SFM Marking Scheme 2019

SFM Marking Scheme 2019

You might also like

- Chapter 5 Final Income Taxation Summary BanggawanDocument8 pagesChapter 5 Final Income Taxation Summary Banggawanyours truly,100% (3)

- Spring 1999: Problem 1Document30 pagesSpring 1999: Problem 1ShubhamNo ratings yet

- National Senior Certificate: Grade 12Document9 pagesNational Senior Certificate: Grade 12Raeesa SNo ratings yet

- Financial Analysis of ApexDocument31 pagesFinancial Analysis of ApexAfrid Khan100% (1)

- Accounting NSC P1 Memo Nov 2022 EngDocument12 pagesAccounting NSC P1 Memo Nov 2022 EngItumeleng MogoleNo ratings yet

- 4AC1 02 Rms 20210604Document11 pages4AC1 02 Rms 20210604attackdfg2002No ratings yet

- Accounting P1 Nov 2022 MG EngDocument11 pagesAccounting P1 Nov 2022 MG Engmthethwathando422No ratings yet

- Accounting Grade 12 Trial 2021 P1 and MemoDocument32 pagesAccounting Grade 12 Trial 2021 P1 and Memotsholofelokgomane29No ratings yet

- Igcse May 2022 Paper 2R MSDocument10 pagesIgcse May 2022 Paper 2R MSmihirNo ratings yet

- ACCOUNTING P2 MEMO GR10 NOV 2019 - EnglishDocument10 pagesACCOUNTING P2 MEMO GR10 NOV 2019 - EnglishmthabisovictoriaNo ratings yet

- Quiz 3 SolDocument54 pagesQuiz 3 SolBekpasha DursunovNo ratings yet

- Ms December 2021Document15 pagesMs December 2021Kuok Hei LeungNo ratings yet

- Corporate Finance - DamodaranDocument3 pagesCorporate Finance - DamodaranagustusNNo ratings yet

- Nanyang Business School AB1201 Financial Management Tutorial 8: The Basics of Capital Budgeting (Common Questions)Document4 pagesNanyang Business School AB1201 Financial Management Tutorial 8: The Basics of Capital Budgeting (Common Questions)asdsadsaNo ratings yet

- Advanced Financial Management May 2016 Past Paper and Suggested Answers Wco8ooDocument17 pagesAdvanced Financial Management May 2016 Past Paper and Suggested Answers Wco8ookaragujsNo ratings yet

- PM EdcDocument10 pagesPM EdcAlbee Koh Jia YeeNo ratings yet

- DBA 320 Exam DecDocument12 pagesDBA 320 Exam DecMabvuto PhiriNo ratings yet

- ©2016 Devry/Becker Educational Development Corp. All Rights ReservedDocument12 pages©2016 Devry/Becker Educational Development Corp. All Rights ReservedUjjal ShiwakotiNo ratings yet

- Section A: Gross ProfitDocument8 pagesSection A: Gross ProfitkangNo ratings yet

- Part A: BMME5103/JAN2013/F-AFDocument4 pagesPart A: BMME5103/JAN2013/F-AFAliNo ratings yet

- Grade 12 NSC Accounting P1 (English) September 2022 Preparatory Examination Possible AnswersDocument13 pagesGrade 12 NSC Accounting P1 (English) September 2022 Preparatory Examination Possible Answersseemaneletlhogonolo30No ratings yet

- 2020 Acc T2 Revision MEMO ENG Updated 2021Document20 pages2020 Acc T2 Revision MEMO ENG Updated 2021Palesa SemakaleNo ratings yet

- Safetex Complete Answer ICAEWDocument2 pagesSafetex Complete Answer ICAEWMuhammmad Ramzan YasinNo ratings yet

- 2017 June Mark SchemeDocument20 pages2017 June Mark SchemeMe MeNo ratings yet

- Accounting NSC P1 MG Sept 2022 Eng GautengDocument13 pagesAccounting NSC P1 MG Sept 2022 Eng GautengSweetness MakaLuthando LeocardiaNo ratings yet

- Finance 221 Problem Set 4 (Practice Problems) : SolutionsDocument9 pagesFinance 221 Problem Set 4 (Practice Problems) : SolutionsEverald SamuelsNo ratings yet

