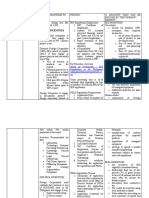

TAX-101 (Estate Tax)

TAX-101 (Estate Tax)

You might also like

- How To Migrate From SAP EWM (Business Suite) To Decentralized EWM Based On SAP S/4HanaDocument30 pagesHow To Migrate From SAP EWM (Business Suite) To Decentralized EWM Based On SAP S/4HanakamalrajNo ratings yet

- Editable Retail Loan Application - ApplicantDocument10 pagesEditable Retail Loan Application - Applicantmadhukar sahayNo ratings yet

- The Nespresso Case: Value Articulation - A Framework For The Strategic Management of Intellectual PropertyDocument6 pagesThe Nespresso Case: Value Articulation - A Framework For The Strategic Management of Intellectual PropertyAna SiqueiraNo ratings yet

- Right To PropertyDocument36 pagesRight To PropertyNilam100% (1)

- Guidelines of Direct Selling LicenseDocument12 pagesGuidelines of Direct Selling LicenseLeon Lu Lih Youn100% (3)

- Chapter 3 - Different Kinds of ObligationDocument18 pagesChapter 3 - Different Kinds of Obligationthatfuturecpa100% (1)

- Cosmeticsandtoiletries201510 DL PDFDocument68 pagesCosmeticsandtoiletries201510 DL PDFtmlNo ratings yet

- Donors To PercentageDocument24 pagesDonors To PercentageFrayladine TabagNo ratings yet

- Estate TaxDocument10 pagesEstate Taxrandomlungs121223No ratings yet

- TAX L002 Individual TaxationDocument18 pagesTAX L002 Individual TaxationYuri CaguioaNo ratings yet

- Excise TaxDocument7 pagesExcise TaxKezNo ratings yet

- Quizzers 12Document13 pagesQuizzers 12Niña Yna Franchesca PantallaNo ratings yet

- Week 3 Income Taxation Individual TaxpayersDocument58 pagesWeek 3 Income Taxation Individual TaxpayersJulienne Untalasco100% (1)

- Photovoltaic (Solar) Installation AgreementDocument6 pagesPhotovoltaic (Solar) Installation AgreementQueNo ratings yet

- Tax Remedies ActDocument8 pagesTax Remedies ActrobNo ratings yet

- For Boi IncentivesDocument7 pagesFor Boi Incentiveskimberly fanoNo ratings yet

- Income Taxation of IndividualsDocument26 pagesIncome Taxation of Individualsarkisha100% (1)

- Codal Reference and Related IssuancesDocument17 pagesCodal Reference and Related IssuancesBernardino PacificAceNo ratings yet

- CPAR Intro To Income Tax and Tax On Individuals (Batch 89) - HandoutDocument29 pagesCPAR Intro To Income Tax and Tax On Individuals (Batch 89) - HandoutMark LapidNo ratings yet

- TAX05-02 Individual Income TaxDocument7 pagesTAX05-02 Individual Income TaxJeth ConchaNo ratings yet

- (Tax) Casino First PreboardDocument5 pages(Tax) Casino First PreboardNor-janisah PundaodayaNo ratings yet

- PRTC 1stpb - 05.22 Sol TaxDocument21 pagesPRTC 1stpb - 05.22 Sol TaxCiatto SpotifyNo ratings yet

- 91-07 Gross IncomeDocument8 pages91-07 Gross IncomeNova PogadoNo ratings yet

- Homecredit Copy Loan AgreementDocument2 pagesHomecredit Copy Loan AgreementMichael Del CarmenNo ratings yet

- Chapter 4 Investments in Debt Securities and Other Long Term InvestmentDocument30 pagesChapter 4 Investments in Debt Securities and Other Long Term InvestmentAngelica Joy ManaoisNo ratings yet

- Rights and Remedies of The Government Under The NIRC: I. Power of The Bir To Obtain Information and Make An AssessmentDocument24 pagesRights and Remedies of The Government Under The NIRC: I. Power of The Bir To Obtain Information and Make An AssessmentPau SaulNo ratings yet

- Income Tax On Individuals and Tax RatesDocument25 pagesIncome Tax On Individuals and Tax RatesmmhNo ratings yet

