Download as pdf or txt

You might also like

- Principles of Corporate Finance 12Th Edition Brealey Solutions Manual Full Chapter PDFDocument35 pagesPrinciples of Corporate Finance 12Th Edition Brealey Solutions Manual Full Chapter PDFgephyreashammyql0100% (14)

- hw2 2015 Bpes SolutionsDocument7 pageshw2 2015 Bpes SolutionsDaryl Khoo Tiong Jinn100% (1)

- Here's The HAMMER You Need To Win A Mortgage DisputeDocument6 pagesHere's The HAMMER You Need To Win A Mortgage DisputeBob Hurt100% (2)

- Asc 303 Group AssignmentDocument20 pagesAsc 303 Group AssignmentSHARIFAH NUR AFIQAH BINTI SYED HISAN SABRYNo ratings yet

- Solnik & McLeavey - Global Investment 6th EdDocument5 pagesSolnik & McLeavey - Global Investment 6th Edhotmail13No ratings yet

- Appendix B Solutions To Concept ChecksDocument31 pagesAppendix B Solutions To Concept Checkshellochinp100% (1)

- How to Trade Cfds Profitably: A Trader's Guide to Successful Cfd TradingFrom EverandHow to Trade Cfds Profitably: A Trader's Guide to Successful Cfd TradingNo ratings yet

- Acc. No.: Boulton's Toy EmporiumDocument5 pagesAcc. No.: Boulton's Toy EmporiumMisty TranquilNo ratings yet

- BFF3751 Derivatives 1 Tutorial 1 Required Reading: Hull Chapter 1 Hull Chapter 2Document9 pagesBFF3751 Derivatives 1 Tutorial 1 Required Reading: Hull Chapter 1 Hull Chapter 2Fira SyawaliaNo ratings yet

- Tutorial 10 - SolutionsDocument5 pagesTutorial 10 - Solutionstrang snoopyNo ratings yet

- BB - 3 - Futures & Options - Hull - Chap - 3Document31 pagesBB - 3 - Futures & Options - Hull - Chap - 3Ibrahim KhatatbehNo ratings yet

- FIN4003 Lecture 03Document24 pagesFIN4003 Lecture 03jason leeNo ratings yet

- Tutorial 1Document24 pagesTutorial 1Fira SyawaliaNo ratings yet

- Brief - Hedge ImplementationDocument5 pagesBrief - Hedge ImplementationAnil GowdaNo ratings yet

- Questions 2Document5 pagesQuestions 2Max WolfNo ratings yet

- Refer Chap 022 SolutionsDocument5 pagesRefer Chap 022 SolutionsRahul BhangaleNo ratings yet

- International Parity Relationships & Forecasting Exchange RatesDocument33 pagesInternational Parity Relationships & Forecasting Exchange RatesKARISHMAATA2No ratings yet

- Practice Set and Solutions #3Document6 pagesPractice Set and Solutions #3ashiq amNo ratings yet

- Hedging Strategies Using FuturesDocument37 pagesHedging Strategies Using FuturesAmeen ShaikhNo ratings yet

- Soln CH 22 Futures IntroDocument5 pagesSoln CH 22 Futures IntroSilviu TrebuianNo ratings yet

- Forex Question With and Ans Upto 30Document38 pagesForex Question With and Ans Upto 30Kavan PatelNo ratings yet

- Soln CH 23 Futures CloserDocument9 pagesSoln CH 23 Futures CloserSilviu TrebuianNo ratings yet

- Future and ForwardsDocument24 pagesFuture and ForwardsamitgtsNo ratings yet

- Fundamental Value of Stocks and BondsDocument5 pagesFundamental Value of Stocks and BondsJohnson Lozano JimenezNo ratings yet

- Tutorial 2 SolutionsDocument4 pagesTutorial 2 SolutionsIvana Second EmailNo ratings yet

- Chapter 22: Futures Markets: Problem SetsDocument8 pagesChapter 22: Futures Markets: Problem SetsMehrab Jami Aumit 1812818630No ratings yet

- Parity PPPDocument42 pagesParity PPPDeus MalimaNo ratings yet

- Chapter 11: Forward and Futures Hedging, Spread, and Target StrategiesDocument9 pagesChapter 11: Forward and Futures Hedging, Spread, and Target StrategiesNam MaiNo ratings yet

- Group 5 - Case 1Document7 pagesGroup 5 - Case 1Nirmal Kumar RoyNo ratings yet

- Chapter 3 (Hedging Strategies Using Futures)Document20 pagesChapter 3 (Hedging Strategies Using Futures)afrainhossain65No ratings yet

- BMAN20072 Week 9 Problem Set 2021 - SolutionDocument4 pagesBMAN20072 Week 9 Problem Set 2021 - SolutionAlok AgrawalNo ratings yet