- Accounting P1 Nov 2020 Memo EngDocument9 pagesAccounting P1 Nov 2020 Memo EngBurning PhenomNo ratings yet

- CA - FM - P8 - May 23Document35 pagesCA - FM - P8 - May 23Simmi AgrawalNo ratings yet

- ACCOUNTING P1 GR11 MEMO NOVEMBER 2023 - EnglishDocument8 pagesACCOUNTING P1 GR11 MEMO NOVEMBER 2023 - EnglishChantelle IsaksNo ratings yet

- 9707 Business Studies: MARK SCHEME For The May/June 2011 Question Paper For The Guidance of TeachersDocument9 pages9707 Business Studies: MARK SCHEME For The May/June 2011 Question Paper For The Guidance of TeachersrumbidzayichatambararaNo ratings yet

- 4ac1 02 Rms 20220825Document10 pages4ac1 02 Rms 20220825attackdfg2002No ratings yet

- PT2 OM24 Question 1Document7 pagesPT2 OM24 Question 1hayatiammadNo ratings yet

- ACCOUNTING P2 MEMO GR10 NOV2020 - EnglishDocument8 pagesACCOUNTING P2 MEMO GR10 NOV2020 - Englishjordan2gardnerNo ratings yet

- Accounting Nov 2019 Nov 2019 Memo EngDocument17 pagesAccounting Nov 2019 Nov 2019 Memo Engkekedieketseng561No ratings yet

- 2015 FBS200 Year Test 2 Final Solution - Revised Fabularies June 2017Document10 pages2015 FBS200 Year Test 2 Final Solution - Revised Fabularies June 2017ger pingNo ratings yet

- Official GR 12 Accounting P1 Eng MemoDocument11 pagesOfficial GR 12 Accounting P1 Eng MemohlayisofilesNo ratings yet

- 35 Practice MCQ Solutions For Website - UPDATEDDocument7 pages35 Practice MCQ Solutions For Website - UPDATEDBaher WilliamNo ratings yet

- f9 2018 Marjun QDocument6 pagesf9 2018 Marjun QDilawar HayatNo ratings yet

- Case 4 Written Report - Third DraftDocument5 pagesCase 4 Written Report - Third DraftMarc MoralesNo ratings yet

- 03 0452 12 MS Final ScorisDocument10 pages03 0452 12 MS Final ScorisFarman FaheemNo ratings yet

- Revision Set 5 AnswerDocument8 pagesRevision Set 5 AnswerKian TuckNo ratings yet

- Academic Session 2022 MAY 2022 Semester: AssignmentDocument6 pagesAcademic Session 2022 MAY 2022 Semester: AssignmentChristopher KipsangNo ratings yet

- Pac-Sdl: Accounting Rate of Return (ARR)Document4 pagesPac-Sdl: Accounting Rate of Return (ARR)Syed Muhammad Kazim RazaNo ratings yet

- Mgmt2023: Financial Management April/May 2009 Answer KeyDocument2 pagesMgmt2023: Financial Management April/May 2009 Answer Keyshaneice_lewisNo ratings yet

- Accn p2 Memo Gr12 p2 June 2021 EnglishDocument10 pagesAccn p2 Memo Gr12 p2 June 2021 Englishmaruthamichellegwen13No ratings yet

- Cambridge IGCSE: Business Studies For Examination From 2020Document10 pagesCambridge IGCSE: Business Studies For Examination From 2020frederickNo ratings yet

- FM. Final Exam (December 2018)Document11 pagesFM. Final Exam (December 2018)elodie Helme GuizonNo ratings yet

- RGKV301 July 2022 Re-Final Exam SolutionDocument6 pagesRGKV301 July 2022 Re-Final Exam Solutionmngunisimthandile60No ratings yet

- Faculty of Commerce and LawDocument4 pagesFaculty of Commerce and LawFaith MpofuNo ratings yet

- End of Unit 3 Assessment FinalDocument8 pagesEnd of Unit 3 Assessment FinalchakiblerariNo ratings yet

- f9 Answer-Mock-Exam-F9Document9 pagesf9 Answer-Mock-Exam-F9amalthomas557No ratings yet

- Exercises - 4 (Solutions) Chapter 10, Practice QuestionsDocument7 pagesExercises - 4 (Solutions) Chapter 10, Practice QuestionsFoititika.netNo ratings yet

