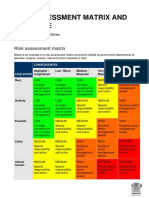

Risk Assesment by Program Area

Risk Assesment by Program Area

You might also like

- Google Cloud PlatforDocument6 pagesGoogle Cloud PlatforjohnNo ratings yet

- Ibm Openpages Operational Risk Mamagement Software SolutionDocument4 pagesIbm Openpages Operational Risk Mamagement Software SolutionJamil BellaghaNo ratings yet

- Alcatraz Analysis (With Explanations)Document16 pagesAlcatraz Analysis (With Explanations)Raul Dolo Quinones100% (1)

- Fleet Parts StorekeeperDocument2 pagesFleet Parts StorekeeperBright Edward NasamuNo ratings yet

- Protegrity HSM Connectivity and FunctionalityDocument250 pagesProtegrity HSM Connectivity and FunctionalitygheodanNo ratings yet

- Chatime Analysis Paper - Group 7Document17 pagesChatime Analysis Paper - Group 7Sunny50% (4)

- Baird - Euroland Foods CaseDocument5 pagesBaird - Euroland Foods CaseKyleNo ratings yet

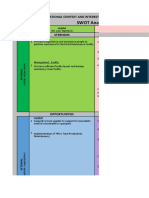

- SWOT Analysis: Organizational Context and Interested Parties Need & ExpectationDocument43 pagesSWOT Analysis: Organizational Context and Interested Parties Need & Expectationamril alrizaNo ratings yet

- Muhammad AliDocument1 pageMuhammad AliMariaJoaquinaCiezaGonzálezNo ratings yet

- General Auditing For IT Auditors PDFDocument4 pagesGeneral Auditing For IT Auditors PDFGerardo AraqueNo ratings yet

- Price Waterhouse Swift PDFDocument4 pagesPrice Waterhouse Swift PDFjairo lopezNo ratings yet

- Defect Management - Bug ReportDocument13 pagesDefect Management - Bug ReportalexNo ratings yet

- Profit Loss StatementDocument1 pageProfit Loss StatementhmarcalNo ratings yet

- EY in A Digital World Do You Know Where Your Risks Are Sa FinalDocument31 pagesEY in A Digital World Do You Know Where Your Risks Are Sa FinalMeet PanchalNo ratings yet

- Business Impact Analysis ExampleDocument4 pagesBusiness Impact Analysis ExampleArnel OlivarNo ratings yet

- Risk Management Policy - CorporateDocument18 pagesRisk Management Policy - CorporatemoinNo ratings yet

- Risk Assessment BackfilligDocument5 pagesRisk Assessment Backfilligmolobe mkhondoNo ratings yet

- KZ Deloitte Information Security Survey 2014 enDocument25 pagesKZ Deloitte Information Security Survey 2014 ensamuelNo ratings yet

- IT Internal Control Framework v7Document26 pagesIT Internal Control Framework v7biasilarissaNo ratings yet

- RA 001 Risk Analysis - Risk AssessementDocument2 pagesRA 001 Risk Analysis - Risk AssessementJoshua Guerrero CaloyongNo ratings yet

- PCS 7 Readme V8.1Document64 pagesPCS 7 Readme V8.1Chen CY100% (1)

- Strategic Risk Register PDF 1660418288Document25 pagesStrategic Risk Register PDF 1660418288mohamedNo ratings yet

- ITGC Assessment ExampleDocument7 pagesITGC Assessment ExampleETTORE JOHN DE VERANo ratings yet

- Enterprise Risk Matrix A3 PDFDocument1 pageEnterprise Risk Matrix A3 PDFDavid VelaNo ratings yet

- Payroll BrochureDocument16 pagesPayroll BrochureInfutureweb TechnologiesNo ratings yet

- DSC WATCH - Coast Stations Participating in MF, HF and VHF Watch-Keeping Using Digital Selective Calling TechniquesDocument5 pagesDSC WATCH - Coast Stations Participating in MF, HF and VHF Watch-Keeping Using Digital Selective Calling TechniquesmanojNo ratings yet

- SWIFT Customer Security ProgramDocument12 pagesSWIFT Customer Security Programco caNo ratings yet

- Systems Application and Products in Data ProcessingDocument22 pagesSystems Application and Products in Data ProcessingSanktifier100% (1)

