Amendment File - CA Final Audit - Green Edition

Amendment File - CA Final Audit - Green Edition

You might also like

- SFM Question Bank by Ajay Agarwal @mission - CA - FinalDocument569 pagesSFM Question Bank by Ajay Agarwal @mission - CA - Finalsrk100% (1)

- HL - Pni - V1 - NTR - 3596132948944013913 - NTR - 7818877607244788448 - 11Document2 pagesHL - Pni - V1 - NTR - 3596132948944013913 - NTR - 7818877607244788448 - 11KanakaReddyKannaNo ratings yet

- Quasem Industries Limited - Annual Report 2019Document122 pagesQuasem Industries Limited - Annual Report 2019JayedNo ratings yet

- Busines Plan-Juice StopDocument41 pagesBusines Plan-Juice StopShareef ChampNo ratings yet

- Chopra Scm5 Tif Ch13Document23 pagesChopra Scm5 Tif Ch13Madyoka RaimbekNo ratings yet

- Legal Action, Rescue and Rehabilitation of Bonded Labour Suresh Musahar and His SonDocument3 pagesLegal Action, Rescue and Rehabilitation of Bonded Labour Suresh Musahar and His Sonpvchr.india9214No ratings yet

- Final List Update PDFDocument44 pagesFinal List Update PDFKaushal TiwariNo ratings yet

- AccuraCap PMSDocument35 pagesAccuraCap PMSAnkur100% (1)

- F Susandra Dan M YusufDocument16 pagesF Susandra Dan M Yusufannisa rahmah niamiNo ratings yet

- Helpdesk 101115Document6 pagesHelpdesk 101115Muhammed Sabeeh100% (1)

- Revising The Bank Secrecy Act To Protect Privacy and Deter CriminalsDocument28 pagesRevising The Bank Secrecy Act To Protect Privacy and Deter CriminalsCato InstituteNo ratings yet

- Case Study RenalDocument29 pagesCase Study RenalZURAINI BT HARON (ILKKMKUBANGKERIAN)No ratings yet

- ROCKanpurFinal 30082018Document98 pagesROCKanpurFinal 30082018Md Robin HossainNo ratings yet

- Bill To / Ship To:: Qty Gross Amount Discount Other Charges Taxable Amount CGST SGST/ Ugst Igst Cess Total AmountDocument1 pageBill To / Ship To:: Qty Gross Amount Discount Other Charges Taxable Amount CGST SGST/ Ugst Igst Cess Total AmountMohit SachdevNo ratings yet

- Monthly Billing Statement: Ma Katherine Dela Cruz PantojaDocument4 pagesMonthly Billing Statement: Ma Katherine Dela Cruz Pantojamaria katherine pantojaNo ratings yet

- Even 11Document31 pagesEven 11jeet pereraNo ratings yet

- Odd 3Document4 pagesOdd 3jeet rogerNo ratings yet

- Ministry of Corporate Affairs - MCA Services PDFDocument2 pagesMinistry of Corporate Affairs - MCA Services PDFwork placeNo ratings yet

- PS Shifting ClaimsDocument7 pagesPS Shifting ClaimsPurnima SinghNo ratings yet

- Company Act, 2013-1 PDFDocument101 pagesCompany Act, 2013-1 PDFAakash JohnsNo ratings yet

- AIA VisaMasterAutoDebit (13-07-21)Document3 pagesAIA VisaMasterAutoDebit (13-07-21)K.Juslly ElisNo ratings yet

- List of FPOs in The State of BiharDocument2 pagesList of FPOs in The State of Biharanon_493704527100% (2)

- Leave-Rules For Rajasthan Government EmployeesDocument120 pagesLeave-Rules For Rajasthan Government EmployeesSatyajeet SinghNo ratings yet

- The New India Assurance Co. Ltd. (Government of India Undertaking)Document3 pagesThe New India Assurance Co. Ltd. (Government of India Undertaking)sarath potnuriNo ratings yet

