M/Chip Functional Architecture For Debit and Credit: Applies To: Summary

M/Chip Functional Architecture For Debit and Credit: Applies To: Summary

You might also like

- Verifone Vx805 DsiEMVUS Platform Integration Guide SupplementDocument60 pagesVerifone Vx805 DsiEMVUS Platform Integration Guide SupplementHammad ShaukatNo ratings yet

- Ethoca Merchant Data Provision API Integration Guide V 3.0.1 (February 13, 2019)Document13 pagesEthoca Merchant Data Provision API Integration Guide V 3.0.1 (February 13, 2019)NastasVasileNo ratings yet

- Section 1. What's New: This Readme File Contains These SectionsDocument6 pagesSection 1. What's New: This Readme File Contains These SectionsNishant SharmaNo ratings yet

- Swift: Icbpo Irrevocable Conditional Bank Pay Order: TRANSACTION CODEDocument2 pagesSwift: Icbpo Irrevocable Conditional Bank Pay Order: TRANSACTION CODEdavid patrick100% (2)

- SessionDocument8 pagesSessionIngrid Vaughn100% (1)

- EMV Contactless Kernel PR FINALDocument2 pagesEMV Contactless Kernel PR FINALPriyanka PalNo ratings yet

- Payment Card Industry 3-D Secure (PCI 3DS)Document7 pagesPayment Card Industry 3-D Secure (PCI 3DS)Al QUinNo ratings yet

- GP Guidelines For Developing Apps On GP Cards V1.0aDocument65 pagesGP Guidelines For Developing Apps On GP Cards V1.0aCharlieBrown100% (2)

- Terminal Information To Enhance Contactless Application SelectionDocument10 pagesTerminal Information To Enhance Contactless Application SelectionSaradhi MedapureddyNo ratings yet

- MasterCard Regional Pricing BulletinDocument4 pagesMasterCard Regional Pricing Bulletinsoricel23No ratings yet

- Postilion Developer ExternalDocument2 pagesPostilion Developer ExternalMwansa MachaloNo ratings yet

- 80 Byte Population Guide - v15.94Document216 pages80 Byte Population Guide - v15.94HMNo ratings yet

- QRCode-v-1 3Document32 pagesQRCode-v-1 3Mohammed KhalidNo ratings yet

- Collis b2 Emv and Contactless OfferingDocument52 pagesCollis b2 Emv and Contactless OfferingmuratNo ratings yet

- EPC020-08 Book 3 - Data Elements - SCS Volume v7.1Document104 pagesEPC020-08 Book 3 - Data Elements - SCS Volume v7.1Makarand LonkarNo ratings yet

- PCI TSP Requirements v1Document92 pagesPCI TSP Requirements v1Juan Cuba AlarcónNo ratings yet

- Kernel C 4 Specification v2.11Document165 pagesKernel C 4 Specification v2.11Robinson MarquesNo ratings yet

- csfb400 Icsf Apg hcr77d1 PDFDocument1,720 pagescsfb400 Icsf Apg hcr77d1 PDFPalmira PérezNo ratings yet

- Terms and DefinitonsDocument23 pagesTerms and DefinitonsMai Nam ThangNo ratings yet

- Iso 8583 2023Document11 pagesIso 8583 2023Srinivas K100% (1)

- Transaction Processing Rules June 2016Document289 pagesTransaction Processing Rules June 2016Armando ReyNo ratings yet

- Visa Chip Simplifying ImplementationDocument2 pagesVisa Chip Simplifying Implementationjagdish kumarNo ratings yet

- 2.5 Support of Merchant Volume Indicator ValuesDocument10 pages2.5 Support of Merchant Volume Indicator ValuesYasir RoniNo ratings yet

- 200-338 - 0.2 Money Controls CcTalk User ManualDocument226 pages200-338 - 0.2 Money Controls CcTalk User ManualRonald M. Diaz0% (2)

- UPI QuickPass Testing Guide For Acquirers - V201905Document14 pagesUPI QuickPass Testing Guide For Acquirers - V201905yoron liu100% (1)

- ISO 14906-2011 ETC 应用层Document120 pagesISO 14906-2011 ETC 应用层中咨No ratings yet

- Mastercard Switch Rules ManualDocument86 pagesMastercard Switch Rules ManualMatteo TorresNo ratings yet

- Operational Support Client Forum PDFDocument129 pagesOperational Support Client Forum PDFASDFGHTNo ratings yet

