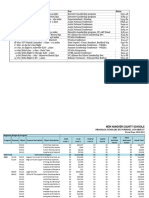

Allowances, Reimbursements and Advances 100122

Allowances, Reimbursements and Advances 100122

You might also like

- Citi Bank Statement PDFDocument6 pagesCiti Bank Statement PDFblack bird100% (1)

- FEASIBILITY REPORT OF LAUNDRY BUSINESS NewDocument17 pagesFEASIBILITY REPORT OF LAUNDRY BUSINESS NewOlamilekan Adedoyin73% (11)

- Enola Holmes and The Black Barouche by Nancy Springer Chapter SamplerDocument28 pagesEnola Holmes and The Black Barouche by Nancy Springer Chapter SamplerAllen & Unwin25% (8)

- AMOUNT DUE: $2,422.35: Charge DetailsDocument2 pagesAMOUNT DUE: $2,422.35: Charge DetailsCaroline Rigby-FeneNo ratings yet

- NovemberDocument3 pagesNovemberAl medrano100% (2)

- Account Number:: Rate: Date Prepared: RS-Residential ServiceDocument4 pagesAccount Number:: Rate: Date Prepared: RS-Residential ServiceRoopa Roopavathy0% (1)

- July 7th Negotiation PresentationDocument100 pagesJuly 7th Negotiation PresentationDan Trotter BN9No ratings yet

- Your Centrelink Statement For Parenting Payment: Reference: 207 828 705JDocument3 pagesYour Centrelink Statement For Parenting Payment: Reference: 207 828 705JhanhNo ratings yet

- How To Sharpen Your KnifeDocument67 pagesHow To Sharpen Your KnifeDiego BouNo ratings yet

- Case Study Decision Making ProcessDocument2 pagesCase Study Decision Making ProcessAdrian SibalNo ratings yet

- Futuresave 62785064660: Summary in Botswana Pula BWPDocument4 pagesFuturesave 62785064660: Summary in Botswana Pula BWPSnr Berel ShepherdNo ratings yet

- First Testbuilder 3rd Edition SampleDocument13 pagesFirst Testbuilder 3rd Edition Sampleabcgf50% (4)

- SOBO Sept 6, 2017 AgendaDocument11 pagesSOBO Sept 6, 2017 AgendaOaklandCBDsNo ratings yet

- PaySlip (4734)Document1 pagePaySlip (4734)Jose Antonio IrazustaNo ratings yet

- Page 1 of 3 Statement Summary December 2021 Statement Period 12/1/2021 - 12/31/2021Document3 pagesPage 1 of 3 Statement Summary December 2021 Statement Period 12/1/2021 - 12/31/2021Blackorchid 1No ratings yet

- Centrelink StatementDocument3 pagesCentrelink StatementAdam Di GiuseppeNo ratings yet

- YWCA 2022 Income & ExpenditureDocument4 pagesYWCA 2022 Income & ExpenditureLusi VeidreyakiNo ratings yet

- 2024 Truth in Taxation PresentationDocument19 pages2024 Truth in Taxation PresentationinforumdocsNo ratings yet

- Verified Final Refunding Numbers 7.10Document1 pageVerified Final Refunding Numbers 7.10maryrozakNo ratings yet

- Simulation 5 - Expense Reports Spring-2020Document2 pagesSimulation 5 - Expense Reports Spring-2020api-520202114No ratings yet

- Bayba Financial Service Update Report RevisedDocument9 pagesBayba Financial Service Update Report Revisedebrima JobzNo ratings yet

- Employee Payroll Report-2021Document2 pagesEmployee Payroll Report-2021ScottNo ratings yet

- Auprecedadata PAY1 TOLF80 Payslips 9455479904493 Sessionid PG0 V1 D5 T8Document1 pageAuprecedadata PAY1 TOLF80 Payslips 9455479904493 Sessionid PG0 V1 D5 T8Eggy PalangatNo ratings yet

- Armadale Rates 433029Document2 pagesArmadale Rates 433029Nishant AgarwalNo ratings yet

- Dr. Superintendent Charles Foust Bills - 2023Document2 pagesDr. Superintendent Charles Foust Bills - 2023Ben SchachtmanNo ratings yet

- Telus 603889349 2023 08 22Document6 pagesTelus 603889349 2023 08 22diamonddeeellNo ratings yet

