Download as pdf or txt

You might also like

- Donald J. Trump IndictmentDocument16 pagesDonald J. Trump IndictmentStefan Becket93% (27)

- Hoover Digest, 2023, No. 3, SummerDocument212 pagesHoover Digest, 2023, No. 3, SummerHoover InstitutionNo ratings yet

- DOD Sexual Assault 22 ReportDocument33 pagesDOD Sexual Assault 22 ReportAustin DeneanNo ratings yet

- Donald Trump Statement of FactDocument13 pagesDonald Trump Statement of FactSebastian M100% (4)

- TDS PDFDocument71 pagesTDS PDFJ.S. RATHOD67% (3)

- Senator Murray Budget Memo 1-24Document12 pagesSenator Murray Budget Memo 1-24Ezra Klein100% (1)

- 10 7 Baucus LetterDocument27 pages10 7 Baucus LetterBrian AhierNo ratings yet

- CBO - Congressional Budget Office - Analysis On Harry Reid Debt Ceiling Proposed Plan - July 27th 2011Document11 pagesCBO - Congressional Budget Office - Analysis On Harry Reid Debt Ceiling Proposed Plan - July 27th 2011Zim VicomNo ratings yet

- House Bill 4001Document7 pagesHouse Bill 4001Elizabeth WashingtonNo ratings yet

- White House Policy Statement: H.R. 3351Document5 pagesWhite House Policy Statement: H.R. 3351FedSmith Inc.No ratings yet

- FY 13 OMB JC Sequestration ReportDocument83 pagesFY 13 OMB JC Sequestration ReportCeleste KatzNo ratings yet

- 2010 Budget Perspective: The Real Deficit Effect of The Health BillDocument5 pages2010 Budget Perspective: The Real Deficit Effect of The Health BillWashington ExaminerNo ratings yet

- House Budget Control ActDocument9 pagesHouse Budget Control ActMichael Robert HusseyNo ratings yet

- Reg 114339Document35 pagesReg 114339Western CPENo ratings yet

- State Medicaid Director Letter Recovery Audit Contractors (RACs) For MedicaidDocument8 pagesState Medicaid Director Letter Recovery Audit Contractors (RACs) For MedicaidBeverly TranNo ratings yet

- OMB Sequestration Update Report To The President and Congress For Fiscal Year 2013 August 20, 2012Document22 pagesOMB Sequestration Update Report To The President and Congress For Fiscal Year 2013 August 20, 2012Peggy W SatterfieldNo ratings yet

- The Budget Control Act of 2011: The Effects On Spending and The Budget Deficit When The Automatic Spending Cuts Are ImplementedDocument19 pagesThe Budget Control Act of 2011: The Effects On Spending and The Budget Deficit When The Automatic Spending Cuts Are ImplementedcaseywootenNo ratings yet

- 2020 HB30 ReconvenedExecAmendHalfsheets 04112020Document159 pages2020 HB30 ReconvenedExecAmendHalfsheets 04112020Lowell FeldNo ratings yet

- Draft Hiring Incentives To Restore Employment (HIRE)Document4 pagesDraft Hiring Incentives To Restore Employment (HIRE)api-25909546No ratings yet

- CBO January 2015 Outlook On ObamacareDocument15 pagesCBO January 2015 Outlook On ObamacareZenger NewsNo ratings yet

- CBO Reid Letter HR3590Document28 pagesCBO Reid Letter HR3590clyde2400No ratings yet

- CBO Cost Estimate For H.R. 1628 Obamacare Repeal Reconciliation Act of 2017Document19 pagesCBO Cost Estimate For H.R. 1628 Obamacare Repeal Reconciliation Act of 2017CNBC.comNo ratings yet

- Congressional Budget Office U.S. Congress Washington, DC 20515Document17 pagesCongressional Budget Office U.S. Congress Washington, DC 20515api-26139761No ratings yet

- Sequestration and The Super Committee: Background On The Budget Control ActDocument4 pagesSequestration and The Super Committee: Background On The Budget Control Actwatton1217No ratings yet

- NEU Award Terms and ConditionsDocument5 pagesNEU Award Terms and ConditionsSomeonelse47No ratings yet

- CBO Score and Assessment To Repeal ObamacareDocument10 pagesCBO Score and Assessment To Repeal ObamacareDarla DawaldNo ratings yet

- Financial Assistance Agreement Tribal GovernmentsDocument5 pagesFinancial Assistance Agreement Tribal GovernmentsOneNationNo ratings yet