- Session 34 (Chap 8 9 of Titman, 2014)Document12 pagesSession 34 (Chap 8 9 of Titman, 2014)Thu Hiền KhươngNo ratings yet

- CA Inter FM ECO Suggested Answer May2023Document35 pagesCA Inter FM ECO Suggested Answer May2023sreeramireddigari abhishekreddyNo ratings yet

- Cambridge International AS & A Level: Accounting 9706/22 March 2020Document7 pagesCambridge International AS & A Level: Accounting 9706/22 March 2020Javed MushtaqNo ratings yet

- Financial Reporting II ACC 402/602, Section 1001-1002 Practice Exam 1Document12 pagesFinancial Reporting II ACC 402/602, Section 1001-1002 Practice Exam 1Joel Christian MascariñaNo ratings yet

- Grade 10 Provincial Exam Accounting P1 (English) November 2019 Possible Answers - 050305Document6 pagesGrade 10 Provincial Exam Accounting P1 (English) November 2019 Possible Answers - 050305hobyanevisionNo ratings yet

- ASE20098 Mark Scheme March 2019Document11 pagesASE20098 Mark Scheme March 2019Ti SodiumNo ratings yet

- Lecture 8 - Relative Val 2Document80 pagesLecture 8 - Relative Val 2kerenkangNo ratings yet

- Ban inDocument21 pagesBan inChi PhạmNo ratings yet

- List of the Most Important Financial Ratios: Formulas and Calculation Examples Defined for Different Types of Key Financial RatiosFrom EverandList of the Most Important Financial Ratios: Formulas and Calculation Examples Defined for Different Types of Key Financial RatiosNo ratings yet

- Conceptual Framework - Presentation and Disclosure Concepts of Capital Presentation and DisclosureDocument3 pagesConceptual Framework - Presentation and Disclosure Concepts of Capital Presentation and DisclosureEllen MaskariñoNo ratings yet

- Cost EstimationDocument7 pagesCost Estimationrubesh_rajaNo ratings yet

- BSE Limited National Stock Exchange of India LimitedDocument26 pagesBSE Limited National Stock Exchange of India LimitedYogesh MittalNo ratings yet

- Soal PBL AKD 1Document3 pagesSoal PBL AKD 1Dita EnsNo ratings yet

- Cma ArttDocument427 pagesCma ArttMUHAMMAD ALINo ratings yet

- SIBUR - 1H 2020 - Results - PresentationDocument22 pagesSIBUR - 1H 2020 - Results - Presentation757rustamNo ratings yet

- Manufacturing ReviewerDocument14 pagesManufacturing ReviewerJenifer D. CariagaNo ratings yet

- Application QuestionsDocument8 pagesApplication QuestionsAbdelnasir HaiderNo ratings yet

- Accounts 11th NotesDocument51 pagesAccounts 11th Notesaman manderNo ratings yet

- Return On Logistics AssetsDocument4 pagesReturn On Logistics Assetshina firdousNo ratings yet

- Guide To Budgeting For NGOsDocument20 pagesGuide To Budgeting For NGOssanjuanaomi100% (1)

- AK Mock BA 99.2 1st LEDocument4 pagesAK Mock BA 99.2 1st LEBromanineNo ratings yet

- Unit-1:-Introduction of Financial Management Accounting, Book Keeping & RecordingDocument5 pagesUnit-1:-Introduction of Financial Management Accounting, Book Keeping & RecordingShradha KapseNo ratings yet

- Final Book WorkDocument229 pagesFinal Book WorkAron Yohannes Gimisso100% (1)

- Vertical AnalysisDocument8 pagesVertical AnalysisHannah Mae BautistaNo ratings yet

- Message From Chairman: Achyut Prasad Prasai ChairmanDocument152 pagesMessage From Chairman: Achyut Prasad Prasai ChairmanDipesh NepalNo ratings yet

- Activity-And Strategy-Based Responsibility AccountingDocument57 pagesActivity-And Strategy-Based Responsibility AccountingMuhammad Rusydi AzizNo ratings yet