- Redcliffe Area Youth Space: A.B.N. 17 724 640 741 Pay Slip For: Leduchowski, MaureenDocument1 pageRedcliffe Area Youth Space: A.B.N. 17 724 640 741 Pay Slip For: Leduchowski, MaureenSam BushNo ratings yet

- SOBO Jan 9, 2018 Agenda PacketDocument19 pagesSOBO Jan 9, 2018 Agenda PacketOaklandCBDsNo ratings yet

- Loan Detail & Fee WorksheetDocument1 pageLoan Detail & Fee WorksheetEricNo ratings yet

- Attachment 16268014602Document5 pagesAttachment 16268014602Web TreamicsNo ratings yet

- Inv40096497 1721332 11152021Document1 pageInv40096497 1721332 11152021Crown LotusNo ratings yet

- Royal Caribbean InternationalDocument4 pagesRoyal Caribbean InternationalVitaliy FedchenkoNo ratings yet

- Telus 603889349 2023 09 22Document6 pagesTelus 603889349 2023 09 22diamonddeeellNo ratings yet

- Simulation 6-Rashini WickramasingheDocument1 pageSimulation 6-Rashini Wickramasingheapi-547107253No ratings yet

- Chime Bank Statement NirtDocument3 pagesChime Bank Statement Nirtfehijan689No ratings yet

- Congratulations Caroline Blanchet!: Your New Honda Is ReadyDocument8 pagesCongratulations Caroline Blanchet!: Your New Honda Is ReadyMARKPNo ratings yet

- SalSlipJan 2022Document1 pageSalSlipJan 2022T TiwariNo ratings yet

- Financial Settlement Schedule LinquistDocument2 pagesFinancial Settlement Schedule LinquistsjlinquistNo ratings yet

- Assignment 5 - Expense Reports Calculations - Melissa BoivinDocument3 pagesAssignment 5 - Expense Reports Calculations - Melissa Boivinapi-507348320No ratings yet

- LoanContract 663805Document13 pagesLoanContract 663805least20022003No ratings yet

- (Worked) (Worked) : Total 5,333.61 Total 7,427.38Document13 pages(Worked) (Worked) : Total 5,333.61 Total 7,427.38Nicole N. BeldinezaNo ratings yet

- Daily Food Cost Report 12/mar/20 Amount in US $ Today Month To-Date Year To-Date TodayDocument3 pagesDaily Food Cost Report 12/mar/20 Amount in US $ Today Month To-Date Year To-Date Todaydinalsam90No ratings yet

- Joe Price: YoutubeDocument65 pagesJoe Price: YoutubeShaun HoltmanNo ratings yet

- Evaluation of Eoi Scoping and Design - Template-Sierra PalmDocument4 pagesEvaluation of Eoi Scoping and Design - Template-Sierra PalmrebeccayeamasesayNo ratings yet

- Activity Design QuennieDocument15 pagesActivity Design QuennieMerdzNo ratings yet

- Pay Stub PortalDocument1 pagePay Stub Portalcynthiaruder74No ratings yet

- Invoice 2 - Self CareDocument1 pageInvoice 2 - Self Carecass23aug72No ratings yet

- BiziMobile Inc.-2021 PDFDocument5 pagesBiziMobile Inc.-2021 PDFtahjinNo ratings yet

- Sagar Sapkota Full Application PDFDocument14 pagesSagar Sapkota Full Application PDFAnnie LamNo ratings yet

- 2017 World Under 17 Hockey Challenge Final ReportDocument82 pages2017 World Under 17 Hockey Challenge Final ReportAlaskaHighwayNewsNo ratings yet

- Abarquez, Roland, PDocument1 pageAbarquez, Roland, PROGER APOSTOLNo ratings yet

- Payment History Centrelink Online 2Document1 pagePayment History Centrelink Online 2mkilfoyle11No ratings yet

- Paystub 2Document2 pagesPaystub 2heaven.edwards2No ratings yet

- Daily Report Title 27166Document1 pageDaily Report Title 27166DIVESH CHANDRANo ratings yet

- 2022 San Pablo Recreation Use FeesDocument4 pages2022 San Pablo Recreation Use FeesKoushik RoyNo ratings yet

- PPNOVA Balance SheetDocument2 pagesPPNOVA Balance Sheetnileshbj.taskseverydayNo ratings yet