- International Covid-19 Vaccination Certificate: Sertifikat Vaksinasi Covid-19 InternasionalDocument1 pageInternational Covid-19 Vaccination Certificate: Sertifikat Vaksinasi Covid-19 InternasionalIko MargaretaNo ratings yet

- Undertaking From The Borrower On End Use of FundsDocument2 pagesUndertaking From The Borrower On End Use of Fundsmadhukar sahayNo ratings yet

- Trustpilot Transparency Report 2022Document26 pagesTrustpilot Transparency Report 2022Rian Abdurr100% (1)

- Bhagalpur Lions Club - Lions E-Clubhouse1Document2 pagesBhagalpur Lions Club - Lions E-Clubhouse1rapscallionxxxNo ratings yet

- Cfma 016 Dt. 23.11.22 To MCXCCL BoardDocument6 pagesCfma 016 Dt. 23.11.22 To MCXCCL BoardPGurusNo ratings yet

- Auction Properties - PDF 30-09-2023Document246 pagesAuction Properties - PDF 30-09-2023Raj ANo ratings yet

- Shipping & Billing Address: Tanya Rai: Date: 14/12/2022Document2 pagesShipping & Billing Address: Tanya Rai: Date: 14/12/2022Tanya RaiNo ratings yet

- Eunice CV 2 UpdateDocument1 pageEunice CV 2 UpdateEunice YeboahNo ratings yet

- Ba (Hons) International Business and Finance: Research Methodology Research ProposalDocument20 pagesBa (Hons) International Business and Finance: Research Methodology Research ProposalTharindu WeerasingheNo ratings yet

- Fruit Roll Ups - Google SearchDocument1 pageFruit Roll Ups - Google Searchrona abrianaNo ratings yet

- Joshua Whitehead Garrity StatementDocument84 pagesJoshua Whitehead Garrity StatementThe Salt Lake TribuneNo ratings yet

- Extraction and Formulation of Perfume From Lemongrass LeavesDocument43 pagesExtraction and Formulation of Perfume From Lemongrass LeavesMartina StanNo ratings yet

- RFQ - 073-019-2021 - INTERSHIP SUPPLYDocument13 pagesRFQ - 073-019-2021 - INTERSHIP SUPPLYRICARDO FELIPE PAREDES ADOLFONo ratings yet

- BT 003196166 TicketDocument3 pagesBT 003196166 TicketSaragadam DilsriNo ratings yet

- PO 4600062173 SDBiosensorHealthcarePvtLtdDocument7 pagesPO 4600062173 SDBiosensorHealthcarePvtLtdChinna ThambiNo ratings yet

- CM20171017 08954 41228Document16 pagesCM20171017 08954 41228Azhari GunawanNo ratings yet

- TanzaniaDocument584 pagesTanzaniaSindy Elfas0% (1)

- GST On Goods Transport Services: CA Yashwant KasarDocument10 pagesGST On Goods Transport Services: CA Yashwant KasarPWD HIGHWAYNo ratings yet

- Paper 13 ICMA Mportant Qns - CA ShivangiDocument43 pagesPaper 13 ICMA Mportant Qns - CA Shivangisivarama marriNo ratings yet

- India Yog Kendra Directory PDFDocument210 pagesIndia Yog Kendra Directory PDFfvfdNo ratings yet

- Draw A Chart Showin Tax Structure in IndiaDocument55 pagesDraw A Chart Showin Tax Structure in IndiaShubh ShahNo ratings yet

- Case Study On Business Model Urban ClapDocument11 pagesCase Study On Business Model Urban Clapnithesh kumar jNo ratings yet

- Od122490077813150000 1 PDFDocument1 pageOd122490077813150000 1 PDFShashant NagwanshiNo ratings yet

- NC Price Verification Summary ReportDocument3 pagesNC Price Verification Summary ReportHank LeeNo ratings yet

- VISem BBA Core Income TaxDocument125 pagesVISem BBA Core Income TaxYELLOWTOOTHNo ratings yet

- RHP Ems LimitedDocument540 pagesRHP Ems LimitedMohammed Ameen SezanNo ratings yet

