Download as docx, pdf, or txt

You might also like

- GO2Bank Template 2Document5 pagesGO2Bank Template 2jeffery lamar0% (2)

- Mutual Fund SEBI RegulationDocument17 pagesMutual Fund SEBI RegulationSarvesh ShuklaNo ratings yet

- DEEMED INCOMES (Aggregation of Income)Document3 pagesDEEMED INCOMES (Aggregation of Income)Dr. Mustafa KozhikkalNo ratings yet

- Assignmnt IIDocument6 pagesAssignmnt IIJeremy RemlalfakaNo ratings yet

- Taxguru - In-Tax Treatment of Cash Credit Us 68 69 69A 69B 69C and 69DDocument4 pagesTaxguru - In-Tax Treatment of Cash Credit Us 68 69 69A 69B 69C and 69DIshanNo ratings yet

- Deemed IncomeDocument3 pagesDeemed IncomeDhruv LawaniyaNo ratings yet

- Income Tax Department On Cash CreditDocument8 pagesIncome Tax Department On Cash CreditkalravNo ratings yet

- 43 - Cash CreditDocument8 pages43 - Cash CreditakashNo ratings yet

- Deemed Income Under Income Tax Act, 1961.: Extended Definition of IncomeDocument5 pagesDeemed Income Under Income Tax Act, 1961.: Extended Definition of IncomeVaibhav GuptaNo ratings yet

- Eligibility For Bonus: Thirty Working DaysDocument17 pagesEligibility For Bonus: Thirty Working DaysAli AsgarNo ratings yet

- Provisions Related AuditDocument29 pagesProvisions Related AuditAsrul AstroNo ratings yet

- 1st Schedule (Part ABC)Document8 pages1st Schedule (Part ABC)Tareq ChowdhuryNo ratings yet

- Definitions of Important TermsDocument61 pagesDefinitions of Important TermsThangavelu SundareswaranNo ratings yet

- 3cd - Review1Document7 pages3cd - Review1prasanna jagtapNo ratings yet

- Assessment of Demonetisation Era by Ca. Pramod Shingte 1Document25 pagesAssessment of Demonetisation Era by Ca. Pramod Shingte 1pramodmurkya13No ratings yet

- The Payment of Bonus Act1965Document9 pagesThe Payment of Bonus Act1965nishi18guptaNo ratings yet

- The Payment of Bonus Act, 1956Document21 pagesThe Payment of Bonus Act, 1956Jasjot BindraNo ratings yet

- ESTATES AND TRUSTS As Per Tax Code Sec. 60-66Document3 pagesESTATES AND TRUSTS As Per Tax Code Sec. 60-662022107419No ratings yet

- Gratuity RulesDocument5 pagesGratuity RulesMuhammad AsifNo ratings yet

- TAX - IPCC Amendment For Nov, 2013 Attempt (Carocks - Wordpress.com)Document84 pagesTAX - IPCC Amendment For Nov, 2013 Attempt (Carocks - Wordpress.com)Dushyant SinghaniaNo ratings yet

- IPC Regulation 9, 11 and 15 DocumentationDocument4 pagesIPC Regulation 9, 11 and 15 Documentationdindi genilNo ratings yet

- The Payment of Bonus & Gratuity Act. Bonus Act-1965 & Gratuity Act-1972Document34 pagesThe Payment of Bonus & Gratuity Act. Bonus Act-1965 & Gratuity Act-1972Dhruti AthaNo ratings yet

- Tax Trail PDFDocument9 pagesTax Trail PDFVinay YerubandiNo ratings yet

- Week 3 - Income From SalariesDocument46 pagesWeek 3 - Income From SalariesAdarsh PandeyNo ratings yet

- DeductionsDocument42 pagesDeductionsNithya RajNo ratings yet

- Payment of Bonus Act 1965 EnglishDocument11 pagesPayment of Bonus Act 1965 EnglishsunilbasaiNo ratings yet

- ASSESSMENT OF VARIOUS ENTITIES - TaxDocument20 pagesASSESSMENT OF VARIOUS ENTITIES - TaxKhushi MultaniNo ratings yet

- The Payment of Bonus Act, 1965Document6 pagesThe Payment of Bonus Act, 1965Ravi GuptaNo ratings yet

- The Payment of Bonus ACT, 1965Document20 pagesThe Payment of Bonus ACT, 1965anandi_meenaNo ratings yet

- InvestmentagreementDocument5 pagesInvestmentagreementmsralamabadi93No ratings yet

- Tax QPDocument41 pagesTax QPchaitali yadavNo ratings yet

- Dr. P. Sree Sudha, Associate Professor, DsnluDocument47 pagesDr. P. Sree Sudha, Associate Professor, Dsnluammu arellaNo ratings yet