- Mark Rollinson, Carole S. Rollinson v. Commissioner of Internal Revenue, 859 F.2d 150, 4th Cir. (1988)Document3 pagesMark Rollinson, Carole S. Rollinson v. Commissioner of Internal Revenue, 859 F.2d 150, 4th Cir. (1988)Scribd Government DocsNo ratings yet

- Pre-Need Manual of Examination - CL2018 - 01Document53 pagesPre-Need Manual of Examination - CL2018 - 01Ipe ClosaNo ratings yet

- DepartmentalDocument29 pagesDepartmentalnus jahanNo ratings yet

- Rallis India Limited, Q1 2022 Earnings Call, Jul 22, 2021Document28 pagesRallis India Limited, Q1 2022 Earnings Call, Jul 22, 2021Anurag JainNo ratings yet

- Adv Issues in CapBud - Gr2 9-02 WipDocument24 pagesAdv Issues in CapBud - Gr2 9-02 WipHimanshu GuptaNo ratings yet

- Register of Wages in Form X Rule 26 (1) or Form V Rule (29) (1) (Min. Wages Act)Document4 pagesRegister of Wages in Form X Rule 26 (1) or Form V Rule (29) (1) (Min. Wages Act)Praveen KumarNo ratings yet

- BRPT Final Report 30 September 2023Document186 pagesBRPT Final Report 30 September 2023Syafrizal ThaherNo ratings yet

- Clemente Ronaliza Auditing ProblemsDocument9 pagesClemente Ronaliza Auditing ProblemsEsse ValdezNo ratings yet

- Taxation - Vietnam (TX - VNM) : Applied SkillsDocument16 pagesTaxation - Vietnam (TX - VNM) : Applied SkillsFive FifthNo ratings yet

- Fundamental Managerial Accounting Concepts 9th Edition Edmonds Solutions ManualDocument35 pagesFundamental Managerial Accounting Concepts 9th Edition Edmonds Solutions ManualDrMichelleHutchinsonegniq100% (15)

- Team - K - CFA - Challenge - 84 - 8 (LOCALIZA)Document29 pagesTeam - K - CFA - Challenge - 84 - 8 (LOCALIZA)Giovanna WaldNo ratings yet

Download as pdf or txt

You might also like

- Chapter 5 Final Income Taxation Summary BanggawanDocument8 pagesChapter 5 Final Income Taxation Summary Banggawanyours truly,100% (3)

- Spring 1999: Problem 1Document30 pagesSpring 1999: Problem 1ShubhamNo ratings yet

- National Senior Certificate: Grade 12Document9 pagesNational Senior Certificate: Grade 12Raeesa SNo ratings yet

- Financial Analysis of ApexDocument31 pagesFinancial Analysis of ApexAfrid Khan100% (1)

- Accounting NSC P1 Memo Nov 2022 EngDocument12 pagesAccounting NSC P1 Memo Nov 2022 EngItumeleng MogoleNo ratings yet

- 4AC1 02 Rms 20210604Document11 pages4AC1 02 Rms 20210604attackdfg2002No ratings yet

- Accounting P1 Nov 2022 MG EngDocument11 pagesAccounting P1 Nov 2022 MG Engmthethwathando422No ratings yet

- Accounting Grade 12 Trial 2021 P1 and MemoDocument32 pagesAccounting Grade 12 Trial 2021 P1 and Memotsholofelokgomane29No ratings yet

- Igcse May 2022 Paper 2R MSDocument10 pagesIgcse May 2022 Paper 2R MSmihirNo ratings yet

- ACCOUNTING P2 MEMO GR10 NOV 2019 - EnglishDocument10 pagesACCOUNTING P2 MEMO GR10 NOV 2019 - EnglishmthabisovictoriaNo ratings yet

- Quiz 3 SolDocument54 pagesQuiz 3 SolBekpasha DursunovNo ratings yet

- Ms December 2021Document15 pagesMs December 2021Kuok Hei LeungNo ratings yet

- Corporate Finance - DamodaranDocument3 pagesCorporate Finance - DamodaranagustusNNo ratings yet

- Nanyang Business School AB1201 Financial Management Tutorial 8: The Basics of Capital Budgeting (Common Questions)Document4 pagesNanyang Business School AB1201 Financial Management Tutorial 8: The Basics of Capital Budgeting (Common Questions)asdsadsaNo ratings yet