- DCI Contact D-PAS Acquirer Host Test Plan v1.2Document89 pagesDCI Contact D-PAS Acquirer Host Test Plan v1.2Roger Cardenas100% (1)

- Biblioteca EMV ContactlessDocument34 pagesBiblioteca EMV ContactlessEder Nunes JúniorNo ratings yet

- Visa USA Interchange Reimbursement FeesDocument26 pagesVisa USA Interchange Reimbursement FeesMark Jasper DabuNo ratings yet

- DOC00310 Verix EVo ACT Programmers GuideDocument348 pagesDOC00310 Verix EVo ACT Programmers GuideFernando75% (4)

- Part II Extended Purchase Specification Based On Contactless Low-Value Payment ApplicationDocument67 pagesPart II Extended Purchase Specification Based On Contactless Low-Value Payment ApplicationMai Nam ThangNo ratings yet

- Contactless Cards WorkingDocument4 pagesContactless Cards WorkingdineshNo ratings yet

- PP MTIP UserGuide Dec2011Document201 pagesPP MTIP UserGuide Dec2011AzzaHassanienNo ratings yet

- PayPass v3 TTAL2-Testing Env Nov2013Document63 pagesPayPass v3 TTAL2-Testing Env Nov2013Phạm Tiến ThànhNo ratings yet

- 7 EMVCo Level3 Framework Implementation Guidelines V 1 1 20190411Document103 pages7 EMVCo Level3 Framework Implementation Guidelines V 1 1 20190411Solomon BuiNo ratings yet

- TIP Entire ManualDocument105 pagesTIP Entire ManualmuratNo ratings yet

- EMV Security Review Emms, M. 2016Document164 pagesEMV Security Review Emms, M. 2016JoDo SayaNo ratings yet

- PayPass - MChip - Acquirer - Imlementation - Requirements - PPMCAIR (V1.0 - July 2008)Document88 pagesPayPass - MChip - Acquirer - Imlementation - Requirements - PPMCAIR (V1.0 - July 2008)berghauptmannNo ratings yet

- Ingenico Driver Installer Release Note ICO-OPE-2012-0820-LTDocument5 pagesIngenico Driver Installer Release Note ICO-OPE-2012-0820-LTtimmyJackson100% (1)

- ATPC Install and Ops Guide 3.10 529056-002 PDFDocument251 pagesATPC Install and Ops Guide 3.10 529056-002 PDFsathish kumarNo ratings yet

- BPC - ER - A1N0170 - Acleda - Fraud Managent v1.0Document54 pagesBPC - ER - A1N0170 - Acleda - Fraud Managent v1.0jch bpcNo ratings yet

- Cwa14050 42 2005 JanDocument49 pagesCwa14050 42 2005 JanoirrazaNo ratings yet

- QVSDC IRWIN Testing ProcessDocument8 pagesQVSDC IRWIN Testing ProcessLewisMuneneNo ratings yet

- ARQC and ARPCDocument3 pagesARQC and ARPCMayur GowdaNo ratings yet

- As 2805.4.2-2006 Electronic Funds Transfer - Requirements For Interfaces Message Authentication - MechanismsDocument8 pagesAs 2805.4.2-2006 Electronic Funds Transfer - Requirements For Interfaces Message Authentication - MechanismsSAI Global - APACNo ratings yet

- EMV Contactless Book C 8 Kernel 8 Specification v1.1 BookmarksDocument303 pagesEMV Contactless Book C 8 Kernel 8 Specification v1.1 BookmarksRobinson MarquesNo ratings yet

- S7000 OperatorManual 1.3Document48 pagesS7000 OperatorManual 1.3Zagiza TuNo ratings yet

- Fis 8583-2017Document600 pagesFis 8583-2017HipHop MarocNo ratings yet

- EPC342-08 Guidelines On Algorithms and Key ManagementDocument57 pagesEPC342-08 Guidelines On Algorithms and Key ManagementScoobs72No ratings yet

- TEUSERDocument98 pagesTEUSERdsr_ecNo ratings yet

- ANZ EGate Virtual Payment Client Guide Rev 1.2Document74 pagesANZ EGate Virtual Payment Client Guide Rev 1.2Nigel GarciaNo ratings yet

- Card Banking 2Document66 pagesCard Banking 2markos mamadeNo ratings yet

- As 2805.9-2000 Electronic Funds Transfer - Requirements For Interfaces Privacy of CommunicationsDocument7 pagesAs 2805.9-2000 Electronic Funds Transfer - Requirements For Interfaces Privacy of CommunicationsSAI Global - APACNo ratings yet

