Theory of Supply and Demand

Theory of Supply and Demand

You might also like

- IB Economics SL 2 - Supply and DemandDocument6 pagesIB Economics SL 2 - Supply and DemandTerran100% (3)

- A level Economics Revision: Cheeky Revision ShortcutsFrom EverandA level Economics Revision: Cheeky Revision ShortcutsRating: 3 out of 5 stars3/5 (1)

- HECO - Supply & Demand - EditedfinalDocument96 pagesHECO - Supply & Demand - EditedfinalJeannie PelonioNo ratings yet

- Chapter 3 Notes Interaction Supply and DemandDocument7 pagesChapter 3 Notes Interaction Supply and DemandBeatriz CanchilaNo ratings yet

- Demand and Supply Chapte RDocument38 pagesDemand and Supply Chapte Rsrijan consultancyNo ratings yet

- Theory of DemandDocument71 pagesTheory of DemandPranjal TiwariNo ratings yet

- Lecture - 4 - Markets 4Document25 pagesLecture - 4 - Markets 4Left LeftNo ratings yet

- Demand, Supply & Market Equilibrium: Instructor: Sajawal AslamDocument25 pagesDemand, Supply & Market Equilibrium: Instructor: Sajawal AslamSajawal AslamNo ratings yet

- Determinants of Demand Followings Are The Determinants or DemandDocument8 pagesDeterminants of Demand Followings Are The Determinants or DemandSherazButtNo ratings yet

- Ch-3 - Supply & Demand Theory - NewDocument30 pagesCh-3 - Supply & Demand Theory - NewSAKIB MD SHAFIUDDINNo ratings yet

- CH 3 Supply Demand TheoryDocument31 pagesCH 3 Supply Demand TheoryLutfun Nesa Aysha 1831892630No ratings yet

- Supply and DemandDocument10 pagesSupply and DemandAshikNo ratings yet

- Fundamental Law of EconomicsDocument12 pagesFundamental Law of Economicsbrigitte shane gedorioNo ratings yet

- King's College of The Philippines College of AccountancyDocument7 pagesKing's College of The Philippines College of AccountancyIrene Bal-iyang DaweNo ratings yet

- 2.1 Basic Economics IDocument21 pages2.1 Basic Economics IRhea llyn BacquialNo ratings yet

- Basic Principles of Supply and Demand-1Document47 pagesBasic Principles of Supply and Demand-1Aniñon, Daizel Maye C.No ratings yet

- Supply Demand and Competition 2015Document42 pagesSupply Demand and Competition 2015satishtirumelaNo ratings yet

- Supply and DemandDocument36 pagesSupply and DemandRebecca NiezenNo ratings yet

- 2 Demand and SupplyDocument38 pages2 Demand and SupplyEarl Louie MasacayanNo ratings yet

- Basic Eco 3Document18 pagesBasic Eco 3Updi kafi YmNo ratings yet

- Demand and SupplyDocument35 pagesDemand and SupplysiribandlaNo ratings yet

- ECO 162-Demand and SupplyDocument46 pagesECO 162-Demand and SupplyPixie Hollow100% (1)

- The Market Forces of Supply and Demand-1Document4 pagesThe Market Forces of Supply and Demand-1Joanna Felisa GoNo ratings yet

- Week 11 BBA The Market SystemDocument61 pagesWeek 11 BBA The Market SystemRachit JainNo ratings yet

- Wa0001Document78 pagesWa0001Harshith KNo ratings yet

- Law of Supply and DemandDocument49 pagesLaw of Supply and DemandArvi Kyle Grospe PunzalanNo ratings yet

- Microeconomics Class NotesDocument12 pagesMicroeconomics Class NotesMiles SmithNo ratings yet

- Law of Demand and SupplyDocument55 pagesLaw of Demand and SupplyXXXXXXXXXXXXXXXXXXNo ratings yet

- Micro EconomicsDocument58 pagesMicro EconomicsAimen AzeemNo ratings yet

- Law and Supply and DemandDocument4 pagesLaw and Supply and DemandBukhani MacabanganNo ratings yet

- Principles of Economics2Document39 pagesPrinciples of Economics2reda gadNo ratings yet

- NOTES - Supply and DemandDocument7 pagesNOTES - Supply and DemandjramNo ratings yet

