Download as pdf or txt

You might also like

- Foreclosure Injunction TroDocument16 pagesForeclosure Injunction TroRon Houchins100% (1)

- Chapter 10: Mortgage Markets and DerivativesDocument6 pagesChapter 10: Mortgage Markets and DerivativesRemar22No ratings yet

- FinQuiz - Smart Summary - Study Session 16 - Reading 56Document7 pagesFinQuiz - Smart Summary - Study Session 16 - Reading 56Rafael100% (1)

- Engineering Economics - SolutionsDocument11 pagesEngineering Economics - SolutionsIssacus Youssouf100% (1)

- Banco Filipino PPT PresentationDocument20 pagesBanco Filipino PPT PresentationKirsten Ann de AsisNo ratings yet

- Beyond AffordabilityDocument20 pagesBeyond AffordabilityUri FontNo ratings yet

- Mortgage Loans: Fixed Income SecuritiesDocument9 pagesMortgage Loans: Fixed Income SecuritiesMonika SutharNo ratings yet

- Chapter 09 PresentationDocument26 pagesChapter 09 PresentationMega_ImranNo ratings yet

- Mortgage MarketDocument3 pagesMortgage MarketnishioyukihimeNo ratings yet

- MortgagepptDocument28 pagesMortgagepptJocelynNo ratings yet

- Chapter 10 - SummaryDocument4 pagesChapter 10 - SummaryjsgiganteNo ratings yet

- Types and Structure of Debt InstrumentsDocument37 pagesTypes and Structure of Debt InstrumentssanjitaNo ratings yet

- Financial Crises of 2007Document26 pagesFinancial Crises of 2007mmsweet911No ratings yet

- Bond Market, Bond Valuation and Risk: CH 7, 8 and Some Additional Materials Part ADocument19 pagesBond Market, Bond Valuation and Risk: CH 7, 8 and Some Additional Materials Part AMD AshrafulNo ratings yet

- Financialmarket Chap5 Mortgage MarketDocument30 pagesFinancialmarket Chap5 Mortgage Marketphamthao7404No ratings yet

- BondsDocument10 pagesBondsGeorge William100% (1)

- What Is A Treasury BondDocument12 pagesWhat Is A Treasury Bondmorris yenenehNo ratings yet

- Chapter 14 The Mortgage MarketsDocument5 pagesChapter 14 The Mortgage Marketslasha Kachkachishvili100% (1)

- Asset Securitization, CDOsDocument23 pagesAsset Securitization, CDOsJAINAM JAINNo ratings yet

- Test FactorsDocument4 pagesTest FactorsHafizullah AnsariNo ratings yet

- First Slide Mortgage Market Second Slide Mortgage MarketDocument6 pagesFirst Slide Mortgage Market Second Slide Mortgage MarketArlene GarciaNo ratings yet

- Chapter 23Document24 pagesChapter 23Abdur RehmanNo ratings yet

- Assignment 1 Medium and Long Term FinancingDocument12 pagesAssignment 1 Medium and Long Term FinancingMohit SahajpalNo ratings yet

- MortgageDocument6 pagesMortgageMohin ChowdhuryNo ratings yet

- Assignment 13 - Mortgage MarketDocument2 pagesAssignment 13 - Mortgage MarketJea Ann CariñozaNo ratings yet

- Bfc3240 Wk4 5 NotesDocument1 pageBfc3240 Wk4 5 NotesAparna RavindranNo ratings yet

- Bond MarketDocument35 pagesBond MarketBhupendra MoreNo ratings yet

- The Secondary Mortgage Market For Real Estate Loans: Lecture MapDocument28 pagesThe Secondary Mortgage Market For Real Estate Loans: Lecture MapGerard DGNo ratings yet

- Chapter 6 Medium and Long Term Financing: Ibm I-G2 International Trade Finance BU1243-G2Document13 pagesChapter 6 Medium and Long Term Financing: Ibm I-G2 International Trade Finance BU1243-G2Mohit SahajpalNo ratings yet

- Equity and DebtDocument4 pagesEquity and DebtpriyaNo ratings yet

- Assignment No. 4 Roll No. L-1184 Financial Institution Topic: Bond Market, Stock Market and Mortgage Market Submitted To: Sir Abdul Qadeer Submitted By: Zainab Shabbir Dated: 21 June, 2020Document16 pagesAssignment No. 4 Roll No. L-1184 Financial Institution Topic: Bond Market, Stock Market and Mortgage Market Submitted To: Sir Abdul Qadeer Submitted By: Zainab Shabbir Dated: 21 June, 2020Faisal NaqviNo ratings yet

- CFA Level 1 FundamentalsDocument5 pagesCFA Level 1 Fundamentalskazimeister1No ratings yet