- MACA ManualDocument597 pagesMACA ManualPrabin ShresthaNo ratings yet

- ArticleforPaymentsSystemsMagazine-13 11 05Document14 pagesArticleforPaymentsSystemsMagazine-13 11 05Syed RazviNo ratings yet

- GlobalPayments Technical SpecificationsDocument66 pagesGlobalPayments Technical SpecificationssanpikNo ratings yet

- ATKEYBLWPDocument9 pagesATKEYBLWPOlusola TalabiNo ratings yet

- 91statistics Annual91Document171 pages91statistics Annual91Abiy MulugetaNo ratings yet

- Efrn 61603Document16 pagesEfrn 61603Abiy MulugetaNo ratings yet

- IE DemandsDocument2 pagesIE DemandsAbiy MulugetaNo ratings yet

- Fundamental Data Mining in Institutional Research WorkshopDocument68 pagesFundamental Data Mining in Institutional Research WorkshopAbiy MulugetaNo ratings yet

- The Application of Data Mining To Support Custemer Relationship Management at Ethiopian AirlinesDocument140 pagesThe Application of Data Mining To Support Custemer Relationship Management at Ethiopian AirlinesAbiy MulugetaNo ratings yet

- Enrollment Prediction - ProjectDocument17 pagesEnrollment Prediction - ProjectAbiy MulugetaNo ratings yet

- Ii - What Is Data Mining?Document4 pagesIi - What Is Data Mining?Abiy MulugetaNo ratings yet

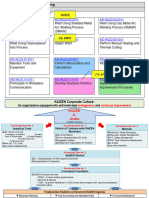

- KAIZEN Road Map & OSDocument2 pagesKAIZEN Road Map & OSAbiy MulugetaNo ratings yet

- Va Enrollment Demand Projection-2001-2010Document62 pagesVa Enrollment Demand Projection-2001-2010Abiy MulugetaNo ratings yet

- Poster FinalDocument1 pagePoster FinalAbiy MulugetaNo ratings yet

- Enrollment StudyDocument33 pagesEnrollment StudyAbiy MulugetaNo ratings yet

- TagarelaDocument11 pagesTagarelaAbiy MulugetaNo ratings yet

- Article 4Document13 pagesArticle 4Abiy MulugetaNo ratings yet

- Paper 28Document6 pagesPaper 28Abiy MulugetaNo ratings yet

- Segmentation of Cells From MicroscopicDocument67 pagesSegmentation of Cells From MicroscopicAbiy MulugetaNo ratings yet

- Vol 101Document124 pagesVol 101Abiy MulugetaNo ratings yet

- SWStutorial ICWE2005Document220 pagesSWStutorial ICWE2005Abiy MulugetaNo ratings yet

- Text Categorization and ClassificationDocument13 pagesText Categorization and ClassificationAbiy MulugetaNo ratings yet

- Python TutorialDocument88 pagesPython TutorialAbiy MulugetaNo ratings yet

- System LinqDocument1,024 pagesSystem LinqAbiy MulugetaNo ratings yet

- Microsoft VisualBasic FileIODocument181 pagesMicrosoft VisualBasic FileIOAbiy MulugetaNo ratings yet

- ED474143Document20 pagesED474143Abiy MulugetaNo ratings yet

- Visa Global Level 3 L3 Testing Guidelines and FAQ Version 1.14 - Build 015 - FINAL - 061523Document8 pagesVisa Global Level 3 L3 Testing Guidelines and FAQ Version 1.14 - Build 015 - FINAL - 061523Abiy MulugetaNo ratings yet

- SPECTRA-SoftPOS ENDocument3 pagesSPECTRA-SoftPOS ENAbiy MulugetaNo ratings yet

- Contactless Mester CardDocument1 pageContactless Mester CardAbiy MulugetaNo ratings yet

- Prediction of Students' Educational Status Using CART Algorithm, Neural Network, and Increase in Prediction Precision Using Combinational ModelDocument5 pagesPrediction of Students' Educational Status Using CART Algorithm, Neural Network, and Increase in Prediction Precision Using Combinational ModelAbiy MulugetaNo ratings yet

- E Book TokenizationDocument8 pagesE Book TokenizationAbiy MulugetaNo ratings yet

