Download as pdf or txt

You might also like

- Bins Dump ListDocument36 pagesBins Dump ListEsteban Camilo Ortiz Zambrano0% (1)

- Unlimited VCC Method PDFDocument9 pagesUnlimited VCC Method PDFAzren Dino100% (3)

- A1-A2 - Business Customer InfoDocument2 pagesA1-A2 - Business Customer InfoSteve Lim100% (1)

- Black Book PDFDocument78 pagesBlack Book PDFSayali Parulekar55% (11)

- Íq2F %$Q%# W (Ywhî Ìç ! Î: Total Due R 857.57Document4 pagesÍq2F %$Q%# W (Ywhî Ìç ! Î: Total Due R 857.57Mindrys100% (2)

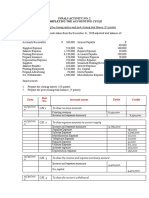

- Nerissa Mae L. Santos Activity On Completing The Accounting Cycle 1Document3 pagesNerissa Mae L. Santos Activity On Completing The Accounting Cycle 1Mica Mae Correa100% (1)

- Research Paper On Banking Sector PDFDocument8 pagesResearch Paper On Banking Sector PDFafmcsmvbr100% (1)

- Research Paper On E-Banking in India PDFDocument6 pagesResearch Paper On E-Banking in India PDFfvgr8hna100% (1)

- Summer Internships 2011 MBA 2010-12: Role of IT in The Banking IndustryDocument71 pagesSummer Internships 2011 MBA 2010-12: Role of IT in The Banking IndustrySakshi DuaNo ratings yet

- Research Papers On Risk Management in Indian BanksDocument5 pagesResearch Papers On Risk Management in Indian BanksafnkjuvgzjzrglNo ratings yet

- UCO BankDocument42 pagesUCO BankLokanath Choudhury100% (1)

- Research Papers On Investment Banking in IndiaDocument7 pagesResearch Papers On Investment Banking in Indiaafnhiheaebysya100% (1)

- Reinforcing Indonesian Banks' Earnings Stability: A Gcg-Moderated Analysis of Risk Profile, Bank Digitalization, and Fintech P2P LendingDocument14 pagesReinforcing Indonesian Banks' Earnings Stability: A Gcg-Moderated Analysis of Risk Profile, Bank Digitalization, and Fintech P2P Lendingindex PubNo ratings yet

- A Study of Credit Risk ManagementDocument60 pagesA Study of Credit Risk ManagementPrince Satish Reddy100% (2)

- Commercial Bank Research PaperDocument5 pagesCommercial Bank Research Paperjppawmrhf100% (1)

- Literature Review On Banking SectorDocument6 pagesLiterature Review On Banking Sectoraebvqfzmi100% (1)

- The Relationship Between Ebanking and Financial PerformanceDocument7 pagesThe Relationship Between Ebanking and Financial PerformanceCIC190020 STUDENTNo ratings yet

- Research Paper On BanksDocument5 pagesResearch Paper On Banksfvdra0st100% (1)

- Literature Review On Information Technology in Banking SectorDocument4 pagesLiterature Review On Information Technology in Banking SectorafdtvdcwfNo ratings yet

- R. Proposal (AAM Sir)Document5 pagesR. Proposal (AAM Sir)Rasha Onkon RiadNo ratings yet

- Corporate BankingDocument122 pagesCorporate Bankingrohan2788No ratings yet

- Customer Satisfaction With Ebanking in Uco BankDocument77 pagesCustomer Satisfaction With Ebanking in Uco BankRamanand100% (3)

- Growth and Development of Retail Banking in India: Drivers of Retail BankingDocument17 pagesGrowth and Development of Retail Banking in India: Drivers of Retail BankingDR.B.REVATHYNo ratings yet

- Banking Research Papers in IndiaDocument9 pagesBanking Research Papers in Indiausbxsqznd100% (1)

- 21-Uco-221 Research ArticleDocument10 pages21-Uco-221 Research Articlesurya79746No ratings yet

- Literature Review of Indian Banking SectorDocument5 pagesLiterature Review of Indian Banking Sectorc5kby94s100% (1)

- GP CoreDocument133 pagesGP CoreDivya GanesanNo ratings yet

- The Effects of Deposits Mobilization On Financial Performance in Commercial Banks in Rwanda. A Case of Equity Bank Rwanda Limited PDFDocument28 pagesThe Effects of Deposits Mobilization On Financial Performance in Commercial Banks in Rwanda. A Case of Equity Bank Rwanda Limited PDFJohn FrancisNo ratings yet

