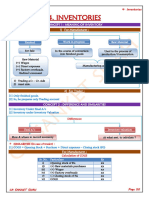

ACC1006 Inventory 2

ACC1006 Inventory 2

You might also like

- Chapter Two Materials ManagementDocument40 pagesChapter Two Materials ManagementYeabsira WorkagegnehuNo ratings yet

- Ifrs Usgaap NotesDocument38 pagesIfrs Usgaap Notesaum_thai100% (1)

- Chap - A Material 22-10-18Document33 pagesChap - A Material 22-10-18LunasNo ratings yet

- Summary FinalDocument28 pagesSummary FinalJackNo ratings yet

- ACC 111 Inventories AutosavedDocument19 pagesACC 111 Inventories AutosavedGiner Mabale Steven100% (1)

- Review Session 01 MA Topics 1-6 AfterDocument32 pagesReview Session 01 MA Topics 1-6 AftermisalNo ratings yet

- Review Session 01 MA Topics 1-6 BeforeDocument32 pagesReview Session 01 MA Topics 1-6 BeforemisalNo ratings yet

- ACC1006 InventoryDocument5 pagesACC1006 Inventoryanele khwelaNo ratings yet

- 06.marchandising Operation-FinalDocument53 pages06.marchandising Operation-FinalChowdhury Mobarrat Haider AdnanNo ratings yet

- Inventory: 1. IAS 2 InventoriesDocument7 pagesInventory: 1. IAS 2 InventoriesHikmət RüstəmovNo ratings yet

- Inventory Management: Chapter 13 (Stevenson)Document51 pagesInventory Management: Chapter 13 (Stevenson)Farhad HussainNo ratings yet

- Cheat SheetDocument15 pagesCheat SheetJason wonwonNo ratings yet

- Subsequent Measurement of InventoryDocument2 pagesSubsequent Measurement of InventorydayanNo ratings yet

- Cost of Sales & InventoriesDocument17 pagesCost of Sales & InventoriesShashank100% (1)

- Introductory Operations Management Chapter 12 Inventory Management Part ADocument26 pagesIntroductory Operations Management Chapter 12 Inventory Management Part APaulina_Choo_8858No ratings yet

- Harrison Chapter 5 Student 6 CeDocument46 pagesHarrison Chapter 5 Student 6 CeAliyan AmjadNo ratings yet

- Acc Prin 2 CH 1Document12 pagesAcc Prin 2 CH 1Bona MisbaNo ratings yet

- Book Chapter - Supply Chain Finance PerspectivesDocument26 pagesBook Chapter - Supply Chain Finance PerspectivesAli MkNo ratings yet

- Tutorial 8 - Basic Cost Concepts and Normal Costing: All Expenses Are Costs But Not All Costs Are ExpensesDocument12 pagesTutorial 8 - Basic Cost Concepts and Normal Costing: All Expenses Are Costs But Not All Costs Are ExpensesLingNo ratings yet

- Ind As 2: Inventories: (I) MeaningDocument6 pagesInd As 2: Inventories: (I) MeaningDinesh KumarNo ratings yet

- Financial Reporting and Analysis: - Session 5-Professor Raluca Ratiu, PHDDocument46 pagesFinancial Reporting and Analysis: - Session 5-Professor Raluca Ratiu, PHDDaniel YebraNo ratings yet

- BackDocument19 pagesBackjadeNo ratings yet

- Inventory Management PDFDocument49 pagesInventory Management PDFVyVyNo ratings yet

- Accounting Notes: Inventory SystemsDocument3 pagesAccounting Notes: Inventory Systemsyigrem abNo ratings yet

- Deterministic-Inventory (Supply Chain Management)Document28 pagesDeterministic-Inventory (Supply Chain Management)rajat aggarwalNo ratings yet

- Lecture 7 Inventories and Cost of Sales Teaching - NUS ACC1002 2020 SpringDocument39 pagesLecture 7 Inventories and Cost of Sales Teaching - NUS ACC1002 2020 SpringZenyuiNo ratings yet

- Accounting For Inventories NotesDocument2 pagesAccounting For Inventories NotesonsongoalexmunaviNo ratings yet

- Inventory Valuation Semester 1Document36 pagesInventory Valuation Semester 1Ankita SinghNo ratings yet

- Purpose: IRCON - Global Business Process Master List (BPML)Document24 pagesPurpose: IRCON - Global Business Process Master List (BPML)AdityaNo ratings yet