- Fixed Income Securities: A Beginner's Guide to Understand, Invest and Evaluate Fixed Income Securities: Investment series, #2From EverandFixed Income Securities: A Beginner's Guide to Understand, Invest and Evaluate Fixed Income Securities: Investment series, #2No ratings yet

- Madura Chapter 9-2 PDFDocument40 pagesMadura Chapter 9-2 PDFMahmoud AbdullahNo ratings yet

- Are Securities That Promise To Make Fixed Payments According ToDocument26 pagesAre Securities That Promise To Make Fixed Payments According Toaddisyawkal18No ratings yet

- Chapter 09 (Financial Institute and Market)Document33 pagesChapter 09 (Financial Institute and Market)Mega_ImranNo ratings yet

- Chapter 10 NOTES 2021Document8 pagesChapter 10 NOTES 2021giannimizrahi5No ratings yet

- Credit RiskDocument9 pagesCredit RiskArfan AliNo ratings yet

- HandoutsDocument9 pagesHandoutsdianarosesarsalejo19No ratings yet

- Residential Mortgage Backed SecuritiesDocument4 pagesResidential Mortgage Backed SecuritiesSwapnil ParabNo ratings yet

- Sub PrimeDocument7 pagesSub PrimeAtul SuranaNo ratings yet

- Lecture Note 10 - Mortgage and Mortgage-Backed SecuritiesDocument58 pagesLecture Note 10 - Mortgage and Mortgage-Backed Securitiesben tenNo ratings yet

- Group 6: by - Garvit Agarwal Gyan Prakash Karan Gupta Ravikumar Soni Sahil SinglaDocument21 pagesGroup 6: by - Garvit Agarwal Gyan Prakash Karan Gupta Ravikumar Soni Sahil SinglaSahil SinglaNo ratings yet

- Financial Markets and Institution: The Bond MarketDocument44 pagesFinancial Markets and Institution: The Bond MarketDavid LeowNo ratings yet

- NotesDocument4 pagesNotesLune NoireNo ratings yet

- LM01 Fixed-Income Instrument Features IFT NotesDocument8 pagesLM01 Fixed-Income Instrument Features IFT NotesClaptrapjackNo ratings yet

- 2 - Debt and CovenantsDocument4 pages2 - Debt and CovenantsVincenzo CassoneNo ratings yet

- Mortgages LatestDocument79 pagesMortgages LatestRohit SingrodiaNo ratings yet

- FMI7 ch07Document38 pagesFMI7 ch07Farzana_SohelyNo ratings yet

- Financial Market &intrestrateDocument34 pagesFinancial Market &intrestrateaksid1No ratings yet

- Syndicated LoanDocument27 pagesSyndicated LoanTaanzim JhumuNo ratings yet

- Financial Markets (Chapter 10)Document3 pagesFinancial Markets (Chapter 10)Kyla Dayawon100% (1)

- Adjustable Rate MortgageDocument17 pagesAdjustable Rate MortgageMuhammad TamimNo ratings yet

- Minimum Attractive Rate of Return (MARR)Document31 pagesMinimum Attractive Rate of Return (MARR)AdiNo ratings yet

- Real Estate TermsDocument7 pagesReal Estate TermsTope MedelNo ratings yet

- Corporate Banking: Funded Services Lending /advances CB-CHPP07Document40 pagesCorporate Banking: Funded Services Lending /advances CB-CHPP07Prakash SharmaNo ratings yet

- Bond MarketDocument22 pagesBond MarketSumonaminur100% (1)

- Short Term Fund Flow: Chapter 06: Money MarketDocument4 pagesShort Term Fund Flow: Chapter 06: Money MarketMuhammad Hamza ZahidNo ratings yet

- Determinants of Interest RatesDocument66 pagesDeterminants of Interest RateskarylledigoNo ratings yet

- Chapter 3Document25 pagesChapter 3Fahad JavaidNo ratings yet

- Unit-4: What Is Cross-Border Financing?Document7 pagesUnit-4: What Is Cross-Border Financing?vansham malikNo ratings yet

- Week 5 Tutorial QuestionsDocument2 pagesWeek 5 Tutorial QuestionsWOP INVESTNo ratings yet

- FINA 3780 Chapter 7Document49 pagesFINA 3780 Chapter 7roBinNo ratings yet

- 2SLSDocument14 pages2SLSMuhibbuddin NoorNo ratings yet

- Sesi 11 - FI-D & ABSDocument37 pagesSesi 11 - FI-D & ABSMuhibbuddin NoorNo ratings yet

- Sesi 13 FI-D & ABSDocument42 pagesSesi 13 FI-D & ABSMuhibbuddin NoorNo ratings yet

- Sesi 12 FI-D & ABSDocument23 pagesSesi 12 FI-D & ABSMuhibbuddin NoorNo ratings yet