- TAX HO1002 Individual Taxation StudentDocument12 pagesTAX HO1002 Individual Taxation StudentYuri CaguioaNo ratings yet

- Moral Theory On UtilitarianismDocument6 pagesMoral Theory On UtilitarianismCharles LaspiñasNo ratings yet

- TB ch03 DDDocument26 pagesTB ch03 DDPatricia Jean DigoNo ratings yet

- CODE OF ETHICS For Professional Accountants in TheDocument61 pagesCODE OF ETHICS For Professional Accountants in TheDiana Rose BassigNo ratings yet

- Tax II Digests Y SanchezDocument32 pagesTax II Digests Y SanchezJubsNo ratings yet

- Aud-90 PWDocument17 pagesAud-90 PWElaine Joyce GarciaNo ratings yet

- TAX-902 (Gross Income - Exclusions)Document6 pagesTAX-902 (Gross Income - Exclusions)MABI ESPENIDONo ratings yet

- Itr2 Fy 2020-21 Ay 2021-22Document42 pagesItr2 Fy 2020-21 Ay 2021-22Pradeep GoudaNo ratings yet

- Aescartin/Tlopez/Jpapa: Mobile Telephone GmailDocument7 pagesAescartin/Tlopez/Jpapa: Mobile Telephone GmailReynalyn BarbosaNo ratings yet

- Business Federal Tax UpdateDocument9 pagesBusiness Federal Tax Updatesean dale porlaresNo ratings yet

- Liabilities ReSA Handouts PDFDocument13 pagesLiabilities ReSA Handouts PDFNinaNo ratings yet

- Personal Loan Application Form: Different Needs, One Answer Personal Loans From TVS SOLUTION Loan SystemDocument7 pagesPersonal Loan Application Form: Different Needs, One Answer Personal Loans From TVS SOLUTION Loan Systemjuned shaikhNo ratings yet

- Chapter 5 - Current Asset ManagementDocument15 pagesChapter 5 - Current Asset ManagementReyes JonahNo ratings yet

- TAX 2021 - Theories and Independent ProblemsDocument28 pagesTAX 2021 - Theories and Independent ProblemsMingcheng JeeNo ratings yet

- TAX 702 - Income Tax Rates CorporationsDocument6 pagesTAX 702 - Income Tax Rates CorporationsJuan Miguel UngsodNo ratings yet

- TAX - Income Tax On IndividualsDocument10 pagesTAX - Income Tax On Individualsall about seventeenNo ratings yet

- Double Taxation Agreements 2022Document19 pagesDouble Taxation Agreements 2022rav danoNo ratings yet

- Tax232 - Excise Tax PDFDocument37 pagesTax232 - Excise Tax PDFClaire Ann ParasNo ratings yet

- Management Advisory Services (Mas) MAS01 Introductioin To Management AccountingDocument38 pagesManagement Advisory Services (Mas) MAS01 Introductioin To Management AccountingEagle OrtegaNo ratings yet

- Manila Cavite Laguna Cebu Cagayan de Oro DavaoDocument6 pagesManila Cavite Laguna Cebu Cagayan de Oro DavaoMonica GarciaNo ratings yet

- Module 2 - Income Taxes For Individuals - Lecture NotesDocument52 pagesModule 2 - Income Taxes For Individuals - Lecture NotesRina Bico Advincula100% (1)

- Far Reviewer 1 7Document8 pagesFar Reviewer 1 7Angel Marie MartinezNo ratings yet

- QUIZ Corporate Income Taxation AnswersDocument4 pagesQUIZ Corporate Income Taxation AnswersAang GrandeNo ratings yet

- Name: Section: Date:: Angel SantaDocument5 pagesName: Section: Date:: Angel SantaJoebet DebuyanNo ratings yet

- Capital Gains Tax PDFDocument6 pagesCapital Gains Tax PDFjanus lopezNo ratings yet

- Tax Rate A. For Individuals Earning Purely Compensation Income and Individuals Engaged in Business and Practice of ProfessionDocument8 pagesTax Rate A. For Individuals Earning Purely Compensation Income and Individuals Engaged in Business and Practice of ProfessionInna De LeonNo ratings yet