- List State Wise Nodal Officers NewDocument20 pagesList State Wise Nodal Officers NewSurbhi SonigraNo ratings yet

- MR 674694Document4 pagesMR 674694pandiyan pNo ratings yet

- Confirmation of Your Two Wheeler Policy atDocument2 pagesConfirmation of Your Two Wheeler Policy atShiwam KumarNo ratings yet

- HDFC Group Health Insurance - Claim ManualDocument6 pagesHDFC Group Health Insurance - Claim ManualNeir KrNo ratings yet

- Cash Transfers MHA GuidlinesDocument12 pagesCash Transfers MHA GuidlinesVignan KumarNo ratings yet

- Corporate GovernanceDocument22 pagesCorporate GovernanceBenita BijuNo ratings yet

- MediaRelease 11112022Document2 pagesMediaRelease 11112022maminder aroraNo ratings yet

- Annexure-II NAPS (Establishments in Haryana)Document618 pagesAnnexure-II NAPS (Establishments in Haryana)Mohit SainiNo ratings yet

- Chapter 1Document94 pagesChapter 1Narendran SrinivasanNo ratings yet

- International Business Class 6Document2 pagesInternational Business Class 6Luke FuquaNo ratings yet

- Project GuideDocument38 pagesProject Guide254No ratings yet

- W K Burton and Other On N CAbreraDocument60 pagesW K Burton and Other On N CAbreraBriseidaNo ratings yet

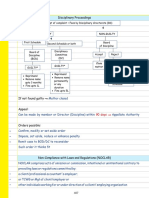

- Disciplinary Proceedings: Professional EthicsDocument3 pagesDisciplinary Proceedings: Professional EthicsDinesh MaheshwariNo ratings yet

- IND AS 41 - Board NotesDocument9 pagesIND AS 41 - Board NotessrkNo ratings yet

- IND AS 2 - Board NotesDocument7 pagesIND AS 2 - Board NotessrkNo ratings yet

- Goods & Services Tax (GST) - ServicesDocument4 pagesGoods & Services Tax (GST) - ServicessrkNo ratings yet

- G3 1 Index and ChecklistDocument123 pagesG3 1 Index and ChecklistWendy Al SyabanaNo ratings yet

- Hard Rock Café Location StrategyDocument3 pagesHard Rock Café Location Strategyfrankmarson100% (2)

- Alfamart Monitoring and TuningDocument11 pagesAlfamart Monitoring and TuningslimederellaNo ratings yet

- Strategic ManagementDocument23 pagesStrategic ManagementPavan Kumar DevarakondaNo ratings yet

- Code of Ethics GhellaDocument28 pagesCode of Ethics GhellaMassimilianoTerenziNo ratings yet

- Case Study & Marketing Strategies of Axis Bank: Tolani College of CommerceDocument56 pagesCase Study & Marketing Strategies of Axis Bank: Tolani College of Commerce2kd Termanito100% (1)

- AbsorptionDocument29 pagesAbsorptionRavi KatiyarNo ratings yet

- Export Finance ProjectDocument67 pagesExport Finance ProjectVinay Singh67% (3)

- Sole ProprietorshipDocument6 pagesSole ProprietorshipEron Roi Centina-gacutanNo ratings yet

- DPR FormatDocument4 pagesDPR Formatjasaulakh0% (1)

- Report On McdonaldsDocument21 pagesReport On McdonaldsMicheal WorthNo ratings yet

- The Winners and Losers of The Zero-Sum Game: The Origins of Trading Profits, Price Efficiency and Market LiquidityDocument34 pagesThe Winners and Losers of The Zero-Sum Game: The Origins of Trading Profits, Price Efficiency and Market LiquidityChiou Ying Chen100% (1)

- TCSDocument4 pagesTCSSarithaNo ratings yet

- Mercantile Law PDFDocument3 pagesMercantile Law PDFSmag SmagNo ratings yet

- Read Before Use: Thanks For DownloadingDocument15 pagesRead Before Use: Thanks For DownloadingARWA AlsofianiNo ratings yet

