Download as pdf or txt

You might also like

- Psychology Contemporary PerspectivesDocument993 pagesPsychology Contemporary PerspectivesTao Han100% (7)

- 100 Principles of Game DesignDocument71 pages100 Principles of Game DesignAgatha Maisie74% (19)

- M2019HRM046 - Cipla - Performance Management AssignementDocument11 pagesM2019HRM046 - Cipla - Performance Management AssignementpritamavhadNo ratings yet

- Mis PDFDocument216 pagesMis PDFPoornima AnnaduraiNo ratings yet

- MSci211 Syllabus-Spring 2014Document5 pagesMSci211 Syllabus-Spring 2014S>No ratings yet

- Unit-Iv: The Sourcing DecisionsDocument31 pagesUnit-Iv: The Sourcing DecisionsGangadhara Rao100% (1)

- A Summer Training Project Report On: "Training and Devlopment at Surya Roshni LTD."Document8 pagesA Summer Training Project Report On: "Training and Devlopment at Surya Roshni LTD."buddysmbdNo ratings yet

- Project Review and Administrative AspectsDocument8 pagesProject Review and Administrative Aspectsamitsingla19No ratings yet

- Unit IV Budgets & Budgetory ControlDocument19 pagesUnit IV Budgets & Budgetory ControlyogeshNo ratings yet

- Training Issues Resulting From Internal Need of The Company Internal TrainingDocument2 pagesTraining Issues Resulting From Internal Need of The Company Internal TrainingQAISER WASEEQNo ratings yet

- Syllabus of Shivaji University MBADocument24 pagesSyllabus of Shivaji University MBAmaheshlakade755No ratings yet

- Final PPT of Marginal CostDocument6 pagesFinal PPT of Marginal Costavanti543No ratings yet

- Case Study Investment and Cost of Capital - Neogi Chemical CompanyDocument5 pagesCase Study Investment and Cost of Capital - Neogi Chemical Companystudytime2574No ratings yet

- 401 GC-14 Enterprise Performance ManagementDocument11 pages401 GC-14 Enterprise Performance ManagementSumedh DipakeNo ratings yet

- LSCM Unit-VDocument28 pagesLSCM Unit-VGangadhara RaoNo ratings yet

- QRM PDFDocument31 pagesQRM PDFSuraj KambleNo ratings yet

- Role and Responsibility of Training ManagerDocument9 pagesRole and Responsibility of Training ManagerbekaluNo ratings yet

- Performance ReportDocument54 pagesPerformance ReportDivya HalpatiNo ratings yet

- 2.fixation of Material Levels - PPTDocument15 pages2.fixation of Material Levels - PPTHasim SaiyedNo ratings yet

- Whether DerivativesDocument11 pagesWhether DerivativesPreity YadavNo ratings yet

- Increased Concern of HRMDocument30 pagesIncreased Concern of HRMAishwarya Chachad33% (3)

- Chapter - 12: Risk Analysis in Capital BudgetingDocument28 pagesChapter - 12: Risk Analysis in Capital Budgetingrajat02No ratings yet

- Arbitrage ProcessDocument5 pagesArbitrage Processzohrah riazNo ratings yet

- Important Questions of Information Technology BBA & B.Com With AnswersDocument60 pagesImportant Questions of Information Technology BBA & B.Com With AnswersRishit GoelNo ratings yet

- Kavitha File 2Document49 pagesKavitha File 2Vinutha RNo ratings yet

- Topic - Compensation Management System at Iocl and Its Relation To Employee SatisfactionDocument12 pagesTopic - Compensation Management System at Iocl and Its Relation To Employee Satisfactionmeghs7682No ratings yet

- Summer Internship Project On OSCBDocument32 pagesSummer Internship Project On OSCBSunil ShekharNo ratings yet

- NTCC RoughDocument55 pagesNTCC RoughAnisha JainNo ratings yet

- A Study On Pricing OptimizationDocument10 pagesA Study On Pricing OptimizationLALITH PRIYANNo ratings yet

- FLIP Finance and Banking Practice Test 2Document14 pagesFLIP Finance and Banking Practice Test 2Aaditya Chawla100% (4)

- CenturyDocument54 pagesCenturySagar BansalNo ratings yet

- Human Resource PROJECT FILEDocument14 pagesHuman Resource PROJECT FILEharshitvaNo ratings yet

- MB0048 Operations ResearchDocument27 pagesMB0048 Operations ResearchdolodeepNo ratings yet

- UNIT-4 Mergers, Diversification and Performance EvaluationDocument13 pagesUNIT-4 Mergers, Diversification and Performance EvaluationRavalika PathipatiNo ratings yet

