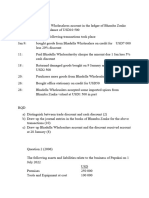

BK Holiday Package Form 4

BK Holiday Package Form 4

You might also like

- Creative Thinking Thinking MmunicationDocument334 pagesCreative Thinking Thinking Mmunicationimminseo6No ratings yet

- Intermediate Accounting - MidtermsDocument9 pagesIntermediate Accounting - MidtermsKim Cristian MaañoNo ratings yet

- INCOMPLETEDocument13 pagesINCOMPLETEOwen Bawlor ManozNo ratings yet

- Talking Fashion: Pierre Cardin Interviewed by Jan KedvesDocument5 pagesTalking Fashion: Pierre Cardin Interviewed by Jan KedvesJanKedves100% (1)

- SA1 - Grade AS CAIE Accounting Paper 2Document7 pagesSA1 - Grade AS CAIE Accounting Paper 221ke23b15089No ratings yet

- Review QuestionsDocument9 pagesReview QuestionsGamaya EmmanuelNo ratings yet

- Baf 1101financial Accounting 1Document3 pagesBaf 1101financial Accounting 1MORRIS GICHININo ratings yet

- Revision Questions-1Document6 pagesRevision Questions-1stanleymudzamiri8No ratings yet

- Accountancy CLASS-XI-WPS OfficeDocument7 pagesAccountancy CLASS-XI-WPS Officemaruthesh.vNo ratings yet

- DSR Mock Test - 1 - Ca FoundationDocument5 pagesDSR Mock Test - 1 - Ca Foundationmaskguy001No ratings yet

- Contentitemfile Clakzz57bxlrw0a21yjksjcx8 PDFDocument4 pagesContentitemfile Clakzz57bxlrw0a21yjksjcx8 PDFJoseph OndariNo ratings yet

- FDN J22 - TS 2 - P1 Account - QueDocument5 pagesFDN J22 - TS 2 - P1 Account - QueShantanu JadhavNo ratings yet

- Fac511s - Financial Accounting 101 - 1st Op - June 2023Document5 pagesFac511s - Financial Accounting 101 - 1st Op - June 2023nettebrandy8No ratings yet

- Exam (3) ASDocument6 pagesExam (3) ASUsama AslamNo ratings yet

- Additional Illustrations-14Document8 pagesAdditional Illustrations-14Gulneer LambaNo ratings yet

- Book-Keeping Form Three PDFDocument4 pagesBook-Keeping Form Three PDFdesa ntosNo ratings yet

- 18.01.2022 11 ACCOUNTS POST MID TERM 2021-22 CC Post Mid Acc 11Document3 pages18.01.2022 11 ACCOUNTS POST MID TERM 2021-22 CC Post Mid Acc 11Jr.No ratings yet

- BCPC 204 Exams Questions and Submission InstructionsDocument5 pagesBCPC 204 Exams Questions and Submission InstructionsHorace IvanNo ratings yet

- FS Withadj QuesDocument7 pagesFS Withadj QuesHimank SaklechaNo ratings yet

- Ca Foundation AccountsDocument7 pagesCa Foundation AccountssmartshivenduNo ratings yet

- Accounting MockDocument6 pagesAccounting MockGSNo ratings yet

- BBS 110 Introduction To Financial Accounting: Test IIDocument8 pagesBBS 110 Introduction To Financial Accounting: Test IIlloydbwalya588No ratings yet

- ACC 281 SEMINAR QUESTIONS Version 2Document8 pagesACC 281 SEMINAR QUESTIONS Version 2Joel SimonNo ratings yet

- 1ST Sem P.Y. Acct PaperDocument30 pages1ST Sem P.Y. Acct PaperSuraj KumarNo ratings yet

- Balance Sheet As On 1-4-2012: Liabilities RS Assets RSDocument2 pagesBalance Sheet As On 1-4-2012: Liabilities RS Assets RSL.D TECHNICAL POINTNo ratings yet

- Financial Accounting. (Sem-1) 2017-20Document39 pagesFinancial Accounting. (Sem-1) 2017-20Rahul DasNo ratings yet

- Model-Financial Accounting - Set1 - CZ21ADocument4 pagesModel-Financial Accounting - Set1 - CZ21AJuli SunNo ratings yet

- Costing and AccountancyDocument3 pagesCosting and AccountancyDeepakNo ratings yet