- SBR Text BookDocument889 pagesSBR Text BookRiaz Ibrahim100% (3)

- Slide RMK Chapter 1 - Kelompok 5 - Maksi 43CDocument15 pagesSlide RMK Chapter 1 - Kelompok 5 - Maksi 43CJali FusNo ratings yet

- HP t5000 Product Overview Jan07Document8 pagesHP t5000 Product Overview Jan07meharNo ratings yet

- Introduction To Max Newyork Life InsuranceDocument21 pagesIntroduction To Max Newyork Life Insurancedhruvpatel_bca2010No ratings yet

- Treatment of Assets Under Construction in SAP - From Creation To Settlement - SapGurusDocument14 pagesTreatment of Assets Under Construction in SAP - From Creation To Settlement - SapGurusAnanthakumar ANo ratings yet

- How To Do Basic Transactions On HCMIS FEDocument9 pagesHow To Do Basic Transactions On HCMIS FEGada GudetaNo ratings yet

- Comms: E3Comms Business English Course SyllabusDocument1 pageComms: E3Comms Business English Course SyllabusKinga NemethNo ratings yet

- SM - Distinctive CompetenciesDocument2 pagesSM - Distinctive CompetenciesVivek PimpleNo ratings yet

- Novi Zakon o Javnim Nabavkama, Engleski, Januar 2013Document113 pagesNovi Zakon o Javnim Nabavkama, Engleski, Januar 2013JelenaNo ratings yet

- Demat AccountDocument4 pagesDemat AccountNIHARIKA AGARWALNo ratings yet

- CHAPTER 9 Written ReportDocument17 pagesCHAPTER 9 Written ReportSharina Mhyca SamonteNo ratings yet

- 2012 MBA/IMBA Salary Survey: Career Development CentreDocument9 pages2012 MBA/IMBA Salary Survey: Career Development CentreLaura MontgomeryNo ratings yet

- FSGO Ethics ProjectDocument10 pagesFSGO Ethics ProjectShahbazNo ratings yet

Download as pdf or txt

You might also like

- SFM Question Bank by Ajay Agarwal @mission - CA - FinalDocument569 pagesSFM Question Bank by Ajay Agarwal @mission - CA - Finalsrk100% (1)

- HL - Pni - V1 - NTR - 3596132948944013913 - NTR - 7818877607244788448 - 11Document2 pagesHL - Pni - V1 - NTR - 3596132948944013913 - NTR - 7818877607244788448 - 11KanakaReddyKannaNo ratings yet

- Quasem Industries Limited - Annual Report 2019Document122 pagesQuasem Industries Limited - Annual Report 2019JayedNo ratings yet

- Busines Plan-Juice StopDocument41 pagesBusines Plan-Juice StopShareef ChampNo ratings yet

- Chopra Scm5 Tif Ch13Document23 pagesChopra Scm5 Tif Ch13Madyoka RaimbekNo ratings yet

- Legal Action, Rescue and Rehabilitation of Bonded Labour Suresh Musahar and His SonDocument3 pagesLegal Action, Rescue and Rehabilitation of Bonded Labour Suresh Musahar and His Sonpvchr.india9214No ratings yet

- Final List Update PDFDocument44 pagesFinal List Update PDFKaushal TiwariNo ratings yet

- AccuraCap PMSDocument35 pagesAccuraCap PMSAnkur100% (1)

- F Susandra Dan M YusufDocument16 pagesF Susandra Dan M Yusufannisa rahmah niamiNo ratings yet

- Helpdesk 101115Document6 pagesHelpdesk 101115Muhammed Sabeeh100% (1)

- Revising The Bank Secrecy Act To Protect Privacy and Deter CriminalsDocument28 pagesRevising The Bank Secrecy Act To Protect Privacy and Deter CriminalsCato InstituteNo ratings yet

- Case Study RenalDocument29 pagesCase Study RenalZURAINI BT HARON (ILKKMKUBANGKERIAN)No ratings yet