- CorporationsDocument46 pagesCorporationsDandred AdrianoNo ratings yet

- Capital Gains Tax: Selling Price Basis of Share (Inc. Dividend-On, Net of Tax) Doc. Stamp TaxDocument2 pagesCapital Gains Tax: Selling Price Basis of Share (Inc. Dividend-On, Net of Tax) Doc. Stamp Taxloonie tunesNo ratings yet

- Illustration VATDocument8 pagesIllustration VATLeah Mae NolascoNo ratings yet

- Chapter 6 - Strategy Analysis and ChoiceDocument26 pagesChapter 6 - Strategy Analysis and ChoiceMalaika Khan 009No ratings yet

- Remedies Tax 4 27 - Power and Remedy of AssessmentDocument15 pagesRemedies Tax 4 27 - Power and Remedy of AssessmentEmille LlorenteNo ratings yet

- Tax Exemption GuidelineDocument8 pagesTax Exemption GuidelineonghpNo ratings yet

- Shakey's 2021Document69 pagesShakey's 2021Megan CastilloNo ratings yet

- Part V Disbursement System 04122021Document19 pagesPart V Disbursement System 04122021Mana XD100% (1)

- Administrative Provisions - Estate Tax (Presentation Slides)Document9 pagesAdministrative Provisions - Estate Tax (Presentation Slides)KezNo ratings yet

- Lecture Notes: Advanced Financial Accounting and Reporting G/N/E de Leon AFAR.3014 - NGASDocument11 pagesLecture Notes: Advanced Financial Accounting and Reporting G/N/E de Leon AFAR.3014 - NGASTatianaNo ratings yet

- DPD DogsDocument13 pagesDPD DogsKen HaddadNo ratings yet

- IAS 33 Earnings Per ShareDocument9 pagesIAS 33 Earnings Per ShareangaNo ratings yet

- TAX-201 (Donor's Tax)Document7 pagesTAX-201 (Donor's Tax)Edith DalidaNo ratings yet

- TAX-502 (Excise Tax Rates - Part 2)Document3 pagesTAX-502 (Excise Tax Rates - Part 2)Princess ManaloNo ratings yet

- TAX-401 (Other Percentage Taxes - Part 1)Document5 pagesTAX-401 (Other Percentage Taxes - Part 1)Princess ManaloNo ratings yet

- Lit 2 - Midterm Lesson Part 2Document5 pagesLit 2 - Midterm Lesson Part 2Princess ManaloNo ratings yet

- TAX-303 (Input Taxes)Document7 pagesTAX-303 (Input Taxes)Princess ManaloNo ratings yet

- TAX-301 (VAT-Subject Transactions)Document9 pagesTAX-301 (VAT-Subject Transactions)Princess ManaloNo ratings yet

- Lit 2 - Midterm Lesson Part 1Document4 pagesLit 2 - Midterm Lesson Part 1Princess ManaloNo ratings yet

- Lit 2 - Midterm Lesson Part 5Document20 pagesLit 2 - Midterm Lesson Part 5Princess ManaloNo ratings yet

- Introduction To Accounting: Certificate in Accounting and Finance Stage ExaminationDocument5 pagesIntroduction To Accounting: Certificate in Accounting and Finance Stage ExaminationSYED ANEES ALINo ratings yet

- Learning CAN SLIM Education Resources: Lee TannerDocument43 pagesLearning CAN SLIM Education Resources: Lee Tannerneagucosmin67% (3)

- University Course Fee For Students & AgentsDocument4 pagesUniversity Course Fee For Students & AgentsChandan Kumar BanerjeeNo ratings yet

- Agenda Item 7 App1Document15 pagesAgenda Item 7 App1Sana KhanNo ratings yet

- C.H. Robinson Contract Addendum and Carrier Load Confirmation - #434674433Document4 pagesC.H. Robinson Contract Addendum and Carrier Load Confirmation - #434674433shayan aliNo ratings yet

- Grounds Prescription Ratification Rescissible Contract 4yrsDocument1 pageGrounds Prescription Ratification Rescissible Contract 4yrsDieanne MaeNo ratings yet

- D Ifta Journal 10Document76 pagesD Ifta Journal 10zushiiiNo ratings yet

- Automatización de ProcesosDocument7 pagesAutomatización de ProcesosFernando FlorNo ratings yet