- Advanced Financial Management May 2016 Past Paper and Suggested Answers Wco8ooDocument17 pagesAdvanced Financial Management May 2016 Past Paper and Suggested Answers Wco8ookaragujsNo ratings yet

- PM EdcDocument10 pagesPM EdcAlbee Koh Jia YeeNo ratings yet

- DBA 320 Exam DecDocument12 pagesDBA 320 Exam DecMabvuto PhiriNo ratings yet

- ©2016 Devry/Becker Educational Development Corp. All Rights ReservedDocument12 pages©2016 Devry/Becker Educational Development Corp. All Rights ReservedUjjal ShiwakotiNo ratings yet

- Section A: Gross ProfitDocument8 pagesSection A: Gross ProfitkangNo ratings yet

- Part A: BMME5103/JAN2013/F-AFDocument4 pagesPart A: BMME5103/JAN2013/F-AFAliNo ratings yet

- Grade 12 NSC Accounting P1 (English) September 2022 Preparatory Examination Possible AnswersDocument13 pagesGrade 12 NSC Accounting P1 (English) September 2022 Preparatory Examination Possible Answersseemaneletlhogonolo30No ratings yet

- 2020 Acc T2 Revision MEMO ENG Updated 2021Document20 pages2020 Acc T2 Revision MEMO ENG Updated 2021Palesa SemakaleNo ratings yet

- Safetex Complete Answer ICAEWDocument2 pagesSafetex Complete Answer ICAEWMuhammmad Ramzan YasinNo ratings yet

- 2017 June Mark SchemeDocument20 pages2017 June Mark SchemeMe MeNo ratings yet

- Accounting NSC P1 MG Sept 2022 Eng GautengDocument13 pagesAccounting NSC P1 MG Sept 2022 Eng GautengSweetness MakaLuthando LeocardiaNo ratings yet

- Finance 221 Problem Set 4 (Practice Problems) : SolutionsDocument9 pagesFinance 221 Problem Set 4 (Practice Problems) : SolutionsEverald SamuelsNo ratings yet

- Accounting P1 Nov 2020 Memo EngDocument9 pagesAccounting P1 Nov 2020 Memo EngBurning PhenomNo ratings yet

- CA - FM - P8 - May 23Document35 pagesCA - FM - P8 - May 23Simmi AgrawalNo ratings yet

- ACCOUNTING P1 GR11 MEMO NOVEMBER 2023 - EnglishDocument8 pagesACCOUNTING P1 GR11 MEMO NOVEMBER 2023 - EnglishChantelle IsaksNo ratings yet

- 9707 Business Studies: MARK SCHEME For The May/June 2011 Question Paper For The Guidance of TeachersDocument9 pages9707 Business Studies: MARK SCHEME For The May/June 2011 Question Paper For The Guidance of TeachersrumbidzayichatambararaNo ratings yet

- 4ac1 02 Rms 20220825Document10 pages4ac1 02 Rms 20220825attackdfg2002No ratings yet

- PT2 OM24 Question 1Document7 pagesPT2 OM24 Question 1hayatiammadNo ratings yet

- ACCOUNTING P2 MEMO GR10 NOV2020 - EnglishDocument8 pagesACCOUNTING P2 MEMO GR10 NOV2020 - Englishjordan2gardnerNo ratings yet

- Accounting Nov 2019 Nov 2019 Memo EngDocument17 pagesAccounting Nov 2019 Nov 2019 Memo Engkekedieketseng561No ratings yet

- 2015 FBS200 Year Test 2 Final Solution - Revised Fabularies June 2017Document10 pages2015 FBS200 Year Test 2 Final Solution - Revised Fabularies June 2017ger pingNo ratings yet

- Official GR 12 Accounting P1 Eng MemoDocument11 pagesOfficial GR 12 Accounting P1 Eng MemohlayisofilesNo ratings yet

- 35 Practice MCQ Solutions For Website - UPDATEDDocument7 pages35 Practice MCQ Solutions For Website - UPDATEDBaher WilliamNo ratings yet

- f9 2018 Marjun QDocument6 pagesf9 2018 Marjun QDilawar HayatNo ratings yet

- Case 4 Written Report - Third DraftDocument5 pagesCase 4 Written Report - Third DraftMarc MoralesNo ratings yet