- 21 Defintions of Income TaxDocument6 pages21 Defintions of Income TaxCA Gourav JashnaniNo ratings yet

- Old - AOP - Complete Study PDFDocument8 pagesOld - AOP - Complete Study PDFSwathi JainNo ratings yet

- A18 Siddharth JainDocument46 pagesA18 Siddharth JainDhiraj YAdavNo ratings yet

- Bonus Act - 1965 - 1Document24 pagesBonus Act - 1965 - 1nawabrp100% (1)

- Payment of Bonus Act - Payment of Bonus Under The Payment of Bonus Act 1965Document3 pagesPayment of Bonus Act - Payment of Bonus Under The Payment of Bonus Act 1965hello everyoneNo ratings yet

- LLC Operating Agreement ContractDocument16 pagesLLC Operating Agreement ContractHoàng NamNo ratings yet

- Deemed Income 68,69,69A - EDITED FINALDocument8 pagesDeemed Income 68,69,69A - EDITED FINALajithsiNo ratings yet

- Unit 2Document20 pagesUnit 2Alok Arun MohapatraNo ratings yet

- EPF SchemeDocument4 pagesEPF SchemeSnigdha MazumdarNo ratings yet

- THE PAYMENT OF BONUS ACT, 1965 (Compatibility Mode)Document17 pagesTHE PAYMENT OF BONUS ACT, 1965 (Compatibility Mode)ronakNo ratings yet

- The First Schedule Part B Recognised Provident Funds (See Section 2 (52) )Document5 pagesThe First Schedule Part B Recognised Provident Funds (See Section 2 (52) )Zahir UddinNo ratings yet

- Comparative Matrix of Social Legislation in The PhilippinesDocument14 pagesComparative Matrix of Social Legislation in The PhilippinesHowie Malik100% (2)

- Section - 36Document5 pagesSection - 36adipawar2824No ratings yet

- Duties of An AuditorDocument4 pagesDuties of An AuditorAtul GuptaNo ratings yet

- DEED OF PARTNERSHIP - Deeds & DraftsDocument6 pagesDEED OF PARTNERSHIP - Deeds & DraftsPravesh SatraNo ratings yet

- Cash Credits LLB Notes Income Tax Act Gen Law CollegeDocument8 pagesCash Credits LLB Notes Income Tax Act Gen Law CollegeJohn WickNo ratings yet

- 40ADocument3 pages40Aashim1No ratings yet

- University Roll No.: L13/LLB/193064 Name of Exam: 3 Year L.L.B Semester: 6 Subject: Law of Taxation Paper: 4 Date of Exam: 16.06.22Document9 pagesUniversity Roll No.: L13/LLB/193064 Name of Exam: 3 Year L.L.B Semester: 6 Subject: Law of Taxation Paper: 4 Date of Exam: 16.06.22প্রি য়া ঙ্কাNo ratings yet

- FINALDocument14 pagesFINALveenagirishNo ratings yet

- Finance PolicyDocument8 pagesFinance PolicynayanavspNo ratings yet

- Pastor Chapters23 24Document47 pagesPastor Chapters23 24Rodken VallenteNo ratings yet

- Corporation NotesDocument10 pagesCorporation Notesmakichanzenin01No ratings yet

- Stock Market ListingDocument7 pagesStock Market ListingHarsh ShahNo ratings yet

- Sample Partnership AgreementDocument5 pagesSample Partnership AgreementATWIINE JAMESNo ratings yet

- Summary PASDocument7 pagesSummary PASRemie Rose BarcebalNo ratings yet

- The Payment of Bonus Act, 1965 - 6178761 - 2023 - 02 - 01 - 23 - 59Document11 pagesThe Payment of Bonus Act, 1965 - 6178761 - 2023 - 02 - 01 - 23 - 59chiranjeevkumar19No ratings yet

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- The Handbook for Reading and Preparing Proxy Statements: A Guide to the SEC Disclosure Rules for Executive and Director Compensation, 6th EditionFrom EverandThe Handbook for Reading and Preparing Proxy Statements: A Guide to the SEC Disclosure Rules for Executive and Director Compensation, 6th EditionNo ratings yet

- 1 Clubbing of Income NEWDocument8 pages1 Clubbing of Income NEWHarnoor SinghNo ratings yet

- 4&5 Deductions, Rebate & ReliefsDocument15 pages4&5 Deductions, Rebate & ReliefsHarnoor SinghNo ratings yet

