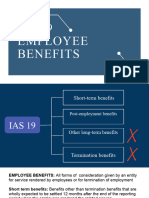

Ias 19

Ias 19

You might also like

- Base DocumentDocument2 pagesBase DocumentPrime Lending Service100% (1)

- Employee Benefits 03Document11 pagesEmployee Benefits 03Nelva Quinio33% (3)

- MFRS 119 Employee BenefitsDocument38 pagesMFRS 119 Employee BenefitsAin YanieNo ratings yet

- U.S. Individual Income Tax Return: Filing StatusDocument2 pagesU.S. Individual Income Tax Return: Filing StatusAndyTomas100% (1)

- Employee BenefitDocument32 pagesEmployee BenefitnatiNo ratings yet

- EmployeebenefitsreportDocument172 pagesEmployeebenefitsreportMikaela LacabaNo ratings yet

- Cfas Pas 19Document4 pagesCfas Pas 19Zyribelle Anne JAPSONNo ratings yet

- Chapter 17 Ia2 No ProblemsDocument23 pagesChapter 17 Ia2 No ProblemsJM Valonda Villena, CPA, MBANo ratings yet

- Ias 19 Employee BenefitsDocument43 pagesIas 19 Employee BenefitsHasan Ali BokhariNo ratings yet

- IAS 19 - Employee BenefitDocument49 pagesIAS 19 - Employee BenefitShah Kamal100% (2)

- Unit 03Document9 pagesUnit 03bobo tangaNo ratings yet

- 5.12.3 Employee BenefitsDocument5 pages5.12.3 Employee BenefitsBaher MohamedNo ratings yet

- Module 7 - Ia2 Final CBLDocument22 pagesModule 7 - Ia2 Final CBLErika EsguerraNo ratings yet

- Ias 19 Employee BeneftDocument24 pagesIas 19 Employee Beneftesulawyer2001No ratings yet

- Defined Benefit Pension PlanDocument8 pagesDefined Benefit Pension Planhenok AbebeNo ratings yet

- Employee BenefitsDocument83 pagesEmployee BenefitsArlene Rose GonzaloNo ratings yet

- Chapter 5 Employee BenefitsDocument29 pagesChapter 5 Employee BenefitsDudz MatienzoNo ratings yet

- Far28 Employee BenefitsDocument26 pagesFar28 Employee BenefitsCzar John JaudNo ratings yet

- IAS 19 - Employee BenefitDocument33 pagesIAS 19 - Employee BenefitlaaybaNo ratings yet

- IAS 19 Employee BenefitsDocument5 pagesIAS 19 Employee Benefitshae1234No ratings yet

- Short Notes - IAS 19Document7 pagesShort Notes - IAS 19Fakhur Zaman Mujeeb Ur RehmanNo ratings yet

- Monika Rehman Roll No 10Document19 pagesMonika Rehman Roll No 10Monika RehmanNo ratings yet

- Practical Accounting 2: BSA51E1 &BSA51E2Document68 pagesPractical Accounting 2: BSA51E1 &BSA51E2Carmelyn GonzalesNo ratings yet

- Chapter 5 Employee Benefit Part 1Document9 pagesChapter 5 Employee Benefit Part 1maria isabellaNo ratings yet

- Employee Benefits: PAS 19 Corpuz, Mary Lorie Anne ODocument38 pagesEmployee Benefits: PAS 19 Corpuz, Mary Lorie Anne OMarylorieanne CorpuzNo ratings yet

- Employee Benefit (Ias 19) FinalDocument36 pagesEmployee Benefit (Ias 19) FinalKanbiro OrkaidoNo ratings yet

- Employee Benefits Ias19Document42 pagesEmployee Benefits Ias19krishnaguptaNo ratings yet

- IAS 19 SummaryDocument6 pagesIAS 19 SummaryMuchaa VlogNo ratings yet

- Acivity Module 4Document2 pagesAcivity Module 4Honey TolentinoNo ratings yet

- Lesson Employee BenefitDocument18 pagesLesson Employee BenefitDesiree GalletoNo ratings yet

- Employee Benefits Pas 19Document44 pagesEmployee Benefits Pas 19Joanne Rey OcanaNo ratings yet