- TokenisationDocument2 pagesTokenisationAbiy MulugetaNo ratings yet

- Emvco Keynote The Future of Contactless Payments Slides 001Document21 pagesEmvco Keynote The Future of Contactless Payments Slides 001Abiy MulugetaNo ratings yet

- Visa - Public - Key - Tables - Accessible - Reformatted 15 Sep 23 (1) - ACCESSIBLEDocument9 pagesVisa - Public - Key - Tables - Accessible - Reformatted 15 Sep 23 (1) - ACCESSIBLEAbiy MulugetaNo ratings yet

- Guitar Ensembles Steve Marsh: A Benslow Music CourseDocument4 pagesGuitar Ensembles Steve Marsh: A Benslow Music Courseapi-210427398No ratings yet

- Standard Chartered Online Banking - ZWDocument2 pagesStandard Chartered Online Banking - ZWrussell makosaNo ratings yet

- Difference Between Pay Order and Demand DraftDocument3 pagesDifference Between Pay Order and Demand DraftAman DegraNo ratings yet

- India and BankingDocument3 pagesIndia and BankingJanu PriyaNo ratings yet

- Modeling Customers Intention To Use E-Wallet in ADocument5 pagesModeling Customers Intention To Use E-Wallet in AFaten bakloutiNo ratings yet

- 201908Document1 page201908HarryNo ratings yet

- TRM N61 V JC OMTKD7Document8 pagesTRM N61 V JC OMTKD7Mukesh Kumar DubeyNo ratings yet

- ADocument3 pagesApradeepNo ratings yet

- List of Conditions Effective From 01-04-2017Document13 pagesList of Conditions Effective From 01-04-2017omidreza tabrizianNo ratings yet

- JAIIB Principles of Banking Module C NewDocument16 pagesJAIIB Principles of Banking Module C News1508198767% (3)

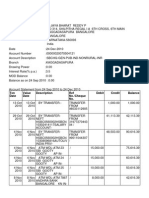

- Bruno - Gomes Statement 2021 07Document4 pagesBruno - Gomes Statement 2021 07B gNo ratings yet

- Calculate EMV Cryptogram ARQC-ARPC For ISO8583 PaymentsDocument6 pagesCalculate EMV Cryptogram ARQC-ARPC For ISO8583 Paymentssajad salehiNo ratings yet

- Ach Code CardDocument2 pagesAch Code CardSankaetPathakNo ratings yet

- PH 9 HK 2 y 3 GGu 4 ZWLNDocument6 pagesPH 9 HK 2 y 3 GGu 4 ZWLNRanjit BeheraNo ratings yet

- Plastic Money Full ProjectDocument54 pagesPlastic Money Full ProjectNevil Surani76% (169)

- COMIN Egypt Launch Strategy-VFDocument45 pagesCOMIN Egypt Launch Strategy-VFSallam BakeerNo ratings yet

- Information On Payment Services Corporate 13.1.2018Document19 pagesInformation On Payment Services Corporate 13.1.2018Riciu IonutNo ratings yet

- Formato Recepcion UsdDocument1 pageFormato Recepcion UsdRicardo Villalón WNo ratings yet

- 279 Villas: Jalan Baik - Baik Nakula BaratDocument4 pages279 Villas: Jalan Baik - Baik Nakula BaratmarkNo ratings yet

- State Bank Collect Reprint Remittance Form Payment HistoryDocument1 pageState Bank Collect Reprint Remittance Form Payment HistoryBinayakSwainNo ratings yet

- Soal Siklus 2Document5 pagesSoal Siklus 2Darmadi0% (1)

- MrcInvoices November2022 272286Document1 pageMrcInvoices November2022 272286Saad AzmatNo ratings yet

- Chartered Accountant 2 0Document3 pagesChartered Accountant 2 0RkNo ratings yet

- 3-D Secure Vendor List v1 10-30-20181Document4 pages3-D Secure Vendor List v1 10-30-20181Mohamed LahlouNo ratings yet

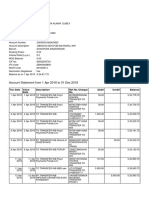

- BOM Statement xxxxxxxx4898 20190401 20191009 20191009022924 PDFDocument14 pagesBOM Statement xxxxxxxx4898 20190401 20191009 20191009022924 PDFtrupti jadhavNo ratings yet