- ACC2203 HandoutsDocument17 pagesACC2203 HandoutsbeaudecoupeNo ratings yet

- Absorption and Variable Costing ReviewDocument13 pagesAbsorption and Variable Costing ReviewRodelLabor100% (1)

- Chapter 7 - InventoriesDocument16 pagesChapter 7 - InventoriesVanessa VelascoNo ratings yet

- Production Mis ReportsDocument36 pagesProduction Mis ReportsgcldesignNo ratings yet

- Dashboard MatrixDocument12 pagesDashboard MatrixJEnnife rHifeNo ratings yet

- Lect 11TVDocument25 pagesLect 11TVsalman siddiqui100% (1)

- Integration: Organization StructureDocument39 pagesIntegration: Organization StructureSantosh TripathiNo ratings yet

- Ias2 SNDocument7 pagesIas2 SNEmaan QaiserNo ratings yet

- Periodic and Perpetual Inventory SystemsDocument17 pagesPeriodic and Perpetual Inventory SystemsMichael Brian TorresNo ratings yet

- Inventory Part 1Document32 pagesInventory Part 1Leddie Bergs Villanueva VelascoNo ratings yet

- Inventory Management, Supply Contracts and Risk PoolingDocument81 pagesInventory Management, Supply Contracts and Risk PoolingnaniagricoNo ratings yet

- Part 4: Absorption and Variable Costing/Product Costing: Melziel A. Emba University of The East - ManilaDocument129 pagesPart 4: Absorption and Variable Costing/Product Costing: Melziel A. Emba University of The East - Manilarodell pabloNo ratings yet

- As 2Document7 pagesAs 2sanjay sNo ratings yet

- Chapter 5 Inventories and CGSDocument68 pagesChapter 5 Inventories and CGSZemene HailuNo ratings yet

- Chapter InventoriesDocument38 pagesChapter Inventoriesangellachavezlabalan.cpalawyerNo ratings yet

- Accounting Entries OPMDocument8 pagesAccounting Entries OPMzeeshan78100% (1)

- Inventory Systems and Periodic Recap PDFDocument4 pagesInventory Systems and Periodic Recap PDFMicah Ellah Reynoso PatindolNo ratings yet

- Just in Time and Backflush Accounting - 0Document27 pagesJust in Time and Backflush Accounting - 0pam pamNo ratings yet

- 08 Ias 2Document3 pages08 Ias 2Irtiza AbbasNo ratings yet

- Inleiding Tot de Logistiek (3542) : Prof. Dr. Kris BraekersDocument54 pagesInleiding Tot de Logistiek (3542) : Prof. Dr. Kris BraekersJoost VerheyenNo ratings yet

- Economic Cost OrderDocument28 pagesEconomic Cost OrderPiyam RazaNo ratings yet

- NAS 2 Inventories - UnlockedDocument33 pagesNAS 2 Inventories - UnlockedAviTvNo ratings yet

- Int Acct Chap 2Document12 pagesInt Acct Chap 2Kimberly NicoleNo ratings yet

- PPA 4 InventoriesDocument8 pagesPPA 4 Inventoriesbullalulla840No ratings yet

- Class Meeting 01 Cost Concepts, Manufacturing Cost, and Cost FlowsDocument55 pagesClass Meeting 01 Cost Concepts, Manufacturing Cost, and Cost FlowsRatu Shavira100% (1)

- Topic 7 - Absorption & Marginal CostingDocument8 pagesTopic 7 - Absorption & Marginal CostingMuhammad Alif100% (5)

- Finacial and Managerial Act Chapter 5-7Document59 pagesFinacial and Managerial Act Chapter 5-7solomon asefaNo ratings yet

- Financial Reporting Standards (Pas # 2) : Inventory Accounting Recognition, Measurement and DisclosuresDocument51 pagesFinancial Reporting Standards (Pas # 2) : Inventory Accounting Recognition, Measurement and DisclosuresKylieNo ratings yet

- SAP Accounting EntriesDocument8 pagesSAP Accounting Entriesprodigious84No ratings yet

- Business Metrics and Tools; Reference for Professionals and StudentsFrom EverandBusiness Metrics and Tools; Reference for Professionals and StudentsNo ratings yet

- Beyond Earnings: Applying the HOLT CFROI and Economic Profit FrameworkFrom EverandBeyond Earnings: Applying the HOLT CFROI and Economic Profit FrameworkNo ratings yet

