Download as pdf or txt

You might also like

- Eacffpc Customs Laws and Procedure Training ManualDocument146 pagesEacffpc Customs Laws and Procedure Training ManualKerretts Kimoikong89% (9)

- Economic CrisesDocument3 pagesEconomic Criseskanwal BalochNo ratings yet

- The Great Lockdown: Worst Economic Downturn Since The Great DepressionDocument5 pagesThe Great Lockdown: Worst Economic Downturn Since The Great DepressionMuhammad FadilNo ratings yet

- Current Economic Status and What It Means For The Future EconomyDocument4 pagesCurrent Economic Status and What It Means For The Future Economymuxie SSUSSNo ratings yet

- Srilankan CrisisDocument12 pagesSrilankan Crisisanchalc890No ratings yet

- ARI129-2009 Vashisht-Pathak Global Economic Crisis IndiaDocument6 pagesARI129-2009 Vashisht-Pathak Global Economic Crisis IndiaViral ChauhanNo ratings yet

- Policymakers Need Steady Hand As Storm Clouds Gather Over Global EconomyDocument11 pagesPolicymakers Need Steady Hand As Storm Clouds Gather Over Global EconomyNúriaNo ratings yet

- CFLCBrazil Impact of Western Public Finance in Least Developed CountriesDocument10 pagesCFLCBrazil Impact of Western Public Finance in Least Developed Countriescluadine dinerosNo ratings yet

- 2021-7 Cleary Progress and ImprovementDocument26 pages2021-7 Cleary Progress and ImprovementSean ClearyNo ratings yet

- Inflation in Pakistan and Its CausesDocument5 pagesInflation in Pakistan and Its CausesNaveed AhmedNo ratings yet

- The Pendamic and Global EconomicDocument8 pagesThe Pendamic and Global EconomicnahedNo ratings yet

- The Pandemic and The Global EconomyDocument8 pagesThe Pandemic and The Global EconomynahedNo ratings yet

- Impact of Credit Crisis in International BusinessDocument5 pagesImpact of Credit Crisis in International BusinessshebinaluvaNo ratings yet

- Connecting The Dots - The USA and Global RecessionsDocument2 pagesConnecting The Dots - The USA and Global RecessionsChinmay PanhaleNo ratings yet

- Coronavirus: Black Swan of Global Economy How It Impacts India?Document2 pagesCoronavirus: Black Swan of Global Economy How It Impacts India?Magnus ChaseNo ratings yet

- The Impact of Global Recession Over Our Economy Next YearDocument11 pagesThe Impact of Global Recession Over Our Economy Next Yearআশিকুর রহমানNo ratings yet

- Deuda de Los Paises en Desarrollo en El Tiempo de Covid-19 UNCADDocument16 pagesDeuda de Los Paises en Desarrollo en El Tiempo de Covid-19 UNCADCristianMilciadesNo ratings yet

- From The Great Lockdown To The Great Meltdown:: Developing Country Debt in The Time of Covid-19Document16 pagesFrom The Great Lockdown To The Great Meltdown:: Developing Country Debt in The Time of Covid-19Teymur DadashovNo ratings yet

- Informe de La UNCTADDocument16 pagesInforme de La UNCTADTélamNo ratings yet

- Informe de La UNCTADDocument16 pagesInforme de La UNCTADTélamNo ratings yet

- Trade Set To Plunge As COVID-19 Pandemic Upends Global EconomyDocument5 pagesTrade Set To Plunge As COVID-19 Pandemic Upends Global EconomySheena SandovalNo ratings yet

- Research Paper 4Document14 pagesResearch Paper 4Alishba AnjumNo ratings yet

- Essay - Global Economy Is at The Brink of CollapseDocument8 pagesEssay - Global Economy Is at The Brink of CollapsebilourNo ratings yet

- India's Growth Prospects Will Remain Strong, Even As World Economy Recovers Slowly, Says New World Bank ReportDocument14 pagesIndia's Growth Prospects Will Remain Strong, Even As World Economy Recovers Slowly, Says New World Bank ReportGaurav WilfredNo ratings yet

- Position PaperDocument4 pagesPosition PaperKyla MendozaNo ratings yet

- Gavas Pleeck Global TrendsDocument17 pagesGavas Pleeck Global Trendsewalied2800No ratings yet

- Why IMF Is Not An OptionDocument4 pagesWhy IMF Is Not An OptionatiswishNo ratings yet

- College of Social Science and HumanityDocument14 pagesCollege of Social Science and Humanitymuluken tewabeNo ratings yet

- FINANCINGFORDEVELOPMENTDocument16 pagesFINANCINGFORDEVELOPMENTRaheel AhmadNo ratings yet

