Individual Federal Tax Updates

Individual Federal Tax Updates

You might also like

- Instructions For Form 941: (Rev. March 2021)Document20 pagesInstructions For Form 941: (Rev. March 2021)Btakeshi1No ratings yet

- Meru CabDocument2 pagesMeru CabMuzammil0% (1)

- Please Complete The 2015 Federal Income Tax Return For Magdalena Schmitz PDFDocument5 pagesPlease Complete The 2015 Federal Income Tax Return For Magdalena Schmitz PDFDoreen0% (1)

- Sample Format of Individual Income Tax Return y A 2017 2018Document3 pagesSample Format of Individual Income Tax Return y A 2017 2018Chathuranga LSISNo ratings yet

- Editable Retail Loan Application - ApplicantDocument10 pagesEditable Retail Loan Application - Applicantmadhukar sahayNo ratings yet

- Early Evidence On The Use of Foreign Cash Following The Tax Cuts and Jobs Act of 2017Document53 pagesEarly Evidence On The Use of Foreign Cash Following The Tax Cuts and Jobs Act of 2017GlennKesslerWPNo ratings yet

- I 843Document6 pagesI 843ayi imaduddinNo ratings yet

- Business Federal Tax UpdateDocument9 pagesBusiness Federal Tax Updatesean dale porlaresNo ratings yet

- 2022 Tax UpdatesDocument12 pages2022 Tax UpdatesJagmohan TeamentigrityNo ratings yet

- Copy B For Student 1098-T: Tuition StatementDocument1 pageCopy B For Student 1098-T: Tuition Statementqqvhc2x2prNo ratings yet

- Home Loan Complete ProcessDocument3 pagesHome Loan Complete ProcessMkb Prasanna Kumar100% (1)

- 2022 Individual Tax Organizer FillableDocument6 pages2022 Individual Tax Organizer FillableTham DangNo ratings yet

- Tax Return 2019Document26 pagesTax Return 2019Cash AppNo ratings yet

- Homecredit Copy Loan AgreementDocument2 pagesHomecredit Copy Loan AgreementMichael Del CarmenNo ratings yet

- Return of Organization Exempt From Income Tax: WWW - Irs.gov/form990Document37 pagesReturn of Organization Exempt From Income Tax: WWW - Irs.gov/form990the kingfishNo ratings yet

- New Jersey Amended Resident Income Tax Return: A / / B / / C / / DDocument3 pagesNew Jersey Amended Resident Income Tax Return: A / / B / / C / / DЛена КиселеваNo ratings yet

- NKC Form w9 SignedDocument4 pagesNKC Form w9 SignedLakes EvansNo ratings yet

- Fall 2023 - Tax ProjectDocument4 pagesFall 2023 - Tax Projectacwriters123No ratings yet

- Itr2 Fy 2020-21 Ay 2021-22Document42 pagesItr2 Fy 2020-21 Ay 2021-22Pradeep GoudaNo ratings yet

- 2021 - Robinhood Securities 1099Document8 pages2021 - Robinhood Securities 1099Estranged GedNo ratings yet

- NCJC 561348186 - 200712 - 990Document28 pagesNCJC 561348186 - 200712 - 990A.P. DillonNo ratings yet

- 1040es Estimated Tax 2014 For IndividualsDocument12 pages1040es Estimated Tax 2014 For IndividualsClaudia MaldonadoNo ratings yet

- Lesson Plan Prepare An Individual Income Tax Return - 0Document5 pagesLesson Plan Prepare An Individual Income Tax Return - 0Clary AgustinNo ratings yet

- Gene Locke Tax Return, 2006Document25 pagesGene Locke Tax Return, 2006Lee Ann O'NealNo ratings yet

- Employer's QUARTERLY Federal Tax Return: Answer These Questions For This QuarterDocument4 pagesEmployer's QUARTERLY Federal Tax Return: Answer These Questions For This QuarterTony MillerNo ratings yet