Download as pdf or txt

You might also like

- Chapter Two Materials ManagementDocument40 pagesChapter Two Materials ManagementYeabsira WorkagegnehuNo ratings yet

- Ifrs Usgaap NotesDocument38 pagesIfrs Usgaap Notesaum_thai100% (1)

- Chap - A Material 22-10-18Document33 pagesChap - A Material 22-10-18LunasNo ratings yet

- Summary FinalDocument28 pagesSummary FinalJackNo ratings yet

- ACC 111 Inventories AutosavedDocument19 pagesACC 111 Inventories AutosavedGiner Mabale Steven100% (1)

- Review Session 01 MA Topics 1-6 AfterDocument32 pagesReview Session 01 MA Topics 1-6 AftermisalNo ratings yet

- Review Session 01 MA Topics 1-6 BeforeDocument32 pagesReview Session 01 MA Topics 1-6 BeforemisalNo ratings yet

- ACC1006 InventoryDocument5 pagesACC1006 Inventoryanele khwelaNo ratings yet

- 06.marchandising Operation-FinalDocument53 pages06.marchandising Operation-FinalChowdhury Mobarrat Haider AdnanNo ratings yet

- Inventory: 1. IAS 2 InventoriesDocument7 pagesInventory: 1. IAS 2 InventoriesHikmət RüstəmovNo ratings yet

- Inventory Management: Chapter 13 (Stevenson)Document51 pagesInventory Management: Chapter 13 (Stevenson)Farhad HussainNo ratings yet

- Cheat SheetDocument15 pagesCheat SheetJason wonwonNo ratings yet

- Subsequent Measurement of InventoryDocument2 pagesSubsequent Measurement of InventorydayanNo ratings yet

- Cost of Sales & InventoriesDocument17 pagesCost of Sales & InventoriesShashank100% (1)

- Introductory Operations Management Chapter 12 Inventory Management Part ADocument26 pagesIntroductory Operations Management Chapter 12 Inventory Management Part APaulina_Choo_8858No ratings yet

- Harrison Chapter 5 Student 6 CeDocument46 pagesHarrison Chapter 5 Student 6 CeAliyan AmjadNo ratings yet

- Acc Prin 2 CH 1Document12 pagesAcc Prin 2 CH 1Bona MisbaNo ratings yet

- Book Chapter - Supply Chain Finance PerspectivesDocument26 pagesBook Chapter - Supply Chain Finance PerspectivesAli MkNo ratings yet

- Tutorial 8 - Basic Cost Concepts and Normal Costing: All Expenses Are Costs But Not All Costs Are ExpensesDocument12 pagesTutorial 8 - Basic Cost Concepts and Normal Costing: All Expenses Are Costs But Not All Costs Are ExpensesLingNo ratings yet

- Ind As 2: Inventories: (I) MeaningDocument6 pagesInd As 2: Inventories: (I) MeaningDinesh KumarNo ratings yet

- Financial Reporting and Analysis: - Session 5-Professor Raluca Ratiu, PHDDocument46 pagesFinancial Reporting and Analysis: - Session 5-Professor Raluca Ratiu, PHDDaniel YebraNo ratings yet

- BackDocument19 pagesBackjadeNo ratings yet

- Inventory Management PDFDocument49 pagesInventory Management PDFVyVyNo ratings yet

- Accounting Notes: Inventory SystemsDocument3 pagesAccounting Notes: Inventory Systemsyigrem abNo ratings yet

- Deterministic-Inventory (Supply Chain Management)Document28 pagesDeterministic-Inventory (Supply Chain Management)rajat aggarwalNo ratings yet

- Lecture 7 Inventories and Cost of Sales Teaching - NUS ACC1002 2020 SpringDocument39 pagesLecture 7 Inventories and Cost of Sales Teaching - NUS ACC1002 2020 SpringZenyuiNo ratings yet

- Accounting For Inventories NotesDocument2 pagesAccounting For Inventories NotesonsongoalexmunaviNo ratings yet

- Inventory Valuation Semester 1Document36 pagesInventory Valuation Semester 1Ankita SinghNo ratings yet

- Purpose: IRCON - Global Business Process Master List (BPML)Document24 pagesPurpose: IRCON - Global Business Process Master List (BPML)AdityaNo ratings yet