- Impact of Global Financial Crisis On PakistanDocument16 pagesImpact of Global Financial Crisis On Pakistannaumanayubi93% (15)

- Sociology AssignmentDocument5 pagesSociology AssignmentKhalil KrNo ratings yet

- Motivation LetterDocument5 pagesMotivation LetterVlad ArmeanuNo ratings yet

- How The West Fell Out of Love With Economic Growth - The EconomistDocument8 pagesHow The West Fell Out of Love With Economic Growth - The EconomistDito InculoNo ratings yet

- Historical Overview of Pakistan - S Economy During The 1990sDocument10 pagesHistorical Overview of Pakistan - S Economy During The 1990sKhatri ZeenatNo ratings yet

- Project On Covid-19 UnemploymentDocument56 pagesProject On Covid-19 UnemploymentMUKESH MANWANINo ratings yet

- Effect of Covid-19 On World Economy: AssignmentDocument3 pagesEffect of Covid-19 On World Economy: AssignmentShubham PandeyNo ratings yet

- Term Paper: Debt Crisis in Pakistan Course: International Trade & FinanceDocument16 pagesTerm Paper: Debt Crisis in Pakistan Course: International Trade & FinanceKanza UsmanNo ratings yet

- Now The Brics Party Is Over, They Must Wind Down The State'S RoleDocument4 pagesNow The Brics Party Is Over, They Must Wind Down The State'S RoleGma BvbNo ratings yet

- Imf & World BankDocument20 pagesImf & World BankSohrab Ghafoor0% (2)

- Karachi:: GDP Growth DefinitionDocument4 pagesKarachi:: GDP Growth DefinitionVicky AullakhNo ratings yet

- Review Questions: 1. Cite Five (5) Major Issues of Economic Development in The World Today. A. Growing Income InequalityDocument7 pagesReview Questions: 1. Cite Five (5) Major Issues of Economic Development in The World Today. A. Growing Income InequalityRozaine Arevalo ReyesNo ratings yet

- Financial CrisisDocument11 pagesFinancial CrisisBlake MirandaNo ratings yet

- Assignment-01: Name: Sheraz Ahmed Roll No: 20021554-048 Submitted To: Sir AhsanDocument11 pagesAssignment-01: Name: Sheraz Ahmed Roll No: 20021554-048 Submitted To: Sir AhsanAhsanNo ratings yet

- Why China Is Facing An Economic Crisis and How India Can GainDocument3 pagesWhy China Is Facing An Economic Crisis and How India Can GainHarsh GhaiNo ratings yet

- UN WESP 2021 - Executive SummaryDocument11 pagesUN WESP 2021 - Executive SummaryC MiNo ratings yet

- ProjectDocument21 pagesProjectshaikhsfamily18No ratings yet

- The Global Dimensions of Development PDFDocument20 pagesThe Global Dimensions of Development PDFaisahNo ratings yet

- BTI 2018 VietnamDocument39 pagesBTI 2018 VietnamGabriell Acuña AlarcónNo ratings yet

- Int PR Models and Lessons Learnt For Vn-EngDocument14 pagesInt PR Models and Lessons Learnt For Vn-EngFaisalNo ratings yet

- Debt Super CycleDocument3 pagesDebt Super Cycleocean8724No ratings yet

- Five Year Economic PlanDocument7 pagesFive Year Economic PlanFarukh KianiNo ratings yet

- The Current Economic Crisis in Pakistan - Paradigm ShiftDocument9 pagesThe Current Economic Crisis in Pakistan - Paradigm ShiftSaqibullahNo ratings yet

- English Project Răducu Elena Nicole CSIE Grupa 1024Document9 pagesEnglish Project Răducu Elena Nicole CSIE Grupa 1024ile 06No ratings yet

- 19.04.08, Dawn - Com-Much Worse To Come PDFDocument2 pages19.04.08, Dawn - Com-Much Worse To Come PDFsindurationNo ratings yet

- Safiullah Sir AssDocument6 pagesSafiullah Sir AssAvijit SahaNo ratings yet

- Preprints202105 0399 v1Document4 pagesPreprints202105 0399 v1Nur AlamNo ratings yet

- Economic Challenges and OpportunitiesDocument3 pagesEconomic Challenges and OpportunitiesAsif Khan ShinwariNo ratings yet

- Vishal Manish M (123PS01629) - IMG CommentryDocument7 pagesVishal Manish M (123PS01629) - IMG Commentryamsavalli.vfNo ratings yet

- Budget Repair - NewspaperDocument3 pagesBudget Repair - NewspaperCSS AspirantsNo ratings yet

- Budget 2023-24 - The IMF Factor - Part IIDocument3 pagesBudget 2023-24 - The IMF Factor - Part IICSS AspirantsNo ratings yet

