Download as docx, pdf, or txt

You might also like

- ADAADocument36 pagesADAAGo Create DesignNo ratings yet

- Parodi, Peter - Pricing in General Insurance-CRC Press (2014) - 73-75Document3 pagesParodi, Peter - Pricing in General Insurance-CRC Press (2014) - 73-75Joseph OndariNo ratings yet

- Prepared By: Mark Price 25 Wall ST Apt 3 01604Document4 pagesPrepared By: Mark Price 25 Wall ST Apt 3 01604jamesNo ratings yet

- Erick Wallace V LA County Sheriffs OfficeDocument11 pagesErick Wallace V LA County Sheriffs OfficeEthan Brown100% (1)

- Thabo Mbeki - Iam An AfricanDocument5 pagesThabo Mbeki - Iam An Africansehlabakmnsnr100% (1)

- MACCDocument7 pagesMACCGerry SajolNo ratings yet

- Complaint - Sum of MoneyDocument6 pagesComplaint - Sum of Moneyplay_pauseNo ratings yet

- American National Standard For Financial PDFDocument19 pagesAmerican National Standard For Financial PDFaakbaralNo ratings yet

- Suggestions and ConclusionsDocument3 pagesSuggestions and ConclusionsimadNo ratings yet

- Intern ReportDocument51 pagesIntern ReportHarsh PandeyNo ratings yet

- Shrimantee Roy - ResumeDocument3 pagesShrimantee Roy - ResumeShrimantee RoyNo ratings yet

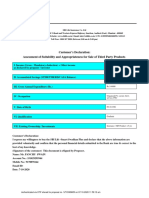

- Customer's Declaration: Assessment of Suitability and Appropriateness For Sale of Third Party ProductsDocument16 pagesCustomer's Declaration: Assessment of Suitability and Appropriateness For Sale of Third Party ProductsPanchu SwainNo ratings yet

- B.Tech Civil Syllabus AR16 RevisedDocument227 pagesB.Tech Civil Syllabus AR16 Revisedabhiram_23355681No ratings yet

- Entrep ReviewerDocument1 pageEntrep ReviewerWAEL, Kyle Angelo A.No ratings yet

- FIBAC 2019 - AnnualBenchmarking PDFDocument92 pagesFIBAC 2019 - AnnualBenchmarking PDFNirav ShahNo ratings yet

- Activity 1: Entrepreneurship Scavenger Hunt: You and The Person YouDocument3 pagesActivity 1: Entrepreneurship Scavenger Hunt: You and The Person YouRosemarie R. ReyesNo ratings yet

- YOCee E-Newspaper Issue 16Document8 pagesYOCee E-Newspaper Issue 16revatheeNo ratings yet

- A1841452586 18818 6 2023 Ca1k22cbDocument33 pagesA1841452586 18818 6 2023 Ca1k22cbSUBAM SINGHNo ratings yet

- Tech Team JDDocument3 pagesTech Team JDtaposh.barmonNo ratings yet

- Profile DhanikuberjiDocument6 pagesProfile Dhanikuberjihetalahir149No ratings yet

- CNTH KRTL YgyDocument22 pagesCNTH KRTL YgyryndraihnNo ratings yet

- GDSC LPU Info Session - 2023Document54 pagesGDSC LPU Info Session - 2023GDSC LPUNo ratings yet

- Summer Internship Training Report: For The MBA Degree (2020-2022)Document50 pagesSummer Internship Training Report: For The MBA Degree (2020-2022)Soham DasNo ratings yet

- Walmart: Submitted By-Vandana Rana (2K18/MBA/083) Sukriti Kanwar (2K18/MBA/085)Document14 pagesWalmart: Submitted By-Vandana Rana (2K18/MBA/083) Sukriti Kanwar (2K18/MBA/085)Sukriti KanwarNo ratings yet

- Unit 8 Role of DGCA/BCAS in Aviation Safety and SecurityDocument7 pagesUnit 8 Role of DGCA/BCAS in Aviation Safety and Securityrathneshkumar100% (2)

- Imaging in Osteoarthritis 2021 YjocaDocument22 pagesImaging in Osteoarthritis 2021 Yjocaal malikNo ratings yet

