Download as pdf or txt

You might also like

- 57427bos46506mod4cp8 U2 PDFDocument43 pages57427bos46506mod4cp8 U2 PDFAmnNo ratings yet

- Risk Flags Action PointDocument5 pagesRisk Flags Action PointAudit Circle IV BhavnagarNo ratings yet

- How to Handle Goods and Service Tax (GST)From EverandHow to Handle Goods and Service Tax (GST)Rating: 4.5 out of 5 stars4.5/5 (4)

- Screenshot 2020-08-05 at 3.15.16 PM PDFDocument2 pagesScreenshot 2020-08-05 at 3.15.16 PM PDFShiv ChauhanNo ratings yet

- Profit Loss - 12month ComparisonDocument2 pagesProfit Loss - 12month ComparisonIbrahim SyedNo ratings yet

- Name: Farwa Samreen ID: 12048 Course: Cost & Management Accounting Instructor: Sir, Yaseen Raza TurabiDocument7 pagesName: Farwa Samreen ID: 12048 Course: Cost & Management Accounting Instructor: Sir, Yaseen Raza TurabiFarwa SamreenNo ratings yet

- .. (Type: Headline That Outlines Key Performance) : Reconciliation To Corporate Tax Rate Reported TaxDocument1 page.. (Type: Headline That Outlines Key Performance) : Reconciliation To Corporate Tax Rate Reported TaxMore TaxNo ratings yet

- Launch Jasper ReportDocument2 pagesLaunch Jasper Reportakmeljundi092No ratings yet

- Solved - Trinity Electro Case - Class WorkDocument5 pagesSolved - Trinity Electro Case - Class WorkPrarthuTandon0% (1)

- Standard - Income STMNT 2020-2021-2Document1 pageStandard - Income STMNT 2020-2021-2ssicaru salud velazquezNo ratings yet

- Baldwin 4Document4 pagesBaldwin 4api-455849499No ratings yet

- Business FinanceDocument35 pagesBusiness FinanceAliyah Belleza MusaNo ratings yet

- Vat Summary-30-09-2010Document2 pagesVat Summary-30-09-2010anon_978060No ratings yet

- Guide To Quarterly VAT ReturnDocument14 pagesGuide To Quarterly VAT ReturnMary Jane MarañoNo ratings yet

- Plas Mech BS 07-08Document32 pagesPlas Mech BS 07-08plasmechNo ratings yet

- Nov2023Document2 pagesNov2023ManiNo ratings yet

- W38W7TV GST InvoiceDocument1 pageW38W7TV GST InvoiceJ MANJUSREENo ratings yet

- Launch Jasper ReportDocument2 pagesLaunch Jasper ReportmttarvNo ratings yet

- Tax Invoice: Bill Amount: 3300.00Document1 pageTax Invoice: Bill Amount: 3300.00Akshay SaneparaNo ratings yet

- Payslip - May - 2020 PDFDocument1 pagePayslip - May - 2020 PDFchanduNo ratings yet

- Invoice 123Document1 pageInvoice 123ANMOL SUKHDEVENo ratings yet

- Alison Is Qualifies To Income Tax From Business and Compensation, OSD and 8% Fixed Tax RateDocument7 pagesAlison Is Qualifies To Income Tax From Business and Compensation, OSD and 8% Fixed Tax RateNichole TumulakNo ratings yet

- Creative Chips Case StudyDocument6 pagesCreative Chips Case StudyDhruvi GandhiNo ratings yet

- Month Net Taxable Income Tax Slabs Tax RateDocument2 pagesMonth Net Taxable Income Tax Slabs Tax RateBhargav ChintalapatiNo ratings yet

- Anexa 3 - Buget Si Previziuni Financiare-Bivolaru RebecaDocument24 pagesAnexa 3 - Buget Si Previziuni Financiare-Bivolaru RebecaRebeca BivolaruNo ratings yet

- Anwar Group of IndustriesDocument1 pageAnwar Group of IndustriesMoment RevealersNo ratings yet

- Name: - Yr. and SectionDocument4 pagesName: - Yr. and SectionClarisse AlimotNo ratings yet

- Doctor Bill Format 01Document1 pageDoctor Bill Format 01Krishna SharmaNo ratings yet

- Project Income CalculatorDocument4 pagesProject Income CalculatorMahmoud ElmohamdyNo ratings yet

