Download as pdf or txt

You might also like

- Mid-Term Exam: Professor: Kevin Petit-Frère Duration: 180 MinutesDocument7 pagesMid-Term Exam: Professor: Kevin Petit-Frère Duration: 180 MinutesAbby Hacther0% (2)

- AssigmentDocument8 pagesAssigmentMuhammad Rafique0% (1)

- (2008 Pattern) PDFDocument231 pages(2008 Pattern) PDFKundan DeoreNo ratings yet

- CA Inter Accounting Full Test 1 Nov 2022 Unscheduled Test PaperDocument18 pagesCA Inter Accounting Full Test 1 Nov 2022 Unscheduled Test Papersinku123No ratings yet

- MA - S2023 (4519201) (GTURanker - Com)Document4 pagesMA - S2023 (4519201) (GTURanker - Com)Sourav SinhaNo ratings yet

- IGNOU MBA Solved Assignments 2018Document26 pagesIGNOU MBA Solved Assignments 2018Dharmendra Singh SikarwarNo ratings yet

- AssignmentsDocument7 pagesAssignmentspratikshakurhade04No ratings yet

- Ita MockDocument8 pagesIta MockAyyan SheikhNo ratings yet

- Financial AccountingDocument3 pagesFinancial AccountingSimran MittalNo ratings yet

- MTP 2 AccountsDocument8 pagesMTP 2 AccountssuzalaggarwalllNo ratings yet

- Fa 10092023Document7 pagesFa 10092023Vaibhav SinghNo ratings yet

- Q.P. Code: 62202: Managerial AccountingDocument6 pagesQ.P. Code: 62202: Managerial Accountinganshul bhutangeNo ratings yet

- Moderator: Mr. L.J. Muthivhi (CA), SADocument11 pagesModerator: Mr. L.J. Muthivhi (CA), SANhlanhla MsizaNo ratings yet

- 78735bos63031 p6Document44 pages78735bos63031 p6dileepkarumuri93No ratings yet

- Gujarat Technological UniversityDocument3 pagesGujarat Technological UniversityMehul VarmaNo ratings yet

- CA Inter FM SM RTP May 2024 Castudynotes ComDocument44 pagesCA Inter FM SM RTP May 2024 Castudynotes ComGeo P BNo ratings yet

- Ignou Mba Solved Assignments For January 2018Document28 pagesIgnou Mba Solved Assignments For January 2018Dharmendra Singh SikarwarNo ratings yet

- 202 - FM Question PaperDocument5 pages202 - FM Question Papersumedh narwadeNo ratings yet

- CH18601 FM - II Model PaperDocument5 pagesCH18601 FM - II Model PaperKarthikNo ratings yet

- Output PDFDocument81 pagesOutput PDFPravin ThoratNo ratings yet

- BComDocument3 pagesBComChristy jamesNo ratings yet

- ECON F315 - FIN F315 - Compre QP PDFDocument3 pagesECON F315 - FIN F315 - Compre QP PDFPrabhjeet Kalsi100% (1)

- CAF 1 FAR1 Spring 2023Document6 pagesCAF 1 FAR1 Spring 2023haris khanNo ratings yet

- Attempt Any Four Questions. All Questions Carry Equal MarksDocument47 pagesAttempt Any Four Questions. All Questions Carry Equal MarksAbhishek GwalNo ratings yet

- Advanced Financial ManagementDocument12 pagesAdvanced Financial Managementnitin bajajNo ratings yet

- ACC2143ACC2543 Test 1 2023Document9 pagesACC2143ACC2543 Test 1 2023kamichidorahNo ratings yet

- Far670 - July 2021 - QuestionDocument4 pagesFar670 - July 2021 - QuestionnurulsyafiqahNo ratings yet

- Final Exam FM Summer 2021Document2 pagesFinal Exam FM Summer 2021AAYAN FARAZNo ratings yet

- Working Capital NumericalsDocument3 pagesWorking Capital NumericalsShriya SajeevNo ratings yet

- 15 Af 503 sfm61Document4 pages15 Af 503 sfm61magnetbox8No ratings yet

- Financial Accounting and Reporting-IDocument6 pagesFinancial Accounting and Reporting-INafay Bin ZubairNo ratings yet

- FMECO M.test HM Question 17.03.2022Document5 pagesFMECO M.test HM Question 17.03.2022sahroshan891No ratings yet

- Instructions To CandidatesDocument3 pagesInstructions To CandidatesSchoTestNo ratings yet

- MS 4Document3 pagesMS 4jaskiranNo ratings yet

- Adobe Scan 24-Jun-2024Document5 pagesAdobe Scan 24-Jun-2024trishala sharmaNo ratings yet

- Financial AccountingDocument2 pagesFinancial AccountingKartik GurmuleNo ratings yet

- Rajdhani College FM Assignment FinalDocument6 pagesRajdhani College FM Assignment Finalayushkorea52629No ratings yet

- Test Series: April, 2021 Mock Test Paper 2 Intermediate (New) : Group - I Paper - 1: AccountingDocument7 pagesTest Series: April, 2021 Mock Test Paper 2 Intermediate (New) : Group - I Paper - 1: AccountingHarsh KumarNo ratings yet

- Quarter Test 2 QPDocument7 pagesQuarter Test 2 QPOmair HasanNo ratings yet

- Cost Management Accounting Full Test 1 Nov 2023 Test Paper 1689158389Document17 pagesCost Management Accounting Full Test 1 Nov 2023 Test Paper 1689158389ahanaghosal2022No ratings yet