- Upi ProjectDocument26 pagesUpi Projectradheshyamsharma9953No ratings yet

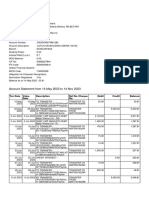

- TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument4 pagesTXN Date Value Date Description Ref No./Cheque No. Debit Credit Balanceswetha_muthumulaNo ratings yet

- 7588 Ca 3891 C 0Document56 pages7588 Ca 3891 C 0luuuNo ratings yet

Download as pdf or txt

You might also like

- Verifone Vx805 DsiEMVUS Platform Integration Guide SupplementDocument60 pagesVerifone Vx805 DsiEMVUS Platform Integration Guide SupplementHammad ShaukatNo ratings yet

- Ethoca Merchant Data Provision API Integration Guide V 3.0.1 (February 13, 2019)Document13 pagesEthoca Merchant Data Provision API Integration Guide V 3.0.1 (February 13, 2019)NastasVasileNo ratings yet

- Section 1. What's New: This Readme File Contains These SectionsDocument6 pagesSection 1. What's New: This Readme File Contains These SectionsNishant SharmaNo ratings yet

- Swift: Icbpo Irrevocable Conditional Bank Pay Order: TRANSACTION CODEDocument2 pagesSwift: Icbpo Irrevocable Conditional Bank Pay Order: TRANSACTION CODEdavid patrick100% (2)

- SessionDocument8 pagesSessionIngrid Vaughn100% (1)

- EMV Contactless Kernel PR FINALDocument2 pagesEMV Contactless Kernel PR FINALPriyanka PalNo ratings yet

- Payment Card Industry 3-D Secure (PCI 3DS)Document7 pagesPayment Card Industry 3-D Secure (PCI 3DS)Al QUinNo ratings yet

- GP Guidelines For Developing Apps On GP Cards V1.0aDocument65 pagesGP Guidelines For Developing Apps On GP Cards V1.0aCharlieBrown100% (2)

- Terminal Information To Enhance Contactless Application SelectionDocument10 pagesTerminal Information To Enhance Contactless Application SelectionSaradhi MedapureddyNo ratings yet

- MasterCard Regional Pricing BulletinDocument4 pagesMasterCard Regional Pricing Bulletinsoricel23No ratings yet

- Postilion Developer ExternalDocument2 pagesPostilion Developer ExternalMwansa MachaloNo ratings yet

- 80 Byte Population Guide - v15.94Document216 pages80 Byte Population Guide - v15.94HMNo ratings yet

- QRCode-v-1 3Document32 pagesQRCode-v-1 3Mohammed KhalidNo ratings yet

- Collis b2 Emv and Contactless OfferingDocument52 pagesCollis b2 Emv and Contactless OfferingmuratNo ratings yet

- EPC020-08 Book 3 - Data Elements - SCS Volume v7.1Document104 pagesEPC020-08 Book 3 - Data Elements - SCS Volume v7.1Makarand LonkarNo ratings yet

- PCI TSP Requirements v1Document92 pagesPCI TSP Requirements v1Juan Cuba AlarcónNo ratings yet

- Kernel C 4 Specification v2.11Document165 pagesKernel C 4 Specification v2.11Robinson MarquesNo ratings yet

- csfb400 Icsf Apg hcr77d1 PDFDocument1,720 pagescsfb400 Icsf Apg hcr77d1 PDFPalmira PérezNo ratings yet

- Terms and DefinitonsDocument23 pagesTerms and DefinitonsMai Nam ThangNo ratings yet

- Iso 8583 2023Document11 pagesIso 8583 2023Srinivas K100% (1)

- Transaction Processing Rules June 2016Document289 pagesTransaction Processing Rules June 2016Armando ReyNo ratings yet

- Visa Chip Simplifying ImplementationDocument2 pagesVisa Chip Simplifying Implementationjagdish kumarNo ratings yet

- 2.5 Support of Merchant Volume Indicator ValuesDocument10 pages2.5 Support of Merchant Volume Indicator ValuesYasir RoniNo ratings yet

- 200-338 - 0.2 Money Controls CcTalk User ManualDocument226 pages200-338 - 0.2 Money Controls CcTalk User ManualRonald M. Diaz0% (2)

- UPI QuickPass Testing Guide For Acquirers - V201905Document14 pagesUPI QuickPass Testing Guide For Acquirers - V201905yoron liu100% (1)

- ISO 14906-2011 ETC 应用层Document120 pagesISO 14906-2011 ETC 应用层中咨No ratings yet

- Mastercard Switch Rules ManualDocument86 pagesMastercard Switch Rules ManualMatteo TorresNo ratings yet