- Audit Framework Under Information System and Cyber Security RegulationsDocument16 pagesAudit Framework Under Information System and Cyber Security Regulationsrishi_rajarshiNo ratings yet

- Sunera Best Practices For Remediating SoDsDocument7 pagesSunera Best Practices For Remediating SoDssura anil reddyNo ratings yet

- HITRUST Policies - Information Security Risk Management ProcedureDocument10 pagesHITRUST Policies - Information Security Risk Management Procedurealan dumsNo ratings yet

- Integration Access Control With Fiori Apps For S4HANA On-PremiseDocument5 pagesIntegration Access Control With Fiori Apps For S4HANA On-PremiseHasbleidy CelisNo ratings yet

- Internal Audit Dashboard Ver. 1Document18 pagesInternal Audit Dashboard Ver. 1Fazal KarimNo ratings yet

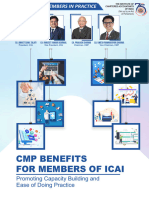

- List of Benefits For The Members of ICAIDocument39 pagesList of Benefits For The Members of ICAIcavishnukhandelwal100% (1)

- Scientific Research and Experimental Development (SR&ED) Expenditures ClaimDocument40 pagesScientific Research and Experimental Development (SR&ED) Expenditures ClaimmetroroadNo ratings yet

- 21 25 VPC Si Sys AdminDocument598 pages21 25 VPC Si Sys AdminNguyễn Lương QuyềnNo ratings yet

- Data Recovery PlanDocument11 pagesData Recovery PlanCream FamilyNo ratings yet

- CIS Microsoft SQL Server 2005 Benchmark v2.0.0Document166 pagesCIS Microsoft SQL Server 2005 Benchmark v2.0.0Oscar Javier Baquero SanchezNo ratings yet

- GRC Interview Q&ADocument22 pagesGRC Interview Q&Aishan royNo ratings yet

- Risk MGMTDocument51 pagesRisk MGMTJhanMarie Castillo-CamposanoNo ratings yet

- IC Agile Risk Register 9419Document4 pagesIC Agile Risk Register 9419senarathNo ratings yet

- Ransomware Self-Assessment Tool: OCTOBER 2020Document14 pagesRansomware Self-Assessment Tool: OCTOBER 2020AhmedAlHefnyNo ratings yet

- Auditing General and Application ControlsDocument13 pagesAuditing General and Application ControlschokriNo ratings yet

- ITT Provision of Web Hosting Services GMB DOM 57-09-21Document36 pagesITT Provision of Web Hosting Services GMB DOM 57-09-21Flexy BeatsNo ratings yet

- Cloud Controls Matrix Version 3.0: Control Domain Control Specification CCM V3.0 Control IDDocument363 pagesCloud Controls Matrix Version 3.0: Control Domain Control Specification CCM V3.0 Control IDmanishNo ratings yet

- Logistics Risk Assessment Tool TemplateDocument48 pagesLogistics Risk Assessment Tool TemplateSampurna SenNo ratings yet

- 2.325-Risk Assessment Procedure FinalDocument8 pages2.325-Risk Assessment Procedure Finalkirandevi1981No ratings yet

- PDF PPR 15 FiccaDocument44 pagesPDF PPR 15 FiccaPankaj GoyalNo ratings yet

- 1 Disaster Management Audit ReportDocument124 pages1 Disaster Management Audit ReportManan ChadhaNo ratings yet

- Windows and Linux Operating Systems From PDFDocument9 pagesWindows and Linux Operating Systems From PDFPAULA ANDREA PERALTA TRIANANo ratings yet

- Module 1 - What Is RiskDocument19 pagesModule 1 - What Is RiskKim Anh NguyenNo ratings yet

- Project Risk Management Lecture 1 (Printables)Document35 pagesProject Risk Management Lecture 1 (Printables)Muhammad AwaisNo ratings yet

- Itgc AssignmentDocument12 pagesItgc AssignmentSparshana KumariNo ratings yet

- Recordkeeping Risk Assessment MatrixDocument2 pagesRecordkeeping Risk Assessment MatrixEsteban OONo ratings yet

- Inventory Inventory IDR Control NoDocument23 pagesInventory Inventory IDR Control NoCA Rahul GuptaNo ratings yet

- Risk Management ProcessDocument40 pagesRisk Management ProcessAliAdnan AliAdnan100% (1)