- Demand & SupplyDocument45 pagesDemand & Supplylishpa123No ratings yet

- Mod 2 MicroecoDocument41 pagesMod 2 MicroecoHeina LyllanNo ratings yet

- Unit 2 - Demand, Supply and The Market 1Document94 pagesUnit 2 - Demand, Supply and The Market 1brianmfula2021No ratings yet

- Supply and Demand by Syed Mainur RashidDocument52 pagesSupply and Demand by Syed Mainur Rashidiftekher miniNo ratings yet

- Unit - I: Engg Economics & ManagementDocument29 pagesUnit - I: Engg Economics & ManagementVasundhara KrishnanNo ratings yet

- Introduction To Micre Economics 2nd SetDocument18 pagesIntroduction To Micre Economics 2nd Setesparagozanichole01No ratings yet

- Demand Supply CurveDocument13 pagesDemand Supply CurveQNo ratings yet

- Demand and SupplyDocument3 pagesDemand and SupplyShalu AgarwalNo ratings yet

- Chapter 4: The Market Forces of Supply and DemandDocument17 pagesChapter 4: The Market Forces of Supply and DemandFarNo ratings yet

- Econ NotesDocument10 pagesEcon Notesdavid27No ratings yet

- Demand and SupplyDocument16 pagesDemand and SupplyGA ahuja Pujabi aaNo ratings yet

- Supply & DemandDocument45 pagesSupply & DemandMazharul HassanNo ratings yet

- Ba LLB Eco Unit 2Document67 pagesBa LLB Eco Unit 2Simar Kaur100% (1)

- Basic Principles of Demand and SupplyDocument29 pagesBasic Principles of Demand and SupplySheilaMarieAnnMagcalas100% (1)

- Supply and DemandDocument19 pagesSupply and DemandUnicorn ProjectNo ratings yet

- Supply and DemandDocument16 pagesSupply and DemandMartin JanuaryNo ratings yet

- Sambheet Pal - Essay AssignmentDocument10 pagesSambheet Pal - Essay AssignmentNIKITA AGARWALLANo ratings yet

- Lecture 2 Ch03Document45 pagesLecture 2 Ch03Fahim Ashab Chowdhury100% (1)

- ECN1101 - Micro Economics: Ms. Farida's ClassDocument25 pagesECN1101 - Micro Economics: Ms. Farida's ClassFarida ViraniNo ratings yet

- Demand: Group Members: Agam Saxena Akshay Akshita Gupta Eshika Singhal Lakshay GoyalDocument19 pagesDemand: Group Members: Agam Saxena Akshay Akshita Gupta Eshika Singhal Lakshay GoyalAkshita GuptaNo ratings yet

- Market Forces PDFDocument8 pagesMarket Forces PDFPriyankar KandarpaNo ratings yet

- Demand: Done By: Rohini PradhanDocument17 pagesDemand: Done By: Rohini PradhanChaitu Un PrediCtbleNo ratings yet

- Unit 2Document62 pagesUnit 2unstopable 7 rodiesNo ratings yet

- Elements of Demand and SupplyDocument38 pagesElements of Demand and SupplyEugene CejeroNo ratings yet

- Microeconomics Part 3Document16 pagesMicroeconomics Part 3YzappleNo ratings yet

- Theory of DemandDocument64 pagesTheory of DemandGEORGENo ratings yet

- Demand and Supply - Price Ceilling and Floor (Autosaved)Document56 pagesDemand and Supply - Price Ceilling and Floor (Autosaved)swakrit banikNo ratings yet

- Lecture 3 & 4 PresentationDocument45 pagesLecture 3 & 4 Presentationmohamed morraNo ratings yet

- Lesson 3 EconDocument2 pagesLesson 3 EconBea Dela PeniaNo ratings yet

- Lesson 3 EconDocument2 pagesLesson 3 EconBea Dela PeniaNo ratings yet

- Business Ethics ReviewerDocument1 pageBusiness Ethics ReviewerBea Dela PeniaNo ratings yet

- Opm CH6Document5 pagesOpm CH6Bea Dela PeniaNo ratings yet

- Uts Notes (Midterm) Lesson 2Document5 pagesUts Notes (Midterm) Lesson 2Bea Dela PeniaNo ratings yet