- 03 0452 12 MS Final ScorisDocument10 pages03 0452 12 MS Final ScorisFarman FaheemNo ratings yet

- Revision Set 5 AnswerDocument8 pagesRevision Set 5 AnswerKian TuckNo ratings yet

- Academic Session 2022 MAY 2022 Semester: AssignmentDocument6 pagesAcademic Session 2022 MAY 2022 Semester: AssignmentChristopher KipsangNo ratings yet

- Pac-Sdl: Accounting Rate of Return (ARR)Document4 pagesPac-Sdl: Accounting Rate of Return (ARR)Syed Muhammad Kazim RazaNo ratings yet

- Mgmt2023: Financial Management April/May 2009 Answer KeyDocument2 pagesMgmt2023: Financial Management April/May 2009 Answer Keyshaneice_lewisNo ratings yet

- Accn p2 Memo Gr12 p2 June 2021 EnglishDocument10 pagesAccn p2 Memo Gr12 p2 June 2021 Englishmaruthamichellegwen13No ratings yet

- Cambridge IGCSE: Business Studies For Examination From 2020Document10 pagesCambridge IGCSE: Business Studies For Examination From 2020frederickNo ratings yet

- FM. Final Exam (December 2018)Document11 pagesFM. Final Exam (December 2018)elodie Helme GuizonNo ratings yet

- RGKV301 July 2022 Re-Final Exam SolutionDocument6 pagesRGKV301 July 2022 Re-Final Exam Solutionmngunisimthandile60No ratings yet

- Faculty of Commerce and LawDocument4 pagesFaculty of Commerce and LawFaith MpofuNo ratings yet

- End of Unit 3 Assessment FinalDocument8 pagesEnd of Unit 3 Assessment FinalchakiblerariNo ratings yet

- f9 Answer-Mock-Exam-F9Document9 pagesf9 Answer-Mock-Exam-F9amalthomas557No ratings yet

- Exercises - 4 (Solutions) Chapter 10, Practice QuestionsDocument7 pagesExercises - 4 (Solutions) Chapter 10, Practice QuestionsFoititika.netNo ratings yet

- Session 34 (Chap 8 9 of Titman, 2014)Document12 pagesSession 34 (Chap 8 9 of Titman, 2014)Thu Hiền KhươngNo ratings yet

- CA Inter FM ECO Suggested Answer May2023Document35 pagesCA Inter FM ECO Suggested Answer May2023sreeramireddigari abhishekreddyNo ratings yet

- Cambridge International AS & A Level: Accounting 9706/22 March 2020Document7 pagesCambridge International AS & A Level: Accounting 9706/22 March 2020Javed MushtaqNo ratings yet

- Financial Reporting II ACC 402/602, Section 1001-1002 Practice Exam 1Document12 pagesFinancial Reporting II ACC 402/602, Section 1001-1002 Practice Exam 1Joel Christian MascariñaNo ratings yet

- Grade 10 Provincial Exam Accounting P1 (English) November 2019 Possible Answers - 050305Document6 pagesGrade 10 Provincial Exam Accounting P1 (English) November 2019 Possible Answers - 050305hobyanevisionNo ratings yet

- ASE20098 Mark Scheme March 2019Document11 pagesASE20098 Mark Scheme March 2019Ti SodiumNo ratings yet

- Lecture 8 - Relative Val 2Document80 pagesLecture 8 - Relative Val 2kerenkangNo ratings yet

- Ban inDocument21 pagesBan inChi PhạmNo ratings yet

- List of the Most Important Financial Ratios: Formulas and Calculation Examples Defined for Different Types of Key Financial RatiosFrom EverandList of the Most Important Financial Ratios: Formulas and Calculation Examples Defined for Different Types of Key Financial RatiosNo ratings yet

- Conceptual Framework - Presentation and Disclosure Concepts of Capital Presentation and DisclosureDocument3 pagesConceptual Framework - Presentation and Disclosure Concepts of Capital Presentation and DisclosureEllen MaskariñoNo ratings yet

- Cost EstimationDocument7 pagesCost Estimationrubesh_rajaNo ratings yet

- BSE Limited National Stock Exchange of India LimitedDocument26 pagesBSE Limited National Stock Exchange of India LimitedYogesh MittalNo ratings yet