- Your Centrelink Statement For Jobseeker Payment: Reference: 421 801 301CDocument3 pagesYour Centrelink Statement For Jobseeker Payment: Reference: 421 801 301CZulfiqar AliNo ratings yet

- BS 21 22Document1 pageBS 21 22Pratik RajNo ratings yet

- Factors Considered Amount: Analysis Provided in Cell A42Document18 pagesFactors Considered Amount: Analysis Provided in Cell A42Shayan ChatterjeeNo ratings yet

- Movie Night Report FinalDocument7 pagesMovie Night Report FinalHyacinth RjsNo ratings yet

- LMU Board August 2, 2017 Agenda PacketDocument13 pagesLMU Board August 2, 2017 Agenda PacketOaklandCBDsNo ratings yet

- Pay Slip Components: Australian Concert and Entertainment Security Pty LTDDocument2 pagesPay Slip Components: Australian Concert and Entertainment Security Pty LTDGaro KhatcherianNo ratings yet

- DOA Board October 4, 2017 Agenda PacketDocument14 pagesDOA Board October 4, 2017 Agenda PacketOaklandCBDsNo ratings yet

- Wipro Offer LetterDocument12 pagesWipro Offer LetterSimran KaurNo ratings yet

- Mens WearDocument30 pagesMens WearAnuradha MasurkarNo ratings yet

- Basics of PressingDocument8 pagesBasics of PressingMæbēTh CuarterosNo ratings yet

- Lookame SsDocument7 pagesLookame SsSofia DoNo ratings yet

- Demonstrative PronounsDocument2 pagesDemonstrative PronounsLamanNo ratings yet

- Jordan BallzyDocument1 pageJordan BallzyСаша ВасильевNo ratings yet

- Max FactorDocument62 pagesMax Factorabc abcNo ratings yet

- Career Options PresentationDocument3 pagesCareer Options PresentationMamillapalli ChowdaryNo ratings yet

- MKT 465 Rajshahi SilkDocument17 pagesMKT 465 Rajshahi SilkRasiqul Islam RabbaniNo ratings yet

- Untitled DocumentDocument26 pagesUntitled DocumentSibina ANo ratings yet

- DR Lal Path LabsDocument69 pagesDR Lal Path Labsabhimanyu adhikaryNo ratings yet

- Grammar Planet Book2 Unit 6 TestDocument5 pagesGrammar Planet Book2 Unit 6 TestAndi RufairahNo ratings yet

- First Aid Kit ChecklistDocument1 pageFirst Aid Kit ChecklistShaira RosarioNo ratings yet

- Activity:: "Name Me"Document52 pagesActivity:: "Name Me"SHATERLAN ALVIAR. TACBOBONo ratings yet

- The Azorean Traditional Costume As A Sign of Regional Identity and Culture: From Clothing To JewelleryDocument11 pagesThe Azorean Traditional Costume As A Sign of Regional Identity and Culture: From Clothing To JewellerySylvie CastroNo ratings yet

- Chanel Perfume Black - Google Search PDFDocument1 pageChanel Perfume Black - Google Search PDFThe Moon N00CNo ratings yet

- T-Shirts Market AnalysisDocument5 pagesT-Shirts Market Analysistournesolsmile05No ratings yet

- CNS-July 2020 DigitalpdfDocument78 pagesCNS-July 2020 DigitalpdfChina-Flag-MakersNo ratings yet

- Customer Profile Demographics CosDocument3 pagesCustomer Profile Demographics Cosapi-742211858No ratings yet

- 14 Chapter6 PDFDocument65 pages14 Chapter6 PDFJohn DoeNo ratings yet

- Unit 2Document8 pagesUnit 2vm6374749809No ratings yet

- Preparatory Process For Weaving: Akshat Rana, TD, Pearl JaipurDocument40 pagesPreparatory Process For Weaving: Akshat Rana, TD, Pearl JaipurAishwarya NairNo ratings yet

- Residential Case Study 1 - SIMRAN SAINIDocument24 pagesResidential Case Study 1 - SIMRAN SAINISimranNo ratings yet

- Corporate Social Grace: 1. Etiquette - Meaning, Its Need and Types of EtiquettesDocument24 pagesCorporate Social Grace: 1. Etiquette - Meaning, Its Need and Types of EtiquettesLyza PacibeNo ratings yet