- CFASDocument3 pagesCFASBea Dela PeniaNo ratings yet

- Anti Smoking CampaignDocument4 pagesAnti Smoking CampaignBea Dela PeniaNo ratings yet

- Financial StatementsDocument5 pagesFinancial StatementsBea Dela PeniaNo ratings yet

- Book 1Document13 pagesBook 1Bea Dela PeniaNo ratings yet

- Business PlanDocument11 pagesBusiness PlanBea Dela PeniaNo ratings yet

- CHAPTER5DRAFTDocument4 pagesCHAPTER5DRAFTBea Dela PeniaNo ratings yet

- Operation Management FormulaDocument2 pagesOperation Management FormulaBea Dela PeniaNo ratings yet

- Chapter 1-4 (Draft)Document43 pagesChapter 1-4 (Draft)Bea Dela PeniaNo ratings yet

- Chapter 1 2 Applied Econ Part I PDFDocument108 pagesChapter 1 2 Applied Econ Part I PDFBea Dela PeniaNo ratings yet

- FinalMarketSurvey BEADocument4 pagesFinalMarketSurvey BEABea Dela PeniaNo ratings yet

- Group7 (Financial Statements)Document6 pagesGroup7 (Financial Statements)Bea Dela PeniaNo ratings yet

- Journal EntryDocument2 pagesJournal EntryBea Dela PeniaNo ratings yet

- GR 7Document7 pagesGR 7Bea Dela PeniaNo ratings yet

- English For Academic and Professional Purposes EAPP 111 - 1Document221 pagesEnglish For Academic and Professional Purposes EAPP 111 - 1Bea Dela PeniaNo ratings yet

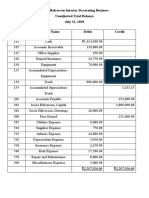

- Halverson With AdjusmentsDocument1 pageHalverson With AdjusmentsBea Dela PeniaNo ratings yet

- Adjusted Trial BalanceDocument1 pageAdjusted Trial BalanceBea Dela PeniaNo ratings yet

- Adjusting EntryDocument1 pageAdjusting EntryBea Dela PeniaNo ratings yet

- Income StatementDocument1 pageIncome StatementBea Dela PeniaNo ratings yet

- ABM A Chapter1Document4 pagesABM A Chapter1Bea Dela PeniaNo ratings yet

Download as docx, pdf, or txt

You might also like

- IB Economics SL 2 - Supply and DemandDocument6 pagesIB Economics SL 2 - Supply and DemandTerran100% (3)

- A level Economics Revision: Cheeky Revision ShortcutsFrom EverandA level Economics Revision: Cheeky Revision ShortcutsRating: 3 out of 5 stars3/5 (1)

- HECO - Supply & Demand - EditedfinalDocument96 pagesHECO - Supply & Demand - EditedfinalJeannie PelonioNo ratings yet

- Chapter 3 Notes Interaction Supply and DemandDocument7 pagesChapter 3 Notes Interaction Supply and DemandBeatriz CanchilaNo ratings yet

- Demand and Supply Chapte RDocument38 pagesDemand and Supply Chapte Rsrijan consultancyNo ratings yet

- Theory of DemandDocument71 pagesTheory of DemandPranjal TiwariNo ratings yet

- Lecture - 4 - Markets 4Document25 pagesLecture - 4 - Markets 4Left LeftNo ratings yet

- Demand, Supply & Market Equilibrium: Instructor: Sajawal AslamDocument25 pagesDemand, Supply & Market Equilibrium: Instructor: Sajawal AslamSajawal AslamNo ratings yet

- Determinants of Demand Followings Are The Determinants or DemandDocument8 pagesDeterminants of Demand Followings Are The Determinants or DemandSherazButtNo ratings yet

- Ch-3 - Supply & Demand Theory - NewDocument30 pagesCh-3 - Supply & Demand Theory - NewSAKIB MD SHAFIUDDINNo ratings yet

- CH 3 Supply Demand TheoryDocument31 pagesCH 3 Supply Demand TheoryLutfun Nesa Aysha 1831892630No ratings yet

- Supply and DemandDocument10 pagesSupply and DemandAshikNo ratings yet

- Fundamental Law of EconomicsDocument12 pagesFundamental Law of Economicsbrigitte shane gedorioNo ratings yet

- King's College of The Philippines College of AccountancyDocument7 pagesKing's College of The Philippines College of AccountancyIrene Bal-iyang DaweNo ratings yet