- Profit or LossDocument1 pageProfit or LossKryss Clyde TabliganNo ratings yet

- Cash FlowDocument3 pagesCash Flowkl2304013112No ratings yet

- GSTDocument19 pagesGSTbhavna khatwaniNo ratings yet

- Massage 2Document2 pagesMassage 2NitinNo ratings yet

- Decrypted ITCS 1514082 Jan-24Document2 pagesDecrypted ITCS 1514082 Jan-24Hemanth KumarNo ratings yet

- Doctor Bill Format 04Document3 pagesDoctor Bill Format 04vdsastationNo ratings yet

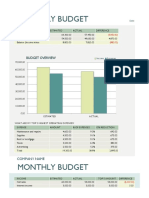

- Monthly Budget Test: Company NameDocument4 pagesMonthly Budget Test: Company NameveeraaaNo ratings yet

- Anlysis For PMGSY Road On HPSR 2016.Document295 pagesAnlysis For PMGSY Road On HPSR 2016.kashish bhardwaj100% (1)

- Consm Jul 20 NewDocument1 pageConsm Jul 20 NewSoumya SwainNo ratings yet

- SalarySlipwithTaxDetailsDocument1 pageSalarySlipwithTaxDetailsabhigopal444No ratings yet

- Less: Cost of Goods Sold: Net Income After Tax: 474,222.00Document3 pagesLess: Cost of Goods Sold: Net Income After Tax: 474,222.00Daniella Mae ElipNo ratings yet

- GST NotesDocument94 pagesGST NotesDiksha AroraNo ratings yet

- Comp 2 ActivitiesDocument4 pagesComp 2 ActivitiesMARINETH SALIGUMBANo ratings yet

- Fluturasi Lichidare Iul 20 DIVEICA CORNELIA PDFDocument1 pageFluturasi Lichidare Iul 20 DIVEICA CORNELIA PDFGeorgeSiCamiNeaguNo ratings yet

- Buying Options : Freehold - Without MortgageDocument17 pagesBuying Options : Freehold - Without MortgageВојислав КовачевићNo ratings yet

- Monthly Business BudgetDocument4 pagesMonthly Business BudgetOkasha HafeezNo ratings yet

- Launch Jasper ReportDocument2 pagesLaunch Jasper ReportNaaben AbNo ratings yet

- Monthly Budget: Company NameDocument2 pagesMonthly Budget: Company NameMalleshNo ratings yet

- Graduated Income Tax 8% Flat RateDocument2 pagesGraduated Income Tax 8% Flat RateAndy ArenasNo ratings yet

- 06mar - CCA Worksheet - Pt2 - CompletedDocument14 pages06mar - CCA Worksheet - Pt2 - Completedsrishtirungta2000No ratings yet

- Addisu Tadesse Adj FSDocument6 pagesAddisu Tadesse Adj FSGali AbamededNo ratings yet

- Basic Accounting ExerciseDocument5 pagesBasic Accounting ExercisechubbybunbunNo ratings yet

- Itemized Deduction Vs Optional Standard Deductions 40OSDDocument4 pagesItemized Deduction Vs Optional Standard Deductions 40OSDjason genitaNo ratings yet

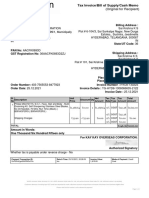

- Tax Invoice/ Tax Credit Note: You Can Find More Information On Where and How To Pay Your Bill byDocument7 pagesTax Invoice/ Tax Credit Note: You Can Find More Information On Where and How To Pay Your Bill bylivefruitbazaar1122No ratings yet

- Chapter 1 GST (Goods and Services Tax)Document17 pagesChapter 1 GST (Goods and Services Tax)Venu Gopal100% (1)

- Capistrano's Shape Up Center Trial Balance: As of January 31, 2020Document2 pagesCapistrano's Shape Up Center Trial Balance: As of January 31, 2020Ryan CapistranoNo ratings yet

- Profit & Loss Account of Reliance Industries - in Rs. Cr.Document9 pagesProfit & Loss Account of Reliance Industries - in Rs. Cr.Mansi DeokarNo ratings yet

- Please Kindly Joint With Us For More:: - Facebook Group: Cambodia Accounting and TaxDocument2 pagesPlease Kindly Joint With Us For More:: - Facebook Group: Cambodia Accounting and TaxLay TekchhayNo ratings yet