- Catalogue Essential Home Mid Century FurnitureDocument161 pagesCatalogue Essential Home Mid Century Furnituretajanan7240No ratings yet

Download as pdf or txt

You might also like

- Citi Bank Statement PDFDocument6 pagesCiti Bank Statement PDFblack bird100% (1)

- FEASIBILITY REPORT OF LAUNDRY BUSINESS NewDocument17 pagesFEASIBILITY REPORT OF LAUNDRY BUSINESS NewOlamilekan Adedoyin73% (11)

- Enola Holmes and The Black Barouche by Nancy Springer Chapter SamplerDocument28 pagesEnola Holmes and The Black Barouche by Nancy Springer Chapter SamplerAllen & Unwin25% (8)

- AMOUNT DUE: $2,422.35: Charge DetailsDocument2 pagesAMOUNT DUE: $2,422.35: Charge DetailsCaroline Rigby-FeneNo ratings yet

- NovemberDocument3 pagesNovemberAl medrano100% (2)

- Account Number:: Rate: Date Prepared: RS-Residential ServiceDocument4 pagesAccount Number:: Rate: Date Prepared: RS-Residential ServiceRoopa Roopavathy0% (1)

- July 7th Negotiation PresentationDocument100 pagesJuly 7th Negotiation PresentationDan Trotter BN9No ratings yet

- Your Centrelink Statement For Parenting Payment: Reference: 207 828 705JDocument3 pagesYour Centrelink Statement For Parenting Payment: Reference: 207 828 705JhanhNo ratings yet

- How To Sharpen Your KnifeDocument67 pagesHow To Sharpen Your KnifeDiego BouNo ratings yet

- Case Study Decision Making ProcessDocument2 pagesCase Study Decision Making ProcessAdrian SibalNo ratings yet

- Futuresave 62785064660: Summary in Botswana Pula BWPDocument4 pagesFuturesave 62785064660: Summary in Botswana Pula BWPSnr Berel ShepherdNo ratings yet

- First Testbuilder 3rd Edition SampleDocument13 pagesFirst Testbuilder 3rd Edition Sampleabcgf50% (4)

- SOBO Sept 6, 2017 AgendaDocument11 pagesSOBO Sept 6, 2017 AgendaOaklandCBDsNo ratings yet

- PaySlip (4734)Document1 pagePaySlip (4734)Jose Antonio IrazustaNo ratings yet

- Page 1 of 3 Statement Summary December 2021 Statement Period 12/1/2021 - 12/31/2021Document3 pagesPage 1 of 3 Statement Summary December 2021 Statement Period 12/1/2021 - 12/31/2021Blackorchid 1No ratings yet

- Centrelink StatementDocument3 pagesCentrelink StatementAdam Di GiuseppeNo ratings yet

- YWCA 2022 Income & ExpenditureDocument4 pagesYWCA 2022 Income & ExpenditureLusi VeidreyakiNo ratings yet

- 2024 Truth in Taxation PresentationDocument19 pages2024 Truth in Taxation PresentationinforumdocsNo ratings yet

- Verified Final Refunding Numbers 7.10Document1 pageVerified Final Refunding Numbers 7.10maryrozakNo ratings yet

- Simulation 5 - Expense Reports Spring-2020Document2 pagesSimulation 5 - Expense Reports Spring-2020api-520202114No ratings yet

- Bayba Financial Service Update Report RevisedDocument9 pagesBayba Financial Service Update Report Revisedebrima JobzNo ratings yet

- Employee Payroll Report-2021Document2 pagesEmployee Payroll Report-2021ScottNo ratings yet

- Auprecedadata PAY1 TOLF80 Payslips 9455479904493 Sessionid PG0 V1 D5 T8Document1 pageAuprecedadata PAY1 TOLF80 Payslips 9455479904493 Sessionid PG0 V1 D5 T8Eggy PalangatNo ratings yet

- Armadale Rates 433029Document2 pagesArmadale Rates 433029Nishant AgarwalNo ratings yet

- Dr. Superintendent Charles Foust Bills - 2023Document2 pagesDr. Superintendent Charles Foust Bills - 2023Ben SchachtmanNo ratings yet

- Telus 603889349 2023 08 22Document6 pagesTelus 603889349 2023 08 22diamonddeeellNo ratings yet

