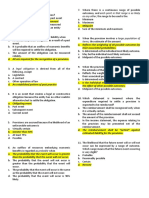

ACC309 Quiz On Current Liabilities 6

ACC309 Quiz On Current Liabilities 6

You might also like

- ToA Quizzer 10 - Provisions, ContingenciesDocument4 pagesToA Quizzer 10 - Provisions, ContingenciesEuniceChung50% (2)

- AccountingDocument50 pagesAccountingVidal Rnel80% (5)

- Ias 37 Provisions Contingent Liabilities and Contingent Assets SummaryDocument5 pagesIas 37 Provisions Contingent Liabilities and Contingent Assets SummaryChristian Dela Pena67% (3)

- Learning Material 4 PROVISION: Contingent Liability A. Discussion of Accounting PrinciplesDocument11 pagesLearning Material 4 PROVISION: Contingent Liability A. Discussion of Accounting PrinciplesJay GoNo ratings yet

- ACC309 Quiz On Current Liabilities 7Document1 pageACC309 Quiz On Current Liabilities 7SalazarNo ratings yet

- 6679 Current LiabilitiesDocument3 pages6679 Current LiabilitiesSungkyu KimNo ratings yet

- FdsedjwhajdhkudshdhxDocument28 pagesFdsedjwhajdhkudshdhxJoylyn CombongNo ratings yet

- Learning Resource 1 Lesson 4 PDFDocument14 pagesLearning Resource 1 Lesson 4 PDFJerald Jay Capistrano Catacutan100% (1)

- Problem 4-1 Multiple Choice (PAS 37)Document3 pagesProblem 4-1 Multiple Choice (PAS 37)jayNo ratings yet

- B. A Liability of Uncertain Timing or AmountDocument15 pagesB. A Liability of Uncertain Timing or Amountcherry blossomNo ratings yet

- SME Part 2 RevisedDocument44 pagesSME Part 2 RevisedJennifer RasonabeNo ratings yet

- FAR 6.3MC - Provisions, Contingent Liabilities and Contingent AssetsDocument5 pagesFAR 6.3MC - Provisions, Contingent Liabilities and Contingent Assetskateangel elleso0% (1)

- Ias 37 PDFDocument27 pagesIas 37 PDFmohedNo ratings yet

- Chapter 48: ProvisionDocument8 pagesChapter 48: ProvisionjsemlpzNo ratings yet

- ACC 211 Discussion - Provisions, Contingent Liability and Decommissioning LiabilityDocument5 pagesACC 211 Discussion - Provisions, Contingent Liability and Decommissioning LiabilitySayadi AdiihNo ratings yet

- Problem 4-3 Multiple Choice (PAS 37)Document2 pagesProblem 4-3 Multiple Choice (PAS 37)jayNo ratings yet

- Accounting Standard 29Document9 pagesAccounting Standard 29Rohit SemlaniNo ratings yet

- IAS 37 - SummaryDocument5 pagesIAS 37 - Summarysitoulamanish100No ratings yet

- Current Liabilities - ProvisionsDocument9 pagesCurrent Liabilities - ProvisionsJerome_JadeNo ratings yet

- AE 16 Prelims TheoriesDocument7 pagesAE 16 Prelims TheoriesJheally SeirNo ratings yet

- C4 ProvisionDocument81 pagesC4 ProvisionJoana RidadNo ratings yet

- Chapter 4 - Provision-Contingent LiabilityDocument7 pagesChapter 4 - Provision-Contingent LiabilityMarx Yuri JaymeNo ratings yet

- Ia2 Compre ToaDocument11 pagesIa2 Compre ToaMagic KentNo ratings yet

- Practice Quiz NonFinlLiabDocument15 pagesPractice Quiz NonFinlLiabIsabelle GuillenaNo ratings yet

- Mock Board Exam On Theory of AccountsDocument16 pagesMock Board Exam On Theory of AccountsNamor OnisaNo ratings yet