- Operational Support Client Forum PDFDocument129 pagesOperational Support Client Forum PDFASDFGHTNo ratings yet

- DCI Contact D-PAS Acquirer Host Test Plan v1.2Document89 pagesDCI Contact D-PAS Acquirer Host Test Plan v1.2Roger Cardenas100% (1)

- Biblioteca EMV ContactlessDocument34 pagesBiblioteca EMV ContactlessEder Nunes JúniorNo ratings yet

- Visa USA Interchange Reimbursement FeesDocument26 pagesVisa USA Interchange Reimbursement FeesMark Jasper DabuNo ratings yet

- DOC00310 Verix EVo ACT Programmers GuideDocument348 pagesDOC00310 Verix EVo ACT Programmers GuideFernando75% (4)

- Part II Extended Purchase Specification Based On Contactless Low-Value Payment ApplicationDocument67 pagesPart II Extended Purchase Specification Based On Contactless Low-Value Payment ApplicationMai Nam ThangNo ratings yet

- Contactless Cards WorkingDocument4 pagesContactless Cards WorkingdineshNo ratings yet

- PP MTIP UserGuide Dec2011Document201 pagesPP MTIP UserGuide Dec2011AzzaHassanienNo ratings yet

- PayPass v3 TTAL2-Testing Env Nov2013Document63 pagesPayPass v3 TTAL2-Testing Env Nov2013Phạm Tiến ThànhNo ratings yet

- 7 EMVCo Level3 Framework Implementation Guidelines V 1 1 20190411Document103 pages7 EMVCo Level3 Framework Implementation Guidelines V 1 1 20190411Solomon BuiNo ratings yet

- TIP Entire ManualDocument105 pagesTIP Entire ManualmuratNo ratings yet

- EMV Security Review Emms, M. 2016Document164 pagesEMV Security Review Emms, M. 2016JoDo SayaNo ratings yet

- PayPass - MChip - Acquirer - Imlementation - Requirements - PPMCAIR (V1.0 - July 2008)Document88 pagesPayPass - MChip - Acquirer - Imlementation - Requirements - PPMCAIR (V1.0 - July 2008)berghauptmannNo ratings yet

- Ingenico Driver Installer Release Note ICO-OPE-2012-0820-LTDocument5 pagesIngenico Driver Installer Release Note ICO-OPE-2012-0820-LTtimmyJackson100% (1)

- ATPC Install and Ops Guide 3.10 529056-002 PDFDocument251 pagesATPC Install and Ops Guide 3.10 529056-002 PDFsathish kumarNo ratings yet

- BPC - ER - A1N0170 - Acleda - Fraud Managent v1.0Document54 pagesBPC - ER - A1N0170 - Acleda - Fraud Managent v1.0jch bpcNo ratings yet

- Cwa14050 42 2005 JanDocument49 pagesCwa14050 42 2005 JanoirrazaNo ratings yet

- QVSDC IRWIN Testing ProcessDocument8 pagesQVSDC IRWIN Testing ProcessLewisMuneneNo ratings yet

- ARQC and ARPCDocument3 pagesARQC and ARPCMayur GowdaNo ratings yet

- As 2805.4.2-2006 Electronic Funds Transfer - Requirements For Interfaces Message Authentication - MechanismsDocument8 pagesAs 2805.4.2-2006 Electronic Funds Transfer - Requirements For Interfaces Message Authentication - MechanismsSAI Global - APACNo ratings yet

- EMV Contactless Book C 8 Kernel 8 Specification v1.1 BookmarksDocument303 pagesEMV Contactless Book C 8 Kernel 8 Specification v1.1 BookmarksRobinson MarquesNo ratings yet

- S7000 OperatorManual 1.3Document48 pagesS7000 OperatorManual 1.3Zagiza TuNo ratings yet

- Fis 8583-2017Document600 pagesFis 8583-2017HipHop MarocNo ratings yet

- EPC342-08 Guidelines On Algorithms and Key ManagementDocument57 pagesEPC342-08 Guidelines On Algorithms and Key ManagementScoobs72No ratings yet

- TEUSERDocument98 pagesTEUSERdsr_ecNo ratings yet

- ANZ EGate Virtual Payment Client Guide Rev 1.2Document74 pagesANZ EGate Virtual Payment Client Guide Rev 1.2Nigel GarciaNo ratings yet