- Redcliffe Area Youth Space: A.B.N. 17 724 640 741 Pay Slip For: Leduchowski, MaureenDocument1 pageRedcliffe Area Youth Space: A.B.N. 17 724 640 741 Pay Slip For: Leduchowski, MaureenSam BushNo ratings yet

- SOBO Jan 9, 2018 Agenda PacketDocument19 pagesSOBO Jan 9, 2018 Agenda PacketOaklandCBDsNo ratings yet

- Loan Detail & Fee WorksheetDocument1 pageLoan Detail & Fee WorksheetEricNo ratings yet

- Attachment 16268014602Document5 pagesAttachment 16268014602Web TreamicsNo ratings yet

- Inv40096497 1721332 11152021Document1 pageInv40096497 1721332 11152021Crown LotusNo ratings yet

- Royal Caribbean InternationalDocument4 pagesRoyal Caribbean InternationalVitaliy FedchenkoNo ratings yet

- Telus 603889349 2023 09 22Document6 pagesTelus 603889349 2023 09 22diamonddeeellNo ratings yet

- Simulation 6-Rashini WickramasingheDocument1 pageSimulation 6-Rashini Wickramasingheapi-547107253No ratings yet

- Chime Bank Statement NirtDocument3 pagesChime Bank Statement Nirtfehijan689No ratings yet

- Congratulations Caroline Blanchet!: Your New Honda Is ReadyDocument8 pagesCongratulations Caroline Blanchet!: Your New Honda Is ReadyMARKPNo ratings yet

- SalSlipJan 2022Document1 pageSalSlipJan 2022T TiwariNo ratings yet

- Financial Settlement Schedule LinquistDocument2 pagesFinancial Settlement Schedule LinquistsjlinquistNo ratings yet

- Assignment 5 - Expense Reports Calculations - Melissa BoivinDocument3 pagesAssignment 5 - Expense Reports Calculations - Melissa Boivinapi-507348320No ratings yet

- LoanContract 663805Document13 pagesLoanContract 663805least20022003No ratings yet

- (Worked) (Worked) : Total 5,333.61 Total 7,427.38Document13 pages(Worked) (Worked) : Total 5,333.61 Total 7,427.38Nicole N. BeldinezaNo ratings yet

- Daily Food Cost Report 12/mar/20 Amount in US $ Today Month To-Date Year To-Date TodayDocument3 pagesDaily Food Cost Report 12/mar/20 Amount in US $ Today Month To-Date Year To-Date Todaydinalsam90No ratings yet

- Joe Price: YoutubeDocument65 pagesJoe Price: YoutubeShaun HoltmanNo ratings yet

- Evaluation of Eoi Scoping and Design - Template-Sierra PalmDocument4 pagesEvaluation of Eoi Scoping and Design - Template-Sierra PalmrebeccayeamasesayNo ratings yet

- Activity Design QuennieDocument15 pagesActivity Design QuennieMerdzNo ratings yet

- Pay Stub PortalDocument1 pagePay Stub Portalcynthiaruder74No ratings yet

- Invoice 2 - Self CareDocument1 pageInvoice 2 - Self Carecass23aug72No ratings yet

- BiziMobile Inc.-2021 PDFDocument5 pagesBiziMobile Inc.-2021 PDFtahjinNo ratings yet

- Sagar Sapkota Full Application PDFDocument14 pagesSagar Sapkota Full Application PDFAnnie LamNo ratings yet

- 2017 World Under 17 Hockey Challenge Final ReportDocument82 pages2017 World Under 17 Hockey Challenge Final ReportAlaskaHighwayNewsNo ratings yet

- Abarquez, Roland, PDocument1 pageAbarquez, Roland, PROGER APOSTOLNo ratings yet

- Payment History Centrelink Online 2Document1 pagePayment History Centrelink Online 2mkilfoyle11No ratings yet

- Paystub 2Document2 pagesPaystub 2heaven.edwards2No ratings yet

- Daily Report Title 27166Document1 pageDaily Report Title 27166DIVESH CHANDRANo ratings yet

- 2022 San Pablo Recreation Use FeesDocument4 pages2022 San Pablo Recreation Use FeesKoushik RoyNo ratings yet

- PPNOVA Balance SheetDocument2 pagesPPNOVA Balance Sheetnileshbj.taskseverydayNo ratings yet

- Your Centrelink Statement For Jobseeker Payment: Reference: 421 801 301CDocument3 pagesYour Centrelink Statement For Jobseeker Payment: Reference: 421 801 301CZulfiqar AliNo ratings yet