- Afar 2Document7 pagesAfar 2Diana Faye CaduadaNo ratings yet

- Answers - Module 2Document4 pagesAnswers - Module 2bhettyna noayNo ratings yet

- FA Weekend TestDocument5 pagesFA Weekend TestIryne MerrieNo ratings yet

- Cafc Test Paper Acc 03Document9 pagesCafc Test Paper Acc 03Vandana GuptaNo ratings yet

- CAF Test2 Accounts June23 R2 (Que)Document4 pagesCAF Test2 Accounts June23 R2 (Que)AISHWARYA DESHMUKHNo ratings yet

- FAR Preweek (B44)Document10 pagesFAR Preweek (B44)Haydy AntonioNo ratings yet

- Practice 2Document2 pagesPractice 2Thanh PhùngNo ratings yet

- Fundamentals of Financial AccountingDocument9 pagesFundamentals of Financial AccountingEmon EftakarNo ratings yet

- Additional Practical Problems-20Document16 pagesAdditional Practical Problems-20areet2701No ratings yet

- Corporate Accounting - IiDocument26 pagesCorporate Accounting - Iishankar1287No ratings yet

- Acctg 102 Prelim Exam With SolutionsDocument12 pagesAcctg 102 Prelim Exam With SolutionsYsabel ApostolNo ratings yet

- RTP Dec2023 p1Document32 pagesRTP Dec2023 p1Vaibhav M S100% (1)

- F&A Level II (Paper B)Document6 pagesF&A Level II (Paper B)almmohamed294No ratings yet

- Sem 2 - End Sem PapersDocument23 pagesSem 2 - End Sem Paperslalith sasankaNo ratings yet

- Book KeepingDocument6 pagesBook KeepingALE MEDIANo ratings yet

- Accounts Mega ModelDocument8 pagesAccounts Mega Modellekha ram100% (1)

- Financial Accounting 2019Document8 pagesFinancial Accounting 2019Ivy NinjaNo ratings yet

- Assets.: (Vi) Due To Lack of Information, Depreciation Has Not Been Provided On FixedDocument6 pagesAssets.: (Vi) Due To Lack of Information, Depreciation Has Not Been Provided On FixedMehul Gupta100% (1)

- Paper - 1: Principles & Practice of Accounting Questions True and FalseDocument32 pagesPaper - 1: Principles & Practice of Accounting Questions True and FalseShaindra SinghNo ratings yet

- Mock-Iv AccountsDocument6 pagesMock-Iv AccountsAnsh UdainiaNo ratings yet

- 2 Accounting PDFDocument3 pages2 Accounting PDFibrahimbdNo ratings yet

- Nama: Melvina Puhut Siregar Nim: 1932150049 E7-23 (Petty Cash) Mcmann, Inc. Decided To Establish A Petty Cash Fund To Help Ensure InternalDocument6 pagesNama: Melvina Puhut Siregar Nim: 1932150049 E7-23 (Petty Cash) Mcmann, Inc. Decided To Establish A Petty Cash Fund To Help Ensure Internalmelvina siregarNo ratings yet

- S4 BAFS 1st Term Test 2019-2020 Question PaperDocument3 pagesS4 BAFS 1st Term Test 2019-2020 Question PaperjjjjjjjjjjjjjjjjjjNo ratings yet

- Midterm Examination Suggested AnswersDocument9 pagesMidterm Examination Suggested AnswersJoshua CaraldeNo ratings yet

- F5 Bafs 2 QueDocument13 pagesF5 Bafs 2 Queouo So方No ratings yet

- Omar Muhktar Abusama Nov 19Document34 pagesOmar Muhktar Abusama Nov 19Garpt Kudasai100% (1)

- Xi Annual NewDocument5 pagesXi Annual NewPragadeshwar KarthikeyanNo ratings yet

- Auditing Problems: First PreboardDocument8 pagesAuditing Problems: First PreboardCarlo AgravanteNo ratings yet

- 13 BRSDocument8 pages13 BRS21ke23b15089No ratings yet

- INSTRUCTIONS: Answer ALL Questions Question One (20 Marks)Document2 pagesINSTRUCTIONS: Answer ALL Questions Question One (20 Marks)Frankincense WesleyNo ratings yet

- Practice 4Document2 pagesPractice 4Thanh PhùngNo ratings yet

- CBM 514-3 Question 3Document3 pagesCBM 514-3 Question 3hafsamohmd793No ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- J.K. Lasser's Small Business Taxes 2007: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2007: Your Complete Guide to a Better Bottom LineNo ratings yet