- Unit 7 E-Tutor PresentationDocument18 pagesUnit 7 E-Tutor PresentationKatrina EustaceNo ratings yet

- April 7 - CH 20 Part IDocument21 pagesApril 7 - CH 20 Part IMichael NguyenNo ratings yet

- CH20 PDFDocument81 pagesCH20 PDFelaine aureliaNo ratings yet

- Pas 19Document38 pagesPas 19Justine VeralloNo ratings yet

- IAS 19 Employee Benefits StudentDocument40 pagesIAS 19 Employee Benefits StudentYI WEI CHANGNo ratings yet

- Demas - Task 2Document7 pagesDemas - Task 2DemastaufiqNo ratings yet

- Chapter 08 FINDocument32 pagesChapter 08 FINUnoNo ratings yet

- Cliff Notes - PM RetirementDocument5 pagesCliff Notes - PM RetirementJohnathan JohnsonNo ratings yet

- MODULE Midterm FAR 3 EmpBenefitsDocument15 pagesMODULE Midterm FAR 3 EmpBenefitsKezNo ratings yet

- Employee Benefit 2020Document18 pagesEmployee Benefit 2020harman singhNo ratings yet

- Chapter 2 Lecture Notes.2021Document15 pagesChapter 2 Lecture Notes.2021Hoyin SinNo ratings yet

- Accounting For Pensions and Postretirement BenefitsDocument3 pagesAccounting For Pensions and Postretirement BenefitsDhivena JeonNo ratings yet

- Lecture # 11: Employee Benefits IAS-19Document3 pagesLecture # 11: Employee Benefits IAS-19ali hassnainNo ratings yet

- Pension Chap 1 IntroductionDocument5 pagesPension Chap 1 IntroductionJoe KimNo ratings yet

- Lesson Six: Accounting For Employee BenefitsDocument27 pagesLesson Six: Accounting For Employee BenefitssamclerryNo ratings yet

- Essay 2 - Employee BenefitsDocument3 pagesEssay 2 - Employee BenefitsSeiniNo ratings yet

- Cash Balance PlansDocument11 pagesCash Balance Plansmphillips36111No ratings yet

- IAS - 19 - Employee BenefitsDocument7 pagesIAS - 19 - Employee BenefitsCatalin BlesnocNo ratings yet

- Compensation and IncentivesDocument2 pagesCompensation and IncentivesLuis WashingtonNo ratings yet

- Ac Standard - AS15Document9 pagesAc Standard - AS15api-3705877No ratings yet

- MODULE Midterm FAR 3 EmpBenefitsDocument15 pagesMODULE Midterm FAR 3 EmpBenefitsJohn Mark FernandoNo ratings yet

- Ias 19 - Employee BenefitsDocument6 pagesIas 19 - Employee BenefitsIfyNo ratings yet

- IAS 19 Employee BenefitsDocument32 pagesIAS 19 Employee BenefitsTamirat Eshetu WoldeNo ratings yet

- IAS 19 Employee Benefits (2021)Document6 pagesIAS 19 Employee Benefits (2021)Tawanda Tatenda Herbert100% (1)

- PAT P13 Notes - Ias 19, 10, Ifrs 11 & Ifrs 12Document14 pagesPAT P13 Notes - Ias 19, 10, Ifrs 11 & Ifrs 12HSFXHFHXNo ratings yet

- Simplified Employee Pension Plan (SEP) - Internal Revenue ServiceDocument8 pagesSimplified Employee Pension Plan (SEP) - Internal Revenue Serviceabdullahkhanlala03No ratings yet

- PCOA Module 4 - For LMSDocument5 pagesPCOA Module 4 - For LMSJan JanNo ratings yet

- FR17 - Employee Benefits (Stud) .Document45 pagesFR17 - Employee Benefits (Stud) .duong duongNo ratings yet

- 1FU491 Employee BenefitsDocument14 pages1FU491 Employee BenefitsEmil DavtyanNo ratings yet

- Maximizing Your Wealth: A Comprehensive Guide to Understanding Gross and Net SalaryFrom EverandMaximizing Your Wealth: A Comprehensive Guide to Understanding Gross and Net SalaryNo ratings yet

