Chapter 3 (Mathematical)

Chapter 3 (Mathematical)

You might also like

- Section 8.1 Review Questions (Page 275)Document65 pagesSection 8.1 Review Questions (Page 275)CJ Ngo100% (13)

- CH 06 SMDocument94 pagesCH 06 SMapi-234680678No ratings yet

- CH 5 - AdjustmentsDocument24 pagesCH 5 - Adjustmentsmuhamad elmiNo ratings yet

- Competency - Based HRD System in Public Service: 1 Hilario P. MartinezDocument142 pagesCompetency - Based HRD System in Public Service: 1 Hilario P. MartinezJewel AnggoyNo ratings yet

- Aimt ProspectusDocument40 pagesAimt ProspectusdustydiamondNo ratings yet

- Depreciation: Submitted By: Abhilasha Lovepreet Parul Sunira TarrunnumDocument31 pagesDepreciation: Submitted By: Abhilasha Lovepreet Parul Sunira TarrunnumnimrandNo ratings yet

- IPPTChap010 1Document38 pagesIPPTChap010 1JackNo ratings yet

- 2019 PES Accounting Unit 4 Outcome 1 Set 1 Solution FINALDocument9 pages2019 PES Accounting Unit 4 Outcome 1 Set 1 Solution FINALLachlan McFarlandNo ratings yet

- Acct225 Cap3Document17 pagesAcct225 Cap3devoflashNo ratings yet

- Modul 04 - Dilutive Securities and Earning Per ShareDocument4 pagesModul 04 - Dilutive Securities and Earning Per ShareHilma Nahla SawalyaNo ratings yet

- Depreciation-2Document9 pagesDepreciation-2divya shindeNo ratings yet

- Module 5 Answer KeysDocument5 pagesModule 5 Answer KeysJaspreetNo ratings yet

- L.T. LiabilitiesDocument18 pagesL.T. LiabilitiesNaeemullah baigNo ratings yet

- Accrual & PrepaymentsDocument4 pagesAccrual & PrepaymentsronstarcaristaNo ratings yet

- Bài tập C3Document10 pagesBài tập C3Khanh LêNo ratings yet

- L T +liabilitiesDocument18 pagesL T +liabilitiesTaha EjazNo ratings yet

- A A P F S: Djusting Ccounts AND Reparing Inancial TatementsDocument39 pagesA A P F S: Djusting Ccounts AND Reparing Inancial TatementsBoo LeNo ratings yet

- DepreciationDocument9 pagesDepreciationPriyank JainNo ratings yet

- L.T. LiabilitiesDocument18 pagesL.T. LiabilitiesMustafa Bin ShakeelNo ratings yet

- F3 - ACCA Chapter-10-1Document18 pagesF3 - ACCA Chapter-10-1Nile NguyenNo ratings yet

- E3-5 (LO 3) Adjusting Entries: InstructionsDocument6 pagesE3-5 (LO 3) Adjusting Entries: InstructionsAntonios Fahed0% (1)

- Adilah Aprilia - 4122201115 - AkuntansiDocument11 pagesAdilah Aprilia - 4122201115 - AkuntansiDava SyafriandanaNo ratings yet

- Topic 7 - Tutorial SolutionsDocument25 pagesTopic 7 - Tutorial SolutionsnaboumilikaNo ratings yet

- Accounts Compiler by Rahul Malkan Sir-73-98Document26 pagesAccounts Compiler by Rahul Malkan Sir-73-98sanketNo ratings yet

- ACCT 1026 Lesson 8Document7 pagesACCT 1026 Lesson 8Daniel MadarangNo ratings yet

- Investment Accounts: Basic ConceptsDocument13 pagesInvestment Accounts: Basic ConceptsDebasis KarNo ratings yet

- Tutorial Letter 202/1/2020: Financial Accounting Principles For Law PractitionersDocument9 pagesTutorial Letter 202/1/2020: Financial Accounting Principles For Law Practitionersall green associatesNo ratings yet

