Download as pdf or txt

You might also like

- Template - Infringement-Passing-off Petition - Compressed-1587132596Document45 pagesTemplate - Infringement-Passing-off Petition - Compressed-1587132596ramya x100% (1)

- Dutch Impact Investors - 20140625Document39 pagesDutch Impact Investors - 20140625Debesh PradhanNo ratings yet

- Summer Internship Report 8.10Document83 pagesSummer Internship Report 8.10Alok0% (1)

- MutualDocument10 pagesMutualTARUN SUTHARNo ratings yet

- Chapter#10 (Financial&Funding)Document40 pagesChapter#10 (Financial&Funding)Ahmad UbaidNo ratings yet

- Barringer Ent6 10Document25 pagesBarringer Ent6 10Hafiz NomanNo ratings yet

- Summer Internship ReportDocument43 pagesSummer Internship Reportnikhil yadavNo ratings yet

- BMO2005 - Session 8 - SlidesDocument77 pagesBMO2005 - Session 8 - SlidesThiruuNo ratings yet

- FINS3623 Venture Capital: Week 2 - Private FinancingDocument55 pagesFINS3623 Venture Capital: Week 2 - Private FinancingHeidi DaoNo ratings yet

- Kashvi Golechha - Internship Research ReportDocument11 pagesKashvi Golechha - Internship Research ReportKashvi GolechhaNo ratings yet

- Lecture 1Document46 pagesLecture 1ishujain007No ratings yet

- Capital Raising GuideDocument41 pagesCapital Raising GuideAnkur DugarNo ratings yet

- Investing StudyDocument21 pagesInvesting Studydedan66No ratings yet

- Barringer Ent6 10Document50 pagesBarringer Ent6 10Ruba khattariNo ratings yet

- Funding Your BusinessDocument26 pagesFunding Your BusinessUb UsoroNo ratings yet

- Literature Review of Reliance Mutual FundDocument6 pagesLiterature Review of Reliance Mutual Fundbteubwbnd100% (1)

- Ba Core 6 Pmodule 9Document6 pagesBa Core 6 Pmodule 9Francheska LarozaNo ratings yet

- Pabrai Investment Funds Annual Meeting Notes - 2014 - Bits - ) BusinessDocument8 pagesPabrai Investment Funds Annual Meeting Notes - 2014 - Bits - ) BusinessnabsNo ratings yet

- Topic 7Document25 pagesTopic 7Tiger HồNo ratings yet

- Pratim SIP FinalDocument74 pagesPratim SIP Finalpratim shindeNo ratings yet

- Ideas20 Ashish KilaDocument81 pagesIdeas20 Ashish Kilaabhishekkumar00No ratings yet

- Guide To Venture Capital 2011Document35 pagesGuide To Venture Capital 2011graceenggint8799No ratings yet

- Study On Venture Capital &private Equity FundDocument18 pagesStudy On Venture Capital &private Equity FundRakesh kumarNo ratings yet

- A Project Report: ON Mutual Fund: A Globally Proven Investment Avenue Submitted in Partial Fulfillment ForDocument51 pagesA Project Report: ON Mutual Fund: A Globally Proven Investment Avenue Submitted in Partial Fulfillment ForSaiby khan KhanNo ratings yet

- Mutual Fund - Project ReportDocument73 pagesMutual Fund - Project ReportAmrit Kar0% (1)

- Chhatrapati Shahu Ji Maharaj University: A Project Report ONDocument66 pagesChhatrapati Shahu Ji Maharaj University: A Project Report ONashok kumar vermaNo ratings yet

- FE 8 Module 1Document7 pagesFE 8 Module 1ysiadoneromNo ratings yet

- Entepreneurship - Pertemuan 10Document38 pagesEntepreneurship - Pertemuan 10fawnianNo ratings yet

- Mutual Fund: A Globally Proven Investment AvenueDocument66 pagesMutual Fund: A Globally Proven Investment AvenueEshaan GuruNo ratings yet

- Efficient InnovationDocument20 pagesEfficient InnovationgudunNo ratings yet

- Lesson 7Document33 pagesLesson 7Mi 12A1 - 19 Nguyễn Ngọc TràNo ratings yet

- Venture Capital Thesis TopicsDocument4 pagesVenture Capital Thesis Topicssjfgexgig100% (2)