- Literature Review On Banking Services in IndiaDocument5 pagesLiterature Review On Banking Services in Indiaafmzvadopepwrb100% (1)

- Research Paper On BankingDocument4 pagesResearch Paper On Bankingzufehil0l0s2100% (1)

- Application of Information Technology in Banking Industry:Current ScenarioDocument7 pagesApplication of Information Technology in Banking Industry:Current ScenariozeeshanNo ratings yet

- Research Paper On Banking Services in IndiaDocument5 pagesResearch Paper On Banking Services in Indiafwuhlvgkf100% (1)

- Need and Importance of The Study: Indian Society of Agricultural MarketingDocument8 pagesNeed and Importance of The Study: Indian Society of Agricultural Marketingdhavalshah99No ratings yet

- HDFC NetBanking SynopsisDocument5 pagesHDFC NetBanking SynopsisPranavi Paul Pandey100% (1)

- Growth and Development of Retail Banking in India: Drivers of Retail BankingDocument17 pagesGrowth and Development of Retail Banking in India: Drivers of Retail BankingPRASANNANo ratings yet

- Determinants of Commercial Banks' Lending Behavior in NigeriaDocument12 pagesDeterminants of Commercial Banks' Lending Behavior in NigeriavqhNo ratings yet

- Literature Review Banking SectorDocument7 pagesLiterature Review Banking Sectoreubvhsvkg100% (1)

- Literature Review of Commercial Banks in NigeriaDocument8 pagesLiterature Review of Commercial Banks in Nigeriagpnovecnd100% (1)

- Credit Risk, Liquidity Risk and Profitability in Nepalese Commercial BanksDocument9 pagesCredit Risk, Liquidity Risk and Profitability in Nepalese Commercial BanksKarim FarjallahNo ratings yet

- Reinforcing Indonesian Banks' Earnings Stability: A Gcg-Moderated Analysis of Risk Profile, Bank Digitalization, and Fintech P2P LendingDocument14 pagesReinforcing Indonesian Banks' Earnings Stability: A Gcg-Moderated Analysis of Risk Profile, Bank Digitalization, and Fintech P2P Lendingindex PubNo ratings yet

- The Effect of E-Money On The Non-Financial Performance of BanksDocument5 pagesThe Effect of E-Money On The Non-Financial Performance of BanksResearch SolutionsNo ratings yet

- Chapter TwoDocument21 pagesChapter Twoafolabidairo5No ratings yet

- Finaacial Innovative and Creativity in Banking Sector.Document5 pagesFinaacial Innovative and Creativity in Banking Sector.SakshiNo ratings yet

- Dissertation On Risk Management in Indian Banking IndustryDocument7 pagesDissertation On Risk Management in Indian Banking IndustryHelpPaperRochesterNo ratings yet

- A Study On Services Quality of SBI In: P.RoselinDocument4 pagesA Study On Services Quality of SBI In: P.RoselinSanchit ParnamiNo ratings yet

- Research Paper On Banking Industry in PakistanDocument7 pagesResearch Paper On Banking Industry in Pakistanc9q0c0q7100% (1)

- Literature Review On Fundamental Analysis On Banking SectorDocument5 pagesLiterature Review On Fundamental Analysis On Banking SectormkcewzbndNo ratings yet

- SaranyaDocument24 pagesSaranyaSachin chinnuNo ratings yet

- E-Banking in Pakistan ThesisDocument5 pagesE-Banking in Pakistan Thesisafbteepof100% (1)

- Impact of M-Banking PDFDocument12 pagesImpact of M-Banking PDFWadhwa ShobhitNo ratings yet

- Challenges Faced by Indian Banking IndustryDocument5 pagesChallenges Faced by Indian Banking IndustryPooja Sakru100% (1)

- Digital Babking Final PDFDocument76 pagesDigital Babking Final PDFAafreen Choudhry100% (1)

- Information Systems in BankingDocument11 pagesInformation Systems in BankingAnonymous miFIQOve8YNo ratings yet

- The Effect of Bank Performance Factors On The Bank's Profitability in Indonesia BanksDocument5 pagesThe Effect of Bank Performance Factors On The Bank's Profitability in Indonesia BanksLISTRI HERLINANo ratings yet