- Unit 1.2 SHRM Mba-4 Introduction To SHRMDocument16 pagesUnit 1.2 SHRM Mba-4 Introduction To SHRMaring100% (1)

- Project Report On Capital Structure On RelianceDocument7 pagesProject Report On Capital Structure On RelianceRashmi Kumari0% (1)

- Working Capital Management in Reliance Industries LimitedDocument5 pagesWorking Capital Management in Reliance Industries LimitedVurdalack666No ratings yet

- AbstractDocument9 pagesAbstractatulgehlot777100% (1)

- Health Care ManagementDocument22 pagesHealth Care ManagementSanskruti PathakNo ratings yet

- Steps in Aggregate Capacity PlanningDocument3 pagesSteps in Aggregate Capacity PlanningAdityaNo ratings yet

- Corporate Evolution Indian ContextDocument13 pagesCorporate Evolution Indian ContextShilpy Ravneet KaurNo ratings yet

- Recruitment, SelectionDocument63 pagesRecruitment, SelectionAkshay Shah100% (1)

- Effectiveness of Training at Canara Bank PROJECT REPORTDocument60 pagesEffectiveness of Training at Canara Bank PROJECT REPORTBabasab Patil (Karrisatte)0% (1)

- Role of Mis in Airtel WithDocument9 pagesRole of Mis in Airtel WithsangeetaaggarwalNo ratings yet

- DBA 7301 - Applied OperationsResearchDocument364 pagesDBA 7301 - Applied OperationsResearchpooja selvakumaranNo ratings yet

- Tailoring Strategy To Fit Specific Industry and Company SituationsDocument18 pagesTailoring Strategy To Fit Specific Industry and Company SituationsVikasSharmaNo ratings yet

- Knowledge Creation and Knowledge Architecture Chapter 4Document23 pagesKnowledge Creation and Knowledge Architecture Chapter 4linshujaNo ratings yet

- HRD Strategies For Long Term Planning & Growth: Unit-9Document28 pagesHRD Strategies For Long Term Planning & Growth: Unit-9rdeepak99No ratings yet

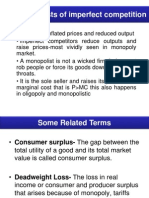

- Economic Costs of Imperfect CompetitionDocument15 pagesEconomic Costs of Imperfect Competitionsszr88No ratings yet

- Mba Project Report On HDFC BankDocument17 pagesMba Project Report On HDFC BankSai YaminiNo ratings yet

- Jntuk Mba III Sem r13Document26 pagesJntuk Mba III Sem r13j2ee.sridhar7319No ratings yet

- Becg Corporate Governance:: Notes Complied by Dr. Dhimen Jani Mba, CBS, Pgdibo, PHD MBA Sem. 1Document32 pagesBecg Corporate Governance:: Notes Complied by Dr. Dhimen Jani Mba, CBS, Pgdibo, PHD MBA Sem. 112Twinkal ModiNo ratings yet

- MBE PPT Unit IV Anna Universit Syllabus 2009 RegulationDocument16 pagesMBE PPT Unit IV Anna Universit Syllabus 2009 RegulationstandalonembaNo ratings yet

- LNMI MBA Syllabus 2020 FinalDocument157 pagesLNMI MBA Syllabus 2020 FinalAlok RajNo ratings yet

- Top Brass RemunerationDocument4 pagesTop Brass RemunerationJaspreetKaurNo ratings yet

- International Recruitment and SelectionDocument9 pagesInternational Recruitment and SelectionAshadul islam SamiulNo ratings yet

- Assignment Rubric Financial Management PFN1223Document2 pagesAssignment Rubric Financial Management PFN1223NURUL FATIN NABILA BINTI MOHD FADZIL (BG)No ratings yet

- IHRM HRM of USADocument48 pagesIHRM HRM of USAnitikadahiya87100% (3)

- Innovative HR Practices of Indian CompaniesDocument5 pagesInnovative HR Practices of Indian CompaniesSneha ShendeNo ratings yet

- Marketing in Indian EconomyDocument15 pagesMarketing in Indian Economyshivakumar NNo ratings yet

- The Human in Human ResourceFrom EverandThe Human in Human ResourceNo ratings yet

- Recruitment Process Outsourcing A Complete Guide - 2020 EditionFrom EverandRecruitment Process Outsourcing A Complete Guide - 2020 EditionNo ratings yet

- Assem Mohamed Abdeltawab Case1Document24 pagesAssem Mohamed Abdeltawab Case1assem mohamedNo ratings yet