- City of Peterborough 2023 Draft Budget HighlightsDocument334 pagesCity of Peterborough 2023 Draft Budget HighlightsPeterborough ExaminerNo ratings yet

- Douglas W. Elmendorf, Director U.S. Congress Washington, DC 20515Document50 pagesDouglas W. Elmendorf, Director U.S. Congress Washington, DC 20515josephragoNo ratings yet

- Debt Limit Memo BanksDocument2 pagesDebt Limit Memo BanksFox NewsNo ratings yet

- A Critical Analysis of The Complexity Posed and Impact On Liquidation Process Due To The Rainbow Papers CaseDocument5 pagesA Critical Analysis of The Complexity Posed and Impact On Liquidation Process Due To The Rainbow Papers CaseHarsh kushwahaNo ratings yet

- Office of The Governor: Kim Reynolds Adam GreggDocument5 pagesOffice of The Governor: Kim Reynolds Adam GreggGazetteonlineNo ratings yet

- Budget Update August 2005Document6 pagesBudget Update August 2005Committee For a Responsible Federal BudgetNo ratings yet

- Peter R. Orszag, Director U.S. Congress Washington, DC 20515Document10 pagesPeter R. Orszag, Director U.S. Congress Washington, DC 20515Gordon NicolNo ratings yet

- CBO Canceling Debt Cost EstimateDocument5 pagesCBO Canceling Debt Cost EstimateAustin DeneanNo ratings yet

- COVID 3 - UI and Tax Title SummaryDocument10 pagesCOVID 3 - UI and Tax Title SummaryFox News84% (19)

- Budget Update March 142006Document10 pagesBudget Update March 142006Committee For a Responsible Federal BudgetNo ratings yet

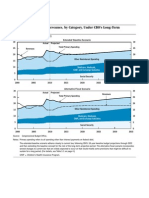

- Primary Spending and Revenues, by Category, Under CBO's Long-Term Budget ScenariosDocument25 pagesPrimary Spending and Revenues, by Category, Under CBO's Long-Term Budget ScenariosPeggy W SatterfieldNo ratings yet

- Issues Raised by Potential Sequestration Pursuant To Section 251A of Thebalanced Budget and Emergency Deficit Control Act of 1985Document2 pagesIssues Raised by Potential Sequestration Pursuant To Section 251A of Thebalanced Budget and Emergency Deficit Control Act of 1985Peggy W SatterfieldNo ratings yet

- LAWSDocument5 pagesLAWSZenez B. LabradorNo ratings yet

- Monetary 20200323 B 3Document2 pagesMonetary 20200323 B 3Michelle SeymourNo ratings yet

- Budget Control Act of 2011Document28 pagesBudget Control Act of 2011jediparalegalNo ratings yet

- FY 2023 Release GuidelinesDocument41 pagesFY 2023 Release GuidelinesTsuhaarukinguKaesuterouReyaizuNo ratings yet

- D66 Araullo-vs-Aquino-III-A-Case-DigestDocument4 pagesD66 Araullo-vs-Aquino-III-A-Case-DigestYash ManinNo ratings yet

- Crapo LTRDocument3 pagesCrapo LTRnchc-scribdNo ratings yet

- Congressional Budget Office: Douglas W. Elmendorf, Director U.S. Congress Washington, DC 20515Document25 pagesCongressional Budget Office: Douglas W. Elmendorf, Director U.S. Congress Washington, DC 20515Zim VicomNo ratings yet

- LFB Memo Asm Gop Covid ProposalsDocument23 pagesLFB Memo Asm Gop Covid ProposalsTMJ4 NewsNo ratings yet

- Bowsher v. Synar, 478 U.S. 714 (1986)Document61 pagesBowsher v. Synar, 478 U.S. 714 (1986)Scribd Government DocsNo ratings yet

- Senate Amendment 2137 To H.R. 3684, The Infrastructure Investment and Jobs Act, As Proposed On August 1, 2021Document19 pagesSenate Amendment 2137 To H.R. 3684, The Infrastructure Investment and Jobs Act, As Proposed On August 1, 2021Cynthia MoranNo ratings yet

- CBO Letter of 7/27/2011 On Revised Boehner PlanDocument10 pagesCBO Letter of 7/27/2011 On Revised Boehner PlanDoug MataconisNo ratings yet

- TD 9968Document86 pagesTD 9968Western CPENo ratings yet

- Summary of Graham-CassidyDocument12 pagesSummary of Graham-CassidyTPPFNo ratings yet