- Research ConceptDocument7 pagesResearch ConceptDuke GlobalNo ratings yet

- Research Paper On Commercial BanksDocument5 pagesResearch Paper On Commercial Banksjicjtjxgf100% (1)

- Research Paper On Indian Banking SectorDocument7 pagesResearch Paper On Indian Banking Sectoriimytdcnd100% (1)

- Factors Affecting Development of Internet Banking in NepalDocument9 pagesFactors Affecting Development of Internet Banking in NepalMadridista KroosNo ratings yet

- E-Banking Strategy and Performance of Commercial BDocument19 pagesE-Banking Strategy and Performance of Commercial BNatinael AbebeNo ratings yet

- A Comparative Study of Digital Banking in Public and Private Sector BanksDocument5 pagesA Comparative Study of Digital Banking in Public and Private Sector BanksVishal Sharma100% (1)

- Report Proposal 086Document8 pagesReport Proposal 086089 Eidmul Hasan ShakibNo ratings yet

- Literature Review of Banking SystemDocument6 pagesLiterature Review of Banking Systemafmzsgbmgwtfoh100% (1)

- T R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)From EverandT R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)No ratings yet

- Asia Small and Medium-Sized Enterprise Monitor 2020: Volume III: Thematic Chapter—Fintech Loans to Tricycle Drivers in the PhilippinesFrom EverandAsia Small and Medium-Sized Enterprise Monitor 2020: Volume III: Thematic Chapter—Fintech Loans to Tricycle Drivers in the PhilippinesNo ratings yet

- EIB Working Papers 2019/10 - Structural and cyclical determinants of access to finance: Evidence from EgyptFrom EverandEIB Working Papers 2019/10 - Structural and cyclical determinants of access to finance: Evidence from EgyptNo ratings yet

- The Impact of Derivatives On Firm Risk JAE1999Document33 pagesThe Impact of Derivatives On Firm Risk JAE1999Faldi HarisNo ratings yet

- An Analysis of The Impact of The Internet On Competition in The Banking Industry Using Porter S Five Forces ModelDocument10 pagesAn Analysis of The Impact of The Internet On Competition in The Banking Industry Using Porter S Five Forces ModelFaldi HarisNo ratings yet

- Temasek Holding and Its Governance of Government-Linked CompaniesDocument32 pagesTemasek Holding and Its Governance of Government-Linked CompaniesFaldi HarisNo ratings yet

- Understanding Bank Valuation: An Application of The Equity Cash Flow and The Residual Income Approach in Bank Financial Accounting StatementsDocument10 pagesUnderstanding Bank Valuation: An Application of The Equity Cash Flow and The Residual Income Approach in Bank Financial Accounting StatementsFaldi HarisNo ratings yet

- Aggarwal 2018 - Sustainable Finance in Emerging Markets A Venture Capital Investment Decision DilemmaDocument13 pagesAggarwal 2018 - Sustainable Finance in Emerging Markets A Venture Capital Investment Decision DilemmaFaldi HarisNo ratings yet

- Sadiq 2022 - Does Green Finance Matter For Sustainable Entrepreneurship and Environmental Corporate Social Responsibility During COVID-19Document17 pagesSadiq 2022 - Does Green Finance Matter For Sustainable Entrepreneurship and Environmental Corporate Social Responsibility During COVID-19Faldi HarisNo ratings yet

- Madi 2020 - Private Equity and Venture Capital in China in The Aftermath of The Sino-American Trade DisputesDocument11 pagesMadi 2020 - Private Equity and Venture Capital in China in The Aftermath of The Sino-American Trade DisputesFaldi HarisNo ratings yet

- Bruton 2014 - Entrepreneurship, Poverty, and Asia Moving Beyond Subsistence EntrepreneurshipDocument22 pagesBruton 2014 - Entrepreneurship, Poverty, and Asia Moving Beyond Subsistence EntrepreneurshipFaldi HarisNo ratings yet

- Venture Capital Networks in Southeast Asia, Network Characteristics and Cohesive Subgroups (Thailand - 2021)Document16 pagesVenture Capital Networks in Southeast Asia, Network Characteristics and Cohesive Subgroups (Thailand - 2021)Faldi HarisNo ratings yet