- FijiTimes - Aug 32012 PDFDocument48 pagesFijiTimes - Aug 32012 PDFfijitimescanadaNo ratings yet

- SOP To Be Adopted by FPOsDocument12 pagesSOP To Be Adopted by FPOssampathsamudralaNo ratings yet

- CNRL Original Internship PostingDocument3 pagesCNRL Original Internship PostingMathew WebsterNo ratings yet

- Atos 2019 Financial Report PDFDocument106 pagesAtos 2019 Financial Report PDFBustamante LisiNo ratings yet

- 1 PDFsam 270120 BM PDFDocument243 pages1 PDFsam 270120 BM PDFSomenath PaulNo ratings yet

- EBSDocument2 pagesEBSsudhakar reddyNo ratings yet

- CH01CR 0799 Insurance Endorsement Ownership TransferDocument3 pagesCH01CR 0799 Insurance Endorsement Ownership Transferstjohnschool41No ratings yet

- Name: Section: - Schedule: - Class Number: - DateDocument21 pagesName: Section: - Schedule: - Class Number: - DateZeny Mae SumayangNo ratings yet

- Prajya Dec 2022 Digital - Final 1 PDFDocument68 pagesPrajya Dec 2022 Digital - Final 1 PDFSasikumar RNo ratings yet

- Sustainability 14 13072 v2Document20 pagesSustainability 14 13072 v2Janelle HafallaNo ratings yet

- It NotesDocument5 pagesIt Notessimran.patilNo ratings yet

- GUIDDocument255 pagesGUIDaymanbandrNo ratings yet

- User Manual: Professional Gaming MouseDocument5 pagesUser Manual: Professional Gaming MousedineshNo ratings yet

- Car MakerDocument1 pageCar MakeranantpalanNo ratings yet

- Minnor Project 0000Document50 pagesMinnor Project 0000Praveenkumarsingh.finnoyNo ratings yet

- Faculty of Law - Bclmjur Class Web Version v3Document56 pagesFaculty of Law - Bclmjur Class Web Version v3KHUSHI SIMHANo ratings yet

- Ar 2023Document284 pagesAr 2023lehung.123298No ratings yet

- Mack How GSPDocument124 pagesMack How GSPTom LNo ratings yet

- User's Manual: GB NL F E D IDocument21 pagesUser's Manual: GB NL F E D IFlorea NicolaeNo ratings yet

- AF-R50cx - 55cx - 60cx - 70cx (1) SHARP SERVICE MANUALDocument44 pagesAF-R50cx - 55cx - 60cx - 70cx (1) SHARP SERVICE MANUALLuis Felipe Msoqueda BañosNo ratings yet

- Rahul R Nair - CV CMEDocument4 pagesRahul R Nair - CV CMERahul NairNo ratings yet

- 3 Peer-Reviewed ArticlesDocument46 pages3 Peer-Reviewed ArticlesMINH Pham Thi QuyNo ratings yet

- EmeakDocument3 pagesEmeakSantosh RecruiterNo ratings yet

- 1 956 1 BOBAnalystPresentationQ4FY20Document71 pages1 956 1 BOBAnalystPresentationQ4FY20SannihithNo ratings yet

- Minor Project Report On Aircel by Mohit ChauhanDocument55 pagesMinor Project Report On Aircel by Mohit ChauhanMohit ChauhanNo ratings yet

- DTDC Courier Cargo LTDDocument3 pagesDTDC Courier Cargo LTDDeepakkmrgupta786No ratings yet

- SSRN Id3685235Document70 pagesSSRN Id3685235HARITHA HARIDASANNo ratings yet

- National Pension SchemeDocument9 pagesNational Pension SchemeSanam BindraNo ratings yet

- Air Cooled Mini Chiller AMAC-C-2009Document180 pagesAir Cooled Mini Chiller AMAC-C-2009ADV C&L Venture S/BNo ratings yet

- 800 Gigacenter Ordering Guide: April 2017Document28 pages800 Gigacenter Ordering Guide: April 2017Antwan JosephNo ratings yet

- GRE Vocabulary02Document20 pagesGRE Vocabulary02refdoc512No ratings yet

- 2013-10 Gbi-Guidelines Final-Operational GuidelinesDocument10 pages2013-10 Gbi-Guidelines Final-Operational Guidelinesmemyself246No ratings yet

