HDFC Defence Fund - Presentation - May 23

HDFC Defence Fund - Presentation - May 23

You might also like

- Infinity Hunger Games 2018Document4 pagesInfinity Hunger Games 2018Anonymous KdzgEHNo ratings yet

- Wargames Illustrated #026Document56 pagesWargames Illustrated #026Анатолий Золотухин100% (1)

- Howard - Forgotten Dimensions of StrategyDocument13 pagesHoward - Forgotten Dimensions of StrategyEdward LeeNo ratings yet

- Leaflet - HDFC Defence Fund NFO (May 2023) - 2Document4 pagesLeaflet - HDFC Defence Fund NFO (May 2023) - 2Akshay ChaudhryNo ratings yet

- Activism GreenspanDocument18 pagesActivism GreenspannewagedanteNo ratings yet

- Macroeconomic Determinants of Stock Market Development: Evidence From Borsa IstanbulDocument21 pagesMacroeconomic Determinants of Stock Market Development: Evidence From Borsa IstanbulMaria KulawikNo ratings yet

- China S Sovereign Wealth Fund Weakness and ChallengesDocument16 pagesChina S Sovereign Wealth Fund Weakness and ChallengesWendy MúsicaNo ratings yet

- The Dash To Trash and The Grab For Growth (01.15.08)Document16 pagesThe Dash To Trash and The Grab For Growth (01.15.08)BunNo ratings yet

- TICAD Africa 2050-Chapter2-V2Document32 pagesTICAD Africa 2050-Chapter2-V2AbdallaNo ratings yet

- International Value Investing (Updated)Document11 pagesInternational Value Investing (Updated)eric_stNo ratings yet

- Oil&gasDocument23 pagesOil&gasPriyankaKesariNo ratings yet

- ECO302: Intermediate Macroeconomic Theory I: Spring 2021Document27 pagesECO302: Intermediate Macroeconomic Theory I: Spring 2021Nafew ProdhanNo ratings yet

- Federal Funds Rate NASDAQ Timeline: June, 1995 April, 1996 January, 1999Document6 pagesFederal Funds Rate NASDAQ Timeline: June, 1995 April, 1996 January, 1999Aditya NevrekarNo ratings yet

- Bruegel March2010 Ext PubDocument19 pagesBruegel March2010 Ext PubBruegelNo ratings yet

- The Plateau in Cinema Attendances and Drop in Video Sales in The UK The Role of Digital Leisure Substitutes 2006 10 10Document25 pagesThe Plateau in Cinema Attendances and Drop in Video Sales in The UK The Role of Digital Leisure Substitutes 2006 10 10Eliza L. KormazopoulosNo ratings yet

- 2 Growth Trends in National IncomeDocument29 pages2 Growth Trends in National IncomeDheeraj Budhiraja0% (1)

- Lecturenote 1 2 24Document27 pagesLecturenote 1 2 24채영No ratings yet

- Inflation Indexed Bonds.Document81 pagesInflation Indexed Bonds.Mythili InnconNo ratings yet

- Economicdisintegrationofthe European UnionDocument11 pagesEconomicdisintegrationofthe European UnionHabib EjazNo ratings yet

- Undernourishment Around The World in 2010: The Number of Undernourished People Has Declined But Remains Unacceptably HighDocument4 pagesUndernourishment Around The World in 2010: The Number of Undernourished People Has Declined But Remains Unacceptably HighKoert OosterhuisNo ratings yet

- PIPP WK 3 - Organised Interests, Power and Public Policy 2023-241.0Document12 pagesPIPP WK 3 - Organised Interests, Power and Public Policy 2023-241.0aliejazmirNo ratings yet

- Etf Playbook 1Document12 pagesEtf Playbook 1langlinglung1985No ratings yet

- GlobalizationDocument2 pagesGlobalizationAngelika C PauleNo ratings yet

- Diagnosis of Sri Lanka's Current Economic Crisis and Potential Solutions - CFA Sri Lanka - 10 Sep 2021 - DistributeDocument128 pagesDiagnosis of Sri Lanka's Current Economic Crisis and Potential Solutions - CFA Sri Lanka - 10 Sep 2021 - DistributeganrajNo ratings yet