- VRTXDocument27 pagesVRTXJeypee De GeeNo ratings yet

- Terex Wheel Loader Skl844 0100 Radlader Parts CatalogDocument11 pagesTerex Wheel Loader Skl844 0100 Radlader Parts Catalogmrpaulwilliams251290oje100% (68)

- Mba Project On Recruitment Selection PDFDocument100 pagesMba Project On Recruitment Selection PDFsumanNo ratings yet

- United States District Court Central District of California Case No: Cv08-01908 DSF (CTX)Document12 pagesUnited States District Court Central District of California Case No: Cv08-01908 DSF (CTX)twebster321100% (1)

- Mis in ICICI BankDocument14 pagesMis in ICICI BankRavindra Khandelwal100% (1)

- BSBLDR411 Project Portfolio Student.v1.0Document23 pagesBSBLDR411 Project Portfolio Student.v1.0ipal.rhdNo ratings yet

- Knowledge Organisers CIE Geography BWDocument19 pagesKnowledge Organisers CIE Geography BWAntoSeitanNo ratings yet

- Swift Ratw HawkDocument1 pageSwift Ratw HawkMajid ImranNo ratings yet

- GoU Statement Victory Day 2019Document4 pagesGoU Statement Victory Day 2019GCICNo ratings yet

- Summer Dhamaka AprilDocument21 pagesSummer Dhamaka AprilPapia ChandaNo ratings yet

- Archiving Production Orders (PP-SFC)Document13 pagesArchiving Production Orders (PP-SFC)Mayte López AymerichNo ratings yet

- The Large Marketplace Comparison GuideDocument43 pagesThe Large Marketplace Comparison GuidegencmetohuNo ratings yet

- BP Annual Report and Form 20f 2017Document302 pagesBP Annual Report and Form 20f 2017golddust2012No ratings yet

- MODULE - ACC 325 - UNIT1 - ULObDocument4 pagesMODULE - ACC 325 - UNIT1 - ULObJay-ar Castillo Watin Jr.No ratings yet

- SWOTDocument10 pagesSWOTGwendolyn PansoyNo ratings yet

- Paytm Wallet TXN HistoryJan2020 9369204281 PDFDocument2 pagesPaytm Wallet TXN HistoryJan2020 9369204281 PDFSandeep RaiNo ratings yet

Download as pdf or txt

You might also like

- How To Migrate From SAP EWM (Business Suite) To Decentralized EWM Based On SAP S/4HanaDocument30 pagesHow To Migrate From SAP EWM (Business Suite) To Decentralized EWM Based On SAP S/4HanakamalrajNo ratings yet

- Editable Retail Loan Application - ApplicantDocument10 pagesEditable Retail Loan Application - Applicantmadhukar sahayNo ratings yet

- The Nespresso Case: Value Articulation - A Framework For The Strategic Management of Intellectual PropertyDocument6 pagesThe Nespresso Case: Value Articulation - A Framework For The Strategic Management of Intellectual PropertyAna SiqueiraNo ratings yet

- Right To PropertyDocument36 pagesRight To PropertyNilam100% (1)

- Guidelines of Direct Selling LicenseDocument12 pagesGuidelines of Direct Selling LicenseLeon Lu Lih Youn100% (3)

- Chapter 3 - Different Kinds of ObligationDocument18 pagesChapter 3 - Different Kinds of Obligationthatfuturecpa100% (1)

- Cosmeticsandtoiletries201510 DL PDFDocument68 pagesCosmeticsandtoiletries201510 DL PDFtmlNo ratings yet

- Donors To PercentageDocument24 pagesDonors To PercentageFrayladine TabagNo ratings yet

- Estate TaxDocument10 pagesEstate Taxrandomlungs121223No ratings yet

- TAX L002 Individual TaxationDocument18 pagesTAX L002 Individual TaxationYuri CaguioaNo ratings yet

- Excise TaxDocument7 pagesExcise TaxKezNo ratings yet

- Quizzers 12Document13 pagesQuizzers 12Niña Yna Franchesca PantallaNo ratings yet

- Week 3 Income Taxation Individual TaxpayersDocument58 pagesWeek 3 Income Taxation Individual TaxpayersJulienne Untalasco100% (1)

- Photovoltaic (Solar) Installation AgreementDocument6 pagesPhotovoltaic (Solar) Installation AgreementQueNo ratings yet