- 2007 Carl & Ruth Shapiro Family Foundation 990 (Includes Madoff Investment)Document42 pages2007 Carl & Ruth Shapiro Family Foundation 990 (Includes Madoff Investment)jpeppard100% (4)

- Fairmount Heights - Documents 1 PDFDocument88 pagesFairmount Heights - Documents 1 PDFAri AsheNo ratings yet

- Preview Copy Do Not File: Eduardo Valle 463 41 4299Document3 pagesPreview Copy Do Not File: Eduardo Valle 463 41 4299evalle13No ratings yet

- Updated Tax Accounting BIS, 2024Document234 pagesUpdated Tax Accounting BIS, 2024fyfyg411No ratings yet

- FIRE 2011 Form 990Document36 pagesFIRE 2011 Form 990FIRENo ratings yet

- Investment Declaration Form - FY 2022-23Document7 pagesInvestment Declaration Form - FY 2022-23varaprasadNo ratings yet

- April 16, 2024 at 5 - 30 PM - Canutillo ISD Board WorkshopDocument36 pagesApril 16, 2024 at 5 - 30 PM - Canutillo ISD Board WorkshopSammy CShowNo ratings yet

- 2020 Federal Tax Return Documents (PATEL ASHOKBHAI and CHE)Document7 pages2020 Federal Tax Return Documents (PATEL ASHOKBHAI and CHE)atul0070No ratings yet

- Houston Community CollegeDocument8 pagesHouston Community CollegeLizzie McGuireNo ratings yet

- Income Tax Return 2023 24 Excluding 82C Businesspartnership3Document18 pagesIncome Tax Return 2023 24 Excluding 82C Businesspartnership3Mehedi HasanNo ratings yet

- 568 - LLC Tax Return FormDocument7 pages568 - LLC Tax Return FormAndreana Dumpling WilliamsNo ratings yet

- Instructions For Form 1099-MISC: Future Developments Specific InstructionsDocument11 pagesInstructions For Form 1099-MISC: Future Developments Specific InstructionsVenkatapavan SinagamNo ratings yet

- 2020 1099-INT WellsFargoDocument2 pages2020 1099-INT WellsFargosayma kandaf0% (1)

- Tuition StatementDocument7 pagesTuition StatementAnonymous 9FlDK6YrJNo ratings yet

- Julian Saud 1095a 2022Document8 pagesJulian Saud 1095a 2022Neyda LarroqueNo ratings yet

- FTF 2023-02-04 1675540608948Document4 pagesFTF 2023-02-04 1675540608948kelsey abrahamNo ratings yet

- 2010 Income Tax ReturnDocument2 pages2010 Income Tax ReturnCkey ArNo ratings yet

- 540 FinalDocument5 pages540 Finalapi-350796322No ratings yet

- Federal TexasDocument22 pagesFederal TexasPaola V. MartinezNo ratings yet

- Employee's Withholding Certificate 2020Document4 pagesEmployee's Withholding Certificate 2020CNBC.comNo ratings yet

- Tabliga Gerwin Andres Agusti Marissa Calzado: Application For Vehicle FinancingDocument3 pagesTabliga Gerwin Andres Agusti Marissa Calzado: Application For Vehicle FinancingJerikah Jec HernandezNo ratings yet

- Form 941 SummaryDocument5 pagesForm 941 SummaryCatori-Dakoda Eil100% (1)

- 2021 Investco 403b 7 Distribution FormDocument19 pages2021 Investco 403b 7 Distribution FormMax PowerNo ratings yet

- Estate TaxDocument8 pagesEstate TaxAngel Alejo AcobaNo ratings yet

- Payroll: Company Financial Salaries Wages DeductionsDocument5 pagesPayroll: Company Financial Salaries Wages DeductionsKavitaNo ratings yet

- Advanced Scenario 6: Samantha Rollins (2017)Document9 pagesAdvanced Scenario 6: Samantha Rollins (2017)Center for Economic Progress0% (1)

- Annual Income Tax Return For Individuals Earning Purely Compensation IncomeDocument2 pagesAnnual Income Tax Return For Individuals Earning Purely Compensation IncomeErikaNo ratings yet