- IAS37Document2 pagesIAS37Mohammad Faisal SaleemNo ratings yet

- Risk and UncertaintiesDocument3 pagesRisk and UncertaintiesMarvin BañagaNo ratings yet

- Accounting Standard - 29 - Provisions, Contingent Liabilities & Contingent Assets - FelixDocument11 pagesAccounting Standard - 29 - Provisions, Contingent Liabilities & Contingent Assets - FelixSHREY ffNo ratings yet

- Reviewer in Theory of Accounts Multiple ChoiceDocument17 pagesReviewer in Theory of Accounts Multiple ChoiceDaniella Mae ElipNo ratings yet

- ACC 211 Review AssignmentDocument5 pagesACC 211 Review Assignmentglrosaaa cNo ratings yet

- All in Theories QuizDocument32 pagesAll in Theories QuizLeinell Sta. MariaNo ratings yet

- Pas 37Document3 pagesPas 37Jewel Ishi RomeroNo ratings yet

- Final Output Chapter 25-26Document27 pagesFinal Output Chapter 25-26Syrell Nabor100% (4)

- All in Theories PDFDocument31 pagesAll in Theories PDFReymel John Dela CruzNo ratings yet

- For Students Prelim ExamDocument8 pagesFor Students Prelim ExamHardly Dare GonzalesNo ratings yet

- LiabilitiesDocument157 pagesLiabilitiesvanNo ratings yet

- ProvisionDocument7 pagesProvisionAiden MagnoNo ratings yet

- Quizzer #10 LiabilitiesDocument19 pagesQuizzer #10 LiabilitiesKimmy ShawwyNo ratings yet

- Ias 37Document2 pagesIas 37Foititika.net100% (2)

- W4 - Tutorial SolutionsDocument8 pagesW4 - Tutorial SolutionsCJNo ratings yet

- Financial Accounting: Theory & Practice Provisions & ContingenciesDocument85 pagesFinancial Accounting: Theory & Practice Provisions & ContingenciesAngeilyn Roda67% (3)

- Ia2 Examination 1 Theories Liabilities and Provisions - CompressDocument3 pagesIa2 Examination 1 Theories Liabilities and Provisions - CompressTRECIA AMOR PAMILARNo ratings yet

- Concept Finals McqsDocument18 pagesConcept Finals Mcqsfiles dumpNo ratings yet

- Ind AS - 21 Provisions, Contingent Liabilities and Contingent Assets Objective ApplicabilityDocument4 pagesInd AS - 21 Provisions, Contingent Liabilities and Contingent Assets Objective ApplicabilityManaswi TripathiNo ratings yet

- Ia 2 Pre-Class NotesDocument67 pagesIa 2 Pre-Class NotesSHEENA MAE ORTIZANo ratings yet

- Act-6j03 Comp2 1stsem05-06Document12 pagesAct-6j03 Comp2 1stsem05-06RegenLudeveseNo ratings yet

- Provisions, Contingent Liabilities and Contingent AssetsDocument36 pagesProvisions, Contingent Liabilities and Contingent Assetspks009No ratings yet

- FAR LiabilitiesDocument31 pagesFAR LiabilitiesKenneth Bryan Tegerero Tegio100% (2)

- Liability FinalDocument26 pagesLiability FinalJomarie UyNo ratings yet

- p1 Corp Reporting Cpa Article 2017 Accounting For Provisions and ContingenciesDocument6 pagesp1 Corp Reporting Cpa Article 2017 Accounting For Provisions and ContingencieskimNo ratings yet

- IA Reviewer 2Document25 pagesIA Reviewer 2Krishele G. GotejerNo ratings yet

- Chapter 12 LiabilitiesDocument4 pagesChapter 12 Liabilitiesmaria isabella0% (1)

- 7208 - PAS 37 - Provisions, Contingent Liabilities and Contingent AssetsDocument6 pages7208 - PAS 37 - Provisions, Contingent Liabilities and Contingent Assetsjsmozol3434qcNo ratings yet

