Download as pdf or txt

You might also like

- Nigerian Minerals and Mining Regulations 2011Document222 pagesNigerian Minerals and Mining Regulations 2011PRASANJIT MISHRA50% (2)

- Acr Core Buyer Price List 11-12-20Document103 pagesAcr Core Buyer Price List 11-12-20Bret HelgesonNo ratings yet

- Chems - List - Updated For 2020Document4 pagesChems - List - Updated For 2020gdubxNo ratings yet

- 01 - Pressure Reducing ValveDocument132 pages01 - Pressure Reducing ValveHydro NguyenNo ratings yet

- New Peiner Grab Accessories ServiceDocument97 pagesNew Peiner Grab Accessories ServiceJorge Jr Chuatoco100% (2)

- TCC202 Cementing Equipment Manual Version 1.01cDocument56 pagesTCC202 Cementing Equipment Manual Version 1.01cFrancisco Wilson Bezerra Francisco100% (3)

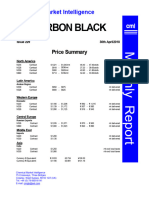

- Issue No 228 March 2018Document53 pagesIssue No 228 March 2018Luna ChenNo ratings yet

- Issue No 229 April 2018Document40 pagesIssue No 229 April 2018Luna ChenNo ratings yet

- Commodity Mantra Pre-Market 020611Document5 pagesCommodity Mantra Pre-Market 020611imukulguptaNo ratings yet

- WINDSORDocument7 pagesWINDSORkartik sharmaNo ratings yet

- Budget (Additional)Document4 pagesBudget (Additional)Mehari GebreyohannesNo ratings yet

- Weekly Recap Jan 15Document1 pageWeekly Recap Jan 15Daviduta IonutNo ratings yet

- North $509,283 $553,887 109% South $483,519 $511,115 106% East $640,603 $606,603 95% West $320,312 $382,753 119%Document17 pagesNorth $509,283 $553,887 109% South $483,519 $511,115 106% East $640,603 $606,603 95% West $320,312 $382,753 119%Hussain AminNo ratings yet

- Weekly Cattle Market Update: For The Week Ending May 1, 2020Document4 pagesWeekly Cattle Market Update: For The Week Ending May 1, 2020jenNo ratings yet

- 2024 05 08 09 30 CJ Services BackupDocument1 page2024 05 08 09 30 CJ Services Backupfortesupermercado2No ratings yet

- Planilha Moral Do Gelo - STNDocument20 pagesPlanilha Moral Do Gelo - STNPivetim ManeiroNo ratings yet

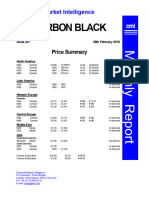

- Issue No 227 February 2018Document34 pagesIssue No 227 February 2018Luna ChenNo ratings yet

- Quotation Final 20231107 BenkanDocument2 pagesQuotation Final 20231107 Benkanchtoil2020No ratings yet

- 1.23.18 MM Sector Update Rel ValDocument44 pages1.23.18 MM Sector Update Rel ValTony NguyenNo ratings yet

- Ethanol Market and Pricing Report 05222024Document16 pagesEthanol Market and Pricing Report 05222024Christian Yao AmegaviNo ratings yet

- Metal and MiningDocument8 pagesMetal and MiningSumit SharmaNo ratings yet

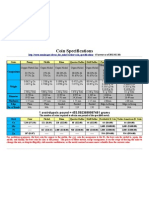

- Coin SpecificationsDocument1 pageCoin SpecificationsrumgodNo ratings yet

- Cattle Situation and OutlookDocument19 pagesCattle Situation and OutlookSaipolNo ratings yet

- Variación Del Punto de Equilibrio Ante Variación Del Costo FijoDocument18 pagesVariación Del Punto de Equilibrio Ante Variación Del Costo FijoHector MacavilcaNo ratings yet

- BG G MH Oasis L700Document2 pagesBG G MH Oasis L700Long Nguyễn ThànhNo ratings yet

- BG G MH Oasis L700Document2 pagesBG G MH Oasis L700Long Nguyễn ThànhNo ratings yet

- Cmu170420 3Document4 pagesCmu170420 3jenNo ratings yet

- Alex Hendel - Schedule of Start Up Funds - Sheet1Document2 pagesAlex Hendel - Schedule of Start Up Funds - Sheet1api-591478454No ratings yet

- RBS - Round Up 300610Document9 pagesRBS - Round Up 300610egolistocksNo ratings yet

- Tipo MOV VLR Unit Cantidad VLR Total Base GravDocument3 pagesTipo MOV VLR Unit Cantidad VLR Total Base GravSandra NievesNo ratings yet

- Campanha Atacado Junho 2022Document1 pageCampanha Atacado Junho 2022Lucas ScrazoloNo ratings yet

- BG G MH Oasis A03 Flat AwningDocument4 pagesBG G MH Oasis A03 Flat AwningLong Nguyễn ThànhNo ratings yet

- Distribution Rates For 2020 - Copia - OdsDocument6 pagesDistribution Rates For 2020 - Copia - OdsMónica Lucía Jiménez ManriqueNo ratings yet