- ROCKanpurFinal 30082018Document98 pagesROCKanpurFinal 30082018Md Robin HossainNo ratings yet

- Bill To / Ship To:: Qty Gross Amount Discount Other Charges Taxable Amount CGST SGST/ Ugst Igst Cess Total AmountDocument1 pageBill To / Ship To:: Qty Gross Amount Discount Other Charges Taxable Amount CGST SGST/ Ugst Igst Cess Total AmountMohit SachdevNo ratings yet

- Monthly Billing Statement: Ma Katherine Dela Cruz PantojaDocument4 pagesMonthly Billing Statement: Ma Katherine Dela Cruz Pantojamaria katherine pantojaNo ratings yet

- Even 11Document31 pagesEven 11jeet pereraNo ratings yet

- Odd 3Document4 pagesOdd 3jeet rogerNo ratings yet

- Ministry of Corporate Affairs - MCA Services PDFDocument2 pagesMinistry of Corporate Affairs - MCA Services PDFwork placeNo ratings yet

- PS Shifting ClaimsDocument7 pagesPS Shifting ClaimsPurnima SinghNo ratings yet

- Company Act, 2013-1 PDFDocument101 pagesCompany Act, 2013-1 PDFAakash JohnsNo ratings yet

- AIA VisaMasterAutoDebit (13-07-21)Document3 pagesAIA VisaMasterAutoDebit (13-07-21)K.Juslly ElisNo ratings yet

- List of FPOs in The State of BiharDocument2 pagesList of FPOs in The State of Biharanon_493704527100% (2)

- Leave-Rules For Rajasthan Government EmployeesDocument120 pagesLeave-Rules For Rajasthan Government EmployeesSatyajeet SinghNo ratings yet

- The New India Assurance Co. Ltd. (Government of India Undertaking)Document3 pagesThe New India Assurance Co. Ltd. (Government of India Undertaking)sarath potnuriNo ratings yet

- International Covid-19 Vaccination Certificate: Sertifikat Vaksinasi Covid-19 InternasionalDocument1 pageInternational Covid-19 Vaccination Certificate: Sertifikat Vaksinasi Covid-19 InternasionalIko MargaretaNo ratings yet

- Undertaking From The Borrower On End Use of FundsDocument2 pagesUndertaking From The Borrower On End Use of Fundsmadhukar sahayNo ratings yet

- Trustpilot Transparency Report 2022Document26 pagesTrustpilot Transparency Report 2022Rian Abdurr100% (1)

- Bhagalpur Lions Club - Lions E-Clubhouse1Document2 pagesBhagalpur Lions Club - Lions E-Clubhouse1rapscallionxxxNo ratings yet

- Cfma 016 Dt. 23.11.22 To MCXCCL BoardDocument6 pagesCfma 016 Dt. 23.11.22 To MCXCCL BoardPGurusNo ratings yet

- Auction Properties - PDF 30-09-2023Document246 pagesAuction Properties - PDF 30-09-2023Raj ANo ratings yet

- Shipping & Billing Address: Tanya Rai: Date: 14/12/2022Document2 pagesShipping & Billing Address: Tanya Rai: Date: 14/12/2022Tanya RaiNo ratings yet

- Eunice CV 2 UpdateDocument1 pageEunice CV 2 UpdateEunice YeboahNo ratings yet

- Ba (Hons) International Business and Finance: Research Methodology Research ProposalDocument20 pagesBa (Hons) International Business and Finance: Research Methodology Research ProposalTharindu WeerasingheNo ratings yet

- Fruit Roll Ups - Google SearchDocument1 pageFruit Roll Ups - Google Searchrona abrianaNo ratings yet

- Joshua Whitehead Garrity StatementDocument84 pagesJoshua Whitehead Garrity StatementThe Salt Lake TribuneNo ratings yet

- Extraction and Formulation of Perfume From Lemongrass LeavesDocument43 pagesExtraction and Formulation of Perfume From Lemongrass LeavesMartina StanNo ratings yet