- Sesi 8 - FI-D & ABSDocument57 pagesSesi 8 - FI-D & ABSMuhibbuddin NoorNo ratings yet

- Beta Portofolio Saham PCA Kel 4 - FinalDocument46 pagesBeta Portofolio Saham PCA Kel 4 - FinalMuhibbuddin NoorNo ratings yet

- Beta Portofolio Saham PCA Kel 4 - 121022Document63 pagesBeta Portofolio Saham PCA Kel 4 - 121022Muhibbuddin NoorNo ratings yet

- RCBC v. MarcopperDocument12 pagesRCBC v. MarcopperPrecious Grace Flores BoloniasNo ratings yet

- Purpose CodeDocument3 pagesPurpose CodeRavi KumarNo ratings yet

- Bcc:Br:104:404 20.11.2012 Circular To All Branches and Offices in IndiaDocument12 pagesBcc:Br:104:404 20.11.2012 Circular To All Branches and Offices in IndiaamilcarNo ratings yet

- AB Bank - 2022Document131 pagesAB Bank - 2022Mostafa Noman DeepNo ratings yet

- Acer India Private LimitedDocument18 pagesAcer India Private LimitedAjitesh AbhishekNo ratings yet

- Analysis of Financial Statements: DATE: January 05, 2021 Presented By: Mr. Florante P. de Leon, Mba, CB, CTTDocument59 pagesAnalysis of Financial Statements: DATE: January 05, 2021 Presented By: Mr. Florante P. de Leon, Mba, CB, CTTFlorante De LeonNo ratings yet

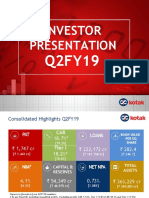

- Kotak - Q2FY19 Investor PresentationDocument37 pagesKotak - Q2FY19 Investor PresentationDivya MukherjeeNo ratings yet

- Chanakya National Law University: Topic-Pledge and Hypothecation Subject - Law of Contract IiDocument23 pagesChanakya National Law University: Topic-Pledge and Hypothecation Subject - Law of Contract IiashishNo ratings yet

- Case 5 Tata Steel's Acquisition of CorusDocument28 pagesCase 5 Tata Steel's Acquisition of Corusashmit100% (1)

- Loan Application FormDocument6 pagesLoan Application FormJohn Okong'oNo ratings yet

- The Wall Street Journal April 14 2017 PDFDocument43 pagesThe Wall Street Journal April 14 2017 PDFrakNo ratings yet

- Sample Board Res.Document2 pagesSample Board Res.Luis Angelo Tabasa100% (1)

- Most Important Terms and Conditions (Mitc) (For Individual Housing/ Non-Housing Loan)Document2 pagesMost Important Terms and Conditions (Mitc) (For Individual Housing/ Non-Housing Loan)Venkatesh W0% (1)

- China Daily - October 19, 2016Document25 pagesChina Daily - October 19, 2016nickhardNo ratings yet

- How Loans Work A Bankers Testimony TriStar 9.13 PDFDocument14 pagesHow Loans Work A Bankers Testimony TriStar 9.13 PDFTRISTARUSANo ratings yet

- Neera Products ProjectDocument39 pagesNeera Products ProjectTejas Kotwal100% (1)

- Video 1 - Priority Sector Lending Lyst5420Document37 pagesVideo 1 - Priority Sector Lending Lyst5420Sumit JanrodeNo ratings yet

- Solved An Analysis of The Transactions of Rutherford Company For The PDFDocument1 pageSolved An Analysis of The Transactions of Rutherford Company For The PDFAnbu jaromiaNo ratings yet

- MGT604 Quizes Mega FileDocument51 pagesMGT604 Quizes Mega FileAbdul Jabbar0% (1)

- Consumer FinanceDocument15 pagesConsumer Financechaudhary9267% (3)

- Chapter 8 - Roculas, SylviaDocument22 pagesChapter 8 - Roculas, SylviaAmbray Lynjoy100% (1)

- Proof of Claim 1Document3 pagesProof of Claim 1Greg Wilder100% (3)

- MF Cost of Capital - Practice QuestionsDocument4 pagesMF Cost of Capital - Practice QuestionsSaad UsmanNo ratings yet

- Final of Final Response To NBE's ExaminersDocument108 pagesFinal of Final Response To NBE's Examinersdaniel nugusieNo ratings yet

- A Case For A Single Loan Origination System For Core Banking Products PDFDocument5 pagesA Case For A Single Loan Origination System For Core Banking Products PDFansh_hcetNo ratings yet

- 1.cebu International V. Ca 316 SCRA 488Document9 pages1.cebu International V. Ca 316 SCRA 488Rhena SaranzaNo ratings yet