Download as xlsx, pdf, or txt

You might also like

- CFA 2024 Level II - SchweserNotes Book 2Document278 pagesCFA 2024 Level II - SchweserNotes Book 2roy772729No ratings yet

- Sol. Man. Chapter 4 Consol. Fs Part 1Document37 pagesSol. Man. Chapter 4 Consol. Fs Part 1itsmenatoy43% (7)

- Chapter 12Document17 pagesChapter 12jake doinog73% (11)

- Sheet at Acquisition: A. P.3-2. Allocation Schedule For Fair Value/book Value Differential and Consolidated BalanceDocument4 pagesSheet at Acquisition: A. P.3-2. Allocation Schedule For Fair Value/book Value Differential and Consolidated BalancePrince Frederic Mangambu100% (1)

- BCVR 5 Years (Company Accounting)Document13 pagesBCVR 5 Years (Company Accounting)celineNo ratings yet

- Summary Project Finance in Theory and PracticeDocument30 pagesSummary Project Finance in Theory and PracticeroseNo ratings yet

- Business Plan For Computer ConsultingDocument20 pagesBusiness Plan For Computer ConsultingjohnNo ratings yet

- Chapter 5 SolutionDocument47 pagesChapter 5 SolutionJay-PNo ratings yet

- Section-A Statement of Financial Position As at 31 Dec 2020 Non-Current AssetsDocument4 pagesSection-A Statement of Financial Position As at 31 Dec 2020 Non-Current AssetsFareeha RizwanNo ratings yet

- Preliminary ComputationsDocument3 pagesPreliminary ComputationsFarrell DmNo ratings yet

- Lecture 4 Exercises ANSWERS Home&StrawDocument3 pagesLecture 4 Exercises ANSWERS Home&StrawZiyodullo IsroilovNo ratings yet

- Tugas Chapter 5: Persentase Kepemilikan Pay Corporation 75%Document6 pagesTugas Chapter 5: Persentase Kepemilikan Pay Corporation 75%Iche IcheNo ratings yet

- Petra Answer 21221Document5 pagesPetra Answer 21221wedu nchiniNo ratings yet

- Tugas 10Document3 pagesTugas 10Reyhan ArioNo ratings yet

- Calculate The Following Ratios:: A) Roce B) Current RatioDocument9 pagesCalculate The Following Ratios:: A) Roce B) Current RatioPham TrangNo ratings yet

- Lab Pengantar AkuntansiDocument6 pagesLab Pengantar Akuntansirahadatul aishyNo ratings yet

- Anggita Awidiya 041911333129 AKL 1 Pertemuan 13Document4 pagesAnggita Awidiya 041911333129 AKL 1 Pertemuan 13anggitaawidiyaNo ratings yet

- Book Value of Stu (100%) : Pop Corporation and SubsidiaryDocument4 pagesBook Value of Stu (100%) : Pop Corporation and SubsidiaryKimberlyNo ratings yet

- Manual A2 FinalDocument43 pagesManual A2 FinalkazamNo ratings yet

- Chapter 4Document6 pagesChapter 4HelloWorldNowNo ratings yet

- Latihan IDocument8 pagesLatihan IPutri SariNo ratings yet

- Devia Febrina 43221110106 - Kuis 10 AKL 2Document4 pagesDevia Febrina 43221110106 - Kuis 10 AKL 2nara kimNo ratings yet

- HW C23 U Can Read But NoDocument2 pagesHW C23 U Can Read But NoLăng Quân VươngNo ratings yet

- Advanced Accounting 2 - Chapter 4 James B. Cantorne Problem 1. T/FDocument7 pagesAdvanced Accounting 2 - Chapter 4 James B. Cantorne Problem 1. T/FJames CantorneNo ratings yet

- Group FinancialDocument8 pagesGroup FinancialNever GonondoNo ratings yet

- Q1) May 2011 ZA Q1 - Ear, Mouth & Nose Mouth LTD Nose LTDDocument8 pagesQ1) May 2011 ZA Q1 - Ear, Mouth & Nose Mouth LTD Nose LTDduong duongNo ratings yet

- Bacc210 Assig 1Document6 pagesBacc210 Assig 1TarusengaNo ratings yet

- XLSXDocument10 pagesXLSXezar zacharyNo ratings yet

- Midlands State University: Faculty of Commerce Department of AccountingDocument5 pagesMidlands State University: Faculty of Commerce Department of AccountingIsheanesu MutusvaNo ratings yet

- Solution To Step AcquisitionDocument7 pagesSolution To Step AcquisitionshakilNo ratings yet

- (GL:5,000×90%), (YL:315×92%) : Page 1 of 8Document8 pages(GL:5,000×90%), (YL:315×92%) : Page 1 of 8Yasin ShaikhNo ratings yet