- BS 21 22Document1 pageBS 21 22Pratik RajNo ratings yet

- Factors Considered Amount: Analysis Provided in Cell A42Document18 pagesFactors Considered Amount: Analysis Provided in Cell A42Shayan ChatterjeeNo ratings yet

- Movie Night Report FinalDocument7 pagesMovie Night Report FinalHyacinth RjsNo ratings yet

- LMU Board August 2, 2017 Agenda PacketDocument13 pagesLMU Board August 2, 2017 Agenda PacketOaklandCBDsNo ratings yet

- Pay Slip Components: Australian Concert and Entertainment Security Pty LTDDocument2 pagesPay Slip Components: Australian Concert and Entertainment Security Pty LTDGaro KhatcherianNo ratings yet

- DOA Board October 4, 2017 Agenda PacketDocument14 pagesDOA Board October 4, 2017 Agenda PacketOaklandCBDsNo ratings yet

- Wipro Offer LetterDocument12 pagesWipro Offer LetterSimran KaurNo ratings yet

- Mens WearDocument30 pagesMens WearAnuradha MasurkarNo ratings yet

- Basics of PressingDocument8 pagesBasics of PressingMæbēTh CuarterosNo ratings yet

- Lookame SsDocument7 pagesLookame SsSofia DoNo ratings yet

- Demonstrative PronounsDocument2 pagesDemonstrative PronounsLamanNo ratings yet

- Jordan BallzyDocument1 pageJordan BallzyСаша ВасильевNo ratings yet

- Max FactorDocument62 pagesMax Factorabc abcNo ratings yet

- Career Options PresentationDocument3 pagesCareer Options PresentationMamillapalli ChowdaryNo ratings yet

- MKT 465 Rajshahi SilkDocument17 pagesMKT 465 Rajshahi SilkRasiqul Islam RabbaniNo ratings yet

- Untitled DocumentDocument26 pagesUntitled DocumentSibina ANo ratings yet

- DR Lal Path LabsDocument69 pagesDR Lal Path Labsabhimanyu adhikaryNo ratings yet

- Grammar Planet Book2 Unit 6 TestDocument5 pagesGrammar Planet Book2 Unit 6 TestAndi RufairahNo ratings yet

- First Aid Kit ChecklistDocument1 pageFirst Aid Kit ChecklistShaira RosarioNo ratings yet

- Activity:: "Name Me"Document52 pagesActivity:: "Name Me"SHATERLAN ALVIAR. TACBOBONo ratings yet

- The Azorean Traditional Costume As A Sign of Regional Identity and Culture: From Clothing To JewelleryDocument11 pagesThe Azorean Traditional Costume As A Sign of Regional Identity and Culture: From Clothing To JewellerySylvie CastroNo ratings yet

- Chanel Perfume Black - Google Search PDFDocument1 pageChanel Perfume Black - Google Search PDFThe Moon N00CNo ratings yet

- T-Shirts Market AnalysisDocument5 pagesT-Shirts Market Analysistournesolsmile05No ratings yet

- CNS-July 2020 DigitalpdfDocument78 pagesCNS-July 2020 DigitalpdfChina-Flag-MakersNo ratings yet

- Customer Profile Demographics CosDocument3 pagesCustomer Profile Demographics Cosapi-742211858No ratings yet

- 14 Chapter6 PDFDocument65 pages14 Chapter6 PDFJohn DoeNo ratings yet

- Unit 2Document8 pagesUnit 2vm6374749809No ratings yet

- Preparatory Process For Weaving: Akshat Rana, TD, Pearl JaipurDocument40 pagesPreparatory Process For Weaving: Akshat Rana, TD, Pearl JaipurAishwarya NairNo ratings yet

- Residential Case Study 1 - SIMRAN SAINIDocument24 pagesResidential Case Study 1 - SIMRAN SAINISimranNo ratings yet

- Corporate Social Grace: 1. Etiquette - Meaning, Its Need and Types of EtiquettesDocument24 pagesCorporate Social Grace: 1. Etiquette - Meaning, Its Need and Types of EtiquettesLyza PacibeNo ratings yet

- Catalogue Essential Home Mid Century FurnitureDocument161 pagesCatalogue Essential Home Mid Century Furnituretajanan7240No ratings yet