- YW - W4 Form-2023Document1 pageYW - W4 Form-2023Whora DoraNo ratings yet

- GSa7JR Document Form I Individual Income Tax Return 2019Document22 pagesGSa7JR Document Form I Individual Income Tax Return 2019Israel PopeNo ratings yet

- 2019 SPAC TaxesDocument50 pages2019 SPAC TaxesWendy LiberatoreNo ratings yet

- Child and Dependent Care Expenses: (If You Have More Than Two Care Providers, See The Instructions.)Document2 pagesChild and Dependent Care Expenses: (If You Have More Than Two Care Providers, See The Instructions.)Sarah KuldipNo ratings yet

- Federal 2016 :DDocument15 pagesFederal 2016 :DAnguila Angel Anguila AngelNo ratings yet

- Classification of Deductible Expenses Section 212 Expenses:: Have AGI LimitationsDocument6 pagesClassification of Deductible Expenses Section 212 Expenses:: Have AGI Limitations张心怡No ratings yet

- Making Use of The Illinois Rules - Part 1: Reducing Illinois Estate Taxes Through Lifetime GiftsDocument36 pagesMaking Use of The Illinois Rules - Part 1: Reducing Illinois Estate Taxes Through Lifetime Giftsrobertkolasa100% (1)

- 333 LineDocument25 pages333 LineTiffany BrooksNo ratings yet

- US Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesFrom EverandUS Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesNo ratings yet

- Surviving the New Tax Landscape: Smart Savings, Investment and Estate Planning StrategiesFrom EverandSurviving the New Tax Landscape: Smart Savings, Investment and Estate Planning StrategiesNo ratings yet

- Tax Deducted at SourceDocument29 pagesTax Deducted at SourceChaitany Joshi0% (2)

- Flytech TechnologyDocument7 pagesFlytech TechnologyLouis ChenNo ratings yet

- Indira Gandhi National Widow Pension SchemeDocument3 pagesIndira Gandhi National Widow Pension SchemeNavinkumar RohitNo ratings yet

- GR Exp 1Document2 pagesGR Exp 1Reddy BodhanapuNo ratings yet

- Revenue Regulations No 2-98Document16 pagesRevenue Regulations No 2-98Lea Samantha GallardoNo ratings yet

- Notice of Assessment 2019 04 29 02 32 21 264865Document4 pagesNotice of Assessment 2019 04 29 02 32 21 264865Dennis EnnsNo ratings yet

- Philtax All InupdateDocument86 pagesPhiltax All InupdateKayezel Kriss75% (4)

- Trips Hotel DownloadETicketDocument1 pageTrips Hotel DownloadETicketRahulNo ratings yet

- Partnership Operations Enabling AssessmentDocument3 pagesPartnership Operations Enabling AssessmentVon Andrei MedinaNo ratings yet

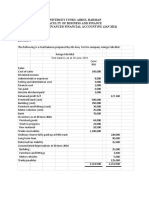

- Universiti Tunku Abdul Rahman Faculty of Business and Finance Ubaf 2113 Advanced Financial Accounting (Jan 2021) Tutorial 1Document5 pagesUniversiti Tunku Abdul Rahman Faculty of Business and Finance Ubaf 2113 Advanced Financial Accounting (Jan 2021) Tutorial 1KAY PHINE NGNo ratings yet

- The Government Accounting ProcessDocument2 pagesThe Government Accounting ProcessrochNo ratings yet

- Columbia WHTDocument7 pagesColumbia WHTAnilNo ratings yet

- Delta AssignmentDocument4 pagesDelta Assignmentbinzidd007No ratings yet

- PM Mandhan Scheme DetailsDocument1 pagePM Mandhan Scheme Detailspave.scgroupNo ratings yet

- Summary of Collections and Remittances - BTDocument18 pagesSummary of Collections and Remittances - BTSt. Veronica Learning CenterNo ratings yet

- Income Tax A.Y. 2023-24Document6 pagesIncome Tax A.Y. 2023-24sandeepsbiradar100% (3)

