Download as pdf or txt

You might also like

- The Study of Global Political Economy John Ravenhill Chapter 1Document27 pagesThe Study of Global Political Economy John Ravenhill Chapter 1Shreeya VatsaNo ratings yet

- Monetary Policy Review - December 2023Document3 pagesMonetary Policy Review - December 2023samyukthasr36No ratings yet

- Rbi Monetary Policy Review Further Cuts LikelyDocument6 pagesRbi Monetary Policy Review Further Cuts LikelyTaransh ANo ratings yet

- Review of Monetary Policy Statement H2'24 by EBLSLDocument7 pagesReview of Monetary Policy Statement H2'24 by EBLSLAnika Nawar ChowdhuryNo ratings yet

- RBI Policy Review: Turning Hawkish: Normalization of Policy Corridor and Introduction of SDFDocument5 pagesRBI Policy Review: Turning Hawkish: Normalization of Policy Corridor and Introduction of SDFswapnaNo ratings yet

- Indopremier MacroInsight 23 Jun 2023 Unchanged BI Rate Aimed atDocument3 pagesIndopremier MacroInsight 23 Jun 2023 Unchanged BI Rate Aimed atbotoy26No ratings yet

- ICICIdirect MonthlyMFReportDocument12 pagesICICIdirect MonthlyMFReportSagar KulkarniNo ratings yet

- Bfsi by AxisDocument14 pagesBfsi by AxisJANARTHAN SANKARANNo ratings yet

- Gic Weekly 080124Document14 pagesGic Weekly 080124eldime06No ratings yet

- Axis Top Picks Jun 2022Document90 pagesAxis Top Picks Jun 2022Ankit GoelNo ratings yet

- Mutual Fund Review: Equity MarketDocument11 pagesMutual Fund Review: Equity MarketNadim ReghiwaleNo ratings yet

- Perspective On The Monetary Policy' by Rajani Sinha, Chief Economist & National Director - Research, Knight Frank IndiaDocument3 pagesPerspective On The Monetary Policy' by Rajani Sinha, Chief Economist & National Director - Research, Knight Frank IndiaNaveen BhaiNo ratings yet

- Calibrated Normalisation: Monetary PolicyDocument4 pagesCalibrated Normalisation: Monetary Policyvikash singhNo ratings yet

- BSP MonetaryPolicySummary August2022 QuizDocument2 pagesBSP MonetaryPolicySummary August2022 Quizcjpadin09No ratings yet

- SG IndiaDocument6 pagesSG IndiaAjay KastureNo ratings yet

- Monetary Policy Review 301007Document3 pagesMonetary Policy Review 301007pranjal92pandeyNo ratings yet

- MCIRFEBRUARY1311Document4 pagesMCIRFEBRUARY1311rohangundpatil096No ratings yet

- Monetary Policy Review No.7 2022Document7 pagesMonetary Policy Review No.7 2022Adaderana OnlineNo ratings yet

- Gathering Speed - Update On The Monetary Policy - June 2022Document5 pagesGathering Speed - Update On The Monetary Policy - June 2022Huzefa BharmalNo ratings yet

- UOB Global Economics & Markets Research 2021Document1 pageUOB Global Economics & Markets Research 2021Freddy Daniel NababanNo ratings yet

- Fixed Income Weekly Update - 20th May-24th May 2024Document1 pageFixed Income Weekly Update - 20th May-24th May 2024YasahNo ratings yet

- Brochure - Group 9 (Influence of RBI)Document8 pagesBrochure - Group 9 (Influence of RBI)Sugandha Gajanan GhadiNo ratings yet

- AXIS No 23Document14 pagesAXIS No 23Rushil KhajanchiNo ratings yet

- March 2021Document15 pagesMarch 2021RajugupatiNo ratings yet

- 8th April Monetary PolicyDocument3 pages8th April Monetary PolicyNeeleshNo ratings yet

- BFSI Q2FY22 - Earnings Preview - 08102021 Final (1) (1) - 08-10-2021 - 09Document13 pagesBFSI Q2FY22 - Earnings Preview - 08102021 Final (1) (1) - 08-10-2021 - 09slohariNo ratings yet

- IIFL - Banks - 4QFY24 Preview - 20240410Document19 pagesIIFL - Banks - 4QFY24 Preview - 20240410Ezzt YasserNo ratings yet

- Wa0059.Document19 pagesWa0059.Aryan NandwaniNo ratings yet

- Economic Outlook ": Empowering The Indonesian Economy For Stronger Recovery"Document23 pagesEconomic Outlook ": Empowering The Indonesian Economy For Stronger Recovery"fadjaradNo ratings yet