- Tax Remedies ActDocument8 pagesTax Remedies ActrobNo ratings yet

- For Boi IncentivesDocument7 pagesFor Boi Incentiveskimberly fanoNo ratings yet

- Income Taxation of IndividualsDocument26 pagesIncome Taxation of Individualsarkisha100% (1)

- Codal Reference and Related IssuancesDocument17 pagesCodal Reference and Related IssuancesBernardino PacificAceNo ratings yet

- CPAR Intro To Income Tax and Tax On Individuals (Batch 89) - HandoutDocument29 pagesCPAR Intro To Income Tax and Tax On Individuals (Batch 89) - HandoutMark LapidNo ratings yet

- TAX05-02 Individual Income TaxDocument7 pagesTAX05-02 Individual Income TaxJeth ConchaNo ratings yet

- (Tax) Casino First PreboardDocument5 pages(Tax) Casino First PreboardNor-janisah PundaodayaNo ratings yet

- PRTC 1stpb - 05.22 Sol TaxDocument21 pagesPRTC 1stpb - 05.22 Sol TaxCiatto SpotifyNo ratings yet

- 91-07 Gross IncomeDocument8 pages91-07 Gross IncomeNova PogadoNo ratings yet

- Homecredit Copy Loan AgreementDocument2 pagesHomecredit Copy Loan AgreementMichael Del CarmenNo ratings yet

- Chapter 4 Investments in Debt Securities and Other Long Term InvestmentDocument30 pagesChapter 4 Investments in Debt Securities and Other Long Term InvestmentAngelica Joy ManaoisNo ratings yet

- Rights and Remedies of The Government Under The NIRC: I. Power of The Bir To Obtain Information and Make An AssessmentDocument24 pagesRights and Remedies of The Government Under The NIRC: I. Power of The Bir To Obtain Information and Make An AssessmentPau SaulNo ratings yet

- Income Tax On Individuals and Tax RatesDocument25 pagesIncome Tax On Individuals and Tax RatesmmhNo ratings yet

- TAX HO1002 Individual Taxation StudentDocument12 pagesTAX HO1002 Individual Taxation StudentYuri CaguioaNo ratings yet

- Moral Theory On UtilitarianismDocument6 pagesMoral Theory On UtilitarianismCharles LaspiñasNo ratings yet

- TB ch03 DDDocument26 pagesTB ch03 DDPatricia Jean DigoNo ratings yet

- CODE OF ETHICS For Professional Accountants in TheDocument61 pagesCODE OF ETHICS For Professional Accountants in TheDiana Rose BassigNo ratings yet

- Tax II Digests Y SanchezDocument32 pagesTax II Digests Y SanchezJubsNo ratings yet

- Aud-90 PWDocument17 pagesAud-90 PWElaine Joyce GarciaNo ratings yet

- TAX-902 (Gross Income - Exclusions)Document6 pagesTAX-902 (Gross Income - Exclusions)MABI ESPENIDONo ratings yet

- Itr2 Fy 2020-21 Ay 2021-22Document42 pagesItr2 Fy 2020-21 Ay 2021-22Pradeep GoudaNo ratings yet

- Aescartin/Tlopez/Jpapa: Mobile Telephone GmailDocument7 pagesAescartin/Tlopez/Jpapa: Mobile Telephone GmailReynalyn BarbosaNo ratings yet

- Business Federal Tax UpdateDocument9 pagesBusiness Federal Tax Updatesean dale porlaresNo ratings yet

- Liabilities ReSA Handouts PDFDocument13 pagesLiabilities ReSA Handouts PDFNinaNo ratings yet

- Personal Loan Application Form: Different Needs, One Answer Personal Loans From TVS SOLUTION Loan SystemDocument7 pagesPersonal Loan Application Form: Different Needs, One Answer Personal Loans From TVS SOLUTION Loan Systemjuned shaikhNo ratings yet

- Chapter 5 - Current Asset ManagementDocument15 pagesChapter 5 - Current Asset ManagementReyes JonahNo ratings yet

- TAX 2021 - Theories and Independent ProblemsDocument28 pagesTAX 2021 - Theories and Independent ProblemsMingcheng JeeNo ratings yet