- FM474 Lecture 5 - Risk and ReturnDocument58 pagesFM474 Lecture 5 - Risk and Returnjie.ji3No ratings yet

- Concept of Unit Linked ProductsDocument37 pagesConcept of Unit Linked Productsapi-19794187No ratings yet

- Financial Risk Management Philippe Jorion 1 Financial Risk ManagementDocument17 pagesFinancial Risk Management Philippe Jorion 1 Financial Risk ManagementWaqasAhmadNo ratings yet

- Lazard Investment - An Introduction To The Emerging Market Debt Asset ClassDocument8 pagesLazard Investment - An Introduction To The Emerging Market Debt Asset ClassPranjayNo ratings yet

- Rice SubsidiesDocument5 pagesRice SubsidiesAbbas KhanNo ratings yet

- 1 - Jan Longeval, Managing Director, Bank Degroof - Are PensDocument25 pages1 - Jan Longeval, Managing Director, Bank Degroof - Are Penspensiontalk100% (1)

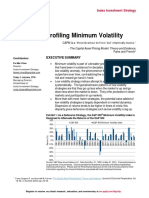

- Profiling Minimum Volatility: Executive SummaryDocument10 pagesProfiling Minimum Volatility: Executive SummaryCalvin YeohNo ratings yet

- Chilean Productivity Presentation-Chad SyversonDocument15 pagesChilean Productivity Presentation-Chad SyversonYorka SánchezNo ratings yet

- AIFI Corso 2016 - Daniele PilchardDocument58 pagesAIFI Corso 2016 - Daniele Pilcharddaniele.pilchard6465No ratings yet

- Macroeconomic Stability: The More The Better?Document27 pagesMacroeconomic Stability: The More The Better?Roselyn Mahinay QuilongquilongNo ratings yet

- SME and Micro Financing: Malaysia's ExperienceDocument67 pagesSME and Micro Financing: Malaysia's Experiencedharmeshmehta31No ratings yet

- MasteringWealthManagement Oct8 2023Document36 pagesMasteringWealthManagement Oct8 2023lakshmi_gamini_1No ratings yet

- Etf Playbook WebDocument12 pagesEtf Playbook WebquangdatphungNo ratings yet

- 13 Chapter 5 InflationDocument36 pages13 Chapter 5 InflationchinuNo ratings yet

- Moeller Et Al. JFDocument26 pagesMoeller Et Al. JFbenjaminNo ratings yet

- KKEK4325 Petroleum Engineering: Assignment 1Document7 pagesKKEK4325 Petroleum Engineering: Assignment 1Muzammil IqbalNo ratings yet

- Effect of Economic Growth On Unemployment and Validity of Okun's Law in MauritiusDocument20 pagesEffect of Economic Growth On Unemployment and Validity of Okun's Law in MauritiusImam Arief PambudiNo ratings yet

- THE Growth and Transformation of The Iiaalaysian Economy and The I'',Iplications FOR Development PianningDocument9 pagesTHE Growth and Transformation of The Iiaalaysian Economy and The I'',Iplications FOR Development PianningKhairul AnuarNo ratings yet

- Excessive Optimism A Short RecessionDocument13 pagesExcessive Optimism A Short RecessionMahad SheikhNo ratings yet

- Overview On Risk in Int BsnsDocument34 pagesOverview On Risk in Int BsnsUmesh ChandraNo ratings yet

- Voituriez - 2001 - What Explains Price Volatility Changes in Commodity Markets Answers From The World Palm-Oil MarketDocument8 pagesVoituriez - 2001 - What Explains Price Volatility Changes in Commodity Markets Answers From The World Palm-Oil MarketFarhah ADNo ratings yet

- Macroeconomics I: Open EconomyDocument26 pagesMacroeconomics I: Open EconomyAlèxia SalvadorNo ratings yet

- Housing and Mortgage Market Update: Philadelphia Council For Business EconomicsDocument16 pagesHousing and Mortgage Market Update: Philadelphia Council For Business EconomicsZerohedgeNo ratings yet