- Deduction in Respect of Expenditure On Specified BusinessDocument5 pagesDeduction in Respect of Expenditure On Specified BusinessMukesh ManwaniNo ratings yet

- House No L - 1311, Sector 5-B/3, North KARACHI, Karachi Central North Karachi Town Arsalan AkkilDocument6 pagesHouse No L - 1311, Sector 5-B/3, North KARACHI, Karachi Central North Karachi Town Arsalan AkkilMuhammad AhsanNo ratings yet

- 5KW With BatteryDocument1 page5KW With BatteryKidzee KidzeeNo ratings yet

- Direct TaxesDocument9 pagesDirect TaxesAnushka TiwariNo ratings yet

- State Tax FormDocument2 pagesState Tax FormSaintjinx21No ratings yet

- PCL Chap 4 en CaDocument69 pagesPCL Chap 4 en CaMitchieNo ratings yet

- Mahaveer Enterprises: Tax InvoiceDocument1 pageMahaveer Enterprises: Tax InvoiceAyush SrivastavNo ratings yet

- Taxation Atty. Macmod, C.P.A. Individual and Corporate Income TaxpayersDocument12 pagesTaxation Atty. Macmod, C.P.A. Individual and Corporate Income TaxpayersJohn Brian D. SorianoNo ratings yet

- Notes On Capital Budgeting BBS First Year (TU)Document1 pageNotes On Capital Budgeting BBS First Year (TU)Manoj GhimireNo ratings yet

- NEW Sales Tax Invoice - 2023-07-27T163454.502Document1 pageNEW Sales Tax Invoice - 2023-07-27T163454.502Saadat IrfanNo ratings yet

- Payroll Accounting 2021 31St Edition Full ChapterDocument41 pagesPayroll Accounting 2021 31St Edition Full Chaptermark.bookman383100% (27)

- DIGEST - Avon Products Manufacturing Inc v. CIRDocument2 pagesDIGEST - Avon Products Manufacturing Inc v. CIRAgatha ApolinarioNo ratings yet

Download as docx, pdf, or txt

You might also like

- Instructions For Form 941: (Rev. March 2021)Document20 pagesInstructions For Form 941: (Rev. March 2021)Btakeshi1No ratings yet

- Meru CabDocument2 pagesMeru CabMuzammil0% (1)

- Please Complete The 2015 Federal Income Tax Return For Magdalena Schmitz PDFDocument5 pagesPlease Complete The 2015 Federal Income Tax Return For Magdalena Schmitz PDFDoreen0% (1)

- Sample Format of Individual Income Tax Return y A 2017 2018Document3 pagesSample Format of Individual Income Tax Return y A 2017 2018Chathuranga LSISNo ratings yet

- Editable Retail Loan Application - ApplicantDocument10 pagesEditable Retail Loan Application - Applicantmadhukar sahayNo ratings yet

- Early Evidence On The Use of Foreign Cash Following The Tax Cuts and Jobs Act of 2017Document53 pagesEarly Evidence On The Use of Foreign Cash Following The Tax Cuts and Jobs Act of 2017GlennKesslerWPNo ratings yet

- I 843Document6 pagesI 843ayi imaduddinNo ratings yet

- Business Federal Tax UpdateDocument9 pagesBusiness Federal Tax Updatesean dale porlaresNo ratings yet

- 2022 Tax UpdatesDocument12 pages2022 Tax UpdatesJagmohan TeamentigrityNo ratings yet

- Copy B For Student 1098-T: Tuition StatementDocument1 pageCopy B For Student 1098-T: Tuition Statementqqvhc2x2prNo ratings yet

- Home Loan Complete ProcessDocument3 pagesHome Loan Complete ProcessMkb Prasanna Kumar100% (1)

- 2022 Individual Tax Organizer FillableDocument6 pages2022 Individual Tax Organizer FillableTham DangNo ratings yet