- Scheela 2015 - Formal and Informal Venture Capital Investing in SEADocument21 pagesScheela 2015 - Formal and Informal Venture Capital Investing in SEAFaldi HarisNo ratings yet

- Summary of Regression Results - VAR ModelDocument34 pagesSummary of Regression Results - VAR ModelFaldi HarisNo ratings yet

- Company Valuation Summary by Faldi Rev.1Document8 pagesCompany Valuation Summary by Faldi Rev.1Faldi HarisNo ratings yet

- Case CH 5Document2 pagesCase CH 5Faldi HarisNo ratings yet

- Indicative Deposit Profit Rates: PKR Savings AccountsDocument3 pagesIndicative Deposit Profit Rates: PKR Savings AccountsEjaz AhmadNo ratings yet

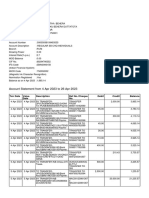

- Account Statement From 4 Apr 2023 To 26 Apr 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument7 pagesAccount Statement From 4 Apr 2023 To 26 Apr 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceBIKRAM KUMAR BEHERANo ratings yet

- Generali France SFCR 31-12-2021 PDFDocument159 pagesGenerali France SFCR 31-12-2021 PDFAlleg SharfokrugovNo ratings yet

- Public Sector Accounting Standards Board (Psacsb) Venue: Coa Professional Development OfficeDocument24 pagesPublic Sector Accounting Standards Board (Psacsb) Venue: Coa Professional Development OfficeLeonardo Don Alis CordovaNo ratings yet

- Financial Management Simplified CA Inter New CourseDocument355 pagesFinancial Management Simplified CA Inter New Courseharshadadalvi01No ratings yet

- Auditing TutorialDocument20 pagesAuditing TutorialDanisa NdhlovuNo ratings yet

- Commercial Bank: The Role of Commercial BanksDocument5 pagesCommercial Bank: The Role of Commercial BanksPreet AmanNo ratings yet

- SHGB Mpassbook 1-10-2023 25-1-2024 83860100035216Document3 pagesSHGB Mpassbook 1-10-2023 25-1-2024 83860100035216SUKHJEEVAN MARTIAL ART GROUPNo ratings yet

- Intermediate Accounting 1Document22 pagesIntermediate Accounting 1Nemalai VitalNo ratings yet

- Equity FundDocument1 pageEquity FundGia JonesNo ratings yet

- Eonnext Statement 2022 11 02Document4 pagesEonnext Statement 2022 11 02ying yingNo ratings yet

- Poa May 2001 Paper 2Document10 pagesPoa May 2001 Paper 2TiARA SerrantNo ratings yet

- 4.36 M.com Banking & FinanceDocument18 pages4.36 M.com Banking & FinancegoodwynjNo ratings yet

- LIC Jeevan Labh Plan (836) DetailsDocument12 pagesLIC Jeevan Labh Plan (836) DetailsMuthukrishnan SankaranNo ratings yet

- TT HiltonDocument2 pagesTT Hiltonnur ardilla mohd norNo ratings yet

- PDF 1st Long Quiz With Answers - CompressDocument5 pagesPDF 1st Long Quiz With Answers - CompressShaneen AdorableNo ratings yet

- Public Sector Accounting Developments and Conceptual FrameworkDocument24 pagesPublic Sector Accounting Developments and Conceptual FrameworkREJAY89No ratings yet

- Schedule of Charges Yes Bank 6Document2 pagesSchedule of Charges Yes Bank 6Sayantika MondalNo ratings yet

- SBR Examinable Docs 2021-22Document6 pagesSBR Examinable Docs 2021-22Stella YakubuNo ratings yet

- Assignment of Advanced Financialaccounting Post Graduate Regular ProgramDocument19 pagesAssignment of Advanced Financialaccounting Post Graduate Regular Programeferem100% (1)

- Acct Statement XX1940 05102022Document1 pageAcct Statement XX1940 05102022ARUN KUMARNo ratings yet

- Standard Chartered Bank ShortcutDocument20 pagesStandard Chartered Bank ShortcutRoyNo ratings yet

- Accounting 1 Review Series Worksheet ExercisesDocument14 pagesAccounting 1 Review Series Worksheet ExercisesKayle Mallillin100% (2)

- Session 8 Chapter 6Document22 pagesSession 8 Chapter 6Nguyen Khuu Vi K14 FUG CTNo ratings yet