- 03-05. - Sox y ITGC FrameworkDocument22 pages03-05. - Sox y ITGC FrameworkPedro PerezNo ratings yet

- RA 01 Risk Assessment FormDocument5 pagesRA 01 Risk Assessment FormAlfa RidziNo ratings yet

- Sample Risk and Issue LogsDocument29 pagesSample Risk and Issue LogsRhodora MaglinaoNo ratings yet

- Risk Analysis MemoDocument7 pagesRisk Analysis MemoAnonymous in4fhbdwkNo ratings yet

- Debt Interest Expense Substantive AnalyticalDocument2 pagesDebt Interest Expense Substantive AnalyticalErik RodriguesNo ratings yet

- AMLA Risk Assessment Methodology 28th February 2020Document26 pagesAMLA Risk Assessment Methodology 28th February 2020nishi nanavatiNo ratings yet

- Establish and Maintain WHS Management Systems: Submission DetailsDocument16 pagesEstablish and Maintain WHS Management Systems: Submission DetailsAndresPradaNo ratings yet

- MTN OFS Application Form EditableDocument1 pageMTN OFS Application Form Editablepeter sundayNo ratings yet

- BM ReviewDocument10 pagesBM ReviewFish SuperNo ratings yet

- Mid Term 2022 Company LawDocument4 pagesMid Term 2022 Company Lawpradeep ranaNo ratings yet

- No 5.1.fourth Generation Evalution Research (Qualitative Research Design)Document4 pagesNo 5.1.fourth Generation Evalution Research (Qualitative Research Design)Eko Wahyu ApriliantoNo ratings yet

- Negen Capital PMS Feb 22 FactsheetDocument5 pagesNegen Capital PMS Feb 22 Factsheetjeevan gangavarapuNo ratings yet

- Cash FlowsDocument26 pagesCash Flowsvickyprimus100% (1)

- Web Design RFP SampleDocument9 pagesWeb Design RFP Samplebarneygurl0% (1)

- PARTCOR NotesDocument19 pagesPARTCOR NotesKatrina PonceNo ratings yet

- Karina Market Structure SummaryDocument4 pagesKarina Market Structure SummaryKarina Permata SariNo ratings yet

- RM Lecture 04Document61 pagesRM Lecture 04vuduyducNo ratings yet

- SAP.C TS4CO 1909.v2020-05-21.q63Document16 pagesSAP.C TS4CO 1909.v2020-05-21.q63Vladimir Jovanovic0% (1)

- Print Media OKDocument23 pagesPrint Media OKEnchan Te TeNo ratings yet

- The Business Case For ASC 606 ComplianceDocument21 pagesThe Business Case For ASC 606 ComplianceSimplusNo ratings yet

- Patni Ar2009Document174 pagesPatni Ar2009chip_blueNo ratings yet

- Financial Analysis of A CompanyDocument10 pagesFinancial Analysis of A CompanyRupesh PuriNo ratings yet

- SCM SlidesDocument15 pagesSCM SlidesAmna NoorNo ratings yet

- Kajal Rai 24Document23 pagesKajal Rai 24KAJAL RAINo ratings yet

- MGT305 Ass1Document5 pagesMGT305 Ass1Trần Phước Diễm TrangNo ratings yet

- FINALDocument20 pagesFINALShubhangi BishnoiNo ratings yet

- Treatment of Assets Under Construction in SAP - From Creation To Settlement - SapGurusDocument14 pagesTreatment of Assets Under Construction in SAP - From Creation To Settlement - SapGurusAnanthakumar ANo ratings yet

- MM User ManualDocument316 pagesMM User ManualANILNo ratings yet

- Can Be Reproduced: Department of Justice Employees' Multi-Purpose CooperativeDocument3 pagesCan Be Reproduced: Department of Justice Employees' Multi-Purpose CooperativeSharlene338No ratings yet

- HRM Assignment - InfosysDocument4 pagesHRM Assignment - Infosyssumit SinghNo ratings yet

- Compare The Merits of The Entry Strategies Discussed in This ChapterDocument3 pagesCompare The Merits of The Entry Strategies Discussed in This ChapterVikram KumarNo ratings yet