- TAX 702 - Income Tax Rates CorporationsDocument6 pagesTAX 702 - Income Tax Rates CorporationsJuan Miguel UngsodNo ratings yet

- TAX - Income Tax On IndividualsDocument10 pagesTAX - Income Tax On Individualsall about seventeenNo ratings yet

- Double Taxation Agreements 2022Document19 pagesDouble Taxation Agreements 2022rav danoNo ratings yet

- Tax232 - Excise Tax PDFDocument37 pagesTax232 - Excise Tax PDFClaire Ann ParasNo ratings yet

- Management Advisory Services (Mas) MAS01 Introductioin To Management AccountingDocument38 pagesManagement Advisory Services (Mas) MAS01 Introductioin To Management AccountingEagle OrtegaNo ratings yet

- Manila Cavite Laguna Cebu Cagayan de Oro DavaoDocument6 pagesManila Cavite Laguna Cebu Cagayan de Oro DavaoMonica GarciaNo ratings yet

- Module 2 - Income Taxes For Individuals - Lecture NotesDocument52 pagesModule 2 - Income Taxes For Individuals - Lecture NotesRina Bico Advincula100% (1)

- Far Reviewer 1 7Document8 pagesFar Reviewer 1 7Angel Marie MartinezNo ratings yet

- QUIZ Corporate Income Taxation AnswersDocument4 pagesQUIZ Corporate Income Taxation AnswersAang GrandeNo ratings yet

- Name: Section: Date:: Angel SantaDocument5 pagesName: Section: Date:: Angel SantaJoebet DebuyanNo ratings yet

- Capital Gains Tax PDFDocument6 pagesCapital Gains Tax PDFjanus lopezNo ratings yet

- Tax Rate A. For Individuals Earning Purely Compensation Income and Individuals Engaged in Business and Practice of ProfessionDocument8 pagesTax Rate A. For Individuals Earning Purely Compensation Income and Individuals Engaged in Business and Practice of ProfessionInna De LeonNo ratings yet

- CorporationsDocument46 pagesCorporationsDandred AdrianoNo ratings yet

- Capital Gains Tax: Selling Price Basis of Share (Inc. Dividend-On, Net of Tax) Doc. Stamp TaxDocument2 pagesCapital Gains Tax: Selling Price Basis of Share (Inc. Dividend-On, Net of Tax) Doc. Stamp Taxloonie tunesNo ratings yet

- Illustration VATDocument8 pagesIllustration VATLeah Mae NolascoNo ratings yet

- Chapter 6 - Strategy Analysis and ChoiceDocument26 pagesChapter 6 - Strategy Analysis and ChoiceMalaika Khan 009No ratings yet

- Remedies Tax 4 27 - Power and Remedy of AssessmentDocument15 pagesRemedies Tax 4 27 - Power and Remedy of AssessmentEmille LlorenteNo ratings yet

- Tax Exemption GuidelineDocument8 pagesTax Exemption GuidelineonghpNo ratings yet

- Shakey's 2021Document69 pagesShakey's 2021Megan CastilloNo ratings yet

- Part V Disbursement System 04122021Document19 pagesPart V Disbursement System 04122021Mana XD100% (1)

- Administrative Provisions - Estate Tax (Presentation Slides)Document9 pagesAdministrative Provisions - Estate Tax (Presentation Slides)KezNo ratings yet

- Lecture Notes: Advanced Financial Accounting and Reporting G/N/E de Leon AFAR.3014 - NGASDocument11 pagesLecture Notes: Advanced Financial Accounting and Reporting G/N/E de Leon AFAR.3014 - NGASTatianaNo ratings yet

- DPD DogsDocument13 pagesDPD DogsKen HaddadNo ratings yet

- IAS 33 Earnings Per ShareDocument9 pagesIAS 33 Earnings Per ShareangaNo ratings yet

- TAX-201 (Donor's Tax)Document7 pagesTAX-201 (Donor's Tax)Edith DalidaNo ratings yet

- TAX-502 (Excise Tax Rates - Part 2)Document3 pagesTAX-502 (Excise Tax Rates - Part 2)Princess ManaloNo ratings yet

- TAX-401 (Other Percentage Taxes - Part 1)Document5 pagesTAX-401 (Other Percentage Taxes - Part 1)Princess ManaloNo ratings yet