- Card Banking 2Document66 pagesCard Banking 2markos mamadeNo ratings yet

- As 2805.9-2000 Electronic Funds Transfer - Requirements For Interfaces Privacy of CommunicationsDocument7 pagesAs 2805.9-2000 Electronic Funds Transfer - Requirements For Interfaces Privacy of CommunicationsSAI Global - APACNo ratings yet

- MACA ManualDocument597 pagesMACA ManualPrabin ShresthaNo ratings yet

- ArticleforPaymentsSystemsMagazine-13 11 05Document14 pagesArticleforPaymentsSystemsMagazine-13 11 05Syed RazviNo ratings yet

- GlobalPayments Technical SpecificationsDocument66 pagesGlobalPayments Technical SpecificationssanpikNo ratings yet

- ATKEYBLWPDocument9 pagesATKEYBLWPOlusola TalabiNo ratings yet

- 91statistics Annual91Document171 pages91statistics Annual91Abiy MulugetaNo ratings yet

- Efrn 61603Document16 pagesEfrn 61603Abiy MulugetaNo ratings yet

- IE DemandsDocument2 pagesIE DemandsAbiy MulugetaNo ratings yet

- Fundamental Data Mining in Institutional Research WorkshopDocument68 pagesFundamental Data Mining in Institutional Research WorkshopAbiy MulugetaNo ratings yet

- The Application of Data Mining To Support Custemer Relationship Management at Ethiopian AirlinesDocument140 pagesThe Application of Data Mining To Support Custemer Relationship Management at Ethiopian AirlinesAbiy MulugetaNo ratings yet

- Enrollment Prediction - ProjectDocument17 pagesEnrollment Prediction - ProjectAbiy MulugetaNo ratings yet

- Ii - What Is Data Mining?Document4 pagesIi - What Is Data Mining?Abiy MulugetaNo ratings yet

- KAIZEN Road Map & OSDocument2 pagesKAIZEN Road Map & OSAbiy MulugetaNo ratings yet

- Va Enrollment Demand Projection-2001-2010Document62 pagesVa Enrollment Demand Projection-2001-2010Abiy MulugetaNo ratings yet

- Poster FinalDocument1 pagePoster FinalAbiy MulugetaNo ratings yet

- Enrollment StudyDocument33 pagesEnrollment StudyAbiy MulugetaNo ratings yet

- TagarelaDocument11 pagesTagarelaAbiy MulugetaNo ratings yet

- Article 4Document13 pagesArticle 4Abiy MulugetaNo ratings yet

- Paper 28Document6 pagesPaper 28Abiy MulugetaNo ratings yet

- Segmentation of Cells From MicroscopicDocument67 pagesSegmentation of Cells From MicroscopicAbiy MulugetaNo ratings yet

- Vol 101Document124 pagesVol 101Abiy MulugetaNo ratings yet

- SWStutorial ICWE2005Document220 pagesSWStutorial ICWE2005Abiy MulugetaNo ratings yet

- Text Categorization and ClassificationDocument13 pagesText Categorization and ClassificationAbiy MulugetaNo ratings yet

- Python TutorialDocument88 pagesPython TutorialAbiy MulugetaNo ratings yet

- System LinqDocument1,024 pagesSystem LinqAbiy MulugetaNo ratings yet

- Microsoft VisualBasic FileIODocument181 pagesMicrosoft VisualBasic FileIOAbiy MulugetaNo ratings yet

- ED474143Document20 pagesED474143Abiy MulugetaNo ratings yet

- Visa Global Level 3 L3 Testing Guidelines and FAQ Version 1.14 - Build 015 - FINAL - 061523Document8 pagesVisa Global Level 3 L3 Testing Guidelines and FAQ Version 1.14 - Build 015 - FINAL - 061523Abiy MulugetaNo ratings yet

- SPECTRA-SoftPOS ENDocument3 pagesSPECTRA-SoftPOS ENAbiy MulugetaNo ratings yet

- Contactless Mester CardDocument1 pageContactless Mester CardAbiy MulugetaNo ratings yet

- Prediction of Students' Educational Status Using CART Algorithm, Neural Network, and Increase in Prediction Precision Using Combinational ModelDocument5 pagesPrediction of Students' Educational Status Using CART Algorithm, Neural Network, and Increase in Prediction Precision Using Combinational ModelAbiy MulugetaNo ratings yet

- E Book TokenizationDocument8 pagesE Book TokenizationAbiy MulugetaNo ratings yet