- Tax Return 2019Document26 pagesTax Return 2019Cash AppNo ratings yet

- Homecredit Copy Loan AgreementDocument2 pagesHomecredit Copy Loan AgreementMichael Del CarmenNo ratings yet

- Return of Organization Exempt From Income Tax: WWW - Irs.gov/form990Document37 pagesReturn of Organization Exempt From Income Tax: WWW - Irs.gov/form990the kingfishNo ratings yet

- New Jersey Amended Resident Income Tax Return: A / / B / / C / / DDocument3 pagesNew Jersey Amended Resident Income Tax Return: A / / B / / C / / DЛена КиселеваNo ratings yet

- NKC Form w9 SignedDocument4 pagesNKC Form w9 SignedLakes EvansNo ratings yet

- Fall 2023 - Tax ProjectDocument4 pagesFall 2023 - Tax Projectacwriters123No ratings yet

- Itr2 Fy 2020-21 Ay 2021-22Document42 pagesItr2 Fy 2020-21 Ay 2021-22Pradeep GoudaNo ratings yet

- 2021 - Robinhood Securities 1099Document8 pages2021 - Robinhood Securities 1099Estranged GedNo ratings yet

- NCJC 561348186 - 200712 - 990Document28 pagesNCJC 561348186 - 200712 - 990A.P. DillonNo ratings yet

- 1040es Estimated Tax 2014 For IndividualsDocument12 pages1040es Estimated Tax 2014 For IndividualsClaudia MaldonadoNo ratings yet

- Lesson Plan Prepare An Individual Income Tax Return - 0Document5 pagesLesson Plan Prepare An Individual Income Tax Return - 0Clary AgustinNo ratings yet

- Gene Locke Tax Return, 2006Document25 pagesGene Locke Tax Return, 2006Lee Ann O'NealNo ratings yet

- Employer's QUARTERLY Federal Tax Return: Answer These Questions For This QuarterDocument4 pagesEmployer's QUARTERLY Federal Tax Return: Answer These Questions For This QuarterTony MillerNo ratings yet

- 2007 Carl & Ruth Shapiro Family Foundation 990 (Includes Madoff Investment)Document42 pages2007 Carl & Ruth Shapiro Family Foundation 990 (Includes Madoff Investment)jpeppard100% (4)

- Fairmount Heights - Documents 1 PDFDocument88 pagesFairmount Heights - Documents 1 PDFAri AsheNo ratings yet

- Preview Copy Do Not File: Eduardo Valle 463 41 4299Document3 pagesPreview Copy Do Not File: Eduardo Valle 463 41 4299evalle13No ratings yet

- Updated Tax Accounting BIS, 2024Document234 pagesUpdated Tax Accounting BIS, 2024fyfyg411No ratings yet

- FIRE 2011 Form 990Document36 pagesFIRE 2011 Form 990FIRENo ratings yet

- Investment Declaration Form - FY 2022-23Document7 pagesInvestment Declaration Form - FY 2022-23varaprasadNo ratings yet

- April 16, 2024 at 5 - 30 PM - Canutillo ISD Board WorkshopDocument36 pagesApril 16, 2024 at 5 - 30 PM - Canutillo ISD Board WorkshopSammy CShowNo ratings yet

- 2020 Federal Tax Return Documents (PATEL ASHOKBHAI and CHE)Document7 pages2020 Federal Tax Return Documents (PATEL ASHOKBHAI and CHE)atul0070No ratings yet

- Houston Community CollegeDocument8 pagesHouston Community CollegeLizzie McGuireNo ratings yet

- Income Tax Return 2023 24 Excluding 82C Businesspartnership3Document18 pagesIncome Tax Return 2023 24 Excluding 82C Businesspartnership3Mehedi HasanNo ratings yet

- 568 - LLC Tax Return FormDocument7 pages568 - LLC Tax Return FormAndreana Dumpling WilliamsNo ratings yet

- Instructions For Form 1099-MISC: Future Developments Specific InstructionsDocument11 pagesInstructions For Form 1099-MISC: Future Developments Specific InstructionsVenkatapavan SinagamNo ratings yet