- 2.1 Basic Economics IDocument21 pages2.1 Basic Economics IRhea llyn BacquialNo ratings yet

- Basic Principles of Supply and Demand-1Document47 pagesBasic Principles of Supply and Demand-1Aniñon, Daizel Maye C.No ratings yet

- Supply Demand and Competition 2015Document42 pagesSupply Demand and Competition 2015satishtirumelaNo ratings yet

- Supply and DemandDocument36 pagesSupply and DemandRebecca NiezenNo ratings yet

- 2 Demand and SupplyDocument38 pages2 Demand and SupplyEarl Louie MasacayanNo ratings yet

- Basic Eco 3Document18 pagesBasic Eco 3Updi kafi YmNo ratings yet

- Demand and SupplyDocument35 pagesDemand and SupplysiribandlaNo ratings yet

- ECO 162-Demand and SupplyDocument46 pagesECO 162-Demand and SupplyPixie Hollow100% (1)

- The Market Forces of Supply and Demand-1Document4 pagesThe Market Forces of Supply and Demand-1Joanna Felisa GoNo ratings yet

- Week 11 BBA The Market SystemDocument61 pagesWeek 11 BBA The Market SystemRachit JainNo ratings yet

- Wa0001Document78 pagesWa0001Harshith KNo ratings yet

- Law of Supply and DemandDocument49 pagesLaw of Supply and DemandArvi Kyle Grospe PunzalanNo ratings yet

- Microeconomics Class NotesDocument12 pagesMicroeconomics Class NotesMiles SmithNo ratings yet

- Law of Demand and SupplyDocument55 pagesLaw of Demand and SupplyXXXXXXXXXXXXXXXXXXNo ratings yet

- Micro EconomicsDocument58 pagesMicro EconomicsAimen AzeemNo ratings yet

- Law and Supply and DemandDocument4 pagesLaw and Supply and DemandBukhani MacabanganNo ratings yet

- Principles of Economics2Document39 pagesPrinciples of Economics2reda gadNo ratings yet

- NOTES - Supply and DemandDocument7 pagesNOTES - Supply and DemandjramNo ratings yet

- Demand & SupplyDocument45 pagesDemand & Supplylishpa123No ratings yet

- Mod 2 MicroecoDocument41 pagesMod 2 MicroecoHeina LyllanNo ratings yet

- Unit 2 - Demand, Supply and The Market 1Document94 pagesUnit 2 - Demand, Supply and The Market 1brianmfula2021No ratings yet

- Supply and Demand by Syed Mainur RashidDocument52 pagesSupply and Demand by Syed Mainur Rashidiftekher miniNo ratings yet

- Unit - I: Engg Economics & ManagementDocument29 pagesUnit - I: Engg Economics & ManagementVasundhara KrishnanNo ratings yet

- Introduction To Micre Economics 2nd SetDocument18 pagesIntroduction To Micre Economics 2nd Setesparagozanichole01No ratings yet

- Demand Supply CurveDocument13 pagesDemand Supply CurveQNo ratings yet

- Demand and SupplyDocument3 pagesDemand and SupplyShalu AgarwalNo ratings yet

- Chapter 4: The Market Forces of Supply and DemandDocument17 pagesChapter 4: The Market Forces of Supply and DemandFarNo ratings yet

- Econ NotesDocument10 pagesEcon Notesdavid27No ratings yet

- Demand and SupplyDocument16 pagesDemand and SupplyGA ahuja Pujabi aaNo ratings yet

- Supply & DemandDocument45 pagesSupply & DemandMazharul HassanNo ratings yet

- Ba LLB Eco Unit 2Document67 pagesBa LLB Eco Unit 2Simar Kaur100% (1)

- Basic Principles of Demand and SupplyDocument29 pagesBasic Principles of Demand and SupplySheilaMarieAnnMagcalas100% (1)

- Supply and DemandDocument19 pagesSupply and DemandUnicorn ProjectNo ratings yet

- Supply and DemandDocument16 pagesSupply and DemandMartin JanuaryNo ratings yet

- Sambheet Pal - Essay AssignmentDocument10 pagesSambheet Pal - Essay AssignmentNIKITA AGARWALLANo ratings yet