- Ias 10Document12 pagesIas 10Reever RiverNo ratings yet

- SBL BPP Kit-2019 Copy 455Document1 pageSBL BPP Kit-2019 Copy 455Reever RiverNo ratings yet

- Ifrs 13Document23 pagesIfrs 13Reever RiverNo ratings yet

- Ias 38Document33 pagesIas 38Reever River100% (1)

- SBL BPP Kit-2019 Copy 423Document1 pageSBL BPP Kit-2019 Copy 423Reever RiverNo ratings yet

- SBL BPP Kit-2019 Copy 429Document1 pageSBL BPP Kit-2019 Copy 429Reever RiverNo ratings yet

- SBL BPP Kit-2019 Copy 447Document1 pageSBL BPP Kit-2019 Copy 447Reever RiverNo ratings yet

- SBL BPP Kit-2019 Copy 439Document1 pageSBL BPP Kit-2019 Copy 439Reever RiverNo ratings yet

- SBL BPP Kit-2019 Copy 453Document1 pageSBL BPP Kit-2019 Copy 453Reever RiverNo ratings yet

- SBL BPP Kit-2019 Copy 457Document1 pageSBL BPP Kit-2019 Copy 457Reever RiverNo ratings yet

- SBL BPP Kit-2019 Copy 450Document1 pageSBL BPP Kit-2019 Copy 450Reever RiverNo ratings yet

- F8-27 Liabilities, Provisions and ContingenciesDocument12 pagesF8-27 Liabilities, Provisions and ContingenciesReever RiverNo ratings yet

- F8-16 Analytical ProceduresDocument18 pagesF8-16 Analytical ProceduresReever RiverNo ratings yet

- Do Not Print Any of The Forms Provided To You Through Mail (If Not Provided and If You Require Blank Templates, Kindly Mail For It)Document16 pagesDo Not Print Any of The Forms Provided To You Through Mail (If Not Provided and If You Require Blank Templates, Kindly Mail For It)Riyaz RatnaNo ratings yet

- PAYE Return SampleDocument42 pagesPAYE Return Sampleoyesigye DennisNo ratings yet

- 4 Types of Retirement Plans and Employer-Sponsored PlansDocument1 page4 Types of Retirement Plans and Employer-Sponsored PlansThanu SuthatharanNo ratings yet

- Accounting Online Final ExamDocument2 pagesAccounting Online Final Examnilo biaNo ratings yet

- Social Protection Module 1Document21 pagesSocial Protection Module 1Bebaskita GintingNo ratings yet

- Chapter 4 pf-1Document20 pagesChapter 4 pf-1Neola LoboNo ratings yet

- WEEK 2-SIPacks-in-General-Mathematics-Quarter-2-FULL-version - WatermarkDocument15 pagesWEEK 2-SIPacks-in-General-Mathematics-Quarter-2-FULL-version - WatermarkMikaela Dianne AquinoNo ratings yet

- Border Roads Organisation: General Reserve Engineer ForceDocument36 pagesBorder Roads Organisation: General Reserve Engineer ForceViasNo ratings yet

- Form e 2022 Bi 16012023Document8 pagesForm e 2022 Bi 16012023HR Dept Urban Seafood SBNo ratings yet

- Salary: What Is Salary Structure?Document3 pagesSalary: What Is Salary Structure?Sri SubhaNo ratings yet

- No Name T1 2022Document42 pagesNo Name T1 2022Indo -CanadianNo ratings yet

- Personal Finance 2Nd Edition by Jane King Full ChapterDocument41 pagesPersonal Finance 2Nd Edition by Jane King Full Chaptermargret.brennan669100% (25)

- Auditing Payroll CycleDocument14 pagesAuditing Payroll CycleVernadette De GuzmanNo ratings yet

- Chapter 10 Review Updated 11th EdDocument15 pagesChapter 10 Review Updated 11th EdalmazwmbashiraNo ratings yet

- Balbes, Bella Ronah P. Act183: Income Taxation Prelim Exam S.Y 2020-2021 True or FalseDocument9 pagesBalbes, Bella Ronah P. Act183: Income Taxation Prelim Exam S.Y 2020-2021 True or FalseBella RonahNo ratings yet

