Download as xlsx, pdf, or txt

You might also like

- Solution Manual For Managerial Economics Business Strategy 9th Edition by Baye PDFDocument7 pagesSolution Manual For Managerial Economics Business Strategy 9th Edition by Baye PDFa55278073479% (34)

- Stravinsky Oedipus RexDocument131 pagesStravinsky Oedipus Rexkantee100% (16)

- Itunes Gifted Card Format-1Document1 pageItunes Gifted Card Format-1Mr Naijatim89% (282)

- Bond and NoteDocument22 pagesBond and NoteEyuel SintayehuNo ratings yet

- Share & Business Valuation Case Study Question and SolutionDocument6 pagesShare & Business Valuation Case Study Question and SolutionSarannyaRajendraNo ratings yet

- 26-06-2020 Financial Management Suggested AnswersDocument3 pages26-06-2020 Financial Management Suggested AnswersJEANNo ratings yet

- Paper - 2: Strategic Financial Management Questions Foreign Exchange Risk ManagementDocument30 pagesPaper - 2: Strategic Financial Management Questions Foreign Exchange Risk ManagementNirupa ChoppaNo ratings yet

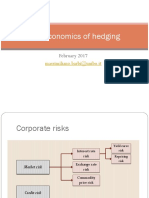

- Economics of Risk ManagementDocument29 pagesEconomics of Risk ManagementRoman RoscaNo ratings yet

- Lecture 3 - Interpreting Financial Statements + Seminar QuestionDocument10 pagesLecture 3 - Interpreting Financial Statements + Seminar QuestionMahad UzairNo ratings yet

- Bsc. Sem - Corporate Finance - Final Exam: Question 1Document4 pagesBsc. Sem - Corporate Finance - Final Exam: Question 1Derek LowNo ratings yet

- Memory Plus Gold For Mas5Document8 pagesMemory Plus Gold For Mas5Ashianna KimNo ratings yet

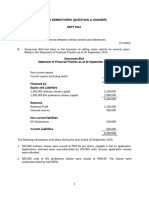

- Sept 2014 - 230716 - 233727Document22 pagesSept 2014 - 230716 - 233727mohddanialhanaffimustaffiNo ratings yet

- c38fn2 - Revision Handout (2018)Document6 pagesc38fn2 - Revision Handout (2018)Syaimma Syed AliNo ratings yet

- Same Questions - F303 - 1st MidDocument5 pagesSame Questions - F303 - 1st MidRafid Al Abid SpondonNo ratings yet

- BRS3B Assessment Opportunity 1 2019Document11 pagesBRS3B Assessment Opportunity 1 2019221103909No ratings yet

- FA II - Chapter 2 & 3 Part IIDocument21 pagesFA II - Chapter 2 & 3 Part IISitra AbduNo ratings yet

- FM 2019 SolutionsDocument6 pagesFM 2019 Solutionsaditikotere92No ratings yet

- 8b Tut Questions SolutionsDocument3 pages8b Tut Questions SolutionsMk SANo ratings yet

- AliyaDocument6 pagesAliyaaserbeyene29No ratings yet

- Cost AccountingDocument6 pagesCost AccountingDorianne BorgNo ratings yet

- Christ CIA FM MidtermDocument6 pagesChrist CIA FM MidtermKSHITIZ CHOUDHARYNo ratings yet

- Girum Tsega PerfectDocument13 pagesGirum Tsega PerfectMesi YE GINo ratings yet

- SFM Challenger SeriesDocument23 pagesSFM Challenger SeriesSagar singlaNo ratings yet

- SIP AmrutleelaDocument14 pagesSIP AmrutleelapremNo ratings yet

- Excercise 1 AnswersDocument3 pagesExcercise 1 AnswersfaisalNo ratings yet

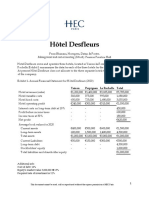

- S07 Desfelurs V3Document2 pagesS07 Desfelurs V3Khushi singhalNo ratings yet

- Tarea9 24octDocument8 pagesTarea9 24octAntia YañezNo ratings yet

- Sample OTsDocument5 pagesSample OTsVishnu ArvindNo ratings yet

- Case 13Document7 pagesCase 13Nguyễn Quốc TháiNo ratings yet

- Operating Exposure (Or Chapter 9)Document19 pagesOperating Exposure (Or Chapter 9)sindhupallavigundaNo ratings yet

- L5M4 Additional SlidesDocument7 pagesL5M4 Additional SlidesTlotlo RamotlhabiNo ratings yet