- Barangay SinabaanDocument1 pageBarangay SinabaanOmar Dizon IINo ratings yet

- Purposive CommunicationDocument15 pagesPurposive CommunicationJm SalvaniaNo ratings yet

- Api 577 Q 114Document31 pagesApi 577 Q 114Mohammed YoussefNo ratings yet

- MYCOBIT Control Objective Assessment FormsDocument5 pagesMYCOBIT Control Objective Assessment FormsRafasaxNo ratings yet

- 4 Statistics and Probability g11 Quarter 4 Module 4 Identifying The Appropriate Test Statistics Involving Population MeanDocument28 pages4 Statistics and Probability g11 Quarter 4 Module 4 Identifying The Appropriate Test Statistics Involving Population MeanISKA COMMISSIONNo ratings yet

- Advanced Quality ManualDocument17 pagesAdvanced Quality ManualalexrferreiraNo ratings yet

- Notice 1560323996Document28 pagesNotice 1560323996Priyadarshini SahooNo ratings yet

- Notch 8 Status - Jan 23 - v2Document1 pageNotch 8 Status - Jan 23 - v2qhq9w86txhNo ratings yet

- SDO Navotas Project-Assist - MAPEH Grade-8..Document17 pagesSDO Navotas Project-Assist - MAPEH Grade-8..Vanessa AsyaoNo ratings yet

- 10 Female Superheroes Who Depict Women EmpowermentDocument3 pages10 Female Superheroes Who Depict Women EmpowermentSharjeel ZamanNo ratings yet

- Bromberger & Halle 89 - Why Phonology Is DifferentDocument20 pagesBromberger & Halle 89 - Why Phonology Is DifferentamirzetzNo ratings yet

- PHD Thesis Library Science DownloadDocument8 pagesPHD Thesis Library Science Downloadyvrpugvcf100% (2)

- Cupid and PsycheDocument3 pagesCupid and PsycheRolex Daclitan BajentingNo ratings yet

- GR 6 Voc Words 4th QTRDocument5 pagesGR 6 Voc Words 4th QTRAzlynn Courtney FernandezNo ratings yet

- What Your Clothes Say About YouDocument2 pagesWhat Your Clothes Say About YousummerNo ratings yet

- McDonald's Vision Statement & Mission Statement Analysis - Panmore InstituteDocument3 pagesMcDonald's Vision Statement & Mission Statement Analysis - Panmore InstituteBorislav FRITZ FrancuskiNo ratings yet

- Services Procurement Data SheetDocument5 pagesServices Procurement Data Sheetrollingstone3mNo ratings yet

- Top 10 Best Fighter JetsDocument14 pagesTop 10 Best Fighter JetsArooj fatimaNo ratings yet

- Introduction To PBL at Hull York Medical School - TranscriptDocument4 pagesIntroduction To PBL at Hull York Medical School - TranscriptTrx AntraxNo ratings yet

- G.R. NO. L-5486 Dela Pena vs. HidalgoDocument18 pagesG.R. NO. L-5486 Dela Pena vs. HidalgoSheridan AnaretaNo ratings yet

- Elegoo Saturn 8K LCD Light Curable 3D Printer User ManualDocument20 pagesElegoo Saturn 8K LCD Light Curable 3D Printer User ManualStanNo ratings yet

- June 2013 Intake: Programmes OfferedDocument2 pagesJune 2013 Intake: Programmes OfferedThuran NathanNo ratings yet

- A User-Friendly Classification: The Irregular Verbs in EnglishDocument10 pagesA User-Friendly Classification: The Irregular Verbs in EnglishPabloNo ratings yet

- PDF The Military Balance 2020 First Edition The International Institute For Strategic Studies Iiss Ebook Full ChapterDocument53 pagesPDF The Military Balance 2020 First Edition The International Institute For Strategic Studies Iiss Ebook Full Chapteranita.reese465100% (1)

- 1,200 Calorie Diet Menu - 7 Day Lose 20 Pounds Weight Loss Meal Plan PDFDocument14 pages1,200 Calorie Diet Menu - 7 Day Lose 20 Pounds Weight Loss Meal Plan PDFABRAHAN SUPO TITONo ratings yet

- OfficialRules-BritneySpearsNYE CRDocument9 pagesOfficialRules-BritneySpearsNYE CRAbelardo Ch.No ratings yet

- Following The Cap Figure by Lydia KievenDocument415 pagesFollowing The Cap Figure by Lydia KievenCatherinNo ratings yet