- Act 6J03 - Comp2 - 1stsem05-06Document12 pagesAct 6J03 - Comp2 - 1stsem05-06ROMAR A. PIGANo ratings yet

- Problem 4-33 Multiple ChoiceDocument2 pagesProblem 4-33 Multiple ChoicemaryaniNo ratings yet

- KTQNNCDocument40 pagesKTQNNCcamnhu622003No ratings yet

- FARAP - Liabilities - TheoriesDocument9 pagesFARAP - Liabilities - TheoriesvanNo ratings yet

- FPQP Practice Question Workbook: 1,000 Comprehensive Practice Questions (2024 Edition)From EverandFPQP Practice Question Workbook: 1,000 Comprehensive Practice Questions (2024 Edition)No ratings yet

- Pension Finance: Putting the Risks and Costs of Defined Benefit Plans Back Under Your ControlFrom EverandPension Finance: Putting the Risks and Costs of Defined Benefit Plans Back Under Your ControlNo ratings yet

- Decoding DCF: A Beginner's Guide to Discounted Cash Flow AnalysisFrom EverandDecoding DCF: A Beginner's Guide to Discounted Cash Flow AnalysisNo ratings yet

- Current Liabilities (Theories) 4Document1 pageCurrent Liabilities (Theories) 4SalazarNo ratings yet

- Current Liabilities (Theories) 5Document1 pageCurrent Liabilities (Theories) 5SalazarNo ratings yet

- ACC309 Quiz On Current Liabilities 4Document1 pageACC309 Quiz On Current Liabilities 4SalazarNo ratings yet

- ACC309 Quiz On Current Liabilities 5Document1 pageACC309 Quiz On Current Liabilities 5SalazarNo ratings yet

- ACC309 Quiz On Current Liabilities 8Document1 pageACC309 Quiz On Current Liabilities 8SalazarNo ratings yet

- ACC309 Quiz On Current Liabilities 7Document1 pageACC309 Quiz On Current Liabilities 7SalazarNo ratings yet

Download as docx, pdf, or txt

You might also like

- ToA Quizzer 10 - Provisions, ContingenciesDocument4 pagesToA Quizzer 10 - Provisions, ContingenciesEuniceChung50% (2)

- AccountingDocument50 pagesAccountingVidal Rnel80% (5)

- Ias 37 Provisions Contingent Liabilities and Contingent Assets SummaryDocument5 pagesIas 37 Provisions Contingent Liabilities and Contingent Assets SummaryChristian Dela Pena67% (3)

- Learning Material 4 PROVISION: Contingent Liability A. Discussion of Accounting PrinciplesDocument11 pagesLearning Material 4 PROVISION: Contingent Liability A. Discussion of Accounting PrinciplesJay GoNo ratings yet

- ACC309 Quiz On Current Liabilities 7Document1 pageACC309 Quiz On Current Liabilities 7SalazarNo ratings yet

- 6679 Current LiabilitiesDocument3 pages6679 Current LiabilitiesSungkyu KimNo ratings yet

- FdsedjwhajdhkudshdhxDocument28 pagesFdsedjwhajdhkudshdhxJoylyn CombongNo ratings yet

- Learning Resource 1 Lesson 4 PDFDocument14 pagesLearning Resource 1 Lesson 4 PDFJerald Jay Capistrano Catacutan100% (1)

- Problem 4-1 Multiple Choice (PAS 37)Document3 pagesProblem 4-1 Multiple Choice (PAS 37)jayNo ratings yet

- B. A Liability of Uncertain Timing or AmountDocument15 pagesB. A Liability of Uncertain Timing or Amountcherry blossomNo ratings yet

- SME Part 2 RevisedDocument44 pagesSME Part 2 RevisedJennifer RasonabeNo ratings yet