- Kts g11 - Principles of Accounts Final AdjustmentsDocument16 pagesKts g11 - Principles of Accounts Final AdjustmentsBupe Banda100% (1)

- Introduction To Financial Modelling: Purpose Steps For Building A Financial ModelDocument22 pagesIntroduction To Financial Modelling: Purpose Steps For Building A Financial ModelAnubhavNo ratings yet

- Assignment 1 - Financial Accounting - January 21Document3 pagesAssignment 1 - Financial Accounting - January 21Ednalyn PascualNo ratings yet

- Chapter 2 (Mathematical)Document9 pagesChapter 2 (Mathematical)Sabbir HossainNo ratings yet

- ACC - Chapter 11Document29 pagesACC - Chapter 11Le Pham Khanh Ha (K17 HCM)No ratings yet

- Aol AccDocument19 pagesAol AccANGELYCA LAURANo ratings yet

- Midterm AccountingDocument28 pagesMidterm Accountingk61.2213520037No ratings yet

- IF2 - Project 1 Solution PDFDocument9 pagesIF2 - Project 1 Solution PDFBillNo ratings yet

- Acc 201 CH3Document7 pagesAcc 201 CH3Trickster TwelveNo ratings yet

- Accruals and PrepaymentsDocument28 pagesAccruals and Prepaymentsvpq7qcwszyNo ratings yet

- 5 Investment AccountsDocument11 pages5 Investment AccountsBAZINGANo ratings yet

- Question On Financial Instruments - Part 1Document9 pagesQuestion On Financial Instruments - Part 1pratikdubey9586No ratings yet

- DepreciationDocument18 pagesDepreciationManuthi HewawasamNo ratings yet

- Acct101-3 - (Your Name)Document9 pagesAcct101-3 - (Your Name)Vedanshi BihaniNo ratings yet

- Fra 3Document7 pagesFra 3Subhajyoti MukhopadhyayNo ratings yet

- Adjusting Entries Pt. BerkahDocument3 pagesAdjusting Entries Pt. Berkahmogi ertantoNo ratings yet

- Depreciation Worksheet Straightline MethodDocument12 pagesDepreciation Worksheet Straightline MethodJamie-Lee O'ConnorNo ratings yet

- Depreciation Research WorkDocument7 pagesDepreciation Research Workgargbhavika875No ratings yet

- Lecture Discussion Final On Adjusting Entries From Accrual To Inventory AdjustmentDocument39 pagesLecture Discussion Final On Adjusting Entries From Accrual To Inventory AdjustmentGarp BarrocaNo ratings yet

- Q.3-Question and SolutionDocument4 pagesQ.3-Question and SolutionFIROZ KHANNo ratings yet

- RERETESTDocument4 pagesRERETESTshveta0% (1)

- KZN 2019 Prelim MemoDocument17 pagesKZN 2019 Prelim Memotshegofatsosekgothe299No ratings yet

- Udocz Inc Monthly Treasury 2023 10Document9 pagesUdocz Inc Monthly Treasury 2023 10Carlos EffioNo ratings yet

- Bsa Lecture Discussion On AccrualsDocument8 pagesBsa Lecture Discussion On AccrualsGarp BarrocaNo ratings yet

- Jimenez, Angel Kaye October 8, 2020 Bsa 2 Year ACC 216 9:45-11:45 Assignment-Depreciation MethodsDocument4 pagesJimenez, Angel Kaye October 8, 2020 Bsa 2 Year ACC 216 9:45-11:45 Assignment-Depreciation MethodsAngel Kaye Nacionales JimenezNo ratings yet

- Unit 2 - Accountingformanager - AnanduDocument52 pagesUnit 2 - Accountingformanager - Ananducraziestidiot31No ratings yet

- Chapter 11Document65 pagesChapter 11Duong Duc Ngoc (K17 HL)No ratings yet

- Q5 Partnership Final Accs QuestionsDocument2 pagesQ5 Partnership Final Accs QuestionsIsha KatiyarNo ratings yet