- Dothraki DoctionaryDocument23 pagesDothraki Doctionaryapi-268945877No ratings yet

- Opt13 4eDocument31 pagesOpt13 4eMohamed Sayed FathyNo ratings yet

- CROSSWORD Current Affairs MAGAZINE JUNE 2023Document225 pagesCROSSWORD Current Affairs MAGAZINE JUNE 2023Bhrt RmnniNo ratings yet

- Oct 2019 Sebring Meals On Wheels NewsletterDocument6 pagesOct 2019 Sebring Meals On Wheels NewsletterPamela McCabeNo ratings yet

- AxtriaDocument3 pagesAxtriaTarang Gupta0% (1)

- Pradeep CSR FinDocument81 pagesPradeep CSR FinShreyash ShahNo ratings yet

- Mayuresh Patil 9162 Marketing Project ReportDocument78 pagesMayuresh Patil 9162 Marketing Project ReportShreyash ShahNo ratings yet

- Outlook PDFDocument85 pagesOutlook PDFKrishan LakhmaniNo ratings yet

- Paint DealDocument6 pagesPaint DealShreyash ShahNo ratings yet

- Pradeep CSR FinDocument81 pagesPradeep CSR FinShreyash ShahNo ratings yet

- Aarti General Management ProjectDocument38 pagesAarti General Management ProjectShreyash ShahNo ratings yet

- Sip ReportDocument64 pagesSip ReportShreyash ShahNo ratings yet

- Mayuresh Patil 9162 Marketing Project ReportDocument78 pagesMayuresh Patil 9162 Marketing Project ReportShreyash ShahNo ratings yet

- Pradeep CSRDocument33 pagesPradeep CSRShreyash ShahNo ratings yet

- Sameed Ansari.Document1 pageSameed Ansari.Shreyash ShahNo ratings yet

- Book1 ReportDocument15 pagesBook1 ReportShreyash ShahNo ratings yet

- Ibcc ReitDocument8 pagesIbcc ReitShreyash ShahNo ratings yet

- Wa0000.Document1 pageWa0000.Shreyash ShahNo ratings yet

- Pradeep SpecDocument68 pagesPradeep SpecShreyash ShahNo ratings yet

- General MDocument53 pagesGeneral MShreyash ShahNo ratings yet

- New DocumentDocument1 pageNew DocumentShreyash ShahNo ratings yet

- Q3 Financial HighlightsDocument1 pageQ3 Financial HighlightsShreyash ShahNo ratings yet

- Company Namcategory Brand + Product Name + Type Size (KG/LT)Document8 pagesCompany Namcategory Brand + Product Name + Type Size (KG/LT)Shreyash ShahNo ratings yet

- Jubilant Foodworks: More Legs For Growth Reflecting Confidence On CoreDocument11 pagesJubilant Foodworks: More Legs For Growth Reflecting Confidence On CoreShreyash ShahNo ratings yet

- Phiroze Je Jeebhoy Towers,: Dalal StreetDocument11 pagesPhiroze Je Jeebhoy Towers,: Dalal StreetShreyash ShahNo ratings yet

- Kullu Manali 5 Days Tour: by King Hills TravelsDocument26 pagesKullu Manali 5 Days Tour: by King Hills TravelsShreyash ShahNo ratings yet

- Visit: When ToDocument5 pagesVisit: When ToShreyash ShahNo ratings yet

- Work Study and Method Study PresentationDocument14 pagesWork Study and Method Study PresentationShreyash ShahNo ratings yet

- Visit Report GoaDocument27 pagesVisit Report GoaShreyash ShahNo ratings yet

- Exterior PaintingDocument10 pagesExterior PaintingShreyash ShahNo ratings yet

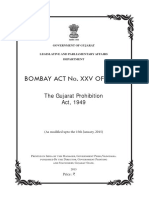

- Prohibition 1949Document81 pagesProhibition 1949Shreyash ShahNo ratings yet

- StateDocument9 pagesStateShreyash ShahNo ratings yet

- JLL AR 2021 22 - For Website - 300622Document287 pagesJLL AR 2021 22 - For Website - 300622Shreyash ShahNo ratings yet