- ACC2203 HandoutsDocument17 pagesACC2203 HandoutsbeaudecoupeNo ratings yet

- Absorption and Variable Costing ReviewDocument13 pagesAbsorption and Variable Costing ReviewRodelLabor100% (1)

- Chapter 7 - InventoriesDocument16 pagesChapter 7 - InventoriesVanessa VelascoNo ratings yet

- Production Mis ReportsDocument36 pagesProduction Mis ReportsgcldesignNo ratings yet

- Dashboard MatrixDocument12 pagesDashboard MatrixJEnnife rHifeNo ratings yet

- Lect 11TVDocument25 pagesLect 11TVsalman siddiqui100% (1)

- Integration: Organization StructureDocument39 pagesIntegration: Organization StructureSantosh TripathiNo ratings yet

- Ias2 SNDocument7 pagesIas2 SNEmaan QaiserNo ratings yet

- Periodic and Perpetual Inventory SystemsDocument17 pagesPeriodic and Perpetual Inventory SystemsMichael Brian TorresNo ratings yet

- Inventory Part 1Document32 pagesInventory Part 1Leddie Bergs Villanueva VelascoNo ratings yet

- Inventory Management, Supply Contracts and Risk PoolingDocument81 pagesInventory Management, Supply Contracts and Risk PoolingnaniagricoNo ratings yet

- Part 4: Absorption and Variable Costing/Product Costing: Melziel A. Emba University of The East - ManilaDocument129 pagesPart 4: Absorption and Variable Costing/Product Costing: Melziel A. Emba University of The East - Manilarodell pabloNo ratings yet

- As 2Document7 pagesAs 2sanjay sNo ratings yet

- Chapter 5 Inventories and CGSDocument68 pagesChapter 5 Inventories and CGSZemene HailuNo ratings yet

- Chapter InventoriesDocument38 pagesChapter Inventoriesangellachavezlabalan.cpalawyerNo ratings yet

- Accounting Entries OPMDocument8 pagesAccounting Entries OPMzeeshan78100% (1)

- Inventory Systems and Periodic Recap PDFDocument4 pagesInventory Systems and Periodic Recap PDFMicah Ellah Reynoso PatindolNo ratings yet

- Just in Time and Backflush Accounting - 0Document27 pagesJust in Time and Backflush Accounting - 0pam pamNo ratings yet

- 08 Ias 2Document3 pages08 Ias 2Irtiza AbbasNo ratings yet

- Inleiding Tot de Logistiek (3542) : Prof. Dr. Kris BraekersDocument54 pagesInleiding Tot de Logistiek (3542) : Prof. Dr. Kris BraekersJoost VerheyenNo ratings yet

- Economic Cost OrderDocument28 pagesEconomic Cost OrderPiyam RazaNo ratings yet

- NAS 2 Inventories - UnlockedDocument33 pagesNAS 2 Inventories - UnlockedAviTvNo ratings yet

- Int Acct Chap 2Document12 pagesInt Acct Chap 2Kimberly NicoleNo ratings yet

- PPA 4 InventoriesDocument8 pagesPPA 4 Inventoriesbullalulla840No ratings yet

- Class Meeting 01 Cost Concepts, Manufacturing Cost, and Cost FlowsDocument55 pagesClass Meeting 01 Cost Concepts, Manufacturing Cost, and Cost FlowsRatu Shavira100% (1)

- Topic 7 - Absorption & Marginal CostingDocument8 pagesTopic 7 - Absorption & Marginal CostingMuhammad Alif100% (5)

- Finacial and Managerial Act Chapter 5-7Document59 pagesFinacial and Managerial Act Chapter 5-7solomon asefaNo ratings yet

- Financial Reporting Standards (Pas # 2) : Inventory Accounting Recognition, Measurement and DisclosuresDocument51 pagesFinancial Reporting Standards (Pas # 2) : Inventory Accounting Recognition, Measurement and DisclosuresKylieNo ratings yet

- SAP Accounting EntriesDocument8 pagesSAP Accounting Entriesprodigious84No ratings yet

- Business Metrics and Tools; Reference for Professionals and StudentsFrom EverandBusiness Metrics and Tools; Reference for Professionals and StudentsNo ratings yet

- Beyond Earnings: Applying the HOLT CFROI and Economic Profit FrameworkFrom EverandBeyond Earnings: Applying the HOLT CFROI and Economic Profit FrameworkNo ratings yet