- Adjustment and Closing Entry-SolutionDocument3 pagesAdjustment and Closing Entry-SolutionSerazul Arafin MrinmoyNo ratings yet

- DepreciationDocument3 pagesDepreciationSarath kumar CNo ratings yet

- Depreciation Provision ReservesDocument60 pagesDepreciation Provision ReservesjonesmbNo ratings yet

- University of Cambridge International Examinations General Certificate of Education Advanced Subsidiary Level and Advanced LevelDocument12 pagesUniversity of Cambridge International Examinations General Certificate of Education Advanced Subsidiary Level and Advanced LevelSamin IslamNo ratings yet

- m7 - Note Sample Problems With Solutions Chs 14 and 15Document6 pagesm7 - Note Sample Problems With Solutions Chs 14 and 15Marie Fe GullesNo ratings yet

- Working Paper - PropertyDocument34 pagesWorking Paper - Propertyjahidemam10No ratings yet

- 4 - Test 4 SolutionDocument7 pages4 - Test 4 SolutionAashika SamaiyaNo ratings yet

- Comprehension Questions: 1. What Are Minimum Lease Payments'?Document13 pagesComprehension Questions: 1. What Are Minimum Lease Payments'?Amit ShuklaNo ratings yet

- Enhanced Cooperation and Integration Between Indonesia and Timor-Leste: Scoping StudyFrom EverandEnhanced Cooperation and Integration Between Indonesia and Timor-Leste: Scoping StudyNo ratings yet

- 06 Genome Assembly 1Document26 pages06 Genome Assembly 1Sabbir HossainNo ratings yet

- 07 Read MappingDocument75 pages07 Read MappingSabbir HossainNo ratings yet

- MYSQL DDL COMMANDS v3 (Updated)Document20 pagesMYSQL DDL COMMANDS v3 (Updated)Sabbir HossainNo ratings yet

- 13 (Sabbir) Cross-Disciplinary Perspectives On Meta-Learning For Algorithm SelectionDocument25 pages13 (Sabbir) Cross-Disciplinary Perspectives On Meta-Learning For Algorithm SelectionSabbir HossainNo ratings yet

- Low Cost Comparisons File CopiesDocument7 pagesLow Cost Comparisons File CopiesSabbir HossainNo ratings yet

- ADVACC JOINT ARRANGEMENT PART 2 PRE-FINAL (Autosaved)Document45 pagesADVACC JOINT ARRANGEMENT PART 2 PRE-FINAL (Autosaved)Christine Joyce MagoteNo ratings yet

- AF102 Assignemnt - Group 4 (7533)Document10 pagesAF102 Assignemnt - Group 4 (7533)Anjali PrasadNo ratings yet

- Accounts InternalDocument6 pagesAccounts Internalaarav balujaNo ratings yet

- BK 16M BoeDocument5 pagesBK 16M BoeMushir LariNo ratings yet

- TRUE FALSE SCANNER by NahtaDocument88 pagesTRUE FALSE SCANNER by NahtaHimanshu RayNo ratings yet

- Deepti CVDocument2 pagesDeepti CVDeeptiNo ratings yet

- Advanced Financial Accounting and Reporting G.P. Costa Installment SalesDocument6 pagesAdvanced Financial Accounting and Reporting G.P. Costa Installment SalesmkNo ratings yet

- Quantity Cutting Department Assembly Department Packaging DepartmentDocument6 pagesQuantity Cutting Department Assembly Department Packaging DepartmentElaine Fiona VillafuerteNo ratings yet

- Disha MehtaDocument2 pagesDisha Mehtaapi-72678201No ratings yet

- Full Download Financial Statement Analysis 13th Edition Gibson Test BankDocument35 pagesFull Download Financial Statement Analysis 13th Edition Gibson Test Bankjulianwellsueiy100% (42)

- Availability and Dependencies of Scope ItemsDocument33 pagesAvailability and Dependencies of Scope ItemsfaridazziNo ratings yet