- 131 San Miguel Corporation Vs InciongDocument1 page131 San Miguel Corporation Vs InciongRobelle RizonNo ratings yet

- SLM-19615-B Com-INCOME TAX LAW AND ACCOUNTS - 0Document308 pagesSLM-19615-B Com-INCOME TAX LAW AND ACCOUNTS - 0Deva T NNo ratings yet

- Identify The Letter of The Choice That Best Completes The Statement or Answers The QuestionDocument171 pagesIdentify The Letter of The Choice That Best Completes The Statement or Answers The QuestionRengeline LucasNo ratings yet

- Lecture 3 EstateDocument21 pagesLecture 3 EstateYanPing AngNo ratings yet

- Income Tax CalculatorDocument4 pagesIncome Tax CalculatorAchin AgarwalNo ratings yet

- Busn298 Assignment1-2Document3 pagesBusn298 Assignment1-2Estephany ChungNo ratings yet

- Tax Formula and Tax Determination An Overview of Property TransactionsDocument23 pagesTax Formula and Tax Determination An Overview of Property TransactionsJames Riley Case100% (1)

- BSNL DR-JTO Salary Analysis-After 2nd PRCDocument2 pagesBSNL DR-JTO Salary Analysis-After 2nd PRCEarnest JayakaranNo ratings yet

- English-Vietnamese Glossary of Tax Words and Phrases: Used in Publications Issued by The IRSDocument21 pagesEnglish-Vietnamese Glossary of Tax Words and Phrases: Used in Publications Issued by The IRSGiang NguyễnNo ratings yet

- Assignment: Ueh University Business School Banking DepartmentDocument16 pagesAssignment: Ueh University Business School Banking DepartmentĐặng Hiểu NghiNo ratings yet

- Epa 20240220434705Document1 pageEpa 20240220434705ekamgulisNo ratings yet

- 32 Claim Procedure Under PMBSBY PMJBY1Document21 pages32 Claim Procedure Under PMBSBY PMJBY1taniaNo ratings yet

- Income TaxationDocument1 pageIncome TaxationJay-ar ReyesNo ratings yet

Download as pdf or txt

You might also like

- Base DocumentDocument2 pagesBase DocumentPrime Lending Service100% (1)

- Employee Benefits 03Document11 pagesEmployee Benefits 03Nelva Quinio33% (3)

- MFRS 119 Employee BenefitsDocument38 pagesMFRS 119 Employee BenefitsAin YanieNo ratings yet

- U.S. Individual Income Tax Return: Filing StatusDocument2 pagesU.S. Individual Income Tax Return: Filing StatusAndyTomas100% (1)

- Employee BenefitDocument32 pagesEmployee BenefitnatiNo ratings yet

- EmployeebenefitsreportDocument172 pagesEmployeebenefitsreportMikaela LacabaNo ratings yet

- Cfas Pas 19Document4 pagesCfas Pas 19Zyribelle Anne JAPSONNo ratings yet

- Chapter 17 Ia2 No ProblemsDocument23 pagesChapter 17 Ia2 No ProblemsJM Valonda Villena, CPA, MBANo ratings yet

- Ias 19 Employee BenefitsDocument43 pagesIas 19 Employee BenefitsHasan Ali BokhariNo ratings yet

- IAS 19 - Employee BenefitDocument49 pagesIAS 19 - Employee BenefitShah Kamal100% (2)

- Unit 03Document9 pagesUnit 03bobo tangaNo ratings yet

- 5.12.3 Employee BenefitsDocument5 pages5.12.3 Employee BenefitsBaher MohamedNo ratings yet

- Module 7 - Ia2 Final CBLDocument22 pagesModule 7 - Ia2 Final CBLErika EsguerraNo ratings yet

- Ias 19 Employee BeneftDocument24 pagesIas 19 Employee Beneftesulawyer2001No ratings yet

- Defined Benefit Pension PlanDocument8 pagesDefined Benefit Pension Planhenok AbebeNo ratings yet

- Employee BenefitsDocument83 pagesEmployee BenefitsArlene Rose GonzaloNo ratings yet