- Lecture 1 PDFDocument23 pagesLecture 1 PDFHawar HANo ratings yet

- Survival of Euro Section-BDocument26 pagesSurvival of Euro Section-BKumar RaunakNo ratings yet

- How Will Real Estate Cap Rates Respond To The Rise in The Fed Funds Rate - 2022 06 23 134238 - UnuiDocument11 pagesHow Will Real Estate Cap Rates Respond To The Rise in The Fed Funds Rate - 2022 06 23 134238 - Unuisascha.kiserNo ratings yet

- Inflation and Price ChangesDocument7 pagesInflation and Price ChangesRica AniñonNo ratings yet

- Econ Macro 5th Edition Mceachern Solutions ManualDocument4 pagesEcon Macro 5th Edition Mceachern Solutions Manualraphaelbacrqu100% (36)

- Fama DB Prize Market Efficiency October 2005Document15 pagesFama DB Prize Market Efficiency October 2005Nathan AwNo ratings yet

- Unido: (United Nation Industrial Development)Document7 pagesUnido: (United Nation Industrial Development)Kyla JadjurieNo ratings yet

- An International Analysis of The Economic Cost - 2020 - Research in InternationaDocument15 pagesAn International Analysis of The Economic Cost - 2020 - Research in InternationaDessy ParamitaNo ratings yet

- India and The World EconomyDocument45 pagesIndia and The World EconomyPraveen BVSNo ratings yet

- Analysis of The International Oil Price Fluctuatio PDFDocument8 pagesAnalysis of The International Oil Price Fluctuatio PDFPadma BhushanNo ratings yet

- The Relationship Between Asia Pacific Markets During The Financial Crisis: Var-Granger Causality AnalysisDocument26 pagesThe Relationship Between Asia Pacific Markets During The Financial Crisis: Var-Granger Causality AnalysisDr. Abdul BashirNo ratings yet

- Economy of JapanDocument24 pagesEconomy of JapanMohanad Al-SehetryNo ratings yet

- John KhumaloDocument12 pagesJohn KhumaloAlfian VioNo ratings yet

- A New Era of Investing Begins 1672488719Document31 pagesA New Era of Investing Begins 1672488719Octavio BrasilNo ratings yet

- Activity 1Document2 pagesActivity 1api-472469147No ratings yet

- Equity Index Performance Tracker - Mar 2024Document1 pageEquity Index Performance Tracker - Mar 2024DeepakNo ratings yet

- Invite - NFO Alert - Launch of HDFC NIFTY100 Low Volatility 30 Index FundDocument1 pageInvite - NFO Alert - Launch of HDFC NIFTY100 Low Volatility 30 Index FundDeepakNo ratings yet

- Screenshot 2024-06-21 at 8.10.54 AMDocument1 pageScreenshot 2024-06-21 at 8.10.54 AMDeepakNo ratings yet

- HDFC Children's Gift Fund Leaflet (As On 31st March 2023)Document4 pagesHDFC Children's Gift Fund Leaflet (As On 31st March 2023)DeepakNo ratings yet

- SIP Mantra - HDFC Flexi Cap Fund (Aprt 2023)Document2 pagesSIP Mantra - HDFC Flexi Cap Fund (Aprt 2023)DeepakNo ratings yet

- Leaflet - Hedged and Unhedged Exposure of Hybrid FundsDocument2 pagesLeaflet - Hedged and Unhedged Exposure of Hybrid FundsDeepakNo ratings yet

- Debt Product Suite - Upto 1 Yr - March 2023Document17 pagesDebt Product Suite - Upto 1 Yr - March 2023DeepakNo ratings yet

- HDFC NIFTY SDL+GSec Jun 2027 40-60 TMF - NFO PresentationDocument17 pagesHDFC NIFTY SDL+GSec Jun 2027 40-60 TMF - NFO PresentationDeepakNo ratings yet

- Protecting Operational Performance Worldwide: MTL Surge Protection SolutionsDocument32 pagesProtecting Operational Performance Worldwide: MTL Surge Protection SolutionsDeepakNo ratings yet