- 2020 1099-INT WellsFargoDocument2 pages2020 1099-INT WellsFargosayma kandaf0% (1)

- Tuition StatementDocument7 pagesTuition StatementAnonymous 9FlDK6YrJNo ratings yet

- Julian Saud 1095a 2022Document8 pagesJulian Saud 1095a 2022Neyda LarroqueNo ratings yet

- FTF 2023-02-04 1675540608948Document4 pagesFTF 2023-02-04 1675540608948kelsey abrahamNo ratings yet

- 2010 Income Tax ReturnDocument2 pages2010 Income Tax ReturnCkey ArNo ratings yet

- 540 FinalDocument5 pages540 Finalapi-350796322No ratings yet

- Federal TexasDocument22 pagesFederal TexasPaola V. MartinezNo ratings yet

- Employee's Withholding Certificate 2020Document4 pagesEmployee's Withholding Certificate 2020CNBC.comNo ratings yet

- Tabliga Gerwin Andres Agusti Marissa Calzado: Application For Vehicle FinancingDocument3 pagesTabliga Gerwin Andres Agusti Marissa Calzado: Application For Vehicle FinancingJerikah Jec HernandezNo ratings yet

- Form 941 SummaryDocument5 pagesForm 941 SummaryCatori-Dakoda Eil100% (1)

- 2021 Investco 403b 7 Distribution FormDocument19 pages2021 Investco 403b 7 Distribution FormMax PowerNo ratings yet

- Estate TaxDocument8 pagesEstate TaxAngel Alejo AcobaNo ratings yet

- Payroll: Company Financial Salaries Wages DeductionsDocument5 pagesPayroll: Company Financial Salaries Wages DeductionsKavitaNo ratings yet

- Advanced Scenario 6: Samantha Rollins (2017)Document9 pagesAdvanced Scenario 6: Samantha Rollins (2017)Center for Economic Progress0% (1)

- Annual Income Tax Return For Individuals Earning Purely Compensation IncomeDocument2 pagesAnnual Income Tax Return For Individuals Earning Purely Compensation IncomeErikaNo ratings yet

- YW - W4 Form-2023Document1 pageYW - W4 Form-2023Whora DoraNo ratings yet

- GSa7JR Document Form I Individual Income Tax Return 2019Document22 pagesGSa7JR Document Form I Individual Income Tax Return 2019Israel PopeNo ratings yet

- 2019 SPAC TaxesDocument50 pages2019 SPAC TaxesWendy LiberatoreNo ratings yet

- Child and Dependent Care Expenses: (If You Have More Than Two Care Providers, See The Instructions.)Document2 pagesChild and Dependent Care Expenses: (If You Have More Than Two Care Providers, See The Instructions.)Sarah KuldipNo ratings yet

- Federal 2016 :DDocument15 pagesFederal 2016 :DAnguila Angel Anguila AngelNo ratings yet

- Classification of Deductible Expenses Section 212 Expenses:: Have AGI LimitationsDocument6 pagesClassification of Deductible Expenses Section 212 Expenses:: Have AGI Limitations张心怡No ratings yet

- Making Use of The Illinois Rules - Part 1: Reducing Illinois Estate Taxes Through Lifetime GiftsDocument36 pagesMaking Use of The Illinois Rules - Part 1: Reducing Illinois Estate Taxes Through Lifetime Giftsrobertkolasa100% (1)

- 333 LineDocument25 pages333 LineTiffany BrooksNo ratings yet

- US Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesFrom EverandUS Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesNo ratings yet

- Surviving the New Tax Landscape: Smart Savings, Investment and Estate Planning StrategiesFrom EverandSurviving the New Tax Landscape: Smart Savings, Investment and Estate Planning StrategiesNo ratings yet

- Tax Deducted at SourceDocument29 pagesTax Deducted at SourceChaitany Joshi0% (2)

- Flytech TechnologyDocument7 pagesFlytech TechnologyLouis ChenNo ratings yet

- Indira Gandhi National Widow Pension SchemeDocument3 pagesIndira Gandhi National Widow Pension SchemeNavinkumar RohitNo ratings yet