- Declaration 1726107Document4 pagesDeclaration 1726107Hanzala NasirNo ratings yet

- Feb PayslipDocument1 pageFeb Payslipnegishilpa051No ratings yet

- Declaration 0659861Document6 pagesDeclaration 0659861Hanzala NasirNo ratings yet

- Edelweiss 2Document1 pageEdelweiss 2JitendraBhartiNo ratings yet

- Train Ticket-Nagarsole To SecunderabadDocument2 pagesTrain Ticket-Nagarsole To SecunderabadglobalrecruitementsNo ratings yet

- Shyamlal TKTDocument1 pageShyamlal TKTkumar shahNo ratings yet

- Impact of GST On Logistics Sector: Submitted To - Sebastian DanielDocument11 pagesImpact of GST On Logistics Sector: Submitted To - Sebastian Danielsaurav singh100% (1)

- Bianchi Casseforme India PVT Ltd.Document1 pageBianchi Casseforme India PVT Ltd.Paras ShahNo ratings yet

- Goods-And-Services-Tax-Gst Solved MCQs (Set-4)Document8 pagesGoods-And-Services-Tax-Gst Solved MCQs (Set-4)Ayushi BhardwajNo ratings yet

- Central Coalfields LimitedDocument26 pagesCentral Coalfields Limitedjaio88No ratings yet

- AC GST Tax InvoiceDocument3 pagesAC GST Tax InvoiceVijay KumarNo ratings yet

- Sample Paper 2Document8 pagesSample Paper 2Kanha BSNo ratings yet

- CRN6658709424Document3 pagesCRN6658709424ranjithreddy916gmailNo ratings yet

- GST Chapter 1Document21 pagesGST Chapter 1Dhriti UmmatNo ratings yet

- Mathematics Book Book 1701441017923Document2 pagesMathematics Book Book 1701441017923tanmaybonde30No ratings yet

- TAX Invoice: SJ ProjectsDocument1 pageTAX Invoice: SJ ProjectsBizEasy AdvisorsNo ratings yet

- 952085825042023INPTPBSB21250420230811Document5 pages952085825042023INPTPBSB21250420230811Eva Akash100% (1)

- OD124238512779415000Document4 pagesOD124238512779415000broken heart “Satyam singh”No ratings yet

- All About E-Ledgers Under GST - E-Cash Ledger, E-Credit Ledger & E-Liability LedgerDocument4 pagesAll About E-Ledgers Under GST - E-Cash Ledger, E-Credit Ledger & E-Liability LedgerDINESH CHANCHALANINo ratings yet

- Idt Aac2Document27 pagesIdt Aac2Vinay KumarNo ratings yet

- (INV0004) Oracle Inventory How To Setup Shortage Parameter and Notifications - Oracle Apps SCM Functional GuideDocument5 pages(INV0004) Oracle Inventory How To Setup Shortage Parameter and Notifications - Oracle Apps SCM Functional GuideAKSHAY PALEKARNo ratings yet

- Invoice DI102305154 RDF52626464Document1 pageInvoice DI102305154 RDF52626464Harbans LalNo ratings yet

- Asus Laptop2 Invoice Ganesh Prasad HDocument1 pageAsus Laptop2 Invoice Ganesh Prasad HganeshNo ratings yet

- OD125147442787674000Document4 pagesOD125147442787674000Sonam KalaNo ratings yet

- PDF 1697193486463Document2 pagesPDF 1697193486463Ritesh GhoshNo ratings yet

- InvoiceDocument1 pageInvoiceMã H IêNo ratings yet

- Goods & Services Tax (G.S.T.)Document15 pagesGoods & Services Tax (G.S.T.)EshanMishra100% (1)

- 12105/vidarbha Express Third Ac (3A) : WL WLDocument3 pages12105/vidarbha Express Third Ac (3A) : WL WL21f1000067No ratings yet

- Trimmer - Invoice PDFDocument1 pageTrimmer - Invoice PDFsai krishna krishna shasthrulaNo ratings yet

- Good & Service Tax: 1. What Is GST?Document5 pagesGood & Service Tax: 1. What Is GST?Rabin DebnathNo ratings yet

- SAC Code PDFDocument2 pagesSAC Code PDFKushaldas patelNo ratings yet

- The New India Assurance Co. LTDDocument3 pagesThe New India Assurance Co. LTDsarath potnuriNo ratings yet