- Deepak R Chauhan FSWDocument1 pageDeepak R Chauhan FSWDeepakNo ratings yet

- Victory in The Pacific 2ED RulesDocument8 pagesVictory in The Pacific 2ED RulesAndrew SmithNo ratings yet

- 32 1 Hitler's Lightning WarDocument3 pages32 1 Hitler's Lightning WarjaiurwgghiurhfuigaewNo ratings yet

- Catalogue 2021 PanzerkampfDocument10 pagesCatalogue 2021 PanzerkampfEmeraldmoxNo ratings yet

- Codex Imperial GuardDocument43 pagesCodex Imperial GuardCole Gartner33% (3)

- Watch Prime Master (1) Watch Prime Brothers (5) Watch Attack WalkerDocument1 pageWatch Prime Master (1) Watch Prime Brothers (5) Watch Attack WalkerduduNo ratings yet

- Strategic Air WarfareDocument158 pagesStrategic Air WarfareBob AndrepontNo ratings yet

- Lion of The North - Rules & ScenariosDocument56 pagesLion of The North - Rules & ScenariosBrant McClureNo ratings yet

- D D I 1334.01 W U: O Nstruction Earing of The NiformDocument6 pagesD D I 1334.01 W U: O Nstruction Earing of The NiformJoel SofeuNo ratings yet

- OSS MotionpicturesasweaponsDocument11 pagesOSS MotionpicturesasweaponsDavid OrozcoNo ratings yet

- Intelligence and Military Operations (PDFDrive)Document481 pagesIntelligence and Military Operations (PDFDrive)serothan100% (1)

- LD Ceremony On The Activation of Adf For OpnsDocument22 pagesLD Ceremony On The Activation of Adf For OpnsDPAO ARMORNo ratings yet

- Schlieffen Plan - NoteDocument9 pagesSchlieffen Plan - NoteJonathan JayakrishnanNo ratings yet

- SdafggDocument69 pagesSdafggapi-269786551No ratings yet

- Dylan Pflughaupt Resume 2023Document1 pageDylan Pflughaupt Resume 2023api-683597584No ratings yet

- Chap1 2Document23 pagesChap1 2Jacie TupasNo ratings yet

- Renegades and HereticsDocument15 pagesRenegades and HereticsGarracGarrakNo ratings yet

- Regimental Guide Upload PDFDocument43 pagesRegimental Guide Upload PDFDarkeanonNo ratings yet

- NTTP 3-07.2.1 Antiterrorism - Nov 2019Document414 pagesNTTP 3-07.2.1 Antiterrorism - Nov 2019kent vaughnNo ratings yet

- Tactical Convoy Ops: Multi-Service Tactics, Techniques, and Procedures For Tactical Convoy OperationsDocument136 pagesTactical Convoy Ops: Multi-Service Tactics, Techniques, and Procedures For Tactical Convoy OperationsFippeFi100% (1)

- Iran US Preventive Strikes PDFDocument97 pagesIran US Preventive Strikes PDFzeontitanNo ratings yet

- The Rizal Retraction and Other CasesDocument3 pagesThe Rizal Retraction and Other CasesArgen Delos Santos RivasNo ratings yet

- Faction Characteristics and TablesFRONTDocument1 pageFaction Characteristics and TablesFRONTCesar BermudezNo ratings yet

- WWII 79th Fighter Group IDocument92 pagesWWII 79th Fighter Group ICAP History Library100% (7)

- Critical Analysis of German Operational Intelligence: UnclassifiedDocument7 pagesCritical Analysis of German Operational Intelligence: UnclassifiedDaniel GargulákNo ratings yet

- Scheldt Estuary Campaign (1944)Document48 pagesScheldt Estuary Campaign (1944)CAP History Library100% (3)

- C. S. Grant With The Fourth in His New Series of Wargames Scenarios and Their SolutionsDocument3 pagesC. S. Grant With The Fourth in His New Series of Wargames Scenarios and Their SolutionsAnonymous uqCzGZINo ratings yet