- Solution 1Document8 pagesSolution 1frq qqrNo ratings yet

- Working Notes Profit and Loss Adjustment AccountDocument11 pagesWorking Notes Profit and Loss Adjustment Accountkvrajan6No ratings yet

- MTP 1 Nov 18 QDocument6 pagesMTP 1 Nov 18 QSampath KumarNo ratings yet

- Osjdioahfnlk, MNLKJLDocument10 pagesOsjdioahfnlk, MNLKJLAlex NievaNo ratings yet

- AK for Chap 15Document12 pagesAK for Chap 15Diệu HuyềnNo ratings yet

- Bond valuationDocument56 pagesBond valuationHarsh pRAJAPATINo ratings yet

- Banks 03 SHAW ValuationDocument57 pagesBanks 03 SHAW Valuationmerag76668No ratings yet

- Parcor TrainingDocument12 pagesParcor TrainingKarl ExacNo ratings yet

- Cash and Credit ManagementDocument11 pagesCash and Credit Managementaoishic2025No ratings yet

- Calamba and Brillantes Problem-Obliga, Shaira MaeDocument3 pagesCalamba and Brillantes Problem-Obliga, Shaira MaeShaira Mae ObligaNo ratings yet

- Interpreting Fin StatementsDocument22 pagesInterpreting Fin StatementskamranNo ratings yet

- Sma Final Mock Exam 2Document5 pagesSma Final Mock Exam 2Lee NguyenNo ratings yet

- Bond Portfolio ManagementDocument58 pagesBond Portfolio ManagementHarshit DwivediNo ratings yet

- Practice Problems On Ratio AnalysisDocument6 pagesPractice Problems On Ratio AnalysisRahul SethiNo ratings yet

- Extra Material On CFDocument127 pagesExtra Material On CFPanosMavrNo ratings yet

- Chapter 11Document43 pagesChapter 11Rishu GargNo ratings yet

- Yogesh P Assignment PDFDocument2 pagesYogesh P Assignment PDFಯೋಗೇಶ್ ಪಿNo ratings yet

- ET Sample Questions - SolnDocument4 pagesET Sample Questions - SolnShivamNo ratings yet

- Esmeralda Springs SurpriseDocument8 pagesEsmeralda Springs Surpriseflorinmen1No ratings yet

- AnswersDocument34 pagesAnswerssathvik.g.m.s.saiNo ratings yet

- IA2 Chapter 9 ActivitiesDocument7 pagesIA2 Chapter 9 ActivitiesShaina TorraineNo ratings yet

- Topic 1 Revision of NPV & WACCDocument10 pagesTopic 1 Revision of NPV & WACCabdirahman farah AbdiNo ratings yet

- Chapter 6 Invetsment ExercisesDocument14 pagesChapter 6 Invetsment ExercisesAntonio Jose DuarteNo ratings yet

- Aug 2015 Question 4 - Topic 1: Introduction To FMGTDocument4 pagesAug 2015 Question 4 - Topic 1: Introduction To FMGTSharleen ZxzNo ratings yet

- Ut Sample Paper Ak G 12 AccDocument4 pagesUt Sample Paper Ak G 12 Accblackpink771170No ratings yet

- Finance&Accounts T3 SolutionDocument4 pagesFinance&Accounts T3 Solutionkanika thakurNo ratings yet

- Acc203 Tut On LiquidationDocument7 pagesAcc203 Tut On LiquidationShivanjani KumarNo ratings yet

- Intacc Chap 9Document26 pagesIntacc Chap 9Shek Severino AlairNo ratings yet

- Capital Budgeting SumsDocument14 pagesCapital Budgeting Sumssunny patwaNo ratings yet

- Diara Po.Document7 pagesDiara Po.Rio Cyrel CelleroNo ratings yet

- Queen Mary, University of London - Print GBP Payment PathwayDocument1 pageQueen Mary, University of London - Print GBP Payment PathwayShravan Deshmukh100% (1)

- ECOM104 - Applied Corporate Finance Problem Set 3 - Week 3Document3 pagesECOM104 - Applied Corporate Finance Problem Set 3 - Week 3Shravan DeshmukhNo ratings yet

- Problem Set - Week 4 - Blank - TemplateDocument5 pagesProblem Set - Week 4 - Blank - TemplateShravan DeshmukhNo ratings yet

- Problem Set Week 5 SolutionsDocument5 pagesProblem Set Week 5 SolutionsShravan DeshmukhNo ratings yet