- Lecture 2 Ch03Document45 pagesLecture 2 Ch03Fahim Ashab Chowdhury100% (1)

- ECN1101 - Micro Economics: Ms. Farida's ClassDocument25 pagesECN1101 - Micro Economics: Ms. Farida's ClassFarida ViraniNo ratings yet

- Demand: Group Members: Agam Saxena Akshay Akshita Gupta Eshika Singhal Lakshay GoyalDocument19 pagesDemand: Group Members: Agam Saxena Akshay Akshita Gupta Eshika Singhal Lakshay GoyalAkshita GuptaNo ratings yet

- Market Forces PDFDocument8 pagesMarket Forces PDFPriyankar KandarpaNo ratings yet

- Demand: Done By: Rohini PradhanDocument17 pagesDemand: Done By: Rohini PradhanChaitu Un PrediCtbleNo ratings yet

- Unit 2Document62 pagesUnit 2unstopable 7 rodiesNo ratings yet

- Elements of Demand and SupplyDocument38 pagesElements of Demand and SupplyEugene CejeroNo ratings yet

- Microeconomics Part 3Document16 pagesMicroeconomics Part 3YzappleNo ratings yet

- Theory of DemandDocument64 pagesTheory of DemandGEORGENo ratings yet

- Demand and Supply - Price Ceilling and Floor (Autosaved)Document56 pagesDemand and Supply - Price Ceilling and Floor (Autosaved)swakrit banikNo ratings yet

- Lecture 3 & 4 PresentationDocument45 pagesLecture 3 & 4 Presentationmohamed morraNo ratings yet

- Lesson 3 EconDocument2 pagesLesson 3 EconBea Dela PeniaNo ratings yet

- Lesson 3 EconDocument2 pagesLesson 3 EconBea Dela PeniaNo ratings yet

- Business Ethics ReviewerDocument1 pageBusiness Ethics ReviewerBea Dela PeniaNo ratings yet

- Opm CH6Document5 pagesOpm CH6Bea Dela PeniaNo ratings yet

- Uts Notes (Midterm) Lesson 2Document5 pagesUts Notes (Midterm) Lesson 2Bea Dela PeniaNo ratings yet

- CFASDocument3 pagesCFASBea Dela PeniaNo ratings yet

- Anti Smoking CampaignDocument4 pagesAnti Smoking CampaignBea Dela PeniaNo ratings yet

- Financial StatementsDocument5 pagesFinancial StatementsBea Dela PeniaNo ratings yet

- Book 1Document13 pagesBook 1Bea Dela PeniaNo ratings yet

- Business PlanDocument11 pagesBusiness PlanBea Dela PeniaNo ratings yet

- CHAPTER5DRAFTDocument4 pagesCHAPTER5DRAFTBea Dela PeniaNo ratings yet

- Operation Management FormulaDocument2 pagesOperation Management FormulaBea Dela PeniaNo ratings yet

- Chapter 1-4 (Draft)Document43 pagesChapter 1-4 (Draft)Bea Dela PeniaNo ratings yet

- Chapter 1 2 Applied Econ Part I PDFDocument108 pagesChapter 1 2 Applied Econ Part I PDFBea Dela PeniaNo ratings yet

- FinalMarketSurvey BEADocument4 pagesFinalMarketSurvey BEABea Dela PeniaNo ratings yet

- Group7 (Financial Statements)Document6 pagesGroup7 (Financial Statements)Bea Dela PeniaNo ratings yet

- Journal EntryDocument2 pagesJournal EntryBea Dela PeniaNo ratings yet

- GR 7Document7 pagesGR 7Bea Dela PeniaNo ratings yet

- English For Academic and Professional Purposes EAPP 111 - 1Document221 pagesEnglish For Academic and Professional Purposes EAPP 111 - 1Bea Dela PeniaNo ratings yet

- Halverson With AdjusmentsDocument1 pageHalverson With AdjusmentsBea Dela PeniaNo ratings yet

- Adjusted Trial BalanceDocument1 pageAdjusted Trial BalanceBea Dela PeniaNo ratings yet

- Adjusting EntryDocument1 pageAdjusting EntryBea Dela PeniaNo ratings yet

- Income StatementDocument1 pageIncome StatementBea Dela PeniaNo ratings yet

- ABM A Chapter1Document4 pagesABM A Chapter1Bea Dela PeniaNo ratings yet