- ANZ Commodity Daily 610 260412Document5 pagesANZ Commodity Daily 610 260412David4564654No ratings yet

- Tabela de Vendas - Jardins FrançaDocument9 pagesTabela de Vendas - Jardins FrançaCaio GraccoNo ratings yet

- Portal 2001 ReaisDocument4 pagesPortal 2001 ReaisdenisaosharpNo ratings yet

- Cópia de Atividade 2 Soma, DIV, Mult, SUB 0Document17 pagesCópia de Atividade 2 Soma, DIV, Mult, SUB 0Informatica CECAPINo ratings yet

- Planilha GerenciamentoDocument10 pagesPlanilha Gerenciamentorafaeljairo21No ratings yet

- Planilha GerenciamentoDocument10 pagesPlanilha Gerenciamentorafaeljairo21No ratings yet

- ANZ Commodity Daily 718 041012Document5 pagesANZ Commodity Daily 718 041012anon_370534332No ratings yet

- Tarea Silver MealDocument4 pagesTarea Silver MealsyedtalhamanzarNo ratings yet

- Aboaboso DraftDocument12 pagesAboaboso DraftProsper AabullehNo ratings yet

- Analisis Suturas 2020Document6 pagesAnalisis Suturas 2020David SantoandreNo ratings yet

- Minerals-Energy-Outlook-May-2024- NABDocument5 pagesMinerals-Energy-Outlook-May-2024- NABhengkyn.daulayNo ratings yet

- Costing Waka Waka Items No. of Pieces Cost Shipping Total InvestmentDocument5 pagesCosting Waka Waka Items No. of Pieces Cost Shipping Total InvestmentPatricia Andrei De GuzmanNo ratings yet

- Plano Meta FixaDocument22 pagesPlano Meta FixaTiago VargasNo ratings yet

- Bunkers Consumption: USD USDDocument2 pagesBunkers Consumption: USD USDTakis RappasNo ratings yet

- Raele FSDocument11 pagesRaele FSAring BaquiranNo ratings yet

- Update Proforma Invoice YYH220927Document3 pagesUpdate Proforma Invoice YYH220927jesus RodriguezNo ratings yet

- Modelo para Regularizar Mais de Um Item Da NFDocument37 pagesModelo para Regularizar Mais de Um Item Da NFLaura TobiasNo ratings yet

- BG G MH Oasis l331-l332Document4 pagesBG G MH Oasis l331-l332Long Nguyễn ThànhNo ratings yet

- BG G MH OASIS L960 Sky AwningDocument4 pagesBG G MH OASIS L960 Sky AwningLong Nguyễn ThànhNo ratings yet

- Working With Cells, Rows and ColumnsDocument6 pagesWorking With Cells, Rows and ColumnsjovanniNo ratings yet

- Calculo Activ Lotes Bra50Document44 pagesCalculo Activ Lotes Bra50wendvieiraNo ratings yet

- Planilha MercadoDocument47 pagesPlanilha MercadoMattNo ratings yet

- Kode Barang Laba Kotor/Unit Laba TotalDocument7 pagesKode Barang Laba Kotor/Unit Laba TotalRaihan Rohadatul 'AisyNo ratings yet

- Ordenes Juntas 4185-4186 NuevasDocument6 pagesOrdenes Juntas 4185-4186 NuevasAngelo Bruno Camargo BenitesNo ratings yet

- Model Prefix PM Type: PM Kit/Parts (STD) PM Kit Discount (10%)Document23 pagesModel Prefix PM Type: PM Kit/Parts (STD) PM Kit Discount (10%)jogremaurNo ratings yet

- Winder FRP Pressure Vessel Price - RyanDocument11 pagesWinder FRP Pressure Vessel Price - RyanAbraham GarciaNo ratings yet

- Budget 2Document9 pagesBudget 2Mehari GebreyohannesNo ratings yet

- ANZ Commodity Daily 631 250512Document5 pagesANZ Commodity Daily 631 250512ChrisBeckerNo ratings yet

- Race Fuel Prices 2010Document2 pagesRace Fuel Prices 2010info7922No ratings yet

- Assignment 2Document9 pagesAssignment 2ThomasNo ratings yet

- TANZANIA Mining Industry Investor Guide - June 2015 - 1 SWDocument48 pagesTANZANIA Mining Industry Investor Guide - June 2015 - 1 SWPRASANJIT MISHRANo ratings yet

- Business Name ReservationDocument1 pageBusiness Name ReservationPRASANJIT MISHRANo ratings yet

- sitesdefaultfilespdfsmigrate17614IIED PDFDocument79 pagessitesdefaultfilespdfsmigrate17614IIED PDFPRASANJIT MISHRANo ratings yet

- 12142018183322ferro Alloys IMYB 2017Document27 pages12142018183322ferro Alloys IMYB 2017PRASANJIT MISHRANo ratings yet

- Economics Sem - 1Document229 pagesEconomics Sem - 1PRASANJIT MISHRANo ratings yet

- Evolution of Green Steel Market Dynamics in Europe 1680545075Document4 pagesEvolution of Green Steel Market Dynamics in Europe 1680545075PRASANJIT MISHRANo ratings yet