- UOB Economic Outlook 2022 - Global Economics & Markets ResearchDocument18 pagesUOB Economic Outlook 2022 - Global Economics & Markets ResearchWagimin SendjajaNo ratings yet

- Westpack JUN 14 Weekly CommentaryDocument7 pagesWestpack JUN 14 Weekly CommentaryMiir ViirNo ratings yet

- FY 10 Monetary ReviewDocument4 pagesFY 10 Monetary ReviewVivek SarinNo ratings yet

- Week Ended September 21, 2012: Icici Amc Idfc Amc Icici BankDocument4 pagesWeek Ended September 21, 2012: Icici Amc Idfc Amc Icici BankBonthala BadrNo ratings yet

- RBI Monetary Policy Statement - Must Read For The Class Now and TodayDocument4 pagesRBI Monetary Policy Statement - Must Read For The Class Now and TodayAnanya SharmaNo ratings yet

- Performance of Debt Markt: An Article ReviewDocument11 pagesPerformance of Debt Markt: An Article ReviewNida SubhaniNo ratings yet

- Credit Policy Review - May 2020Document5 pagesCredit Policy Review - May 2020Sanjay SharmaNo ratings yet

- Spark CapitalDocument57 pagesSpark CapitalNaushil ShahNo ratings yet

- Pakistan's Monetary Policy of 2022Document14 pagesPakistan's Monetary Policy of 2022Gohar KhalidNo ratings yet

- Ed - 11-08-2023Document1 pageEd - 11-08-2023Avinash Chandra RanaNo ratings yet

- FinSights - RBI Monetary Policy Statement Dec 2020Document2 pagesFinSights - RBI Monetary Policy Statement Dec 2020speedenquiryNo ratings yet

- MPR Quarter III 2022Document20 pagesMPR Quarter III 2022Muhammad HasyimNo ratings yet

- RBI 25bp HIkeDocument1 pageRBI 25bp HIkeadithyaNo ratings yet

- Bullish Under The Hood December Policy TakeawaysDocument3 pagesBullish Under The Hood December Policy Takeawaysvishal_lal89No ratings yet

- Task 7 ESSAYDocument1 pageTask 7 ESSAYDanielle UgayNo ratings yet

- NH-2022-Indonesia Market-Outlook-Final PDFDocument82 pagesNH-2022-Indonesia Market-Outlook-Final PDFUdan RMNo ratings yet

- Icici Prudential Mutual Fund Rbi Second Quarter Review of Monetary Policy 2010-11Document4 pagesIcici Prudential Mutual Fund Rbi Second Quarter Review of Monetary Policy 2010-11Vinit KumarNo ratings yet

- Aryan Chaudhary BE PSDA 2Document4 pagesAryan Chaudhary BE PSDA 2Anuj VermaNo ratings yet

- Credence Capital - MPC Aug 2022Document1 pageCredence Capital - MPC Aug 2022Sandeep TiwariNo ratings yet

- Key Highlights:: Inflationary Pressures Overrides Downside Risks To GrowthDocument6 pagesKey Highlights:: Inflationary Pressures Overrides Downside Risks To Growthsamyak_jain_8No ratings yet

- Annual Report Investments FY23 CPDocument4 pagesAnnual Report Investments FY23 CPVipul MangalathNo ratings yet

- Mortgage Rate ForecastDocument2 pagesMortgage Rate ForecastIgorNo ratings yet

- Interest Rate Cut 11-06Document2 pagesInterest Rate Cut 11-06ijaz AhmadNo ratings yet

- Credit Policy 5 Reasons Why RBI Is Unlikely To ActDocument2 pagesCredit Policy 5 Reasons Why RBI Is Unlikely To ActShwetabh SrivastavaNo ratings yet

- Schroders Outlook 2022 Macro Market Outlook FinalDocument24 pagesSchroders Outlook 2022 Macro Market Outlook FinalOkinawan P.SNo ratings yet

- 0RBIBULLETIN2D1CE48Document200 pages0RBIBULLETIN2D1CE48sp78gxmfkrNo ratings yet

- BFSI Q4FY24 - Earnings Preview - 090424 - 09-04-2024 - 11Document15 pagesBFSI Q4FY24 - Earnings Preview - 090424 - 09-04-2024 - 11Haardik GandhiNo ratings yet

- Monetary PolicyDocument2 pagesMonetary PolicyFuture Leaders of the PhilippinesNo ratings yet

- End of Cheap Deposits: Implications For Banks' Deposit Betas, Asset Growth, and FundingDocument9 pagesEnd of Cheap Deposits: Implications For Banks' Deposit Betas, Asset Growth, and FundingMinzhe LiNo ratings yet