- RFQ - 073-019-2021 - INTERSHIP SUPPLYDocument13 pagesRFQ - 073-019-2021 - INTERSHIP SUPPLYRICARDO FELIPE PAREDES ADOLFONo ratings yet

- BT 003196166 TicketDocument3 pagesBT 003196166 TicketSaragadam DilsriNo ratings yet

- PO 4600062173 SDBiosensorHealthcarePvtLtdDocument7 pagesPO 4600062173 SDBiosensorHealthcarePvtLtdChinna ThambiNo ratings yet

- CM20171017 08954 41228Document16 pagesCM20171017 08954 41228Azhari GunawanNo ratings yet

- TanzaniaDocument584 pagesTanzaniaSindy Elfas0% (1)

- GST On Goods Transport Services: CA Yashwant KasarDocument10 pagesGST On Goods Transport Services: CA Yashwant KasarPWD HIGHWAYNo ratings yet

- Paper 13 ICMA Mportant Qns - CA ShivangiDocument43 pagesPaper 13 ICMA Mportant Qns - CA Shivangisivarama marriNo ratings yet

- India Yog Kendra Directory PDFDocument210 pagesIndia Yog Kendra Directory PDFfvfdNo ratings yet

- Draw A Chart Showin Tax Structure in IndiaDocument55 pagesDraw A Chart Showin Tax Structure in IndiaShubh ShahNo ratings yet

- Case Study On Business Model Urban ClapDocument11 pagesCase Study On Business Model Urban Clapnithesh kumar jNo ratings yet

- Od122490077813150000 1 PDFDocument1 pageOd122490077813150000 1 PDFShashant NagwanshiNo ratings yet

- NC Price Verification Summary ReportDocument3 pagesNC Price Verification Summary ReportHank LeeNo ratings yet

- VISem BBA Core Income TaxDocument125 pagesVISem BBA Core Income TaxYELLOWTOOTHNo ratings yet

- RHP Ems LimitedDocument540 pagesRHP Ems LimitedMohammed Ameen SezanNo ratings yet

- List State Wise Nodal Officers NewDocument20 pagesList State Wise Nodal Officers NewSurbhi SonigraNo ratings yet

- MR 674694Document4 pagesMR 674694pandiyan pNo ratings yet

- Confirmation of Your Two Wheeler Policy atDocument2 pagesConfirmation of Your Two Wheeler Policy atShiwam KumarNo ratings yet

- HDFC Group Health Insurance - Claim ManualDocument6 pagesHDFC Group Health Insurance - Claim ManualNeir KrNo ratings yet

- Cash Transfers MHA GuidlinesDocument12 pagesCash Transfers MHA GuidlinesVignan KumarNo ratings yet

- Corporate GovernanceDocument22 pagesCorporate GovernanceBenita BijuNo ratings yet

- MediaRelease 11112022Document2 pagesMediaRelease 11112022maminder aroraNo ratings yet

- Annexure-II NAPS (Establishments in Haryana)Document618 pagesAnnexure-II NAPS (Establishments in Haryana)Mohit SainiNo ratings yet

- Chapter 1Document94 pagesChapter 1Narendran SrinivasanNo ratings yet

- International Business Class 6Document2 pagesInternational Business Class 6Luke FuquaNo ratings yet

- Project GuideDocument38 pagesProject Guide254No ratings yet

- W K Burton and Other On N CAbreraDocument60 pagesW K Burton and Other On N CAbreraBriseidaNo ratings yet

- Disciplinary Proceedings: Professional EthicsDocument3 pagesDisciplinary Proceedings: Professional EthicsDinesh MaheshwariNo ratings yet

- IND AS 41 - Board NotesDocument9 pagesIND AS 41 - Board NotessrkNo ratings yet

- IND AS 2 - Board NotesDocument7 pagesIND AS 2 - Board NotessrkNo ratings yet

- Goods & Services Tax (GST) - ServicesDocument4 pagesGoods & Services Tax (GST) - ServicessrkNo ratings yet