- Excel 19Document6 pagesExcel 19debojyotiNo ratings yet

- ProblemSet1 PDFDocument5 pagesProblemSet1 PDFjeremy AntoninNo ratings yet

- Week 4-5 Tutorial Solutions UpdatedDocument7 pagesWeek 4-5 Tutorial Solutions UpdatedAshley ChandNo ratings yet

- Bodie Essentials of Investments 12e Ch17 SM CKDocument11 pagesBodie Essentials of Investments 12e Ch17 SM CKpavistatsNo ratings yet

- BMA 12e SM CH 26 Final PDFDocument14 pagesBMA 12e SM CH 26 Final PDFNikhil ChadhaNo ratings yet

- FINS 3616 Tutorial Questions-Week 4Document6 pagesFINS 3616 Tutorial Questions-Week 4Alex WuNo ratings yet

- Soln Er Main AP, FM Chapter Forward, Futures (Shared)Document24 pagesSoln Er Main AP, FM Chapter Forward, Futures (Shared)eshitanayyarNo ratings yet

- Mining For Short-Term Micro-ArbitrageDocument24 pagesMining For Short-Term Micro-ArbitragehlehuyNo ratings yet

- Problem Set of Session 3Document8 pagesProblem Set of Session 3Pauline CavéNo ratings yet

- Lecture 5Document9 pagesLecture 5Nhung Phuong Ha NguyenNo ratings yet

- Capital Markets and PortfolioDocument7 pagesCapital Markets and PortfolioshameempalyamNo ratings yet

- Answers To Practice Questions: Managing RiskDocument11 pagesAnswers To Practice Questions: Managing RiskTestNo ratings yet

- Financial Risk Management Complete Notes PDFDocument305 pagesFinancial Risk Management Complete Notes PDFSagar KansalNo ratings yet

- Ross 7 e CH 04Document58 pagesRoss 7 e CH 04Antora HoqueNo ratings yet

- Ch05 Part 2 Questions and Problems AnswersDocument5 pagesCh05 Part 2 Questions and Problems AnswersJemma JadeNo ratings yet

- Investment & Portfolio Management FIN730: This Is January Effect Anomaly (Like July Effect in Pakistan)Document14 pagesInvestment & Portfolio Management FIN730: This Is January Effect Anomaly (Like July Effect in Pakistan)Abdul Rauf Khan100% (3)

- FRM1 SD FRMDocument4 pagesFRM1 SD FRMSheetal DisaleNo ratings yet

- Solution of InvestmentDocument74 pagesSolution of Investmentahsanmalik2050No ratings yet

- SwapsDocument12 pagesSwapsSilenceNo ratings yet

- Bonds and Their Valuation: Key Features of Bonds Bond Valuation Measuring Yield Assessing RiskDocument49 pagesBonds and Their Valuation: Key Features of Bonds Bond Valuation Measuring Yield Assessing RiskfahadaijazNo ratings yet

- Lecture Session 8 - Currency Futures Forwards Payoff ProfilesDocument8 pagesLecture Session 8 - Currency Futures Forwards Payoff Profilesapi-19974928No ratings yet

- Stake Steak: Product Paper M A Y 2 0 2 1Document12 pagesStake Steak: Product Paper M A Y 2 0 2 1JoseNo ratings yet

- South-Western: Lecture Suggestions: 5 - 1Document7 pagesSouth-Western: Lecture Suggestions: 5 - 1Kathryn TeoNo ratings yet

- Time Value of Money: Mcgraw-Hill/Irwin Corporate Finance, 7/EDocument44 pagesTime Value of Money: Mcgraw-Hill/Irwin Corporate Finance, 7/Ehuy anh leNo ratings yet

- 03 PS4 FF - SolDocument4 pages03 PS4 FF - SolhatemNo ratings yet

- Hogwarts ThemeDocument43 pagesHogwarts ThemeLeDatNo ratings yet

- McDonald Chapter5Document11 pagesMcDonald Chapter5Tu TruongNo ratings yet

- Ross FCF 11ce Ch08Document34 pagesRoss FCF 11ce Ch08amyna abhavaniNo ratings yet

- Section A: Multiple Choice Questions - Single Option: This Section Has 70 Questions Worth 1 Mark Each (Total of 70 Marks)Document24 pagesSection A: Multiple Choice Questions - Single Option: This Section Has 70 Questions Worth 1 Mark Each (Total of 70 Marks)Kenny HoNo ratings yet

- Agricultural, Energy and Metallurgical Futures ContractsDocument68 pagesAgricultural, Energy and Metallurgical Futures ContractsCan BayirNo ratings yet