- Venture Capital FundsDocument95 pagesVenture Capital FundsEsha ShahNo ratings yet

- Early Stage FundingDocument29 pagesEarly Stage FundingHarsh AgarwalNo ratings yet

- Entrepreneurship - Slides - Getting Funding or Financing - Lesson 7Document42 pagesEntrepreneurship - Slides - Getting Funding or Financing - Lesson 7Hsk KogilanNo ratings yet

- Jurnal 4Document9 pagesJurnal 4Uchi TaragusaNo ratings yet

- Investment Thesis SynonymDocument8 pagesInvestment Thesis SynonymMonica Franklin100% (2)

- Mutualfundamit 130926045819 Phpapp01Document49 pagesMutualfundamit 130926045819 Phpapp01priyanshu singhNo ratings yet

- Joint Venture ProjectDocument20 pagesJoint Venture ProjectRajeev Raj100% (1)

- PT 10. Funding Plan Pitch DeckDocument20 pagesPT 10. Funding Plan Pitch Deckaminma006No ratings yet

- © 2018 Elsevier Inc. All Rights Reserved: Financing Entrepreneurship and Innovation in Emerging MarketsDocument5 pages© 2018 Elsevier Inc. All Rights Reserved: Financing Entrepreneurship and Innovation in Emerging Marketsrohini jhaNo ratings yet

- P Ev ArticleDocument6 pagesP Ev Articledivaamy4No ratings yet

- Angel and Venture CapitaDocument36 pagesAngel and Venture CapitaprachiNo ratings yet

- Project On Venture CapitalDocument60 pagesProject On Venture CapitalbabataukirNo ratings yet

- Day 4 BootcampDocument48 pagesDay 4 BootcampLissaNo ratings yet

- Private Equity Fund ThesisDocument6 pagesPrivate Equity Fund Thesisgxgtpggld100% (2)

- A Guide To Venture Capital 3261Document64 pagesA Guide To Venture Capital 3261graylogicNo ratings yet

- Various Stages of Venture Capital FinancingDocument19 pagesVarious Stages of Venture Capital Financingjoy9crasto100% (2)

- Venture Capital - Definition, Types, Advantages ADocument1 pageVenture Capital - Definition, Types, Advantages APriyanka VNo ratings yet

- Team 12 SubmissionDocument20 pagesTeam 12 SubmissionAnoushka GuptaNo ratings yet

- ExamDocument137 pagesExamHalimah SheikhNo ratings yet

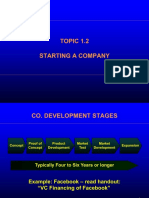

- 1.2 Starting A CompanyDocument14 pages1.2 Starting A CompanyRizky JuniardiNo ratings yet

- Reliance Money PDFDocument40 pagesReliance Money PDFMofa UmairNo ratings yet

- ZBNLV Iz MQX QY1665429971882Document8 pagesZBNLV Iz MQX QY1665429971882HARSHIT SAXENA 22IB428No ratings yet

- Ch15 Venture CapitalDocument43 pagesCh15 Venture CapitalAshima GuptaNo ratings yet

- Venture Capital - MithileshDocument88 pagesVenture Capital - MithileshTejas BamaneNo ratings yet

- Venture Capital in India Research PaperDocument8 pagesVenture Capital in India Research Paperhkdxiutlg100% (1)

- The ImpactAssets Handbook for Investors: Generating Social and Environmental Value through Capital InvestingFrom EverandThe ImpactAssets Handbook for Investors: Generating Social and Environmental Value through Capital InvestingNo ratings yet

- Innovation That Fits (Review and Analysis of Lord, Debethizy and Wager's Book)From EverandInnovation That Fits (Review and Analysis of Lord, Debethizy and Wager's Book)No ratings yet

- Danny Elfman Corpse Bride Official Sheet MusicDocument65 pagesDanny Elfman Corpse Bride Official Sheet MusicDavide CistrianiNo ratings yet

- Instant Download Direct Social Work Practice Theory and Skills 10th Edition Hepworth Test Bank PDF Full ChapterDocument15 pagesInstant Download Direct Social Work Practice Theory and Skills 10th Edition Hepworth Test Bank PDF Full ChapterBrookeWilkinsonMDpqjz100% (13)