- TLSU Prospectus 10Document56 pagesTLSU Prospectus 10manish.kumar.i360No ratings yet

- Ias 23Document6 pagesIas 23faridaNo ratings yet

- Bookkeeping Is The Recording of Financial Transactions. Transactions Include SalesDocument247 pagesBookkeeping Is The Recording of Financial Transactions. Transactions Include SalesSantosh PanigrahiNo ratings yet

- Useful Reports Tcode in SAP FIDocument2 pagesUseful Reports Tcode in SAP FIfaiqalikhanNo ratings yet

- Kelompok 8 - Tugas Audit SimulationDocument68 pagesKelompok 8 - Tugas Audit SimulationDhimas Satria WirakusumaNo ratings yet

- Acc 109 p2 Quiz Statement of Comprehensive IncomeDocument11 pagesAcc 109 p2 Quiz Statement of Comprehensive IncomeRonel CastillonNo ratings yet

- ACCO 30043 Auditing and Assurance Principles - Course SyllabusDocument6 pagesACCO 30043 Auditing and Assurance Principles - Course Syllabusadulusman501No ratings yet

- Tugas Personal Ke-1 Week 2: Soal 1Document14 pagesTugas Personal Ke-1 Week 2: Soal 1meifangNo ratings yet

- BPP Publishing ACCA 2017 Studying Materials: Study Text Practice & Revision KitDocument4 pagesBPP Publishing ACCA 2017 Studying Materials: Study Text Practice & Revision KitYasir AliNo ratings yet

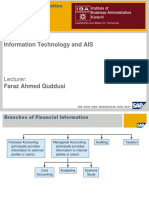

- Role of AISDocument20 pagesRole of AISFaraz Ahmed QuddusiNo ratings yet

- Junior Philippine Institute of Accountants: Cagayan State University ChapterDocument9 pagesJunior Philippine Institute of Accountants: Cagayan State University ChapterYatots Kulet EslabonNo ratings yet

- Módulo 31: Hiperinflación: Fundación IFRS: Material de Formación Sobre La NIIFDocument45 pagesMódulo 31: Hiperinflación: Fundación IFRS: Material de Formación Sobre La NIIFAnna ReyesNo ratings yet

- Accounting For Managers - FinalDocument21 pagesAccounting For Managers - FinalAnuj SharmaNo ratings yet

- Auditing in A Computerized EnvironmentDocument15 pagesAuditing in A Computerized EnvironmentSed Reyes100% (1)

- ACC Chapter 8 QuestionsDocument12 pagesACC Chapter 8 Questionsmasud.mily06No ratings yet

Download as pdf or txt

You might also like

- Section 8.1 Review Questions (Page 275)Document65 pagesSection 8.1 Review Questions (Page 275)CJ Ngo100% (13)

- CH 06 SMDocument94 pagesCH 06 SMapi-234680678No ratings yet

- CH 5 - AdjustmentsDocument24 pagesCH 5 - Adjustmentsmuhamad elmiNo ratings yet

- Competency - Based HRD System in Public Service: 1 Hilario P. MartinezDocument142 pagesCompetency - Based HRD System in Public Service: 1 Hilario P. MartinezJewel AnggoyNo ratings yet

- Aimt ProspectusDocument40 pagesAimt ProspectusdustydiamondNo ratings yet

- Depreciation: Submitted By: Abhilasha Lovepreet Parul Sunira TarrunnumDocument31 pagesDepreciation: Submitted By: Abhilasha Lovepreet Parul Sunira TarrunnumnimrandNo ratings yet

- IPPTChap010 1Document38 pagesIPPTChap010 1JackNo ratings yet

- 2019 PES Accounting Unit 4 Outcome 1 Set 1 Solution FINALDocument9 pages2019 PES Accounting Unit 4 Outcome 1 Set 1 Solution FINALLachlan McFarlandNo ratings yet

