 1 - PDFDocument4 pagesModule 1 - PDFMelanie SamsonaNo ratings yet

- RCM On Renting of Motor Vehicle Under GST - Taxguru - inDocument3 pagesRCM On Renting of Motor Vehicle Under GST - Taxguru - invneha0707No ratings yet

- Tax Refund On Rescinded Contracts - RSC 4 12 17Document3 pagesTax Refund On Rescinded Contracts - RSC 4 12 17Mikee Baliguat TanNo ratings yet

- Tax ProjectDocument7 pagesTax Projectipant2884No ratings yet

- Confirm Vat Audit ProjectDocument33 pagesConfirm Vat Audit ProjectkennyajayNo ratings yet

- RCM ChargesDocument9 pagesRCM Chargesnallarahul86No ratings yet

- Acca Ifrs 15Document19 pagesAcca Ifrs 15Ittihadul islamNo ratings yet

- GST CircularDocument5 pagesGST Circularanju shuklaNo ratings yet

- Transfer PricingDocument111 pagesTransfer PricingMamun0% (1)

- Vat Audit by Chetan SarafDocument33 pagesVat Audit by Chetan Sarafchetan saraf100% (1)

- Value of SupplyDocument5 pagesValue of SupplyMohanNo ratings yet

- Compliance Barriers On The Road To GST An Analysis of Model GST LawDocument6 pagesCompliance Barriers On The Road To GST An Analysis of Model GST LawTaxmann PublicationNo ratings yet

- Circular 92 ExplainedDocument2 pagesCircular 92 ExplainedaekurnoolNo ratings yet

- Iv Sem Tax ProjDocument9 pagesIv Sem Tax ProjVagisha SharmaNo ratings yet

- Morgan Stanley Case LawDocument2 pagesMorgan Stanley Case LawakshNo ratings yet

- Transfer Pricing CasesDocument6 pagesTransfer Pricing CasesShreya SinghNo ratings yet

- ISD Vs Cross Charge The Saga Continues 1693273129Document3 pagesISD Vs Cross Charge The Saga Continues 1693273129onkar_gnlu8745No ratings yet

- 3A2013s2WK5 - RevenueDocument8 pages3A2013s2WK5 - RevenueAngela AuNo ratings yet

- The Regalia Group Corporation: BIR RULING (DA-295-08)Document4 pagesThe Regalia Group Corporation: BIR RULING (DA-295-08)Johnallen MarillaNo ratings yet

- A Global Guide To M&A - India: by Vivek Gupta and Rohit BerryDocument14 pagesA Global Guide To M&A - India: by Vivek Gupta and Rohit BerryvinaymathewNo ratings yet

- Judicial Snippets: /idt /service TaxDocument4 pagesJudicial Snippets: /idt /service Taxswami_ratanNo ratings yet

- IFRS 15 Revenue From Contracts With Customers-2Document8 pagesIFRS 15 Revenue From Contracts With Customers-2abbyNo ratings yet

- Ifrs 15: Revenue From Contracts With CustomersDocument8 pagesIfrs 15: Revenue From Contracts With CustomersAira Nhaira MecateNo ratings yet

- The New Revenue Recognition Rules: What Is The Impact For Franchisors?Document25 pagesThe New Revenue Recognition Rules: What Is The Impact For Franchisors?Tag SenNo ratings yet

- Cir Vs San Roque PowerDocument3 pagesCir Vs San Roque PowerHa MisNo ratings yet

- IFRS 15 (IAS) - Revenue From Contracts With CustomersDocument10 pagesIFRS 15 (IAS) - Revenue From Contracts With CustomersAngie MagnayeNo ratings yet

- 28548vol3stvatcp14 PDFDocument5 pages28548vol3stvatcp14 PDFNaveed AnsariNo ratings yet

- Jagran Prakashan (All HC)Document38 pagesJagran Prakashan (All HC)Priyank GalaNo ratings yet

- MFRS 15 Implementation Issues and Challenges in For The Construction, TelecommunDocument6 pagesMFRS 15 Implementation Issues and Challenges in For The Construction, TelecommunNik RubiahNo ratings yet

- Judgments On Input Tax CreditDocument3 pagesJudgments On Input Tax CreditANUJ VISHWAKARMANo ratings yet

- Consumer Protection in India: A brief Guide on the Subject along with the Specimen form of a ComplaintFrom EverandConsumer Protection in India: A brief Guide on the Subject along with the Specimen form of a ComplaintNo ratings yet

- ANPC v. BIR and CIR v. PAGCORDocument2 pagesANPC v. BIR and CIR v. PAGCORDerek C. Egalla100% (2)