- Final PB Exam - Answers - SolutionsDocument10 pagesFinal PB Exam - Answers - SolutionsJazehl ValdezNo ratings yet

- AL Principles of Accounts: Suggested AnswerDocument14 pagesAL Principles of Accounts: Suggested AnswerElaine NgNo ratings yet

- Lets Try This 4Document2 pagesLets Try This 4syramaebillones26No ratings yet

- Sazkiya Aldina - Lat Soal AKL 1 Chapter 2Document3 pagesSazkiya Aldina - Lat Soal AKL 1 Chapter 2sazkiyaNo ratings yet

- Accounting IAS (Malaysia) Model Answers Series 2 2007 Old SyllabusDocument18 pagesAccounting IAS (Malaysia) Model Answers Series 2 2007 Old SyllabusAung Zaw HtweNo ratings yet

- Akl Soal 3 - Kelompok 2Document9 pagesAkl Soal 3 - Kelompok 2M KhairiNo ratings yet

- Akl Soal 3 Kelompok 2Document9 pagesAkl Soal 3 Kelompok 2dikaNo ratings yet

- Question 5: Ias 7 Statements of Cash FlowsDocument4 pagesQuestion 5: Ias 7 Statements of Cash FlowsShiza ArifNo ratings yet

- 2076 - Varias, Aizel Ann B - Module 2Document20 pages2076 - Varias, Aizel Ann B - Module 2Aizel Ann VariasNo ratings yet

- Financial Planning and Control AssignmentDocument3 pagesFinancial Planning and Control AssignmentnkwatalindiweNo ratings yet

- Seminar 09 Calculating NCInt Simple Example ColourDocument2 pagesSeminar 09 Calculating NCInt Simple Example Colour金鑫No ratings yet

- Malabanan - Activity Chapter 2 2 PDFDocument5 pagesMalabanan - Activity Chapter 2 2 PDFJv MalabananNo ratings yet

- FAR610 Consolidated Cashflow Past Semester FinalexamDocument18 pagesFAR610 Consolidated Cashflow Past Semester FinalexamANIS SYAKIRAH ADHWA MAHDILLAHNo ratings yet

- CH 10 Incomplete RecordsDocument27 pagesCH 10 Incomplete RecordsPawan Poynauth0% (1)

- Chapter 9 Financial Reporting in Hyperinflationary EconomiesDocument10 pagesChapter 9 Financial Reporting in Hyperinflationary EconomiesKathrina RoxasNo ratings yet

- M - 30 S 2020 o ($'000) ($'000) ADocument10 pagesM - 30 S 2020 o ($'000) ($'000) AAmmar TahirNo ratings yet

- Assigment Week 6 Laila Fitriana 12030120120020 DDocument17 pagesAssigment Week 6 Laila Fitriana 12030120120020 DLaila FitrianaNo ratings yet

- Akl Kelompok 4Document15 pagesAkl Kelompok 4Sry WahyuniNo ratings yet

- CHP 4Document16 pagesCHP 4Beenish JafriNo ratings yet

- Alfiani - QUIZ 1 IASDocument23 pagesAlfiani - QUIZ 1 IASWilda Sania MtNo ratings yet

- Chapter 4 AssignmentDocument2 pagesChapter 4 AssignmentJasmin MarreroNo ratings yet

- L7 Consolidation 3 Lecture SolutionsDocument6 pagesL7 Consolidation 3 Lecture SolutionsrohmasspamNo ratings yet

- No Items RM'000 Working (RM'000)Document4 pagesNo Items RM'000 Working (RM'000)Chushan TehNo ratings yet

- Abc FR263Document2 pagesAbc FR263Krishna 11No ratings yet

- Dec 2020Document17 pagesDec 2020Anjana TimalsinaNo ratings yet

- Fath Abdul Azis - A031211044Document6 pagesFath Abdul Azis - A031211044Fath Abdul AzisNo ratings yet

- 3jun24 - Intercompany Transaction - EquipmentDocument16 pages3jun24 - Intercompany Transaction - Equipmentsisilia rachelNo ratings yet

- Consolidation Q72Document5 pagesConsolidation Q72Fredben BenardNo ratings yet

- Statement of CFDocument1 pageStatement of CFnr1520122No ratings yet

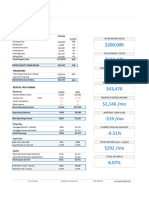

- Rental Investment ReportDocument5 pagesRental Investment ReportTuba TunaNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- May June 2018 (21) - QDocument20 pagesMay June 2018 (21) - QMarie Xavier - FelixNo ratings yet