- PneumaticDocument15 pagesPneumaticDesign ErNo ratings yet

- Statement of Single Largest Completed Contract BulbulDocument2 pagesStatement of Single Largest Completed Contract BulbulZeny BocadNo ratings yet

- Law 346Document2 pagesLaw 346Nuradilah BahardinNo ratings yet

Download as xlsx, pdf, or txt

You might also like

- Google Cloud PlatforDocument6 pagesGoogle Cloud PlatforjohnNo ratings yet

- Ibm Openpages Operational Risk Mamagement Software SolutionDocument4 pagesIbm Openpages Operational Risk Mamagement Software SolutionJamil BellaghaNo ratings yet

- Alcatraz Analysis (With Explanations)Document16 pagesAlcatraz Analysis (With Explanations)Raul Dolo Quinones100% (1)

- Fleet Parts StorekeeperDocument2 pagesFleet Parts StorekeeperBright Edward NasamuNo ratings yet

- Protegrity HSM Connectivity and FunctionalityDocument250 pagesProtegrity HSM Connectivity and FunctionalitygheodanNo ratings yet

- Chatime Analysis Paper - Group 7Document17 pagesChatime Analysis Paper - Group 7Sunny50% (4)

- Baird - Euroland Foods CaseDocument5 pagesBaird - Euroland Foods CaseKyleNo ratings yet

- SWOT Analysis: Organizational Context and Interested Parties Need & ExpectationDocument43 pagesSWOT Analysis: Organizational Context and Interested Parties Need & Expectationamril alrizaNo ratings yet

- Muhammad AliDocument1 pageMuhammad AliMariaJoaquinaCiezaGonzálezNo ratings yet

- General Auditing For IT Auditors PDFDocument4 pagesGeneral Auditing For IT Auditors PDFGerardo AraqueNo ratings yet

- Price Waterhouse Swift PDFDocument4 pagesPrice Waterhouse Swift PDFjairo lopezNo ratings yet

- Defect Management - Bug ReportDocument13 pagesDefect Management - Bug ReportalexNo ratings yet

- Profit Loss StatementDocument1 pageProfit Loss StatementhmarcalNo ratings yet

- EY in A Digital World Do You Know Where Your Risks Are Sa FinalDocument31 pagesEY in A Digital World Do You Know Where Your Risks Are Sa FinalMeet PanchalNo ratings yet

- Business Impact Analysis ExampleDocument4 pagesBusiness Impact Analysis ExampleArnel OlivarNo ratings yet

- Risk Management Policy - CorporateDocument18 pagesRisk Management Policy - CorporatemoinNo ratings yet

- Risk Assessment BackfilligDocument5 pagesRisk Assessment Backfilligmolobe mkhondoNo ratings yet

- KZ Deloitte Information Security Survey 2014 enDocument25 pagesKZ Deloitte Information Security Survey 2014 ensamuelNo ratings yet

- IT Internal Control Framework v7Document26 pagesIT Internal Control Framework v7biasilarissaNo ratings yet

- RA 001 Risk Analysis - Risk AssessementDocument2 pagesRA 001 Risk Analysis - Risk AssessementJoshua Guerrero CaloyongNo ratings yet

- PCS 7 Readme V8.1Document64 pagesPCS 7 Readme V8.1Chen CY100% (1)

- Strategic Risk Register PDF 1660418288Document25 pagesStrategic Risk Register PDF 1660418288mohamedNo ratings yet

- ITGC Assessment ExampleDocument7 pagesITGC Assessment ExampleETTORE JOHN DE VERANo ratings yet

- Enterprise Risk Matrix A3 PDFDocument1 pageEnterprise Risk Matrix A3 PDFDavid VelaNo ratings yet

- Payroll BrochureDocument16 pagesPayroll BrochureInfutureweb TechnologiesNo ratings yet

- DSC WATCH - Coast Stations Participating in MF, HF and VHF Watch-Keeping Using Digital Selective Calling TechniquesDocument5 pagesDSC WATCH - Coast Stations Participating in MF, HF and VHF Watch-Keeping Using Digital Selective Calling TechniquesmanojNo ratings yet

- SWIFT Customer Security ProgramDocument12 pagesSWIFT Customer Security Programco caNo ratings yet

- Systems Application and Products in Data ProcessingDocument22 pagesSystems Application and Products in Data ProcessingSanktifier100% (1)