- Chapter 5 Employee BenefitsDocument29 pagesChapter 5 Employee BenefitsDudz MatienzoNo ratings yet

- Far28 Employee BenefitsDocument26 pagesFar28 Employee BenefitsCzar John JaudNo ratings yet

- IAS 19 - Employee BenefitDocument33 pagesIAS 19 - Employee BenefitlaaybaNo ratings yet

- IAS 19 Employee BenefitsDocument5 pagesIAS 19 Employee Benefitshae1234No ratings yet

- Short Notes - IAS 19Document7 pagesShort Notes - IAS 19Fakhur Zaman Mujeeb Ur RehmanNo ratings yet

- Monika Rehman Roll No 10Document19 pagesMonika Rehman Roll No 10Monika RehmanNo ratings yet

- Practical Accounting 2: BSA51E1 &BSA51E2Document68 pagesPractical Accounting 2: BSA51E1 &BSA51E2Carmelyn GonzalesNo ratings yet

- Chapter 5 Employee Benefit Part 1Document9 pagesChapter 5 Employee Benefit Part 1maria isabellaNo ratings yet

- Employee Benefits: PAS 19 Corpuz, Mary Lorie Anne ODocument38 pagesEmployee Benefits: PAS 19 Corpuz, Mary Lorie Anne OMarylorieanne CorpuzNo ratings yet

- Employee Benefit (Ias 19) FinalDocument36 pagesEmployee Benefit (Ias 19) FinalKanbiro OrkaidoNo ratings yet

- Employee Benefits Ias19Document42 pagesEmployee Benefits Ias19krishnaguptaNo ratings yet

- IAS 19 SummaryDocument6 pagesIAS 19 SummaryMuchaa VlogNo ratings yet

- Acivity Module 4Document2 pagesAcivity Module 4Honey TolentinoNo ratings yet

- Lesson Employee BenefitDocument18 pagesLesson Employee BenefitDesiree GalletoNo ratings yet

- Employee Benefits Pas 19Document44 pagesEmployee Benefits Pas 19Joanne Rey OcanaNo ratings yet

- Unit 7 E-Tutor PresentationDocument18 pagesUnit 7 E-Tutor PresentationKatrina EustaceNo ratings yet

- April 7 - CH 20 Part IDocument21 pagesApril 7 - CH 20 Part IMichael NguyenNo ratings yet

- CH20 PDFDocument81 pagesCH20 PDFelaine aureliaNo ratings yet

- Pas 19Document38 pagesPas 19Justine VeralloNo ratings yet

- IAS 19 Employee Benefits StudentDocument40 pagesIAS 19 Employee Benefits StudentYI WEI CHANGNo ratings yet

- Demas - Task 2Document7 pagesDemas - Task 2DemastaufiqNo ratings yet

- Chapter 08 FINDocument32 pagesChapter 08 FINUnoNo ratings yet

- Cliff Notes - PM RetirementDocument5 pagesCliff Notes - PM RetirementJohnathan JohnsonNo ratings yet

- MODULE Midterm FAR 3 EmpBenefitsDocument15 pagesMODULE Midterm FAR 3 EmpBenefitsKezNo ratings yet

- Employee Benefit 2020Document18 pagesEmployee Benefit 2020harman singhNo ratings yet

- Chapter 2 Lecture Notes.2021Document15 pagesChapter 2 Lecture Notes.2021Hoyin SinNo ratings yet

- Accounting For Pensions and Postretirement BenefitsDocument3 pagesAccounting For Pensions and Postretirement BenefitsDhivena JeonNo ratings yet

- Lecture # 11: Employee Benefits IAS-19Document3 pagesLecture # 11: Employee Benefits IAS-19ali hassnainNo ratings yet

- Pension Chap 1 IntroductionDocument5 pagesPension Chap 1 IntroductionJoe KimNo ratings yet

- Lesson Six: Accounting For Employee BenefitsDocument27 pagesLesson Six: Accounting For Employee BenefitssamclerryNo ratings yet

- Essay 2 - Employee BenefitsDocument3 pagesEssay 2 - Employee BenefitsSeiniNo ratings yet

- Cash Balance PlansDocument11 pagesCash Balance Plansmphillips36111No ratings yet