- Battle of Al-BabDocument4 pagesBattle of Al-BabSaurav RathodNo ratings yet

Download as pdf or txt

You might also like

- Infinity Hunger Games 2018Document4 pagesInfinity Hunger Games 2018Anonymous KdzgEHNo ratings yet

- Wargames Illustrated #026Document56 pagesWargames Illustrated #026Анатолий Золотухин100% (1)

- Howard - Forgotten Dimensions of StrategyDocument13 pagesHoward - Forgotten Dimensions of StrategyEdward LeeNo ratings yet

- Leaflet - HDFC Defence Fund NFO (May 2023) - 2Document4 pagesLeaflet - HDFC Defence Fund NFO (May 2023) - 2Akshay ChaudhryNo ratings yet

- Activism GreenspanDocument18 pagesActivism GreenspannewagedanteNo ratings yet

- Macroeconomic Determinants of Stock Market Development: Evidence From Borsa IstanbulDocument21 pagesMacroeconomic Determinants of Stock Market Development: Evidence From Borsa IstanbulMaria KulawikNo ratings yet

- China S Sovereign Wealth Fund Weakness and ChallengesDocument16 pagesChina S Sovereign Wealth Fund Weakness and ChallengesWendy MúsicaNo ratings yet

- The Dash To Trash and The Grab For Growth (01.15.08)Document16 pagesThe Dash To Trash and The Grab For Growth (01.15.08)BunNo ratings yet

- TICAD Africa 2050-Chapter2-V2Document32 pagesTICAD Africa 2050-Chapter2-V2AbdallaNo ratings yet

- International Value Investing (Updated)Document11 pagesInternational Value Investing (Updated)eric_stNo ratings yet

- Oil&gasDocument23 pagesOil&gasPriyankaKesariNo ratings yet

- ECO302: Intermediate Macroeconomic Theory I: Spring 2021Document27 pagesECO302: Intermediate Macroeconomic Theory I: Spring 2021Nafew ProdhanNo ratings yet

- Federal Funds Rate NASDAQ Timeline: June, 1995 April, 1996 January, 1999Document6 pagesFederal Funds Rate NASDAQ Timeline: June, 1995 April, 1996 January, 1999Aditya NevrekarNo ratings yet

- Bruegel March2010 Ext PubDocument19 pagesBruegel March2010 Ext PubBruegelNo ratings yet

- The Plateau in Cinema Attendances and Drop in Video Sales in The UK The Role of Digital Leisure Substitutes 2006 10 10Document25 pagesThe Plateau in Cinema Attendances and Drop in Video Sales in The UK The Role of Digital Leisure Substitutes 2006 10 10Eliza L. KormazopoulosNo ratings yet

- 2 Growth Trends in National IncomeDocument29 pages2 Growth Trends in National IncomeDheeraj Budhiraja0% (1)

- Lecturenote 1 2 24Document27 pagesLecturenote 1 2 24채영No ratings yet

- Inflation Indexed Bonds.Document81 pagesInflation Indexed Bonds.Mythili InnconNo ratings yet

- Economicdisintegrationofthe European UnionDocument11 pagesEconomicdisintegrationofthe European UnionHabib EjazNo ratings yet

- Undernourishment Around The World in 2010: The Number of Undernourished People Has Declined But Remains Unacceptably HighDocument4 pagesUndernourishment Around The World in 2010: The Number of Undernourished People Has Declined But Remains Unacceptably HighKoert OosterhuisNo ratings yet

- PIPP WK 3 - Organised Interests, Power and Public Policy 2023-241.0Document12 pagesPIPP WK 3 - Organised Interests, Power and Public Policy 2023-241.0aliejazmirNo ratings yet

- Etf Playbook 1Document12 pagesEtf Playbook 1langlinglung1985No ratings yet

- GlobalizationDocument2 pagesGlobalizationAngelika C PauleNo ratings yet

- Diagnosis of Sri Lanka's Current Economic Crisis and Potential Solutions - CFA Sri Lanka - 10 Sep 2021 - DistributeDocument128 pagesDiagnosis of Sri Lanka's Current Economic Crisis and Potential Solutions - CFA Sri Lanka - 10 Sep 2021 - DistributeganrajNo ratings yet