- Hedging Strategies Using FuturesDocument22 pagesHedging Strategies Using FuturesMd Rayhan UddinNo ratings yet

- The Determinants of Dividend PolicyDocument4 pagesThe Determinants of Dividend PolicyShahnewaj ShaanNo ratings yet

- Questions 2Document5 pagesQuestions 2Max WolfNo ratings yet

- Answers 4Document12 pagesAnswers 4Max WolfNo ratings yet

- Answers 2Document10 pagesAnswers 2Max WolfNo ratings yet

- Superannuation Industry Supervision Regulations 1994Document105 pagesSuperannuation Industry Supervision Regulations 1994Max WolfNo ratings yet

- smsfr2010 002Document20 pagessmsfr2010 002Max WolfNo ratings yet

- Multiple Choice QuestionsDocument18 pagesMultiple Choice Questionsnadya erlyNo ratings yet

- Adv AFARDocument145 pagesAdv AFARDvcLouisNo ratings yet

- State of The European Asset Management Industry: Adapting To A New NormalDocument15 pagesState of The European Asset Management Industry: Adapting To A New NormalJuan Manuel VeronNo ratings yet

- Daily Ex 09042013Document2 pagesDaily Ex 09042013Caleb LeeNo ratings yet

- Consolidation End Solutions Demo in SAP BPCDocument36 pagesConsolidation End Solutions Demo in SAP BPCjoesaranNo ratings yet

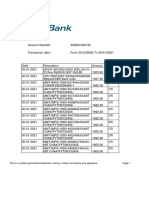

- ANZ Bank StatementDocument5 pagesANZ Bank Statement衡治洲No ratings yet

- AIS Chapter 1 Lecture NotesDocument28 pagesAIS Chapter 1 Lecture NotesNhi Ho50% (4)

- This Is A System-Generated Statement. Hence, It Does Not Require Any SignatureDocument16 pagesThis Is A System-Generated Statement. Hence, It Does Not Require Any SignatureRaju SambheNo ratings yet

- Ekotek - Alfiano Fuadi3Document50 pagesEkotek - Alfiano Fuadi3Alfiano Fuadi0% (1)

- European Union: Post Crisis Challenges and Prospects For GrowthDocument292 pagesEuropean Union: Post Crisis Challenges and Prospects For GrowtharmandoibanezNo ratings yet

- FINS 3616 Tutorial Questions-Week 7 - AnswersDocument2 pagesFINS 3616 Tutorial Questions-Week 7 - AnswersbenNo ratings yet

- 3 Adjusting Entries HandoutsDocument10 pages3 Adjusting Entries HandoutsJuan Dela CruzNo ratings yet

- 61 Fernandez Hermanos v. CIRDocument2 pages61 Fernandez Hermanos v. CIRAgus DiazNo ratings yet

- Crypto Mega Theses - MulticoinDocument12 pagesCrypto Mega Theses - MulticointempvjNo ratings yet

- BS Commerce Syllabus, UoBDocument117 pagesBS Commerce Syllabus, UoBMasood BabarNo ratings yet

- Comparative Study of Lic and Icici Pension PlanDocument67 pagesComparative Study of Lic and Icici Pension PlanNitesh Singh100% (2)

- Castillo V PascoDocument2 pagesCastillo V PascoSui50% (2)

- Nes 124 - Quiz #6Document2 pagesNes 124 - Quiz #6PatrickNo ratings yet

- The Duty of Disclosure PDFDocument8 pagesThe Duty of Disclosure PDFVusi Bhebhe83% (6)

- Account TestDocument2 pagesAccount Testajay chaudhary0% (1)

- Principles of Microeconomics 9Th Edition Sayre Test Bank Full Chapter PDFDocument67 pagesPrinciples of Microeconomics 9Th Edition Sayre Test Bank Full Chapter PDFphenicboxironicu9100% (11)

- Indian Institute of Technology: Delhi Summary Sheet Consumable StoresDocument2 pagesIndian Institute of Technology: Delhi Summary Sheet Consumable StoresSumit SinghNo ratings yet

- FA 2 Chapter 1 Control AccountsDocument19 pagesFA 2 Chapter 1 Control AccountsMhd Amin0% (1)

- HoshangABackEnd - Offer LetterDocument2 pagesHoshangABackEnd - Offer LetterShivansh GuptaNo ratings yet

- The Four Dimensions of Public Financial ManagementDocument9 pagesThe Four Dimensions of Public Financial ManagementInternational Consortium on Governmental Financial Management100% (2)

- Acca IPSAS CertificationDocument63 pagesAcca IPSAS CertificationemanOgie100% (1)

- FI S4 FunctionalitiesDocument31 pagesFI S4 FunctionalitiesNikhil KaikadeNo ratings yet