- Practical Valuation - Problem Set Week 2 - Solutions - UpgradeDocument4 pagesPractical Valuation - Problem Set Week 2 - Solutions - UpgradeShravan DeshmukhNo ratings yet

- Practice - Problem Set - Week 4 SolutionsDocument3 pagesPractice - Problem Set - Week 4 SolutionsShravan DeshmukhNo ratings yet

- Problem Set - Week 2Document3 pagesProblem Set - Week 2Shravan DeshmukhNo ratings yet

- AssetManagement Problem Set Week 3 Blank TemplateDocument6 pagesAssetManagement Problem Set Week 3 Blank TemplateShravan DeshmukhNo ratings yet

- Chapter 1. Electronic Components & SignalsDocument12 pagesChapter 1. Electronic Components & SignalsPavankumar Gosavi100% (2)

- ISP Assignment REV 2019Document3 pagesISP Assignment REV 2019terranNo ratings yet

- 001Document2 pages001Adnan DizdarNo ratings yet

- Volvo B5TL: When All You Need Is Everything in A Double Deck BusDocument13 pagesVolvo B5TL: When All You Need Is Everything in A Double Deck BusКонстантин КосаревNo ratings yet

- Verified Component List Aama Certification Program: Part One Components of Certified Windows and DoorsDocument14 pagesVerified Component List Aama Certification Program: Part One Components of Certified Windows and Doorsjuan rodriguezNo ratings yet

- Activa Product ImprovementsDocument17 pagesActiva Product ImprovementsadityatfiNo ratings yet

- South Indian RecipesDocument7 pagesSouth Indian RecipesJagannath AcharyaNo ratings yet

- Air France vs. Carrascoso, 18 SCRA 155, No. L-21438 September 28, 1966Document5 pagesAir France vs. Carrascoso, 18 SCRA 155, No. L-21438 September 28, 1966Lyka Angelique CisnerosNo ratings yet

- FPEMDocument5 pagesFPEMJaya Chandra ReddyNo ratings yet

- Marki DuvanaDocument27 pagesMarki DuvanamijpedjapedjaNo ratings yet

- Lab 2 Group 2Document11 pagesLab 2 Group 2ianmansour100% (5)

- Ahsan's CVDocument2 pagesAhsan's CVAhsan DilshadNo ratings yet

- Somaliland Electoral Laws HandbookDocument0 pagesSomaliland Electoral Laws HandbookGaryaqaan Muuse YuusufNo ratings yet

- 2.2.5 Lab - Becoming A Defender - ILMDocument2 pages2.2.5 Lab - Becoming A Defender - ILMhazwanNo ratings yet

- Earth Charter and The Global ImpactDocument27 pagesEarth Charter and The Global ImpactDaisyNo ratings yet

- DR Niharika Maharshi Sharma ResumeDocument6 pagesDR Niharika Maharshi Sharma ResumeMSSPSNo ratings yet

- Principles of Organization & ManagementDocument6 pagesPrinciples of Organization & Managementsehj888No ratings yet

- FoodBalt 2017 Abstract BookDocument140 pagesFoodBalt 2017 Abstract BookEngr Muhammad IrfanNo ratings yet

- HDocument13 pagesHPrasoon PremrajNo ratings yet

- Kumar Sabnani Org CultureDocument2 pagesKumar Sabnani Org CultureAayushi SinghNo ratings yet

- Section Viii Div 1 Div 2 Div ComparisonDocument2 pagesSection Viii Div 1 Div 2 Div Comparisonapparaokr100% (5)

- Republic of The Philippines Department of Education Ugong Pasig National High SchoolDocument12 pagesRepublic of The Philippines Department of Education Ugong Pasig National High SchoolJOEL MONTERDENo ratings yet

- 12 Method of MilkingDocument5 pages12 Method of MilkingDr Maroof100% (2)

- DEVELOPMENT BANK OF RIZAL vs. SIMA WEIDocument2 pagesDEVELOPMENT BANK OF RIZAL vs. SIMA WEIelaine bercenioNo ratings yet

- Narrative Report On The Conduct of Joint BSP & GSP School Based Camp 2017Document3 pagesNarrative Report On The Conduct of Joint BSP & GSP School Based Camp 2017Archie De Los ArcosNo ratings yet

- Menstruation Disorders NotesDocument27 pagesMenstruation Disorders NotesemmaNo ratings yet

- Curriculum Vitae - SUDHIR GUDURIDocument8 pagesCurriculum Vitae - SUDHIR GUDURIsudhirguduruNo ratings yet

- Learning Disabilities Summary1Document11 pagesLearning Disabilities Summary1fordmayNo ratings yet