- G3 1 Index and ChecklistDocument123 pagesG3 1 Index and ChecklistWendy Al SyabanaNo ratings yet

- Hard Rock Café Location StrategyDocument3 pagesHard Rock Café Location Strategyfrankmarson100% (2)

- Alfamart Monitoring and TuningDocument11 pagesAlfamart Monitoring and TuningslimederellaNo ratings yet

- Strategic ManagementDocument23 pagesStrategic ManagementPavan Kumar DevarakondaNo ratings yet

- Code of Ethics GhellaDocument28 pagesCode of Ethics GhellaMassimilianoTerenziNo ratings yet

- Case Study & Marketing Strategies of Axis Bank: Tolani College of CommerceDocument56 pagesCase Study & Marketing Strategies of Axis Bank: Tolani College of Commerce2kd Termanito100% (1)

- AbsorptionDocument29 pagesAbsorptionRavi KatiyarNo ratings yet

- Export Finance ProjectDocument67 pagesExport Finance ProjectVinay Singh67% (3)

- Sole ProprietorshipDocument6 pagesSole ProprietorshipEron Roi Centina-gacutanNo ratings yet

- DPR FormatDocument4 pagesDPR Formatjasaulakh0% (1)

- Report On McdonaldsDocument21 pagesReport On McdonaldsMicheal WorthNo ratings yet

- The Winners and Losers of The Zero-Sum Game: The Origins of Trading Profits, Price Efficiency and Market LiquidityDocument34 pagesThe Winners and Losers of The Zero-Sum Game: The Origins of Trading Profits, Price Efficiency and Market LiquidityChiou Ying Chen100% (1)

- TCSDocument4 pagesTCSSarithaNo ratings yet

- Mercantile Law PDFDocument3 pagesMercantile Law PDFSmag SmagNo ratings yet

- Read Before Use: Thanks For DownloadingDocument15 pagesRead Before Use: Thanks For DownloadingARWA AlsofianiNo ratings yet

- SBR Text BookDocument889 pagesSBR Text BookRiaz Ibrahim100% (3)

- Slide RMK Chapter 1 - Kelompok 5 - Maksi 43CDocument15 pagesSlide RMK Chapter 1 - Kelompok 5 - Maksi 43CJali FusNo ratings yet

- HP t5000 Product Overview Jan07Document8 pagesHP t5000 Product Overview Jan07meharNo ratings yet

- Introduction To Max Newyork Life InsuranceDocument21 pagesIntroduction To Max Newyork Life Insurancedhruvpatel_bca2010No ratings yet

- Treatment of Assets Under Construction in SAP - From Creation To Settlement - SapGurusDocument14 pagesTreatment of Assets Under Construction in SAP - From Creation To Settlement - SapGurusAnanthakumar ANo ratings yet

- How To Do Basic Transactions On HCMIS FEDocument9 pagesHow To Do Basic Transactions On HCMIS FEGada GudetaNo ratings yet

- Comms: E3Comms Business English Course SyllabusDocument1 pageComms: E3Comms Business English Course SyllabusKinga NemethNo ratings yet

- SM - Distinctive CompetenciesDocument2 pagesSM - Distinctive CompetenciesVivek PimpleNo ratings yet

- Novi Zakon o Javnim Nabavkama, Engleski, Januar 2013Document113 pagesNovi Zakon o Javnim Nabavkama, Engleski, Januar 2013JelenaNo ratings yet

- Demat AccountDocument4 pagesDemat AccountNIHARIKA AGARWALNo ratings yet

- CHAPTER 9 Written ReportDocument17 pagesCHAPTER 9 Written ReportSharina Mhyca SamonteNo ratings yet

- 2012 MBA/IMBA Salary Survey: Career Development CentreDocument9 pages2012 MBA/IMBA Salary Survey: Career Development CentreLaura MontgomeryNo ratings yet

- FSGO Ethics ProjectDocument10 pagesFSGO Ethics ProjectShahbazNo ratings yet