- Audit Framework Under Information System and Cyber Security RegulationsDocument16 pagesAudit Framework Under Information System and Cyber Security Regulationsrishi_rajarshiNo ratings yet

- Sunera Best Practices For Remediating SoDsDocument7 pagesSunera Best Practices For Remediating SoDssura anil reddyNo ratings yet

- HITRUST Policies - Information Security Risk Management ProcedureDocument10 pagesHITRUST Policies - Information Security Risk Management Procedurealan dumsNo ratings yet

- Integration Access Control With Fiori Apps For S4HANA On-PremiseDocument5 pagesIntegration Access Control With Fiori Apps For S4HANA On-PremiseHasbleidy CelisNo ratings yet

- Internal Audit Dashboard Ver. 1Document18 pagesInternal Audit Dashboard Ver. 1Fazal KarimNo ratings yet

- List of Benefits For The Members of ICAIDocument39 pagesList of Benefits For The Members of ICAIcavishnukhandelwal100% (1)

- Scientific Research and Experimental Development (SR&ED) Expenditures ClaimDocument40 pagesScientific Research and Experimental Development (SR&ED) Expenditures ClaimmetroroadNo ratings yet

- 21 25 VPC Si Sys AdminDocument598 pages21 25 VPC Si Sys AdminNguyễn Lương QuyềnNo ratings yet

- Data Recovery PlanDocument11 pagesData Recovery PlanCream FamilyNo ratings yet

- CIS Microsoft SQL Server 2005 Benchmark v2.0.0Document166 pagesCIS Microsoft SQL Server 2005 Benchmark v2.0.0Oscar Javier Baquero SanchezNo ratings yet

- GRC Interview Q&ADocument22 pagesGRC Interview Q&Aishan royNo ratings yet

- Risk MGMTDocument51 pagesRisk MGMTJhanMarie Castillo-CamposanoNo ratings yet

- IC Agile Risk Register 9419Document4 pagesIC Agile Risk Register 9419senarathNo ratings yet

- Ransomware Self-Assessment Tool: OCTOBER 2020Document14 pagesRansomware Self-Assessment Tool: OCTOBER 2020AhmedAlHefnyNo ratings yet

- Auditing General and Application ControlsDocument13 pagesAuditing General and Application ControlschokriNo ratings yet

- ITT Provision of Web Hosting Services GMB DOM 57-09-21Document36 pagesITT Provision of Web Hosting Services GMB DOM 57-09-21Flexy BeatsNo ratings yet

- Cloud Controls Matrix Version 3.0: Control Domain Control Specification CCM V3.0 Control IDDocument363 pagesCloud Controls Matrix Version 3.0: Control Domain Control Specification CCM V3.0 Control IDmanishNo ratings yet

- Logistics Risk Assessment Tool TemplateDocument48 pagesLogistics Risk Assessment Tool TemplateSampurna SenNo ratings yet

- 2.325-Risk Assessment Procedure FinalDocument8 pages2.325-Risk Assessment Procedure Finalkirandevi1981No ratings yet

- PDF PPR 15 FiccaDocument44 pagesPDF PPR 15 FiccaPankaj GoyalNo ratings yet

- 1 Disaster Management Audit ReportDocument124 pages1 Disaster Management Audit ReportManan ChadhaNo ratings yet

- Windows and Linux Operating Systems From PDFDocument9 pagesWindows and Linux Operating Systems From PDFPAULA ANDREA PERALTA TRIANANo ratings yet

- Module 1 - What Is RiskDocument19 pagesModule 1 - What Is RiskKim Anh NguyenNo ratings yet

- Project Risk Management Lecture 1 (Printables)Document35 pagesProject Risk Management Lecture 1 (Printables)Muhammad AwaisNo ratings yet

- Itgc AssignmentDocument12 pagesItgc AssignmentSparshana KumariNo ratings yet

- Recordkeeping Risk Assessment MatrixDocument2 pagesRecordkeeping Risk Assessment MatrixEsteban OONo ratings yet

- Inventory Inventory IDR Control NoDocument23 pagesInventory Inventory IDR Control NoCA Rahul GuptaNo ratings yet

- Risk Management ProcessDocument40 pagesRisk Management ProcessAliAdnan AliAdnan100% (1)

- 03-05. - Sox y ITGC FrameworkDocument22 pages03-05. - Sox y ITGC FrameworkPedro PerezNo ratings yet