- Berer 2Document19 pagesBerer 2Shreyash ShahNo ratings yet

- IC Indigo - Paints - MOSLDocument34 pagesIC Indigo - Paints - MOSLShreyash ShahNo ratings yet

- Moral Teachings in IslamDocument183 pagesMoral Teachings in Islamjmohideenkadhar50% (2)

- Krabi Riviera Company Ltd. - 251/13 Moo.2, Ao Nang, Muang, Krabi 81000 ThailandDocument2 pagesKrabi Riviera Company Ltd. - 251/13 Moo.2, Ao Nang, Muang, Krabi 81000 ThailandJames OtienoNo ratings yet

- MDL Doa 30B 11022020 V1Document17 pagesMDL Doa 30B 11022020 V1Imam Syafi'iNo ratings yet

- Time Frame of Depreciation-fixed-AssetsDocument17 pagesTime Frame of Depreciation-fixed-AssetsXuân ĐỗNo ratings yet

- The Murder of The Caliph 'UthmanDocument21 pagesThe Murder of The Caliph 'UthmanJaffer Abbas100% (1)

- Labour Law Short Answers Labour Law Short Answers: Semester 3&4 (Osmania University) Semester 3&4 (Osmania University)Document4 pagesLabour Law Short Answers Labour Law Short Answers: Semester 3&4 (Osmania University) Semester 3&4 (Osmania University)Srini VasaNo ratings yet

- Corruption and Governance: The Philippine ExperienceDocument12 pagesCorruption and Governance: The Philippine ExperienceJuliean Torres AkiatanNo ratings yet

- Wollheim DemocracyDocument19 pagesWollheim Democracygilbertosacerdoti_91No ratings yet

- General Comment No. 18 On Non Discrimination, UNHRCDocument3 pagesGeneral Comment No. 18 On Non Discrimination, UNHRCKangarooNo ratings yet

- California Unveils Latest Cannabis RulesDocument15 pagesCalifornia Unveils Latest Cannabis RulesJohn sonNo ratings yet

- Anti Defection Law The 52nd Amendment Act 1985 - Critical EvaluationDocument4 pagesAnti Defection Law The 52nd Amendment Act 1985 - Critical EvaluationSai Malavika TuluguNo ratings yet

- Sumulong v. ComelecDocument5 pagesSumulong v. ComelecHaniyyah FtmNo ratings yet

- 6331A-En Deploy Manage SystemCenterVMM-TrainerHandbookDocument380 pages6331A-En Deploy Manage SystemCenterVMM-TrainerHandbookFernando Gutierrez MedinaNo ratings yet

- Familia PDFDocument85 pagesFamilia PDFKatherine BlakeNo ratings yet

- Vahan and SarthiDocument36 pagesVahan and SarthiRaman YadavNo ratings yet

- Discharge Summary - Medical Abstract FormDocument1 pageDischarge Summary - Medical Abstract FormKevin AgbonesNo ratings yet

- Teacher-Induction-Program (TIP) Module 3 PDFDocument136 pagesTeacher-Induction-Program (TIP) Module 3 PDFDiana Jasmin Pascual Celestino50% (4)

- Legendary Chef Makes A Triumphant Return: Pierre KoffmannDocument36 pagesLegendary Chef Makes A Triumphant Return: Pierre KoffmannCity A.M.No ratings yet

- Town of Riverhead COVID-19 Update Issued May 12, 2020Document8 pagesTown of Riverhead COVID-19 Update Issued May 12, 2020RiverheadLOCALNo ratings yet

- Analysis of StressDocument2 pagesAnalysis of StresssijyvinodNo ratings yet

- Dangerous Liaisons Capri 2009Document140 pagesDangerous Liaisons Capri 2009Mark LauchsNo ratings yet

- Tabang vs. National Labor Relations CommissionDocument6 pagesTabang vs. National Labor Relations CommissionRMC PropertyLawNo ratings yet

- Original Complaint Against Heleen MeesDocument2 pagesOriginal Complaint Against Heleen MeesJulia Reynolds La RocheNo ratings yet

- As485070 Dec2022 PayslipDocument2 pagesAs485070 Dec2022 PayslipAKM Enterprises Pvt LtdNo ratings yet