- Acct225 Cap3Document17 pagesAcct225 Cap3devoflashNo ratings yet

- Modul 04 - Dilutive Securities and Earning Per ShareDocument4 pagesModul 04 - Dilutive Securities and Earning Per ShareHilma Nahla SawalyaNo ratings yet

- Depreciation-2Document9 pagesDepreciation-2divya shindeNo ratings yet

- Module 5 Answer KeysDocument5 pagesModule 5 Answer KeysJaspreetNo ratings yet

- L.T. LiabilitiesDocument18 pagesL.T. LiabilitiesNaeemullah baigNo ratings yet

- Accrual & PrepaymentsDocument4 pagesAccrual & PrepaymentsronstarcaristaNo ratings yet

- Bài tập C3Document10 pagesBài tập C3Khanh LêNo ratings yet

- L T +liabilitiesDocument18 pagesL T +liabilitiesTaha EjazNo ratings yet

- A A P F S: Djusting Ccounts AND Reparing Inancial TatementsDocument39 pagesA A P F S: Djusting Ccounts AND Reparing Inancial TatementsBoo LeNo ratings yet

- DepreciationDocument9 pagesDepreciationPriyank JainNo ratings yet

- L.T. LiabilitiesDocument18 pagesL.T. LiabilitiesMustafa Bin ShakeelNo ratings yet

- F3 - ACCA Chapter-10-1Document18 pagesF3 - ACCA Chapter-10-1Nile NguyenNo ratings yet

- E3-5 (LO 3) Adjusting Entries: InstructionsDocument6 pagesE3-5 (LO 3) Adjusting Entries: InstructionsAntonios Fahed0% (1)

- Adilah Aprilia - 4122201115 - AkuntansiDocument11 pagesAdilah Aprilia - 4122201115 - AkuntansiDava SyafriandanaNo ratings yet

- Topic 7 - Tutorial SolutionsDocument25 pagesTopic 7 - Tutorial SolutionsnaboumilikaNo ratings yet

- Accounts Compiler by Rahul Malkan Sir-73-98Document26 pagesAccounts Compiler by Rahul Malkan Sir-73-98sanketNo ratings yet

- ACCT 1026 Lesson 8Document7 pagesACCT 1026 Lesson 8Daniel MadarangNo ratings yet

- Investment Accounts: Basic ConceptsDocument13 pagesInvestment Accounts: Basic ConceptsDebasis KarNo ratings yet

- Tutorial Letter 202/1/2020: Financial Accounting Principles For Law PractitionersDocument9 pagesTutorial Letter 202/1/2020: Financial Accounting Principles For Law Practitionersall green associatesNo ratings yet

- Kts g11 - Principles of Accounts Final AdjustmentsDocument16 pagesKts g11 - Principles of Accounts Final AdjustmentsBupe Banda100% (1)

- Introduction To Financial Modelling: Purpose Steps For Building A Financial ModelDocument22 pagesIntroduction To Financial Modelling: Purpose Steps For Building A Financial ModelAnubhavNo ratings yet

- Assignment 1 - Financial Accounting - January 21Document3 pagesAssignment 1 - Financial Accounting - January 21Ednalyn PascualNo ratings yet

- Chapter 2 (Mathematical)Document9 pagesChapter 2 (Mathematical)Sabbir HossainNo ratings yet

- ACC - Chapter 11Document29 pagesACC - Chapter 11Le Pham Khanh Ha (K17 HCM)No ratings yet

- Aol AccDocument19 pagesAol AccANGELYCA LAURANo ratings yet

- Midterm AccountingDocument28 pagesMidterm Accountingk61.2213520037No ratings yet

- IF2 - Project 1 Solution PDFDocument9 pagesIF2 - Project 1 Solution PDFBillNo ratings yet

- Acc 201 CH3Document7 pagesAcc 201 CH3Trickster TwelveNo ratings yet

- Accruals and PrepaymentsDocument28 pagesAccruals and Prepaymentsvpq7qcwszyNo ratings yet