- Chapter 3 Govt AcctngDocument25 pagesChapter 3 Govt AcctngDez ZaNo ratings yet

- Legislative Fiscal Office Analysis of HB 1 Reengrossed (Updated 5/25/15)Document135 pagesLegislative Fiscal Office Analysis of HB 1 Reengrossed (Updated 5/25/15)RepNLandryNo ratings yet

- BSLFRF Compliance and Reporting GuidanceDocument50 pagesBSLFRF Compliance and Reporting GuidanceSomeonelse47No ratings yet

- Economic Impacts of Waiting To Resolve The Long Term Budget ImbalanceDocument12 pagesEconomic Impacts of Waiting To Resolve The Long Term Budget ImbalanceMilton RechtNo ratings yet

- Debt Ceiling FAQDocument9 pagesDebt Ceiling FAQNancy AmideiNo ratings yet

- Budget of the U.S. Government: A New Foundation for American Greatness: Fiscal Year 2018From EverandBudget of the U.S. Government: A New Foundation for American Greatness: Fiscal Year 2018No ratings yet

- Hidden Spending: The Politics of Federal Credit ProgramsFrom EverandHidden Spending: The Politics of Federal Credit ProgramsNo ratings yet

- The Debt Ceiling Dilemma: Balancing Act of Politics, Policy, and FinanceFrom EverandThe Debt Ceiling Dilemma: Balancing Act of Politics, Policy, and FinanceNo ratings yet

- Judge Rejects Trump's Effort To Recuse HerDocument20 pagesJudge Rejects Trump's Effort To Recuse HerKaelan DeeseNo ratings yet

- California Oil LawsuitDocument135 pagesCalifornia Oil LawsuitAustin DeneanNo ratings yet

- U.S. V Menendez Et Al IndictmentDocument39 pagesU.S. V Menendez Et Al IndictmentMichelle Rotuno-Johnson0% (1)

- Authors Guild OpenAI Class Action Complaint Sep 2023Document57 pagesAuthors Guild OpenAI Class Action Complaint Sep 2023Austin DeneanNo ratings yet

- 7.20.2023 - Letter To Ford - China Select Ways and MeansDocument5 pages7.20.2023 - Letter To Ford - China Select Ways and MeansBen OrnerNo ratings yet

- Biden Administration BriefDocument32 pagesBiden Administration BriefAustin DeneanNo ratings yet

- AM Radio For Every Vehicle ActDocument9 pagesAM Radio For Every Vehicle ActAustin DeneanNo ratings yet

- Judge Andrew Hanen DACA RulingDocument40 pagesJudge Andrew Hanen DACA RulingAustin DeneanNo ratings yet

- Department of Education V BrownDocument19 pagesDepartment of Education V BrownAustin DeneanNo ratings yet

- Trump Defense Motion To DelayDocument12 pagesTrump Defense Motion To DelayAustin DeneanNo ratings yet

- Biden v. NebraskaDocument77 pagesBiden v. NebraskaAustin DeneanNo ratings yet

- 2023 Willow MDP Record of DecisionDocument124 pages2023 Willow MDP Record of DecisionAustin DeneanNo ratings yet

- April Beige BookDocument32 pagesApril Beige BookAustin DeneanNo ratings yet

- IRS Free File ReportDocument106 pagesIRS Free File ReportAustin DeneanNo ratings yet

- National Task Force On The COVID-19 Pandemic ActDocument20 pagesNational Task Force On The COVID-19 Pandemic ActAustin DeneanNo ratings yet

- Fiscal Responsibility ActDocument99 pagesFiscal Responsibility ActRyan KingNo ratings yet

- Failed Bank Executives ActDocument4 pagesFailed Bank Executives ActAustin DeneanNo ratings yet

- TikTok V MontanaDocument62 pagesTikTok V MontanaAustin DeneanNo ratings yet

- FDIC Reform OptionsDocument17 pagesFDIC Reform OptionsAustin DeneanNo ratings yet

- Biden 2023 Annual ExamDocument5 pagesBiden 2023 Annual ExamAustin DeneanNo ratings yet

- IRS Strategic Operation PlanDocument150 pagesIRS Strategic Operation PlanAustin DeneanNo ratings yet

- Sore Loser Laws StudyDocument12 pagesSore Loser Laws StudyAustin DeneanNo ratings yet

- Americans For ProsperityDocument3 pagesAmericans For ProsperityAustin DeneanNo ratings yet

- UI Claims Nov. 23Document9 pagesUI Claims Nov. 23Austin DeneanNo ratings yet

- FHA Insurance Premium DropDocument4 pagesFHA Insurance Premium DropAustin DeneanNo ratings yet