- ABB Fittings PlugsDocument204 pagesABB Fittings PlugsjohnNo ratings yet

Download as docx, pdf, or txt

You might also like

- Creative Thinking Thinking MmunicationDocument334 pagesCreative Thinking Thinking Mmunicationimminseo6No ratings yet

- Intermediate Accounting - MidtermsDocument9 pagesIntermediate Accounting - MidtermsKim Cristian MaañoNo ratings yet

- INCOMPLETEDocument13 pagesINCOMPLETEOwen Bawlor ManozNo ratings yet

- Talking Fashion: Pierre Cardin Interviewed by Jan KedvesDocument5 pagesTalking Fashion: Pierre Cardin Interviewed by Jan KedvesJanKedves100% (1)

- SA1 - Grade AS CAIE Accounting Paper 2Document7 pagesSA1 - Grade AS CAIE Accounting Paper 221ke23b15089No ratings yet

- Review QuestionsDocument9 pagesReview QuestionsGamaya EmmanuelNo ratings yet

- Baf 1101financial Accounting 1Document3 pagesBaf 1101financial Accounting 1MORRIS GICHININo ratings yet

- Revision Questions-1Document6 pagesRevision Questions-1stanleymudzamiri8No ratings yet

- Accountancy CLASS-XI-WPS OfficeDocument7 pagesAccountancy CLASS-XI-WPS Officemaruthesh.vNo ratings yet

- DSR Mock Test - 1 - Ca FoundationDocument5 pagesDSR Mock Test - 1 - Ca Foundationmaskguy001No ratings yet

- Contentitemfile Clakzz57bxlrw0a21yjksjcx8 PDFDocument4 pagesContentitemfile Clakzz57bxlrw0a21yjksjcx8 PDFJoseph OndariNo ratings yet

- FDN J22 - TS 2 - P1 Account - QueDocument5 pagesFDN J22 - TS 2 - P1 Account - QueShantanu JadhavNo ratings yet

- Fac511s - Financial Accounting 101 - 1st Op - June 2023Document5 pagesFac511s - Financial Accounting 101 - 1st Op - June 2023nettebrandy8No ratings yet

- Exam (3) ASDocument6 pagesExam (3) ASUsama AslamNo ratings yet

- Additional Illustrations-14Document8 pagesAdditional Illustrations-14Gulneer LambaNo ratings yet

- Book-Keeping Form Three PDFDocument4 pagesBook-Keeping Form Three PDFdesa ntosNo ratings yet

- 18.01.2022 11 ACCOUNTS POST MID TERM 2021-22 CC Post Mid Acc 11Document3 pages18.01.2022 11 ACCOUNTS POST MID TERM 2021-22 CC Post Mid Acc 11Jr.No ratings yet

- BCPC 204 Exams Questions and Submission InstructionsDocument5 pagesBCPC 204 Exams Questions and Submission InstructionsHorace IvanNo ratings yet

- FS Withadj QuesDocument7 pagesFS Withadj QuesHimank SaklechaNo ratings yet

- Ca Foundation AccountsDocument7 pagesCa Foundation AccountssmartshivenduNo ratings yet

- Accounting MockDocument6 pagesAccounting MockGSNo ratings yet

- BBS 110 Introduction To Financial Accounting: Test IIDocument8 pagesBBS 110 Introduction To Financial Accounting: Test IIlloydbwalya588No ratings yet

- ACC 281 SEMINAR QUESTIONS Version 2Document8 pagesACC 281 SEMINAR QUESTIONS Version 2Joel SimonNo ratings yet

- 1ST Sem P.Y. Acct PaperDocument30 pages1ST Sem P.Y. Acct PaperSuraj KumarNo ratings yet

- Balance Sheet As On 1-4-2012: Liabilities RS Assets RSDocument2 pagesBalance Sheet As On 1-4-2012: Liabilities RS Assets RSL.D TECHNICAL POINTNo ratings yet

- Financial Accounting. (Sem-1) 2017-20Document39 pagesFinancial Accounting. (Sem-1) 2017-20Rahul DasNo ratings yet

- Model-Financial Accounting - Set1 - CZ21ADocument4 pagesModel-Financial Accounting - Set1 - CZ21AJuli SunNo ratings yet

- Costing and AccountancyDocument3 pagesCosting and AccountancyDeepakNo ratings yet