- Soal PBL AKD 1Document3 pagesSoal PBL AKD 1Dita EnsNo ratings yet

- Cma ArttDocument427 pagesCma ArttMUHAMMAD ALINo ratings yet

- SIBUR - 1H 2020 - Results - PresentationDocument22 pagesSIBUR - 1H 2020 - Results - Presentation757rustamNo ratings yet

- Manufacturing ReviewerDocument14 pagesManufacturing ReviewerJenifer D. CariagaNo ratings yet

- Application QuestionsDocument8 pagesApplication QuestionsAbdelnasir HaiderNo ratings yet

- Accounts 11th NotesDocument51 pagesAccounts 11th Notesaman manderNo ratings yet

- Return On Logistics AssetsDocument4 pagesReturn On Logistics Assetshina firdousNo ratings yet

- Guide To Budgeting For NGOsDocument20 pagesGuide To Budgeting For NGOssanjuanaomi100% (1)

- AK Mock BA 99.2 1st LEDocument4 pagesAK Mock BA 99.2 1st LEBromanineNo ratings yet

- Unit-1:-Introduction of Financial Management Accounting, Book Keeping & RecordingDocument5 pagesUnit-1:-Introduction of Financial Management Accounting, Book Keeping & RecordingShradha KapseNo ratings yet

- Final Book WorkDocument229 pagesFinal Book WorkAron Yohannes Gimisso100% (1)

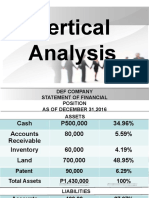

- Vertical AnalysisDocument8 pagesVertical AnalysisHannah Mae BautistaNo ratings yet

- Message From Chairman: Achyut Prasad Prasai ChairmanDocument152 pagesMessage From Chairman: Achyut Prasad Prasai ChairmanDipesh NepalNo ratings yet

- Activity-And Strategy-Based Responsibility AccountingDocument57 pagesActivity-And Strategy-Based Responsibility AccountingMuhammad Rusydi AzizNo ratings yet

- Mark Rollinson, Carole S. Rollinson v. Commissioner of Internal Revenue, 859 F.2d 150, 4th Cir. (1988)Document3 pagesMark Rollinson, Carole S. Rollinson v. Commissioner of Internal Revenue, 859 F.2d 150, 4th Cir. (1988)Scribd Government DocsNo ratings yet

- Pre-Need Manual of Examination - CL2018 - 01Document53 pagesPre-Need Manual of Examination - CL2018 - 01Ipe ClosaNo ratings yet

- DepartmentalDocument29 pagesDepartmentalnus jahanNo ratings yet

- Rallis India Limited, Q1 2022 Earnings Call, Jul 22, 2021Document28 pagesRallis India Limited, Q1 2022 Earnings Call, Jul 22, 2021Anurag JainNo ratings yet

- Adv Issues in CapBud - Gr2 9-02 WipDocument24 pagesAdv Issues in CapBud - Gr2 9-02 WipHimanshu GuptaNo ratings yet

- Register of Wages in Form X Rule 26 (1) or Form V Rule (29) (1) (Min. Wages Act)Document4 pagesRegister of Wages in Form X Rule 26 (1) or Form V Rule (29) (1) (Min. Wages Act)Praveen KumarNo ratings yet

- BRPT Final Report 30 September 2023Document186 pagesBRPT Final Report 30 September 2023Syafrizal ThaherNo ratings yet

- Clemente Ronaliza Auditing ProblemsDocument9 pagesClemente Ronaliza Auditing ProblemsEsse ValdezNo ratings yet

- Taxation - Vietnam (TX - VNM) : Applied SkillsDocument16 pagesTaxation - Vietnam (TX - VNM) : Applied SkillsFive FifthNo ratings yet

- Fundamental Managerial Accounting Concepts 9th Edition Edmonds Solutions ManualDocument35 pagesFundamental Managerial Accounting Concepts 9th Edition Edmonds Solutions ManualDrMichelleHutchinsonegniq100% (15)

- Team - K - CFA - Challenge - 84 - 8 (LOCALIZA)Document29 pagesTeam - K - CFA - Challenge - 84 - 8 (LOCALIZA)Giovanna WaldNo ratings yet