- IAS - 19 - Employee BenefitsDocument7 pagesIAS - 19 - Employee BenefitsCatalin BlesnocNo ratings yet

- Compensation and IncentivesDocument2 pagesCompensation and IncentivesLuis WashingtonNo ratings yet

- Ac Standard - AS15Document9 pagesAc Standard - AS15api-3705877No ratings yet

- MODULE Midterm FAR 3 EmpBenefitsDocument15 pagesMODULE Midterm FAR 3 EmpBenefitsJohn Mark FernandoNo ratings yet

- Ias 19 - Employee BenefitsDocument6 pagesIas 19 - Employee BenefitsIfyNo ratings yet

- IAS 19 Employee BenefitsDocument32 pagesIAS 19 Employee BenefitsTamirat Eshetu WoldeNo ratings yet

- IAS 19 Employee Benefits (2021)Document6 pagesIAS 19 Employee Benefits (2021)Tawanda Tatenda Herbert100% (1)

- PAT P13 Notes - Ias 19, 10, Ifrs 11 & Ifrs 12Document14 pagesPAT P13 Notes - Ias 19, 10, Ifrs 11 & Ifrs 12HSFXHFHXNo ratings yet

- Simplified Employee Pension Plan (SEP) - Internal Revenue ServiceDocument8 pagesSimplified Employee Pension Plan (SEP) - Internal Revenue Serviceabdullahkhanlala03No ratings yet

- PCOA Module 4 - For LMSDocument5 pagesPCOA Module 4 - For LMSJan JanNo ratings yet

- FR17 - Employee Benefits (Stud) .Document45 pagesFR17 - Employee Benefits (Stud) .duong duongNo ratings yet

- 1FU491 Employee BenefitsDocument14 pages1FU491 Employee BenefitsEmil DavtyanNo ratings yet

- Maximizing Your Wealth: A Comprehensive Guide to Understanding Gross and Net SalaryFrom EverandMaximizing Your Wealth: A Comprehensive Guide to Understanding Gross and Net SalaryNo ratings yet

- Ias 10Document12 pagesIas 10Reever RiverNo ratings yet

- SBL BPP Kit-2019 Copy 455Document1 pageSBL BPP Kit-2019 Copy 455Reever RiverNo ratings yet

- Ifrs 13Document23 pagesIfrs 13Reever RiverNo ratings yet

- Ias 38Document33 pagesIas 38Reever River100% (1)

- SBL BPP Kit-2019 Copy 423Document1 pageSBL BPP Kit-2019 Copy 423Reever RiverNo ratings yet

- SBL BPP Kit-2019 Copy 429Document1 pageSBL BPP Kit-2019 Copy 429Reever RiverNo ratings yet

- SBL BPP Kit-2019 Copy 447Document1 pageSBL BPP Kit-2019 Copy 447Reever RiverNo ratings yet

- SBL BPP Kit-2019 Copy 439Document1 pageSBL BPP Kit-2019 Copy 439Reever RiverNo ratings yet

- SBL BPP Kit-2019 Copy 453Document1 pageSBL BPP Kit-2019 Copy 453Reever RiverNo ratings yet

- SBL BPP Kit-2019 Copy 457Document1 pageSBL BPP Kit-2019 Copy 457Reever RiverNo ratings yet

- SBL BPP Kit-2019 Copy 450Document1 pageSBL BPP Kit-2019 Copy 450Reever RiverNo ratings yet

- F8-27 Liabilities, Provisions and ContingenciesDocument12 pagesF8-27 Liabilities, Provisions and ContingenciesReever RiverNo ratings yet

- F8-16 Analytical ProceduresDocument18 pagesF8-16 Analytical ProceduresReever RiverNo ratings yet

- Do Not Print Any of The Forms Provided To You Through Mail (If Not Provided and If You Require Blank Templates, Kindly Mail For It)Document16 pagesDo Not Print Any of The Forms Provided To You Through Mail (If Not Provided and If You Require Blank Templates, Kindly Mail For It)Riyaz RatnaNo ratings yet

- PAYE Return SampleDocument42 pagesPAYE Return Sampleoyesigye DennisNo ratings yet