- 22A444Document42 pages22A444Chris GeidnerNo ratings yet

- NTIA Mobile Apps ReportDocument50 pagesNTIA Mobile Apps ReportAustin DeneanNo ratings yet

- 12 Accountancy Notes CH05 Retirement and Death of A Partner 01Document15 pages12 Accountancy Notes CH05 Retirement and Death of A Partner 01Kaustubh Urfa Amol ParanjapeNo ratings yet

- Week 2 Homework (Chap. 4) - PostedDocument4 pagesWeek 2 Homework (Chap. 4) - PostedMs. Nina100% (5)

- Importance of Hiring A Licensed HandymanDocument2 pagesImportance of Hiring A Licensed Handymanhuda fatimaNo ratings yet

- Internship Report of PLIDocument12 pagesInternship Report of PLIAhmad AliNo ratings yet

- Budgeting and Budgetary ControlDocument2 pagesBudgeting and Budgetary ControlpalkeeNo ratings yet

- SwitchDocument2 pagesSwitchvasuNo ratings yet

- Reducing Irs PenaltiesDocument37 pagesReducing Irs PenaltiesMcKenzieLaw100% (1)

- Đề thi CK ESP111 TACN1 SAMPLEDocument4 pagesĐề thi CK ESP111 TACN1 SAMPLENguyễn Trần Như HuyềnNo ratings yet

- Chapter 3...Document10 pagesChapter 3...hakseng lyNo ratings yet

- Card Account Number: Statement Date: 5342 7312 3017 6006 Payment Due Date: Minimum Amount Due: Credit Limit: Available LimitDocument1 pageCard Account Number: Statement Date: 5342 7312 3017 6006 Payment Due Date: Minimum Amount Due: Credit Limit: Available LimitNuruzzaman BiplobNo ratings yet

- 31 C.F.R. 363.06, .11, .20, .22, .27 (2017 - 08 - 31 22 - 03 - 00 Utc)Document15 pages31 C.F.R. 363.06, .11, .20, .22, .27 (2017 - 08 - 31 22 - 03 - 00 Utc)Ghetto Vader100% (1)

- Persistent Creativity: Peter CampbellDocument300 pagesPersistent Creativity: Peter CampbellViona ShafiyahNo ratings yet

- State Level Bankers' Committee For UT of Puducherry Phone: 0413 233 0288 Fax: 0413 233 0217Document13 pagesState Level Bankers' Committee For UT of Puducherry Phone: 0413 233 0288 Fax: 0413 233 0217gautambhut0% (1)

- EPBDocument74 pagesEPBskn092No ratings yet

- Level of Knowledge: Objective:: Syllabus: International Business - Laws and PracticesDocument6 pagesLevel of Knowledge: Objective:: Syllabus: International Business - Laws and PracticesAna Carmela DomingoNo ratings yet

- Sponsorship Proposal TemplateDocument6 pagesSponsorship Proposal TemplateMike100% (1)

- Objective of DisinvestmentDocument9 pagesObjective of Disinvestmentsaketms009No ratings yet

- NSE ProjectDocument24 pagesNSE ProjectRonnie KapoorNo ratings yet

- Aman IcfaiDocument14 pagesAman IcfaiDanish IrshadNo ratings yet

- Community Profile Assignment RevisedDocument4 pagesCommunity Profile Assignment RevisedKing EbenGhNo ratings yet

- 5 Types of Budgets For BusinessesDocument2 pages5 Types of Budgets For BusinessesJohh Paul GarlitosNo ratings yet

- Proposal Ride To Himalaya Gunadi English RevisedDocument13 pagesProposal Ride To Himalaya Gunadi English RevisedarisyiNo ratings yet

- Chapter 5 - (22) (1) - 220310 - 003215Document115 pagesChapter 5 - (22) (1) - 220310 - 003215Celine Clemence胡嘉欣No ratings yet

- 2020 OWS InfographicsDocument1 page2020 OWS InfographicsElisha PaloNo ratings yet

- 2011 Ifadc Participants ListDocument31 pages2011 Ifadc Participants ListFazila KhanNo ratings yet

- Securities and Exchange Commission (SEC) - Formsb-1Document7 pagesSecurities and Exchange Commission (SEC) - Formsb-1highfinanceNo ratings yet

- Consumer AnalysisDocument2 pagesConsumer AnalysisammarNo ratings yet

- 2 Ndquiz 1 To 22 LecrepeatingignoreDocument19 pages2 Ndquiz 1 To 22 LecrepeatingignoreKhurramSadiqNo ratings yet