- GR Exp 1Document2 pagesGR Exp 1Reddy BodhanapuNo ratings yet

- Revenue Regulations No 2-98Document16 pagesRevenue Regulations No 2-98Lea Samantha GallardoNo ratings yet

- Notice of Assessment 2019 04 29 02 32 21 264865Document4 pagesNotice of Assessment 2019 04 29 02 32 21 264865Dennis EnnsNo ratings yet

- Philtax All InupdateDocument86 pagesPhiltax All InupdateKayezel Kriss75% (4)

- Trips Hotel DownloadETicketDocument1 pageTrips Hotel DownloadETicketRahulNo ratings yet

- Partnership Operations Enabling AssessmentDocument3 pagesPartnership Operations Enabling AssessmentVon Andrei MedinaNo ratings yet

- Universiti Tunku Abdul Rahman Faculty of Business and Finance Ubaf 2113 Advanced Financial Accounting (Jan 2021) Tutorial 1Document5 pagesUniversiti Tunku Abdul Rahman Faculty of Business and Finance Ubaf 2113 Advanced Financial Accounting (Jan 2021) Tutorial 1KAY PHINE NGNo ratings yet

- The Government Accounting ProcessDocument2 pagesThe Government Accounting ProcessrochNo ratings yet

- Columbia WHTDocument7 pagesColumbia WHTAnilNo ratings yet

- Delta AssignmentDocument4 pagesDelta Assignmentbinzidd007No ratings yet

- PM Mandhan Scheme DetailsDocument1 pagePM Mandhan Scheme Detailspave.scgroupNo ratings yet

- Summary of Collections and Remittances - BTDocument18 pagesSummary of Collections and Remittances - BTSt. Veronica Learning CenterNo ratings yet

- Income Tax A.Y. 2023-24Document6 pagesIncome Tax A.Y. 2023-24sandeepsbiradar100% (3)

- Deduction in Respect of Expenditure On Specified BusinessDocument5 pagesDeduction in Respect of Expenditure On Specified BusinessMukesh ManwaniNo ratings yet

- House No L - 1311, Sector 5-B/3, North KARACHI, Karachi Central North Karachi Town Arsalan AkkilDocument6 pagesHouse No L - 1311, Sector 5-B/3, North KARACHI, Karachi Central North Karachi Town Arsalan AkkilMuhammad AhsanNo ratings yet

- 5KW With BatteryDocument1 page5KW With BatteryKidzee KidzeeNo ratings yet

- Direct TaxesDocument9 pagesDirect TaxesAnushka TiwariNo ratings yet

- State Tax FormDocument2 pagesState Tax FormSaintjinx21No ratings yet

- PCL Chap 4 en CaDocument69 pagesPCL Chap 4 en CaMitchieNo ratings yet

- Mahaveer Enterprises: Tax InvoiceDocument1 pageMahaveer Enterprises: Tax InvoiceAyush SrivastavNo ratings yet

- Taxation Atty. Macmod, C.P.A. Individual and Corporate Income TaxpayersDocument12 pagesTaxation Atty. Macmod, C.P.A. Individual and Corporate Income TaxpayersJohn Brian D. SorianoNo ratings yet

- Notes On Capital Budgeting BBS First Year (TU)Document1 pageNotes On Capital Budgeting BBS First Year (TU)Manoj GhimireNo ratings yet

- NEW Sales Tax Invoice - 2023-07-27T163454.502Document1 pageNEW Sales Tax Invoice - 2023-07-27T163454.502Saadat IrfanNo ratings yet

- Payroll Accounting 2021 31St Edition Full ChapterDocument41 pagesPayroll Accounting 2021 31St Edition Full Chaptermark.bookman383100% (27)

- DIGEST - Avon Products Manufacturing Inc v. CIRDocument2 pagesDIGEST - Avon Products Manufacturing Inc v. CIRAgatha ApolinarioNo ratings yet