- GST Aftab 2.0Document76 pagesGST Aftab 2.0AFTAB PIRJADENo ratings yet

- Taxation of Electricity in India: Prepared by Abhay Kumar Singh 16SBSBA11046 BBA Sem-5 Under Guidance-Hetal UpadhayaDocument17 pagesTaxation of Electricity in India: Prepared by Abhay Kumar Singh 16SBSBA11046 BBA Sem-5 Under Guidance-Hetal UpadhayaKRUPALI RAIYANINo ratings yet

- Curriculum Vitae: Sonal Sujay Patil. 4/2, Yashoda Kunj, Mohili Village, Pipeline Sakinaka, Mumbai-400072. ObjectiveDocument4 pagesCurriculum Vitae: Sonal Sujay Patil. 4/2, Yashoda Kunj, Mohili Village, Pipeline Sakinaka, Mumbai-400072. ObjectiveGayatri GowdaNo ratings yet

- Draft Invoice Cyprus LLC MigrationDocument7 pagesDraft Invoice Cyprus LLC MigrationShehryar KhanNo ratings yet

- In Partial Fulfilment For The Award of The Degree ofDocument15 pagesIn Partial Fulfilment For The Award of The Degree ofnithyaNo ratings yet

- Proposed Tax Changes Under The Finance Bill 2022 ALN Kenya Legal Alert April 2022Document24 pagesProposed Tax Changes Under The Finance Bill 2022 ALN Kenya Legal Alert April 2022yomak94018No ratings yet

- Tender Document - 1 - 2 - 3 PDFDocument60 pagesTender Document - 1 - 2 - 3 PDFsunikesh shuklaNo ratings yet

- RR No. 8-2018Document27 pagesRR No. 8-2018deltsen100% (1)

- Bottled Water Market in MexicoDocument18 pagesBottled Water Market in MexicofuentenaturaNo ratings yet

- Chapter OneDocument48 pagesChapter OneChigozieNo ratings yet

- Invoice 40 Palmeto MulesoftDocument6 pagesInvoice 40 Palmeto MulesoftSrinivasa HelavarNo ratings yet

- VAT RulesDocument11 pagesVAT RulesamrkiplNo ratings yet

- Intl FormsDocument3 pagesIntl FormsRS ENTERPRISESNo ratings yet

- Guide To Publishing ContractsDocument17 pagesGuide To Publishing ContractsreadalotbutnowisdomyetNo ratings yet

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Syed SameerNo ratings yet

- Comparative Analysis Real Estate MEX USDocument40 pagesComparative Analysis Real Estate MEX USquijote82No ratings yet

- Maharashtra Value Added Tax Act 2Document27 pagesMaharashtra Value Added Tax Act 2Minal ShethNo ratings yet

- Place of Supply of Goods or Services or BothDocument38 pagesPlace of Supply of Goods or Services or BothHarshit GuptaNo ratings yet

- Liyu - 2021 G.CDocument8 pagesLiyu - 2021 G.CElias Abubeker AhmedNo ratings yet

- Finance Act 2020:: Key Changes and ImplicationsDocument5 pagesFinance Act 2020:: Key Changes and ImplicationsAdebayo Yusuff AdesholaNo ratings yet

- Taxation Cases On Remedies (1) DigestDocument77 pagesTaxation Cases On Remedies (1) DigestGuiller MagsumbolNo ratings yet

- B. O Q For BuildingDocument37 pagesB. O Q For Buildingalinaitwe shalifuNo ratings yet

- IM ACCO 20173 Business and Transfer Taxes Module 5 PDFDocument5 pagesIM ACCO 20173 Business and Transfer Taxes Module 5 PDFMakoy BixenmanNo ratings yet

- Rural and Urban DevelopmentDocument14 pagesRural and Urban DevelopmentChatleen Pagulayan TumanguilNo ratings yet

- FAR 100 Merchandising Quiz Answer KeyDocument4 pagesFAR 100 Merchandising Quiz Answer KeyclaudellerosetteNo ratings yet

- New Murlidhar Stone Crusher: Tax Invoice OriginalDocument1 pageNew Murlidhar Stone Crusher: Tax Invoice OriginalrajendranrajendranNo ratings yet

- 04-Duty Free Phils. v. Bureau of Internal Revenue. GR No 197228Document6 pages04-Duty Free Phils. v. Bureau of Internal Revenue. GR No 197228ryanmeinNo ratings yet

- S.No Procedure NAMEDocument22 pagesS.No Procedure NAMEMithun NNo ratings yet