- 5 Investment AccountsDocument11 pages5 Investment AccountsBAZINGANo ratings yet

- Question On Financial Instruments - Part 1Document9 pagesQuestion On Financial Instruments - Part 1pratikdubey9586No ratings yet

- DepreciationDocument18 pagesDepreciationManuthi HewawasamNo ratings yet

- Acct101-3 - (Your Name)Document9 pagesAcct101-3 - (Your Name)Vedanshi BihaniNo ratings yet

- Fra 3Document7 pagesFra 3Subhajyoti MukhopadhyayNo ratings yet

- Adjusting Entries Pt. BerkahDocument3 pagesAdjusting Entries Pt. Berkahmogi ertantoNo ratings yet

- Depreciation Worksheet Straightline MethodDocument12 pagesDepreciation Worksheet Straightline MethodJamie-Lee O'ConnorNo ratings yet

- Depreciation Research WorkDocument7 pagesDepreciation Research Workgargbhavika875No ratings yet

- Lecture Discussion Final On Adjusting Entries From Accrual To Inventory AdjustmentDocument39 pagesLecture Discussion Final On Adjusting Entries From Accrual To Inventory AdjustmentGarp BarrocaNo ratings yet

- Q.3-Question and SolutionDocument4 pagesQ.3-Question and SolutionFIROZ KHANNo ratings yet

- RERETESTDocument4 pagesRERETESTshveta0% (1)

- KZN 2019 Prelim MemoDocument17 pagesKZN 2019 Prelim Memotshegofatsosekgothe299No ratings yet

- Udocz Inc Monthly Treasury 2023 10Document9 pagesUdocz Inc Monthly Treasury 2023 10Carlos EffioNo ratings yet

- Bsa Lecture Discussion On AccrualsDocument8 pagesBsa Lecture Discussion On AccrualsGarp BarrocaNo ratings yet

- Jimenez, Angel Kaye October 8, 2020 Bsa 2 Year ACC 216 9:45-11:45 Assignment-Depreciation MethodsDocument4 pagesJimenez, Angel Kaye October 8, 2020 Bsa 2 Year ACC 216 9:45-11:45 Assignment-Depreciation MethodsAngel Kaye Nacionales JimenezNo ratings yet

- Unit 2 - Accountingformanager - AnanduDocument52 pagesUnit 2 - Accountingformanager - Ananducraziestidiot31No ratings yet

- Chapter 11Document65 pagesChapter 11Duong Duc Ngoc (K17 HL)No ratings yet

- Q5 Partnership Final Accs QuestionsDocument2 pagesQ5 Partnership Final Accs QuestionsIsha KatiyarNo ratings yet

- Adjustment and Closing Entry-SolutionDocument3 pagesAdjustment and Closing Entry-SolutionSerazul Arafin MrinmoyNo ratings yet

- DepreciationDocument3 pagesDepreciationSarath kumar CNo ratings yet

- Depreciation Provision ReservesDocument60 pagesDepreciation Provision ReservesjonesmbNo ratings yet

- University of Cambridge International Examinations General Certificate of Education Advanced Subsidiary Level and Advanced LevelDocument12 pagesUniversity of Cambridge International Examinations General Certificate of Education Advanced Subsidiary Level and Advanced LevelSamin IslamNo ratings yet

- m7 - Note Sample Problems With Solutions Chs 14 and 15Document6 pagesm7 - Note Sample Problems With Solutions Chs 14 and 15Marie Fe GullesNo ratings yet

- Working Paper - PropertyDocument34 pagesWorking Paper - Propertyjahidemam10No ratings yet

- 4 - Test 4 SolutionDocument7 pages4 - Test 4 SolutionAashika SamaiyaNo ratings yet

- Comprehension Questions: 1. What Are Minimum Lease Payments'?Document13 pagesComprehension Questions: 1. What Are Minimum Lease Payments'?Amit ShuklaNo ratings yet