- Chapter 15 - Optimism Bias PDFDocument19 pagesChapter 15 - Optimism Bias PDFassem mohamedNo ratings yet

- Chapter 1-What Is Behavioral FinanceDocument25 pagesChapter 1-What Is Behavioral Financeassem mohamedNo ratings yet

- Chapter 13 - Endowment Bias PDFDocument19 pagesChapter 13 - Endowment Bias PDFassem mohamedNo ratings yet

- International Finance - Monetary SystemsDocument44 pagesInternational Finance - Monetary Systemsassem mohamedNo ratings yet

- Dessler Chapter 8 TrainingDocument43 pagesDessler Chapter 8 Trainingassem mohamedNo ratings yet

- BDA Assessment 3Document10 pagesBDA Assessment 3harika vanguruNo ratings yet

- One of Us?: The Inclusion SolutionDocument29 pagesOne of Us?: The Inclusion SolutionKhalid Javaid AnwerNo ratings yet

- Decision MakingDocument16 pagesDecision MakingAnanda SalmaNo ratings yet

- Unit 1information and System ConceptsDocument34 pagesUnit 1information and System ConceptsKanchan SengarNo ratings yet

- Synopsis Jaya MamtaDocument36 pagesSynopsis Jaya MamtaNisha Dhanasekaran100% (1)

- Chapter+4 +Perceiving+PersonsDocument57 pagesChapter+4 +Perceiving+PersonslamitaNo ratings yet

- Cognitive Sample ResponsesDocument27 pagesCognitive Sample ResponsesSara ChoudharyNo ratings yet

- Bias and PrejudiceDocument3 pagesBias and Prejudicebilly saura100% (1)

- A Structured Approach To Strategic DecisionsDocument12 pagesA Structured Approach To Strategic DecisionsKSHITIJ CHANDRACHOORNo ratings yet

- Bab IDocument80 pagesBab ISitiHartinahNo ratings yet

- Heuristics in Judgment and Decision-MakingDocument10 pagesHeuristics in Judgment and Decision-MakingHomo CyberneticusNo ratings yet

- Barnum Effect - Biases & Heuristics - The Decision LabDocument4 pagesBarnum Effect - Biases & Heuristics - The Decision LabSahil SharmaNo ratings yet

- The Problem of Circularity in Evidence, Argument, and ExplanationDocument12 pagesThe Problem of Circularity in Evidence, Argument, and ExplanationShuvo H AhmedNo ratings yet

- Brief Analysis of StephaneDocument5 pagesBrief Analysis of StephaneMikeNo ratings yet

- Renn Benighaus Risk Perception 2013Document23 pagesRenn Benighaus Risk Perception 2013Abdurahman AbdNo ratings yet

- Investor Behavior and Asset Allocation ProcessDocument19 pagesInvestor Behavior and Asset Allocation ProcessAnjali Ajz77No ratings yet

- 배치고사 시험범위 실제기출문제 모음집Document9 pages배치고사 시험범위 실제기출문제 모음집gamechaehoNo ratings yet

- Thinking Fast and Slow PDF Summary FromDocument63 pagesThinking Fast and Slow PDF Summary Fromdastagir ahmedNo ratings yet

- Cognitive Bias or Logical Fallacy Presentation - 2Document3 pagesCognitive Bias or Logical Fallacy Presentation - 2mohammadwaheed88No ratings yet

- Sherwin.18-24.Modern Equity - CURRENTDocument27 pagesSherwin.18-24.Modern Equity - CURRENTZakariaNo ratings yet

- 03 - Review of LiteratureDocument8 pages03 - Review of Literatureammukhan khanNo ratings yet

- CH03 Emotional Errors HODocument44 pagesCH03 Emotional Errors HOFatima Zahra ElhaddekNo ratings yet

- Chapter 2 Introduction To Behavioral AnalysisDocument7 pagesChapter 2 Introduction To Behavioral AnalysisSwee Yi LeeNo ratings yet

- Institutional Economics - Concise NotesDocument42 pagesInstitutional Economics - Concise Notespoorvishetty2005No ratings yet

- Performance Management 3rd Edition Aguinis Solutions ManualDocument31 pagesPerformance Management 3rd Edition Aguinis Solutions ManualMariaBrownrgyib100% (19)

- FULL Download Ebook PDF Key Risk Indicators by Ann Rodriguez PDF EbookDocument35 pagesFULL Download Ebook PDF Key Risk Indicators by Ann Rodriguez PDF Ebookmary.grooms166100% (44)

- CognitiveDocument2 pagesCognitiveMuhammadNo ratings yet