- FAR 6.3MC - Provisions, Contingent Liabilities and Contingent AssetsDocument5 pagesFAR 6.3MC - Provisions, Contingent Liabilities and Contingent Assetskateangel elleso0% (1)

- Ias 37 PDFDocument27 pagesIas 37 PDFmohedNo ratings yet

- Chapter 48: ProvisionDocument8 pagesChapter 48: ProvisionjsemlpzNo ratings yet

- ACC 211 Discussion - Provisions, Contingent Liability and Decommissioning LiabilityDocument5 pagesACC 211 Discussion - Provisions, Contingent Liability and Decommissioning LiabilitySayadi AdiihNo ratings yet

- Problem 4-3 Multiple Choice (PAS 37)Document2 pagesProblem 4-3 Multiple Choice (PAS 37)jayNo ratings yet

- Accounting Standard 29Document9 pagesAccounting Standard 29Rohit SemlaniNo ratings yet

- IAS 37 - SummaryDocument5 pagesIAS 37 - Summarysitoulamanish100No ratings yet

- Current Liabilities - ProvisionsDocument9 pagesCurrent Liabilities - ProvisionsJerome_JadeNo ratings yet

- AE 16 Prelims TheoriesDocument7 pagesAE 16 Prelims TheoriesJheally SeirNo ratings yet

- C4 ProvisionDocument81 pagesC4 ProvisionJoana RidadNo ratings yet

- Chapter 4 - Provision-Contingent LiabilityDocument7 pagesChapter 4 - Provision-Contingent LiabilityMarx Yuri JaymeNo ratings yet

- Ia2 Compre ToaDocument11 pagesIa2 Compre ToaMagic KentNo ratings yet

- Practice Quiz NonFinlLiabDocument15 pagesPractice Quiz NonFinlLiabIsabelle GuillenaNo ratings yet

- Mock Board Exam On Theory of AccountsDocument16 pagesMock Board Exam On Theory of AccountsNamor OnisaNo ratings yet

- IAS37Document2 pagesIAS37Mohammad Faisal SaleemNo ratings yet

- Risk and UncertaintiesDocument3 pagesRisk and UncertaintiesMarvin BañagaNo ratings yet

- Accounting Standard - 29 - Provisions, Contingent Liabilities & Contingent Assets - FelixDocument11 pagesAccounting Standard - 29 - Provisions, Contingent Liabilities & Contingent Assets - FelixSHREY ffNo ratings yet

- Reviewer in Theory of Accounts Multiple ChoiceDocument17 pagesReviewer in Theory of Accounts Multiple ChoiceDaniella Mae ElipNo ratings yet

- ACC 211 Review AssignmentDocument5 pagesACC 211 Review Assignmentglrosaaa cNo ratings yet

- All in Theories QuizDocument32 pagesAll in Theories QuizLeinell Sta. MariaNo ratings yet

- Pas 37Document3 pagesPas 37Jewel Ishi RomeroNo ratings yet

- Final Output Chapter 25-26Document27 pagesFinal Output Chapter 25-26Syrell Nabor100% (4)

- All in Theories PDFDocument31 pagesAll in Theories PDFReymel John Dela CruzNo ratings yet

- For Students Prelim ExamDocument8 pagesFor Students Prelim ExamHardly Dare GonzalesNo ratings yet

- LiabilitiesDocument157 pagesLiabilitiesvanNo ratings yet

- ProvisionDocument7 pagesProvisionAiden MagnoNo ratings yet

- Quizzer #10 LiabilitiesDocument19 pagesQuizzer #10 LiabilitiesKimmy ShawwyNo ratings yet

- Ias 37Document2 pagesIas 37Foititika.net100% (2)

- W4 - Tutorial SolutionsDocument8 pagesW4 - Tutorial SolutionsCJNo ratings yet

- Financial Accounting: Theory & Practice Provisions & ContingenciesDocument85 pagesFinancial Accounting: Theory & Practice Provisions & ContingenciesAngeilyn Roda67% (3)