- New Paper With SAC ISRO 1680544531Document4 pagesNew Paper With SAC ISRO 1680544531PRASANJIT MISHRANo ratings yet

- Information Technology For ManagersDocument169 pagesInformation Technology For ManagersPRASANJIT MISHRANo ratings yet

- Accounting For Manager DDocument315 pagesAccounting For Manager DPRASANJIT MISHRANo ratings yet

- Nigeruian Minerals and Mining Act, 2007Document60 pagesNigeruian Minerals and Mining Act, 2007PRASANJIT MISHRANo ratings yet

- JD Mining Shift EngineerDocument1 pageJD Mining Shift EngineerPRASANJIT MISHRANo ratings yet

- NG Government Gazette Dated 2011 07 15 No 124Document232 pagesNG Government Gazette Dated 2011 07 15 No 124PRASANJIT MISHRANo ratings yet

- JD Quarry ManagerDocument1 pageJD Quarry ManagerPRASANJIT MISHRANo ratings yet

- Abul Hassan CV As A Boiler TechnicianDocument3 pagesAbul Hassan CV As A Boiler Technicianmuhammad75makeNo ratings yet

- Ficha Tecnica 2 PDFDocument2 pagesFicha Tecnica 2 PDFrosmeryNo ratings yet

- Interpretations To Asme b31 3Document17 pagesInterpretations To Asme b31 3Phornlert WanaNo ratings yet

- Basic Engine D12DDocument11 pagesBasic Engine D12DHamilton Miranda100% (7)

- Module 3: Sequence Components and Fault Analysis: Sequence ComponentsDocument11 pagesModule 3: Sequence Components and Fault Analysis: Sequence Componentssunny1725No ratings yet

- Fuersteneau Power Model (See Mill Power - Ball Mills Spreadsheet For Further Details On Such Model)Document3 pagesFuersteneau Power Model (See Mill Power - Ball Mills Spreadsheet For Further Details On Such Model)Rolando QuispeNo ratings yet

- Homework #1 WorkDocument5 pagesHomework #1 WorkM NabilNo ratings yet

- Rickmeier 34Document12 pagesRickmeier 34carlosNo ratings yet

- Datos Tecnicos Quemador OVENPAK 400 PDFDocument8 pagesDatos Tecnicos Quemador OVENPAK 400 PDFIsaias de la CruzNo ratings yet

- Thermodynamics States A Set of Four Laws Which Are Valid For All Systems That Fall Within The Constraints Implied by EachDocument2 pagesThermodynamics States A Set of Four Laws Which Are Valid For All Systems That Fall Within The Constraints Implied by EachKevin Alberto Tejera PereiraNo ratings yet

- PVM (X) Series: Vertical Multistage PumpsDocument11 pagesPVM (X) Series: Vertical Multistage PumpsNelson IglesiasNo ratings yet

- Microwave TubesDocument139 pagesMicrowave TubesGopichand DasariNo ratings yet

- Functional Role of Ge (Maintenance) 17 May 2016Document3 pagesFunctional Role of Ge (Maintenance) 17 May 2016Sri WatsonNo ratings yet

- Fosfa Certificate of Compliance, Cleanliness and Suitability of Ship'S TankDocument2 pagesFosfa Certificate of Compliance, Cleanliness and Suitability of Ship'S Tanknatasha manobanNo ratings yet

- Coatings Word November 2011Document52 pagesCoatings Word November 2011sami_sakrNo ratings yet

- Grass Crete PaversDocument12 pagesGrass Crete Paversprerna93No ratings yet

- Fluid Power Graphic SymbolsDocument24 pagesFluid Power Graphic SymbolsJShearer94% (16)

- PHYSICS 2048 - Quiz - 04 - 02Document2 pagesPHYSICS 2048 - Quiz - 04 - 02alphacetaNo ratings yet

- TMEIC Container Crane ModernizationDocument8 pagesTMEIC Container Crane ModernizationBoy AlfredoNo ratings yet

- Mini and Metro Engine Numbers CCDocument11 pagesMini and Metro Engine Numbers CCFrancesco Matteoli0% (1)

- Solar y CaterpillarDocument48 pagesSolar y CaterpillarRobert BlancoNo ratings yet

- Independent Driving Pattern Factors and Their in Uence On Fuel-Use and Exhaust Emission FactorsDocument21 pagesIndependent Driving Pattern Factors and Their in Uence On Fuel-Use and Exhaust Emission FactorssigitNo ratings yet

- Knowledge Generates Economy ENDocument20 pagesKnowledge Generates Economy ENDavid DragosNo ratings yet

- BirpowerDocument236 pagesBirpowerRajesh KumarNo ratings yet

- DOOSAN Air Compressors 12 150 en DoosanDocument2 pagesDOOSAN Air Compressors 12 150 en DoosanMehman NasibovNo ratings yet

- VFD DrawingsDocument24 pagesVFD DrawingsShrikant KajaleNo ratings yet

- Inter 2 Physics Success SeriesDocument12 pagesInter 2 Physics Success SeriesZain AliNo ratings yet