- FM474 Lecture 5 - Risk and ReturnDocument58 pagesFM474 Lecture 5 - Risk and Returnjie.ji3No ratings yet

- Concept of Unit Linked ProductsDocument37 pagesConcept of Unit Linked Productsapi-19794187No ratings yet

- Financial Risk Management Philippe Jorion 1 Financial Risk ManagementDocument17 pagesFinancial Risk Management Philippe Jorion 1 Financial Risk ManagementWaqasAhmadNo ratings yet

- Lazard Investment - An Introduction To The Emerging Market Debt Asset ClassDocument8 pagesLazard Investment - An Introduction To The Emerging Market Debt Asset ClassPranjayNo ratings yet

- Rice SubsidiesDocument5 pagesRice SubsidiesAbbas KhanNo ratings yet

- 1 - Jan Longeval, Managing Director, Bank Degroof - Are PensDocument25 pages1 - Jan Longeval, Managing Director, Bank Degroof - Are Penspensiontalk100% (1)

- Profiling Minimum Volatility: Executive SummaryDocument10 pagesProfiling Minimum Volatility: Executive SummaryCalvin YeohNo ratings yet

- Chilean Productivity Presentation-Chad SyversonDocument15 pagesChilean Productivity Presentation-Chad SyversonYorka SánchezNo ratings yet

- AIFI Corso 2016 - Daniele PilchardDocument58 pagesAIFI Corso 2016 - Daniele Pilcharddaniele.pilchard6465No ratings yet

- Macroeconomic Stability: The More The Better?Document27 pagesMacroeconomic Stability: The More The Better?Roselyn Mahinay QuilongquilongNo ratings yet

- SME and Micro Financing: Malaysia's ExperienceDocument67 pagesSME and Micro Financing: Malaysia's Experiencedharmeshmehta31No ratings yet

- MasteringWealthManagement Oct8 2023Document36 pagesMasteringWealthManagement Oct8 2023lakshmi_gamini_1No ratings yet

- Etf Playbook WebDocument12 pagesEtf Playbook WebquangdatphungNo ratings yet

- 13 Chapter 5 InflationDocument36 pages13 Chapter 5 InflationchinuNo ratings yet

- Moeller Et Al. JFDocument26 pagesMoeller Et Al. JFbenjaminNo ratings yet

- KKEK4325 Petroleum Engineering: Assignment 1Document7 pagesKKEK4325 Petroleum Engineering: Assignment 1Muzammil IqbalNo ratings yet

- Effect of Economic Growth On Unemployment and Validity of Okun's Law in MauritiusDocument20 pagesEffect of Economic Growth On Unemployment and Validity of Okun's Law in MauritiusImam Arief PambudiNo ratings yet

- THE Growth and Transformation of The Iiaalaysian Economy and The I'',Iplications FOR Development PianningDocument9 pagesTHE Growth and Transformation of The Iiaalaysian Economy and The I'',Iplications FOR Development PianningKhairul AnuarNo ratings yet

- Excessive Optimism A Short RecessionDocument13 pagesExcessive Optimism A Short RecessionMahad SheikhNo ratings yet

- Overview On Risk in Int BsnsDocument34 pagesOverview On Risk in Int BsnsUmesh ChandraNo ratings yet

- Voituriez - 2001 - What Explains Price Volatility Changes in Commodity Markets Answers From The World Palm-Oil MarketDocument8 pagesVoituriez - 2001 - What Explains Price Volatility Changes in Commodity Markets Answers From The World Palm-Oil MarketFarhah ADNo ratings yet

- Macroeconomics I: Open EconomyDocument26 pagesMacroeconomics I: Open EconomyAlèxia SalvadorNo ratings yet

- Housing and Mortgage Market Update: Philadelphia Council For Business EconomicsDocument16 pagesHousing and Mortgage Market Update: Philadelphia Council For Business EconomicsZerohedgeNo ratings yet