- RA 01 Risk Assessment FormDocument5 pagesRA 01 Risk Assessment FormAlfa RidziNo ratings yet

- Sample Risk and Issue LogsDocument29 pagesSample Risk and Issue LogsRhodora MaglinaoNo ratings yet

- Risk Analysis MemoDocument7 pagesRisk Analysis MemoAnonymous in4fhbdwkNo ratings yet

- Debt Interest Expense Substantive AnalyticalDocument2 pagesDebt Interest Expense Substantive AnalyticalErik RodriguesNo ratings yet

- AMLA Risk Assessment Methodology 28th February 2020Document26 pagesAMLA Risk Assessment Methodology 28th February 2020nishi nanavatiNo ratings yet

- Establish and Maintain WHS Management Systems: Submission DetailsDocument16 pagesEstablish and Maintain WHS Management Systems: Submission DetailsAndresPradaNo ratings yet

- MTN OFS Application Form EditableDocument1 pageMTN OFS Application Form Editablepeter sundayNo ratings yet

- BM ReviewDocument10 pagesBM ReviewFish SuperNo ratings yet

- Mid Term 2022 Company LawDocument4 pagesMid Term 2022 Company Lawpradeep ranaNo ratings yet

- No 5.1.fourth Generation Evalution Research (Qualitative Research Design)Document4 pagesNo 5.1.fourth Generation Evalution Research (Qualitative Research Design)Eko Wahyu ApriliantoNo ratings yet

- Negen Capital PMS Feb 22 FactsheetDocument5 pagesNegen Capital PMS Feb 22 Factsheetjeevan gangavarapuNo ratings yet

- Cash FlowsDocument26 pagesCash Flowsvickyprimus100% (1)

- Web Design RFP SampleDocument9 pagesWeb Design RFP Samplebarneygurl0% (1)

- PARTCOR NotesDocument19 pagesPARTCOR NotesKatrina PonceNo ratings yet

- Karina Market Structure SummaryDocument4 pagesKarina Market Structure SummaryKarina Permata SariNo ratings yet

- RM Lecture 04Document61 pagesRM Lecture 04vuduyducNo ratings yet

- SAP.C TS4CO 1909.v2020-05-21.q63Document16 pagesSAP.C TS4CO 1909.v2020-05-21.q63Vladimir Jovanovic0% (1)

- Print Media OKDocument23 pagesPrint Media OKEnchan Te TeNo ratings yet

- The Business Case For ASC 606 ComplianceDocument21 pagesThe Business Case For ASC 606 ComplianceSimplusNo ratings yet

- Patni Ar2009Document174 pagesPatni Ar2009chip_blueNo ratings yet

- Financial Analysis of A CompanyDocument10 pagesFinancial Analysis of A CompanyRupesh PuriNo ratings yet

- SCM SlidesDocument15 pagesSCM SlidesAmna NoorNo ratings yet

- Kajal Rai 24Document23 pagesKajal Rai 24KAJAL RAINo ratings yet

- MGT305 Ass1Document5 pagesMGT305 Ass1Trần Phước Diễm TrangNo ratings yet

- FINALDocument20 pagesFINALShubhangi BishnoiNo ratings yet

- Treatment of Assets Under Construction in SAP - From Creation To Settlement - SapGurusDocument14 pagesTreatment of Assets Under Construction in SAP - From Creation To Settlement - SapGurusAnanthakumar ANo ratings yet

- MM User ManualDocument316 pagesMM User ManualANILNo ratings yet

- Can Be Reproduced: Department of Justice Employees' Multi-Purpose CooperativeDocument3 pagesCan Be Reproduced: Department of Justice Employees' Multi-Purpose CooperativeSharlene338No ratings yet

- HRM Assignment - InfosysDocument4 pagesHRM Assignment - Infosyssumit SinghNo ratings yet

- Compare The Merits of The Entry Strategies Discussed in This ChapterDocument3 pagesCompare The Merits of The Entry Strategies Discussed in This ChapterVikram KumarNo ratings yet

- PneumaticDocument15 pagesPneumaticDesign ErNo ratings yet

- Statement of Single Largest Completed Contract BulbulDocument2 pagesStatement of Single Largest Completed Contract BulbulZeny BocadNo ratings yet

- Law 346Document2 pagesLaw 346Nuradilah BahardinNo ratings yet