- 4 Types of Retirement Plans and Employer-Sponsored PlansDocument1 page4 Types of Retirement Plans and Employer-Sponsored PlansThanu SuthatharanNo ratings yet

- Accounting Online Final ExamDocument2 pagesAccounting Online Final Examnilo biaNo ratings yet

- Social Protection Module 1Document21 pagesSocial Protection Module 1Bebaskita GintingNo ratings yet

- Chapter 4 pf-1Document20 pagesChapter 4 pf-1Neola LoboNo ratings yet

- WEEK 2-SIPacks-in-General-Mathematics-Quarter-2-FULL-version - WatermarkDocument15 pagesWEEK 2-SIPacks-in-General-Mathematics-Quarter-2-FULL-version - WatermarkMikaela Dianne AquinoNo ratings yet

- Border Roads Organisation: General Reserve Engineer ForceDocument36 pagesBorder Roads Organisation: General Reserve Engineer ForceViasNo ratings yet

- Form e 2022 Bi 16012023Document8 pagesForm e 2022 Bi 16012023HR Dept Urban Seafood SBNo ratings yet

- Salary: What Is Salary Structure?Document3 pagesSalary: What Is Salary Structure?Sri SubhaNo ratings yet

- No Name T1 2022Document42 pagesNo Name T1 2022Indo -CanadianNo ratings yet

- Personal Finance 2Nd Edition by Jane King Full ChapterDocument41 pagesPersonal Finance 2Nd Edition by Jane King Full Chaptermargret.brennan669100% (25)

- Auditing Payroll CycleDocument14 pagesAuditing Payroll CycleVernadette De GuzmanNo ratings yet

- Chapter 10 Review Updated 11th EdDocument15 pagesChapter 10 Review Updated 11th EdalmazwmbashiraNo ratings yet

- Balbes, Bella Ronah P. Act183: Income Taxation Prelim Exam S.Y 2020-2021 True or FalseDocument9 pagesBalbes, Bella Ronah P. Act183: Income Taxation Prelim Exam S.Y 2020-2021 True or FalseBella RonahNo ratings yet

- 131 San Miguel Corporation Vs InciongDocument1 page131 San Miguel Corporation Vs InciongRobelle RizonNo ratings yet

- SLM-19615-B Com-INCOME TAX LAW AND ACCOUNTS - 0Document308 pagesSLM-19615-B Com-INCOME TAX LAW AND ACCOUNTS - 0Deva T NNo ratings yet

- Identify The Letter of The Choice That Best Completes The Statement or Answers The QuestionDocument171 pagesIdentify The Letter of The Choice That Best Completes The Statement or Answers The QuestionRengeline LucasNo ratings yet

- Lecture 3 EstateDocument21 pagesLecture 3 EstateYanPing AngNo ratings yet

- Income Tax CalculatorDocument4 pagesIncome Tax CalculatorAchin AgarwalNo ratings yet

- Busn298 Assignment1-2Document3 pagesBusn298 Assignment1-2Estephany ChungNo ratings yet

- Tax Formula and Tax Determination An Overview of Property TransactionsDocument23 pagesTax Formula and Tax Determination An Overview of Property TransactionsJames Riley Case100% (1)

- BSNL DR-JTO Salary Analysis-After 2nd PRCDocument2 pagesBSNL DR-JTO Salary Analysis-After 2nd PRCEarnest JayakaranNo ratings yet

- English-Vietnamese Glossary of Tax Words and Phrases: Used in Publications Issued by The IRSDocument21 pagesEnglish-Vietnamese Glossary of Tax Words and Phrases: Used in Publications Issued by The IRSGiang NguyễnNo ratings yet

- Assignment: Ueh University Business School Banking DepartmentDocument16 pagesAssignment: Ueh University Business School Banking DepartmentĐặng Hiểu NghiNo ratings yet

- Epa 20240220434705Document1 pageEpa 20240220434705ekamgulisNo ratings yet

- 32 Claim Procedure Under PMBSBY PMJBY1Document21 pages32 Claim Procedure Under PMBSBY PMJBY1taniaNo ratings yet

- Income TaxationDocument1 pageIncome TaxationJay-ar ReyesNo ratings yet