- Esential KnowledgeDocument1 pageEsential KnowledgeCSS AspirantsNo ratings yet

- Css Recommended Books ListDocument4 pagesCss Recommended Books ListCSS AspirantsNo ratings yet

- Facts and FigureDocument1 pageFacts and FigureCSS AspirantsNo ratings yet

- Daily Study ScheduleDocument1 pageDaily Study ScheduleCSS AspirantsNo ratings yet

- Chapter Two (Ayodola)Document28 pagesChapter Two (Ayodola)sitespirit96No ratings yet

- Crude Oil Price Trends in Global MarketDocument28 pagesCrude Oil Price Trends in Global MarketRITESH MADRECHA100% (1)

- C03 Krugman 12e AccessibleDocument92 pagesC03 Krugman 12e Accessiblesong neeNo ratings yet

- ĐỀ TA TĂNG CƯỜNG 9 (ĐÊ 1)Document7 pagesĐỀ TA TĂNG CƯỜNG 9 (ĐÊ 1)Nguyễn Lê Phương ThúyNo ratings yet

- DHL and Shopee Partnership CaseletDocument5 pagesDHL and Shopee Partnership Caseletchristian merreraNo ratings yet

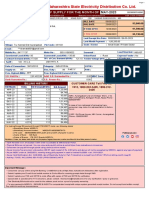

- Bill 670 502039075170 202305Document5 pagesBill 670 502039075170 202305pravin ghatgeNo ratings yet

- My Most Precious Investing Lessons - Series 2Document19 pagesMy Most Precious Investing Lessons - Series 2Mangesh kNo ratings yet

- Export IncentivesDocument14 pagesExport IncentivesDhananjana Joshi100% (1)

- The Legal Nature of WTO Obligations and The Consequences of Their ViolationDocument20 pagesThe Legal Nature of WTO Obligations and The Consequences of Their Violationrohan hebbalNo ratings yet

- Export-Import Management PDFDocument1 pageExport-Import Management PDFNidhi BahotNo ratings yet

- AP #: 1900135531 Request For Payment: 2020-0169733: Status: TransmitDocument1 pageAP #: 1900135531 Request For Payment: 2020-0169733: Status: TransmitIlove music096No ratings yet

- Time Value - ADocument22 pagesTime Value - ANAVNIT CHOUDHARYNo ratings yet

- Scartafaccio 2017 Marzo 1,2,3,4 - DerDocument165 pagesScartafaccio 2017 Marzo 1,2,3,4 - DerdertoninoNo ratings yet

- L4 - The Great Indian DemonetizationDocument20 pagesL4 - The Great Indian DemonetizationGOWRISHANKAR SNo ratings yet

- Buyers Info - PadpaoDocument32 pagesBuyers Info - PadpaoJonas RevañoNo ratings yet

- Financial Fitness Report: Nishant ChauhanDocument7 pagesFinancial Fitness Report: Nishant ChauhanNishantNo ratings yet

- Time Value of Money Problem and Solution 5Document4 pagesTime Value of Money Problem and Solution 5Vonreev OntoyNo ratings yet

- B. Com 5 Sem Advance Financial Accounting 1Document9 pagesB. Com 5 Sem Advance Financial Accounting 1AlankritaNo ratings yet

- Lembar Jawaban 1-JURNALDocument9 pagesLembar Jawaban 1-JURNALClara Shinta OceeNo ratings yet

- NI Act Cheque, Endorsement, CrossingDocument6 pagesNI Act Cheque, Endorsement, CrossingJAS 0313No ratings yet

- IFRS 15 (Solutions)Document18 pagesIFRS 15 (Solutions)adeelkacaNo ratings yet

- Assignment On "An Overview of International Business" (Chapter-1)Document24 pagesAssignment On "An Overview of International Business" (Chapter-1)Lutfur RahmanNo ratings yet

- Kuwait Traders (Export and Import Lists)Document14 pagesKuwait Traders (Export and Import Lists)gobudas3No ratings yet

- Macro EconomicsDocument63 pagesMacro EconomicsShimpi BeraNo ratings yet

- Synsea Shipping & Logistics Pte LTD: OriginalDocument1 pageSynsea Shipping & Logistics Pte LTD: OriginalOskar SimanjuntakNo ratings yet

- Commodit Y Market: M.archana, 2 MBADocument11 pagesCommodit Y Market: M.archana, 2 MBAAchu PappuNo ratings yet

- Hard Copy Books andDocument103 pagesHard Copy Books andLEWOYE BANTIE100% (1)

- MRTP Act, 1969 (Updated)Document4 pagesMRTP Act, 1969 (Updated)Jeeten PatelNo ratings yet

- Merchandising Lecture MRFDDocument59 pagesMerchandising Lecture MRFDMaria Louella MagadaNo ratings yet