- LOD Spec 2017 Part I - 2017-10-03 PDFDocument233 pagesLOD Spec 2017 Part I - 2017-10-03 PDFAniruddhNo ratings yet

- The Vigil - Guardian Angel Racial OptionDocument8 pagesThe Vigil - Guardian Angel Racial OptionIlia lnnkNo ratings yet

- Net Settings Menu ConfigDocument3 pagesNet Settings Menu ConfighaveNo ratings yet

- Trade Secret-IPRDocument16 pagesTrade Secret-IPRjaiNo ratings yet

- Ieee C57.12.31 - 2020Document24 pagesIeee C57.12.31 - 2020Anand SinghNo ratings yet

- Intellectual Property RightsDocument35 pagesIntellectual Property RightsUjjwal AnandNo ratings yet

- Mccormick Tractor Xtx145 Xtx165 Parts CatalogDocument20 pagesMccormick Tractor Xtx145 Xtx165 Parts Catalogjamesmiller060901qms100% (32)

- AviacionDocument301 pagesAviacionPablo Andres Gomez OrtizNo ratings yet

- Exponents Worksheet-2Document3 pagesExponents Worksheet-2Samaira GoelNo ratings yet

- PocketSwab Plus Operator's ManualDocument2 pagesPocketSwab Plus Operator's ManualTrroudNo ratings yet

- China Company Verification Report CatelogDocument5 pagesChina Company Verification Report CatelogDale DanNo ratings yet

- Clean Up and Re-Activate Profile Section DFF and Profile Item Attribute Category DataDocument5 pagesClean Up and Re-Activate Profile Section DFF and Profile Item Attribute Category DataSadiqNo ratings yet

- C940.28412 Expansion and Bleeding of Freshly Mixed Grouts ForDocument3 pagesC940.28412 Expansion and Bleeding of Freshly Mixed Grouts ForSabine Alejandra Kunze HidalgoNo ratings yet

- ECHELON FLEX GST Reload Tissue Thickness Comparison 060420 160920Document1 pageECHELON FLEX GST Reload Tissue Thickness Comparison 060420 160920Akbar Adrian RamadhanNo ratings yet

- MIL - Module 8 CopyrightDocument37 pagesMIL - Module 8 CopyrightJudy Ann EstuyaNo ratings yet

- Fatimah Chau - Sukd1902342Document13 pagesFatimah Chau - Sukd190234211 ChiaNo ratings yet

- 1876 Twiss Monumenta Juridica The Black Book of The Admiralty Vol 4Document761 pages1876 Twiss Monumenta Juridica The Black Book of The Admiralty Vol 4enickNo ratings yet

- Information Systems in Organizations 1st Edition Patricia Wallace Test BankDocument14 pagesInformation Systems in Organizations 1st Edition Patricia Wallace Test Banklesliepooleutss100% (28)

- Certificado Conformidad UL - Tubos EMTDocument1 pageCertificado Conformidad UL - Tubos EMTFrancisco Bolognesi VeraNo ratings yet

- Franchise Agreement: Created byDocument5 pagesFranchise Agreement: Created byJohn Kenneth BoholNo ratings yet

- 21-05-28 Intel Riso Rule 52 Motion JMOL '759 Under DoEDocument15 pages21-05-28 Intel Riso Rule 52 Motion JMOL '759 Under DoEFlorian MuellerNo ratings yet

- This Agreement Is Made This of 2021 Between Evolution Media LimitedDocument2 pagesThis Agreement Is Made This of 2021 Between Evolution Media LimitedVelasco BobbyNo ratings yet

- 3 Audit ReportDocument50 pages3 Audit ReportCristel TannaganNo ratings yet

- Assignment 1 - IPR - 2019 - 2020 AU PDFDocument1 pageAssignment 1 - IPR - 2019 - 2020 AU PDFPratyashNo ratings yet

- التجارة الإلكترونيةDocument100 pagesالتجارة الإلكترونيةAbdelkarim FettahNo ratings yet

- Ebm2024 1946Document43 pagesEbm2024 1946karen.oldham702No ratings yet

- Research Methodology and IPRDocument2 pagesResearch Methodology and IPRHaran HariNo ratings yet