- Afar 2Document7 pagesAfar 2Diana Faye CaduadaNo ratings yet

- Answers - Module 2Document4 pagesAnswers - Module 2bhettyna noayNo ratings yet

- FA Weekend TestDocument5 pagesFA Weekend TestIryne MerrieNo ratings yet

- Cafc Test Paper Acc 03Document9 pagesCafc Test Paper Acc 03Vandana GuptaNo ratings yet

- CAF Test2 Accounts June23 R2 (Que)Document4 pagesCAF Test2 Accounts June23 R2 (Que)AISHWARYA DESHMUKHNo ratings yet

- FAR Preweek (B44)Document10 pagesFAR Preweek (B44)Haydy AntonioNo ratings yet

- Practice 2Document2 pagesPractice 2Thanh PhùngNo ratings yet

- Fundamentals of Financial AccountingDocument9 pagesFundamentals of Financial AccountingEmon EftakarNo ratings yet

- Additional Practical Problems-20Document16 pagesAdditional Practical Problems-20areet2701No ratings yet

- Corporate Accounting - IiDocument26 pagesCorporate Accounting - Iishankar1287No ratings yet

- Acctg 102 Prelim Exam With SolutionsDocument12 pagesAcctg 102 Prelim Exam With SolutionsYsabel ApostolNo ratings yet

- RTP Dec2023 p1Document32 pagesRTP Dec2023 p1Vaibhav M S100% (1)

- F&A Level II (Paper B)Document6 pagesF&A Level II (Paper B)almmohamed294No ratings yet

- Sem 2 - End Sem PapersDocument23 pagesSem 2 - End Sem Paperslalith sasankaNo ratings yet

- Book KeepingDocument6 pagesBook KeepingALE MEDIANo ratings yet

- Accounts Mega ModelDocument8 pagesAccounts Mega Modellekha ram100% (1)

- Financial Accounting 2019Document8 pagesFinancial Accounting 2019Ivy NinjaNo ratings yet

- Assets.: (Vi) Due To Lack of Information, Depreciation Has Not Been Provided On FixedDocument6 pagesAssets.: (Vi) Due To Lack of Information, Depreciation Has Not Been Provided On FixedMehul Gupta100% (1)

- Paper - 1: Principles & Practice of Accounting Questions True and FalseDocument32 pagesPaper - 1: Principles & Practice of Accounting Questions True and FalseShaindra SinghNo ratings yet

- Mock-Iv AccountsDocument6 pagesMock-Iv AccountsAnsh UdainiaNo ratings yet

- 2 Accounting PDFDocument3 pages2 Accounting PDFibrahimbdNo ratings yet

- Nama: Melvina Puhut Siregar Nim: 1932150049 E7-23 (Petty Cash) Mcmann, Inc. Decided To Establish A Petty Cash Fund To Help Ensure InternalDocument6 pagesNama: Melvina Puhut Siregar Nim: 1932150049 E7-23 (Petty Cash) Mcmann, Inc. Decided To Establish A Petty Cash Fund To Help Ensure Internalmelvina siregarNo ratings yet

- S4 BAFS 1st Term Test 2019-2020 Question PaperDocument3 pagesS4 BAFS 1st Term Test 2019-2020 Question PaperjjjjjjjjjjjjjjjjjjNo ratings yet

- Midterm Examination Suggested AnswersDocument9 pagesMidterm Examination Suggested AnswersJoshua CaraldeNo ratings yet

- F5 Bafs 2 QueDocument13 pagesF5 Bafs 2 Queouo So方No ratings yet

- Omar Muhktar Abusama Nov 19Document34 pagesOmar Muhktar Abusama Nov 19Garpt Kudasai100% (1)

- Xi Annual NewDocument5 pagesXi Annual NewPragadeshwar KarthikeyanNo ratings yet

- Auditing Problems: First PreboardDocument8 pagesAuditing Problems: First PreboardCarlo AgravanteNo ratings yet

- 13 BRSDocument8 pages13 BRS21ke23b15089No ratings yet

- INSTRUCTIONS: Answer ALL Questions Question One (20 Marks)Document2 pagesINSTRUCTIONS: Answer ALL Questions Question One (20 Marks)Frankincense WesleyNo ratings yet

- Practice 4Document2 pagesPractice 4Thanh PhùngNo ratings yet

- CBM 514-3 Question 3Document3 pagesCBM 514-3 Question 3hafsamohmd793No ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- J.K. Lasser's Small Business Taxes 2007: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2007: Your Complete Guide to a Better Bottom LineNo ratings yet