- Lecture 1 PDFDocument23 pagesLecture 1 PDFHawar HANo ratings yet

- Survival of Euro Section-BDocument26 pagesSurvival of Euro Section-BKumar RaunakNo ratings yet

- How Will Real Estate Cap Rates Respond To The Rise in The Fed Funds Rate - 2022 06 23 134238 - UnuiDocument11 pagesHow Will Real Estate Cap Rates Respond To The Rise in The Fed Funds Rate - 2022 06 23 134238 - Unuisascha.kiserNo ratings yet

- Inflation and Price ChangesDocument7 pagesInflation and Price ChangesRica AniñonNo ratings yet

- Econ Macro 5th Edition Mceachern Solutions ManualDocument4 pagesEcon Macro 5th Edition Mceachern Solutions Manualraphaelbacrqu100% (36)

- Fama DB Prize Market Efficiency October 2005Document15 pagesFama DB Prize Market Efficiency October 2005Nathan AwNo ratings yet

- Unido: (United Nation Industrial Development)Document7 pagesUnido: (United Nation Industrial Development)Kyla JadjurieNo ratings yet

- An International Analysis of The Economic Cost - 2020 - Research in InternationaDocument15 pagesAn International Analysis of The Economic Cost - 2020 - Research in InternationaDessy ParamitaNo ratings yet

- India and The World EconomyDocument45 pagesIndia and The World EconomyPraveen BVSNo ratings yet

- Analysis of The International Oil Price Fluctuatio PDFDocument8 pagesAnalysis of The International Oil Price Fluctuatio PDFPadma BhushanNo ratings yet

- The Relationship Between Asia Pacific Markets During The Financial Crisis: Var-Granger Causality AnalysisDocument26 pagesThe Relationship Between Asia Pacific Markets During The Financial Crisis: Var-Granger Causality AnalysisDr. Abdul BashirNo ratings yet

- Economy of JapanDocument24 pagesEconomy of JapanMohanad Al-SehetryNo ratings yet

- John KhumaloDocument12 pagesJohn KhumaloAlfian VioNo ratings yet

- A New Era of Investing Begins 1672488719Document31 pagesA New Era of Investing Begins 1672488719Octavio BrasilNo ratings yet

- Activity 1Document2 pagesActivity 1api-472469147No ratings yet

- Equity Index Performance Tracker - Mar 2024Document1 pageEquity Index Performance Tracker - Mar 2024DeepakNo ratings yet

- Invite - NFO Alert - Launch of HDFC NIFTY100 Low Volatility 30 Index FundDocument1 pageInvite - NFO Alert - Launch of HDFC NIFTY100 Low Volatility 30 Index FundDeepakNo ratings yet

- Screenshot 2024-06-21 at 8.10.54 AMDocument1 pageScreenshot 2024-06-21 at 8.10.54 AMDeepakNo ratings yet

- HDFC Children's Gift Fund Leaflet (As On 31st March 2023)Document4 pagesHDFC Children's Gift Fund Leaflet (As On 31st March 2023)DeepakNo ratings yet

- SIP Mantra - HDFC Flexi Cap Fund (Aprt 2023)Document2 pagesSIP Mantra - HDFC Flexi Cap Fund (Aprt 2023)DeepakNo ratings yet

- Leaflet - Hedged and Unhedged Exposure of Hybrid FundsDocument2 pagesLeaflet - Hedged and Unhedged Exposure of Hybrid FundsDeepakNo ratings yet

- Debt Product Suite - Upto 1 Yr - March 2023Document17 pagesDebt Product Suite - Upto 1 Yr - March 2023DeepakNo ratings yet

- HDFC NIFTY SDL+GSec Jun 2027 40-60 TMF - NFO PresentationDocument17 pagesHDFC NIFTY SDL+GSec Jun 2027 40-60 TMF - NFO PresentationDeepakNo ratings yet

- Protecting Operational Performance Worldwide: MTL Surge Protection SolutionsDocument32 pagesProtecting Operational Performance Worldwide: MTL Surge Protection SolutionsDeepakNo ratings yet