- TokenisationDocument2 pagesTokenisationAbiy MulugetaNo ratings yet

- Emvco Keynote The Future of Contactless Payments Slides 001Document21 pagesEmvco Keynote The Future of Contactless Payments Slides 001Abiy MulugetaNo ratings yet

- Visa - Public - Key - Tables - Accessible - Reformatted 15 Sep 23 (1) - ACCESSIBLEDocument9 pagesVisa - Public - Key - Tables - Accessible - Reformatted 15 Sep 23 (1) - ACCESSIBLEAbiy MulugetaNo ratings yet

- Guitar Ensembles Steve Marsh: A Benslow Music CourseDocument4 pagesGuitar Ensembles Steve Marsh: A Benslow Music Courseapi-210427398No ratings yet

- Standard Chartered Online Banking - ZWDocument2 pagesStandard Chartered Online Banking - ZWrussell makosaNo ratings yet

- Difference Between Pay Order and Demand DraftDocument3 pagesDifference Between Pay Order and Demand DraftAman DegraNo ratings yet

- India and BankingDocument3 pagesIndia and BankingJanu PriyaNo ratings yet

- Modeling Customers Intention To Use E-Wallet in ADocument5 pagesModeling Customers Intention To Use E-Wallet in AFaten bakloutiNo ratings yet

- 201908Document1 page201908HarryNo ratings yet

- TRM N61 V JC OMTKD7Document8 pagesTRM N61 V JC OMTKD7Mukesh Kumar DubeyNo ratings yet

- ADocument3 pagesApradeepNo ratings yet

- List of Conditions Effective From 01-04-2017Document13 pagesList of Conditions Effective From 01-04-2017omidreza tabrizianNo ratings yet

- JAIIB Principles of Banking Module C NewDocument16 pagesJAIIB Principles of Banking Module C News1508198767% (3)

- Bruno - Gomes Statement 2021 07Document4 pagesBruno - Gomes Statement 2021 07B gNo ratings yet

- Calculate EMV Cryptogram ARQC-ARPC For ISO8583 PaymentsDocument6 pagesCalculate EMV Cryptogram ARQC-ARPC For ISO8583 Paymentssajad salehiNo ratings yet

- Ach Code CardDocument2 pagesAch Code CardSankaetPathakNo ratings yet

- PH 9 HK 2 y 3 GGu 4 ZWLNDocument6 pagesPH 9 HK 2 y 3 GGu 4 ZWLNRanjit BeheraNo ratings yet

- Plastic Money Full ProjectDocument54 pagesPlastic Money Full ProjectNevil Surani76% (169)

- COMIN Egypt Launch Strategy-VFDocument45 pagesCOMIN Egypt Launch Strategy-VFSallam BakeerNo ratings yet

- Information On Payment Services Corporate 13.1.2018Document19 pagesInformation On Payment Services Corporate 13.1.2018Riciu IonutNo ratings yet

- Formato Recepcion UsdDocument1 pageFormato Recepcion UsdRicardo Villalón WNo ratings yet

- 279 Villas: Jalan Baik - Baik Nakula BaratDocument4 pages279 Villas: Jalan Baik - Baik Nakula BaratmarkNo ratings yet

- State Bank Collect Reprint Remittance Form Payment HistoryDocument1 pageState Bank Collect Reprint Remittance Form Payment HistoryBinayakSwainNo ratings yet

- Soal Siklus 2Document5 pagesSoal Siklus 2Darmadi0% (1)

- MrcInvoices November2022 272286Document1 pageMrcInvoices November2022 272286Saad AzmatNo ratings yet

- Chartered Accountant 2 0Document3 pagesChartered Accountant 2 0RkNo ratings yet

- 3-D Secure Vendor List v1 10-30-20181Document4 pages3-D Secure Vendor List v1 10-30-20181Mohamed LahlouNo ratings yet

- BOM Statement xxxxxxxx4898 20190401 20191009 20191009022924 PDFDocument14 pagesBOM Statement xxxxxxxx4898 20190401 20191009 20191009022924 PDFtrupti jadhavNo ratings yet

- Upi ProjectDocument26 pagesUpi Projectradheshyamsharma9953No ratings yet

- TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument4 pagesTXN Date Value Date Description Ref No./Cheque No. Debit Credit Balanceswetha_muthumulaNo ratings yet

- 7588 Ca 3891 C 0Document56 pages7588 Ca 3891 C 0luuuNo ratings yet