- Barangay SinabaanDocument1 pageBarangay SinabaanOmar Dizon IINo ratings yet

- Purposive CommunicationDocument15 pagesPurposive CommunicationJm SalvaniaNo ratings yet

- Api 577 Q 114Document31 pagesApi 577 Q 114Mohammed YoussefNo ratings yet

- MYCOBIT Control Objective Assessment FormsDocument5 pagesMYCOBIT Control Objective Assessment FormsRafasaxNo ratings yet

- 4 Statistics and Probability g11 Quarter 4 Module 4 Identifying The Appropriate Test Statistics Involving Population MeanDocument28 pages4 Statistics and Probability g11 Quarter 4 Module 4 Identifying The Appropriate Test Statistics Involving Population MeanISKA COMMISSIONNo ratings yet

- Advanced Quality ManualDocument17 pagesAdvanced Quality ManualalexrferreiraNo ratings yet

- Notice 1560323996Document28 pagesNotice 1560323996Priyadarshini SahooNo ratings yet

- Notch 8 Status - Jan 23 - v2Document1 pageNotch 8 Status - Jan 23 - v2qhq9w86txhNo ratings yet

- SDO Navotas Project-Assist - MAPEH Grade-8..Document17 pagesSDO Navotas Project-Assist - MAPEH Grade-8..Vanessa AsyaoNo ratings yet

- 10 Female Superheroes Who Depict Women EmpowermentDocument3 pages10 Female Superheroes Who Depict Women EmpowermentSharjeel ZamanNo ratings yet

- Bromberger & Halle 89 - Why Phonology Is DifferentDocument20 pagesBromberger & Halle 89 - Why Phonology Is DifferentamirzetzNo ratings yet

- PHD Thesis Library Science DownloadDocument8 pagesPHD Thesis Library Science Downloadyvrpugvcf100% (2)

- Cupid and PsycheDocument3 pagesCupid and PsycheRolex Daclitan BajentingNo ratings yet

- GR 6 Voc Words 4th QTRDocument5 pagesGR 6 Voc Words 4th QTRAzlynn Courtney FernandezNo ratings yet

- What Your Clothes Say About YouDocument2 pagesWhat Your Clothes Say About YousummerNo ratings yet

- McDonald's Vision Statement & Mission Statement Analysis - Panmore InstituteDocument3 pagesMcDonald's Vision Statement & Mission Statement Analysis - Panmore InstituteBorislav FRITZ FrancuskiNo ratings yet

- Services Procurement Data SheetDocument5 pagesServices Procurement Data Sheetrollingstone3mNo ratings yet

- Top 10 Best Fighter JetsDocument14 pagesTop 10 Best Fighter JetsArooj fatimaNo ratings yet

- Introduction To PBL at Hull York Medical School - TranscriptDocument4 pagesIntroduction To PBL at Hull York Medical School - TranscriptTrx AntraxNo ratings yet

- G.R. NO. L-5486 Dela Pena vs. HidalgoDocument18 pagesG.R. NO. L-5486 Dela Pena vs. HidalgoSheridan AnaretaNo ratings yet

- Elegoo Saturn 8K LCD Light Curable 3D Printer User ManualDocument20 pagesElegoo Saturn 8K LCD Light Curable 3D Printer User ManualStanNo ratings yet

- June 2013 Intake: Programmes OfferedDocument2 pagesJune 2013 Intake: Programmes OfferedThuran NathanNo ratings yet

- A User-Friendly Classification: The Irregular Verbs in EnglishDocument10 pagesA User-Friendly Classification: The Irregular Verbs in EnglishPabloNo ratings yet

- PDF The Military Balance 2020 First Edition The International Institute For Strategic Studies Iiss Ebook Full ChapterDocument53 pagesPDF The Military Balance 2020 First Edition The International Institute For Strategic Studies Iiss Ebook Full Chapteranita.reese465100% (1)

- 1,200 Calorie Diet Menu - 7 Day Lose 20 Pounds Weight Loss Meal Plan PDFDocument14 pages1,200 Calorie Diet Menu - 7 Day Lose 20 Pounds Weight Loss Meal Plan PDFABRAHAN SUPO TITONo ratings yet

- OfficialRules-BritneySpearsNYE CRDocument9 pagesOfficialRules-BritneySpearsNYE CRAbelardo Ch.No ratings yet

- Following The Cap Figure by Lydia KievenDocument415 pagesFollowing The Cap Figure by Lydia KievenCatherinNo ratings yet

- ABB Fittings PlugsDocument204 pagesABB Fittings PlugsjohnNo ratings yet