- Deepak R Chauhan FSWDocument1 pageDeepak R Chauhan FSWDeepakNo ratings yet

- Victory in The Pacific 2ED RulesDocument8 pagesVictory in The Pacific 2ED RulesAndrew SmithNo ratings yet

- 32 1 Hitler's Lightning WarDocument3 pages32 1 Hitler's Lightning WarjaiurwgghiurhfuigaewNo ratings yet

- Catalogue 2021 PanzerkampfDocument10 pagesCatalogue 2021 PanzerkampfEmeraldmoxNo ratings yet

- Codex Imperial GuardDocument43 pagesCodex Imperial GuardCole Gartner33% (3)

- Watch Prime Master (1) Watch Prime Brothers (5) Watch Attack WalkerDocument1 pageWatch Prime Master (1) Watch Prime Brothers (5) Watch Attack WalkerduduNo ratings yet

- Strategic Air WarfareDocument158 pagesStrategic Air WarfareBob AndrepontNo ratings yet

- Lion of The North - Rules & ScenariosDocument56 pagesLion of The North - Rules & ScenariosBrant McClureNo ratings yet

- D D I 1334.01 W U: O Nstruction Earing of The NiformDocument6 pagesD D I 1334.01 W U: O Nstruction Earing of The NiformJoel SofeuNo ratings yet

- OSS MotionpicturesasweaponsDocument11 pagesOSS MotionpicturesasweaponsDavid OrozcoNo ratings yet

- Intelligence and Military Operations (PDFDrive)Document481 pagesIntelligence and Military Operations (PDFDrive)serothan100% (1)

- LD Ceremony On The Activation of Adf For OpnsDocument22 pagesLD Ceremony On The Activation of Adf For OpnsDPAO ARMORNo ratings yet

- Schlieffen Plan - NoteDocument9 pagesSchlieffen Plan - NoteJonathan JayakrishnanNo ratings yet

- SdafggDocument69 pagesSdafggapi-269786551No ratings yet

- Dylan Pflughaupt Resume 2023Document1 pageDylan Pflughaupt Resume 2023api-683597584No ratings yet

- Chap1 2Document23 pagesChap1 2Jacie TupasNo ratings yet

- Renegades and HereticsDocument15 pagesRenegades and HereticsGarracGarrakNo ratings yet

- Regimental Guide Upload PDFDocument43 pagesRegimental Guide Upload PDFDarkeanonNo ratings yet

- NTTP 3-07.2.1 Antiterrorism - Nov 2019Document414 pagesNTTP 3-07.2.1 Antiterrorism - Nov 2019kent vaughnNo ratings yet

- Tactical Convoy Ops: Multi-Service Tactics, Techniques, and Procedures For Tactical Convoy OperationsDocument136 pagesTactical Convoy Ops: Multi-Service Tactics, Techniques, and Procedures For Tactical Convoy OperationsFippeFi100% (1)

- Iran US Preventive Strikes PDFDocument97 pagesIran US Preventive Strikes PDFzeontitanNo ratings yet

- The Rizal Retraction and Other CasesDocument3 pagesThe Rizal Retraction and Other CasesArgen Delos Santos RivasNo ratings yet

- Faction Characteristics and TablesFRONTDocument1 pageFaction Characteristics and TablesFRONTCesar BermudezNo ratings yet

- WWII 79th Fighter Group IDocument92 pagesWWII 79th Fighter Group ICAP History Library100% (7)

- Critical Analysis of German Operational Intelligence: UnclassifiedDocument7 pagesCritical Analysis of German Operational Intelligence: UnclassifiedDaniel GargulákNo ratings yet

- Scheldt Estuary Campaign (1944)Document48 pagesScheldt Estuary Campaign (1944)CAP History Library100% (3)

- C. S. Grant With The Fourth in His New Series of Wargames Scenarios and Their SolutionsDocument3 pagesC. S. Grant With The Fourth in His New Series of Wargames Scenarios and Their SolutionsAnonymous uqCzGZINo ratings yet

- Battle of Al-BabDocument4 pagesBattle of Al-BabSaurav RathodNo ratings yet