- Ia2 Examination 1 Theories Liabilities and Provisions - CompressDocument3 pagesIa2 Examination 1 Theories Liabilities and Provisions - CompressTRECIA AMOR PAMILARNo ratings yet

- Concept Finals McqsDocument18 pagesConcept Finals Mcqsfiles dumpNo ratings yet

- Ind AS - 21 Provisions, Contingent Liabilities and Contingent Assets Objective ApplicabilityDocument4 pagesInd AS - 21 Provisions, Contingent Liabilities and Contingent Assets Objective ApplicabilityManaswi TripathiNo ratings yet

- Ia 2 Pre-Class NotesDocument67 pagesIa 2 Pre-Class NotesSHEENA MAE ORTIZANo ratings yet

- Act-6j03 Comp2 1stsem05-06Document12 pagesAct-6j03 Comp2 1stsem05-06RegenLudeveseNo ratings yet

- Provisions, Contingent Liabilities and Contingent AssetsDocument36 pagesProvisions, Contingent Liabilities and Contingent Assetspks009No ratings yet

- FAR LiabilitiesDocument31 pagesFAR LiabilitiesKenneth Bryan Tegerero Tegio100% (2)

- Liability FinalDocument26 pagesLiability FinalJomarie UyNo ratings yet

- p1 Corp Reporting Cpa Article 2017 Accounting For Provisions and ContingenciesDocument6 pagesp1 Corp Reporting Cpa Article 2017 Accounting For Provisions and ContingencieskimNo ratings yet

- IA Reviewer 2Document25 pagesIA Reviewer 2Krishele G. GotejerNo ratings yet

- Chapter 12 LiabilitiesDocument4 pagesChapter 12 Liabilitiesmaria isabella0% (1)

- 7208 - PAS 37 - Provisions, Contingent Liabilities and Contingent AssetsDocument6 pages7208 - PAS 37 - Provisions, Contingent Liabilities and Contingent Assetsjsmozol3434qcNo ratings yet

- Act 6J03 - Comp2 - 1stsem05-06Document12 pagesAct 6J03 - Comp2 - 1stsem05-06ROMAR A. PIGANo ratings yet

- Problem 4-33 Multiple ChoiceDocument2 pagesProblem 4-33 Multiple ChoicemaryaniNo ratings yet

- KTQNNCDocument40 pagesKTQNNCcamnhu622003No ratings yet

- FARAP - Liabilities - TheoriesDocument9 pagesFARAP - Liabilities - TheoriesvanNo ratings yet

- FPQP Practice Question Workbook: 1,000 Comprehensive Practice Questions (2024 Edition)From EverandFPQP Practice Question Workbook: 1,000 Comprehensive Practice Questions (2024 Edition)No ratings yet

- Pension Finance: Putting the Risks and Costs of Defined Benefit Plans Back Under Your ControlFrom EverandPension Finance: Putting the Risks and Costs of Defined Benefit Plans Back Under Your ControlNo ratings yet

- Decoding DCF: A Beginner's Guide to Discounted Cash Flow AnalysisFrom EverandDecoding DCF: A Beginner's Guide to Discounted Cash Flow AnalysisNo ratings yet

- Current Liabilities (Theories) 4Document1 pageCurrent Liabilities (Theories) 4SalazarNo ratings yet

- Current Liabilities (Theories) 5Document1 pageCurrent Liabilities (Theories) 5SalazarNo ratings yet

- ACC309 Quiz On Current Liabilities 4Document1 pageACC309 Quiz On Current Liabilities 4SalazarNo ratings yet

- ACC309 Quiz On Current Liabilities 5Document1 pageACC309 Quiz On Current Liabilities 5SalazarNo ratings yet

- ACC309 Quiz On Current Liabilities 8Document1 pageACC309 Quiz On Current Liabilities 8SalazarNo ratings yet

- ACC309 Quiz On Current Liabilities 7Document1 pageACC309 Quiz On Current Liabilities 7SalazarNo ratings yet