- Mirae Macro Update 23 Jun 2023 June Policy Rate Decision, RemainDocument5 pagesMirae Macro Update 23 Jun 2023 June Policy Rate Decision, Remainbotoy26No ratings yet

- Quick TestDocument7 pagesQuick TestLittle RariesNo ratings yet

- Jawaban CaseDocument4 pagesJawaban CaseLittle RariesNo ratings yet

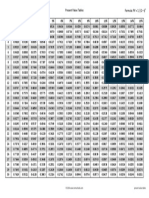

- Tabel PV of 1Document1 pageTabel PV of 1Little RariesNo ratings yet

- Tabel PV AnnuityDocument1 pageTabel PV AnnuityLittle RariesNo ratings yet

- Tealicious Class ScheduleDocument1 pageTealicious Class ScheduleLittle RariesNo ratings yet

- Own Mahmood PresiDocument3 pagesOwn Mahmood PresiOwn AbbadiNo ratings yet

- Ecom525 SyllabusDocument2 pagesEcom525 Syllabusastitvaawasthi33No ratings yet

- The Time Value of Money: ExampleDocument4 pagesThe Time Value of Money: ExampleMoneca MillerNo ratings yet

- Final 1 - Chapter 1-2Document30 pagesFinal 1 - Chapter 1-2jonalyn arellanoNo ratings yet

- HUSS Study Guide - GIIS MUN 2022Document37 pagesHUSS Study Guide - GIIS MUN 2022Kashish AroraNo ratings yet

- Problämes ch05Document6 pagesProblämes ch05jessicalaurent1999No ratings yet

- Assignment: Name of Assignment: International Trade How OurDocument9 pagesAssignment: Name of Assignment: International Trade How OurAmeen IslamNo ratings yet

- Chapter-2 Central Bank and Its Functions: An Institution Such As National Bank of EthiopiaDocument44 pagesChapter-2 Central Bank and Its Functions: An Institution Such As National Bank of Ethiopiasabit hussenNo ratings yet

- Instruction: Write The Letter of The Correct AnswerDocument4 pagesInstruction: Write The Letter of The Correct Answerzanderhero30No ratings yet

- Chapter 2 - Data of MacroeconomicsDocument23 pagesChapter 2 - Data of MacroeconomicsBenny TanNo ratings yet

- Economic Factors: Demand-Consumer-Goods - AspDocument3 pagesEconomic Factors: Demand-Consumer-Goods - AspMary Joy Villaflor HepanaNo ratings yet

- A Slowing Malaysian Economy: The Circular Flow of IncomeDocument7 pagesA Slowing Malaysian Economy: The Circular Flow of IncomeMuhammad FaizanNo ratings yet

- Macroeconomics Notes Unit 3Document30 pagesMacroeconomics Notes Unit 3Eshaan GuruNo ratings yet

- Risk Management - Tutorial 4Document7 pagesRisk Management - Tutorial 4chziNo ratings yet

- PRACTICEDocument4 pagesPRACTICEtotoroc4tNo ratings yet

- Impact of Inflation Research InstitutionalDocument6 pagesImpact of Inflation Research InstitutionalVamie SamasNo ratings yet

- Macro Economics Exercise 1Document2 pagesMacro Economics Exercise 1Daisy MistyNo ratings yet

- Economic SurveyDocument11 pagesEconomic SurveycfzbscjdghNo ratings yet

- Kathleen Brooks On ForexDocument36 pagesKathleen Brooks On ForexLawalNo ratings yet

- Business Cycle and Stabilisation PolicyDocument19 pagesBusiness Cycle and Stabilisation PolicyKrunal PatelNo ratings yet

- Ch. 22 & 23 - As-AD Analysis - PostedDocument35 pagesCh. 22 & 23 - As-AD Analysis - PostedEslam HendawiNo ratings yet

- ProductivityDocument2 pagesProductivityLina SimbolonNo ratings yet

- National Income AccountingDocument25 pagesNational Income AccountingAnuska ThapaNo ratings yet

- CPI and Inflation Practice Problems - 1Document4 pagesCPI and Inflation Practice Problems - 1lixvanterNo ratings yet

- Brave New World by Ritesh JainDocument5 pagesBrave New World by Ritesh JainDeveshNo ratings yet

- Moody's - Government of ArgentinaDocument28 pagesMoody's - Government of ArgentinaCronista.com100% (1)

- Chapter OneDocument33 pagesChapter OneTesfahun GetachewNo ratings yet

- The Australian EconomyDocument35 pagesThe Australian Economybiangbiang bangNo ratings yet

- 2.1exchange Rate Parity Currency ForecastingDocument30 pages2.1exchange Rate Parity Currency ForecastingFATIN NADJWA MAZLANNo ratings yet