- 3 Set Off & Carry Forward of LossesDocument8 pages3 Set Off & Carry Forward of LossesHarnoor SinghNo ratings yet

- MsmeDocument57 pagesMsmeHarnoor Singh100% (1)

- Certificate, Ack, DecDocument3 pagesCertificate, Ack, DecHarnoor SinghNo ratings yet

- Schedule of Charges 2023Document2 pagesSchedule of Charges 2023Shakeel AhmadNo ratings yet

- Icici Bank PF FormDocument2 pagesIcici Bank PF FormDeepika Punj90% (10)

- (Solved) Respond To The Following Question in Your Textbook C - 2-26 - Carl... - Course HeroDocument3 pages(Solved) Respond To The Following Question in Your Textbook C - 2-26 - Carl... - Course HeroJdkrkejNo ratings yet

- Us153 Exmeption Jan-Jun'2016 (F)Document8 pagesUs153 Exmeption Jan-Jun'2016 (F)Fakhar QureshiNo ratings yet

- Statement of Axis Account No:917010056046995 For The Period (From: 30-09-2021 To: 29-12-2021)Document9 pagesStatement of Axis Account No:917010056046995 For The Period (From: 30-09-2021 To: 29-12-2021)Divya satya Srinivas kondaNo ratings yet

- Taxation Quiz 2Document2 pagesTaxation Quiz 2jackie delos santosNo ratings yet

- Money Laundering ProcessDocument15 pagesMoney Laundering ProcesspadminiNo ratings yet

- Business 2257 Tutorial #2Document17 pagesBusiness 2257 Tutorial #2westernbebeNo ratings yet

- Value Added Tax: Commercial MathematicsDocument9 pagesValue Added Tax: Commercial MathematicsMridulNo ratings yet

- 82202BIR Form 1702-MXDocument9 pages82202BIR Form 1702-MXRen A EleponioNo ratings yet

- Acct Statement - XX2150 - 02022024Document3 pagesAcct Statement - XX2150 - 02022024Praveen SainiNo ratings yet

- Hoodies & Sweaters - NUDE PROJECTDocument1 pageHoodies & Sweaters - NUDE PROJECTMartina Carbonell TorderaNo ratings yet

- CTA 8703 (Hoya) - DividendsDocument33 pagesCTA 8703 (Hoya) - DividendsJerwin DaveNo ratings yet

- ING Banking vs. CIR (Digest)Document2 pagesING Banking vs. CIR (Digest)Theodore Dolar100% (1)

- Chair BillDocument1 pageChair BillRakesh S RNo ratings yet

- 15 - OECD Pillar 1 & 2 (Deloitte) PDFDocument7 pages15 - OECD Pillar 1 & 2 (Deloitte) PDFIan TehNo ratings yet

- Assignment 2 - InvoiceDocument2 pagesAssignment 2 - Invoiceapi-507638249No ratings yet

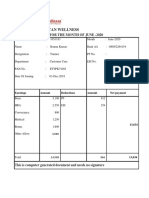

- Hindustan Wellness: Pay Slip For The Month of June - 2020Document3 pagesHindustan Wellness: Pay Slip For The Month of June - 2020ManishNo ratings yet

- Intercompany Charging Transactions TemplateDocument31 pagesIntercompany Charging Transactions TemplateNorberto CercadoNo ratings yet

- LT E-BillDocument2 pagesLT E-BillAbhijit GaikwadNo ratings yet

- House Bill 2526Document17 pagesHouse Bill 2526Kristofer PlonaNo ratings yet

- Billing Address: Tax InvoiceDocument1 pageBilling Address: Tax InvoiceShivani SinghNo ratings yet

- SGV & Co.: BIR RULING (DA-224-07)Document3 pagesSGV & Co.: BIR RULING (DA-224-07)cool_peachNo ratings yet

- KZ Edx ProDocument1 pageKZ Edx ProA KNo ratings yet

- Bill Overview: Jlb9Dkydwubgxfivcivc9Xcvxmvbc7Y Gcrkmmk5F9Pjivk9XsvfrvDocument5 pagesBill Overview: Jlb9Dkydwubgxfivcivc9Xcvxmvbc7Y Gcrkmmk5F9Pjivk9XsvfrvparamaguruNo ratings yet

- Ez Payment 2 UDocument12 pagesEz Payment 2 USophy Sufian SulaimanNo ratings yet

- Mercantile Law and TaxationDocument9 pagesMercantile Law and TaxationJoe SolimanNo ratings yet

- 20180918Document4 pages20180918Nor Fauzi IsmailNo ratings yet

- PNB Savings Smart Salary LoansDocument11 pagesPNB Savings Smart Salary LoanstinNo ratings yet