- Lit 2 - Midterm Lesson Part 2Document5 pagesLit 2 - Midterm Lesson Part 2Princess ManaloNo ratings yet

- TAX-303 (Input Taxes)Document7 pagesTAX-303 (Input Taxes)Princess ManaloNo ratings yet

- TAX-301 (VAT-Subject Transactions)Document9 pagesTAX-301 (VAT-Subject Transactions)Princess ManaloNo ratings yet

- Lit 2 - Midterm Lesson Part 1Document4 pagesLit 2 - Midterm Lesson Part 1Princess ManaloNo ratings yet

- Lit 2 - Midterm Lesson Part 5Document20 pagesLit 2 - Midterm Lesson Part 5Princess ManaloNo ratings yet

- Introduction To Accounting: Certificate in Accounting and Finance Stage ExaminationDocument5 pagesIntroduction To Accounting: Certificate in Accounting and Finance Stage ExaminationSYED ANEES ALINo ratings yet

- Learning CAN SLIM Education Resources: Lee TannerDocument43 pagesLearning CAN SLIM Education Resources: Lee Tannerneagucosmin67% (3)

- University Course Fee For Students & AgentsDocument4 pagesUniversity Course Fee For Students & AgentsChandan Kumar BanerjeeNo ratings yet

- Agenda Item 7 App1Document15 pagesAgenda Item 7 App1Sana KhanNo ratings yet

- C.H. Robinson Contract Addendum and Carrier Load Confirmation - #434674433Document4 pagesC.H. Robinson Contract Addendum and Carrier Load Confirmation - #434674433shayan aliNo ratings yet

- Grounds Prescription Ratification Rescissible Contract 4yrsDocument1 pageGrounds Prescription Ratification Rescissible Contract 4yrsDieanne MaeNo ratings yet

- D Ifta Journal 10Document76 pagesD Ifta Journal 10zushiiiNo ratings yet

- Automatización de ProcesosDocument7 pagesAutomatización de ProcesosFernando FlorNo ratings yet

- VRTXDocument27 pagesVRTXJeypee De GeeNo ratings yet

- Terex Wheel Loader Skl844 0100 Radlader Parts CatalogDocument11 pagesTerex Wheel Loader Skl844 0100 Radlader Parts Catalogmrpaulwilliams251290oje100% (68)

- Mba Project On Recruitment Selection PDFDocument100 pagesMba Project On Recruitment Selection PDFsumanNo ratings yet

- United States District Court Central District of California Case No: Cv08-01908 DSF (CTX)Document12 pagesUnited States District Court Central District of California Case No: Cv08-01908 DSF (CTX)twebster321100% (1)

- Mis in ICICI BankDocument14 pagesMis in ICICI BankRavindra Khandelwal100% (1)

- BSBLDR411 Project Portfolio Student.v1.0Document23 pagesBSBLDR411 Project Portfolio Student.v1.0ipal.rhdNo ratings yet

- Knowledge Organisers CIE Geography BWDocument19 pagesKnowledge Organisers CIE Geography BWAntoSeitanNo ratings yet

- Swift Ratw HawkDocument1 pageSwift Ratw HawkMajid ImranNo ratings yet

- GoU Statement Victory Day 2019Document4 pagesGoU Statement Victory Day 2019GCICNo ratings yet

- Summer Dhamaka AprilDocument21 pagesSummer Dhamaka AprilPapia ChandaNo ratings yet

- Archiving Production Orders (PP-SFC)Document13 pagesArchiving Production Orders (PP-SFC)Mayte López AymerichNo ratings yet

- The Large Marketplace Comparison GuideDocument43 pagesThe Large Marketplace Comparison GuidegencmetohuNo ratings yet

- BP Annual Report and Form 20f 2017Document302 pagesBP Annual Report and Form 20f 2017golddust2012No ratings yet

- MODULE - ACC 325 - UNIT1 - ULObDocument4 pagesMODULE - ACC 325 - UNIT1 - ULObJay-ar Castillo Watin Jr.No ratings yet

- SWOTDocument10 pagesSWOTGwendolyn PansoyNo ratings yet

- Paytm Wallet TXN HistoryJan2020 9369204281 PDFDocument2 pagesPaytm Wallet TXN HistoryJan2020 9369204281 PDFSandeep RaiNo ratings yet