- May June 2023 (22) - Q2 AnalysisDocument3 pagesMay June 2023 (22) - Q2 AnalysisMarie Xavier - FelixNo ratings yet

- Oct Nov 2023 (13) - QDocument12 pagesOct Nov 2023 (13) - QMarie Xavier - FelixNo ratings yet

- Limiting Factors - Q1 - June 2022Document1 pageLimiting Factors - Q1 - June 2022Marie Xavier - FelixNo ratings yet

- Cement CoDocument1 pageCement CoMarie Xavier - FelixNo ratings yet

- Frongoch CoDocument2 pagesFrongoch CoMarie Xavier - FelixNo ratings yet

- PYQ - Activity Based CostingDocument2 pagesPYQ - Activity Based CostingMarie Xavier - FelixNo ratings yet

- Sea Turtle Fact CardsDocument1 pageSea Turtle Fact CardsMarie Xavier - FelixNo ratings yet

- Balance Sheet: - Assets - Liabilities - Stockholder's EquityDocument11 pagesBalance Sheet: - Assets - Liabilities - Stockholder's EquitySASWAT MISHRANo ratings yet

- MEDINA - Homework 2 Nos. 8 & 9Document7 pagesMEDINA - Homework 2 Nos. 8 & 9Von Andrei MedinaNo ratings yet

- Financial Accounting and Reporting Iii Financial Accounting and Reporting Iii (Reviewer) (Reviewer)Document18 pagesFinancial Accounting and Reporting Iii Financial Accounting and Reporting Iii (Reviewer) (Reviewer)Jhaan Key Losita�oNo ratings yet

- MCQ Part 1Document41 pagesMCQ Part 1Santosh Shrestha100% (1)

- ACCT-UB 3 - Financial Statement Analysis Module 2 HomeworkDocument2 pagesACCT-UB 3 - Financial Statement Analysis Module 2 HomeworkpratheekNo ratings yet

- Financial Markets (Chapter 8)Document4 pagesFinancial Markets (Chapter 8)Kyla DayawonNo ratings yet

- This Study Resource Was: Module 1. Week 1 Statement of Financial PositionDocument8 pagesThis Study Resource Was: Module 1. Week 1 Statement of Financial PositionVhia Rashelle Galzote100% (1)

- An Accounting StandardDocument6 pagesAn Accounting StandardRAMOS ERLYN P.No ratings yet

- Ratio Analysis Based On Colgate Palmolive India LTDDocument3 pagesRatio Analysis Based On Colgate Palmolive India LTDwantANo ratings yet

- P1 - Corporate Reporting April 09Document21 pagesP1 - Corporate Reporting April 09IrfanNo ratings yet

- Annual Report 2010 - MCBDocument256 pagesAnnual Report 2010 - MCBkharalzNo ratings yet

- Fish 2018Document136 pagesFish 2018Anto KristianNo ratings yet

- 70259Document6 pages70259Mega Pop LockerNo ratings yet

- Module 5Document1 pageModule 5Margaveth P. BalbinNo ratings yet

- Corporations: Organization and Capital Stock Transactions: Weygandt - Kieso - KimmelDocument54 pagesCorporations: Organization and Capital Stock Transactions: Weygandt - Kieso - Kimmelkey aidanNo ratings yet

- Financial Analysis - Group Assignment - Group 9Document22 pagesFinancial Analysis - Group Assignment - Group 9Nguyen Quy Tran TranNo ratings yet

- Corporate Reporting Manual Part 2 - Up To 2018Document774 pagesCorporate Reporting Manual Part 2 - Up To 2018Masum GaziNo ratings yet

- Valuation Lecture I: WACC vs. APV and Capital Structure DecisionsDocument14 pagesValuation Lecture I: WACC vs. APV and Capital Structure DecisionsJuan Manuel VeronNo ratings yet

- APLI - Annual Report - 2017 PDFDocument156 pagesAPLI - Annual Report - 2017 PDFMichelle Hartasya SitompulNo ratings yet

- ACCT2020 Introduction To Accounting For Non-Business Majors Chapter 1Document15 pagesACCT2020 Introduction To Accounting For Non-Business Majors Chapter 1H20-spoutNo ratings yet

- Irctc IpoDocument8 pagesIrctc IpoAbhishek PadhyeNo ratings yet

- BankingDocument47 pagesBankingDeepansh GoyalNo ratings yet

- Accounting For Amalgamation (As Per As-14)Document9 pagesAccounting For Amalgamation (As Per As-14)Gs AbhilashNo ratings yet

- Praposal For ReportDocument18 pagesPraposal For ReportBadri maurya100% (1)

- Fa Msu PDFDocument254 pagesFa Msu PDFSelvakumar Thangaraj100% (1)