- MB20202 CF Unit V Working Capital Management Application QuestionsDocument4 pagesMB20202 CF Unit V Working Capital Management Application QuestionsSarath kumar CNo ratings yet

- Financial ManagementDocument3 pagesFinancial Managementakshaymatey007No ratings yet

- Indian Institute of TechnologyDocument8 pagesIndian Institute of TechnologySohini RoyNo ratings yet

- 402 - Corporate Financial ManagementDocument2 pages402 - Corporate Financial Managementmahmudhasan5051No ratings yet

- 8) FM EcoDocument19 pages8) FM EcoKrushna MateNo ratings yet

- Assignment: Advanced Financial Management and Policy Code: MCCC 204 UPC 324101204Document2 pagesAssignment: Advanced Financial Management and Policy Code: MCCC 204 UPC 324101204Ramesh Chand GuptaNo ratings yet

- MA - W2022 (4519201) (GTURanker - Com)Document3 pagesMA - W2022 (4519201) (GTURanker - Com)Sourav SinhaNo ratings yet

- Mba Ii Sem. Prelim Exam SUBJECT: Financial Management: Roll NoDocument4 pagesMba Ii Sem. Prelim Exam SUBJECT: Financial Management: Roll NoAkash raiNo ratings yet

- (4870) - 2002 M.B.A. 202: Financial Management (CBCS) (2013 Pattern) (Semester - II)Document5 pages(4870) - 2002 M.B.A. 202: Financial Management (CBCS) (2013 Pattern) (Semester - II)AK Aru ShettyNo ratings yet

- Caf-8 Cma PDFDocument5 pagesCaf-8 Cma PDFMuqtasid AhmedNo ratings yet

- First Semester Mba IdeDocument7 pagesFirst Semester Mba IdeJayaraj JayachandranNo ratings yet

- New 1st Semester English (MCO-01,04,05,21) M.com AssignmentDocument8 pagesNew 1st Semester English (MCO-01,04,05,21) M.com AssignmentRajni KumariNo ratings yet

- 2 Financial Accounting ReportingDocument5 pages2 Financial Accounting ReportingBizness Zenius HantNo ratings yet

- Cost and Management AccountingDocument6 pagesCost and Management AccountingAli HaiderNo ratings yet

- Acc3204 - Jan2018Document5 pagesAcc3204 - Jan2018natlyhNo ratings yet

- RE Exam FA Sem I MFM MMM MHRDMDocument4 pagesRE Exam FA Sem I MFM MMM MHRDMPARAM CLOTHINGNo ratings yet

- Management Accounting (Acct 321) P2 PT 2ND Trimester 2017Document5 pagesManagement Accounting (Acct 321) P2 PT 2ND Trimester 2017Nodeh Deh SpartaNo ratings yet

- Class 11 Acc FinalDocument3 pagesClass 11 Acc Finalmnmehta1990No ratings yet

- Cost Accounting (781) Sample Question Paper Class XII 2018-19Document5 pagesCost Accounting (781) Sample Question Paper Class XII 2018-19Saif HasanNo ratings yet

- Innovative Infrastructure Financing through Value Capture in IndonesiaFrom EverandInnovative Infrastructure Financing through Value Capture in IndonesiaRating: 5 out of 5 stars5/5 (1)

- 2 Swot MathsDocument8 pages2 Swot MathsLakshayNo ratings yet

- DJBBill 151093714822 PDFDocument2 pagesDJBBill 151093714822 PDFLakshayNo ratings yet

- 1 Swot EnglishDocument8 pages1 Swot EnglishLakshayNo ratings yet

- Board Note 31.03.2020 and 30.06.2020Document4 pagesBoard Note 31.03.2020 and 30.06.2020LakshayNo ratings yet

- 3 Swot CommnunicationDocument4 pages3 Swot CommnunicationLakshayNo ratings yet

- 4 SWOT Goal Clarity & Self-AwarenessDocument4 pages4 SWOT Goal Clarity & Self-AwarenessLakshayNo ratings yet

- FM Practical QuestionsDocument6 pagesFM Practical QuestionsLakshayNo ratings yet

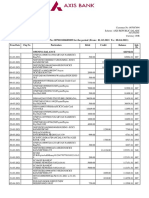

- Statement of Axis Account No:007010100685009 For The Period (From: 01-03-2021 To: 08-04-2021)Document3 pagesStatement of Axis Account No:007010100685009 For The Period (From: 01-03-2021 To: 08-04-2021)LakshayNo ratings yet

- One Page Brief As On 30.06.2020Document4 pagesOne Page Brief As On 30.06.2020LakshayNo ratings yet

- Fdocuments - in Harvest-GoldDocument25 pagesFdocuments - in Harvest-GoldLakshayNo ratings yet

- Jsfa - 5 July 2021Document15 pagesJsfa - 5 July 2021LakshayNo ratings yet

- Noting Board Note 31.03.2020 & 30.06.2020Document3 pagesNoting Board Note 31.03.2020 & 30.06.2020LakshayNo ratings yet

- Roster June, 2021 IIDocument1 pageRoster June, 2021 IILakshayNo ratings yet

- Problems Facec by ROsDocument1 pageProblems Facec by ROsLakshayNo ratings yet