- Enhanced Cooperation and Integration Between Indonesia and Timor-Leste: Scoping StudyFrom EverandEnhanced Cooperation and Integration Between Indonesia and Timor-Leste: Scoping StudyNo ratings yet

- 06 Genome Assembly 1Document26 pages06 Genome Assembly 1Sabbir HossainNo ratings yet

- 07 Read MappingDocument75 pages07 Read MappingSabbir HossainNo ratings yet

- MYSQL DDL COMMANDS v3 (Updated)Document20 pagesMYSQL DDL COMMANDS v3 (Updated)Sabbir HossainNo ratings yet

- 13 (Sabbir) Cross-Disciplinary Perspectives On Meta-Learning For Algorithm SelectionDocument25 pages13 (Sabbir) Cross-Disciplinary Perspectives On Meta-Learning For Algorithm SelectionSabbir HossainNo ratings yet

- Low Cost Comparisons File CopiesDocument7 pagesLow Cost Comparisons File CopiesSabbir HossainNo ratings yet

- ADVACC JOINT ARRANGEMENT PART 2 PRE-FINAL (Autosaved)Document45 pagesADVACC JOINT ARRANGEMENT PART 2 PRE-FINAL (Autosaved)Christine Joyce MagoteNo ratings yet

- AF102 Assignemnt - Group 4 (7533)Document10 pagesAF102 Assignemnt - Group 4 (7533)Anjali PrasadNo ratings yet

- Accounts InternalDocument6 pagesAccounts Internalaarav balujaNo ratings yet

- BK 16M BoeDocument5 pagesBK 16M BoeMushir LariNo ratings yet

- TRUE FALSE SCANNER by NahtaDocument88 pagesTRUE FALSE SCANNER by NahtaHimanshu RayNo ratings yet

- Deepti CVDocument2 pagesDeepti CVDeeptiNo ratings yet

- Advanced Financial Accounting and Reporting G.P. Costa Installment SalesDocument6 pagesAdvanced Financial Accounting and Reporting G.P. Costa Installment SalesmkNo ratings yet

- Quantity Cutting Department Assembly Department Packaging DepartmentDocument6 pagesQuantity Cutting Department Assembly Department Packaging DepartmentElaine Fiona VillafuerteNo ratings yet

- Disha MehtaDocument2 pagesDisha Mehtaapi-72678201No ratings yet

- Full Download Financial Statement Analysis 13th Edition Gibson Test BankDocument35 pagesFull Download Financial Statement Analysis 13th Edition Gibson Test Bankjulianwellsueiy100% (42)

- Availability and Dependencies of Scope ItemsDocument33 pagesAvailability and Dependencies of Scope ItemsfaridazziNo ratings yet

- TLSU Prospectus 10Document56 pagesTLSU Prospectus 10manish.kumar.i360No ratings yet

- Ias 23Document6 pagesIas 23faridaNo ratings yet

- Bookkeeping Is The Recording of Financial Transactions. Transactions Include SalesDocument247 pagesBookkeeping Is The Recording of Financial Transactions. Transactions Include SalesSantosh PanigrahiNo ratings yet

- Useful Reports Tcode in SAP FIDocument2 pagesUseful Reports Tcode in SAP FIfaiqalikhanNo ratings yet

- Kelompok 8 - Tugas Audit SimulationDocument68 pagesKelompok 8 - Tugas Audit SimulationDhimas Satria WirakusumaNo ratings yet

- Acc 109 p2 Quiz Statement of Comprehensive IncomeDocument11 pagesAcc 109 p2 Quiz Statement of Comprehensive IncomeRonel CastillonNo ratings yet

- ACCO 30043 Auditing and Assurance Principles - Course SyllabusDocument6 pagesACCO 30043 Auditing and Assurance Principles - Course Syllabusadulusman501No ratings yet

- Tugas Personal Ke-1 Week 2: Soal 1Document14 pagesTugas Personal Ke-1 Week 2: Soal 1meifangNo ratings yet

- BPP Publishing ACCA 2017 Studying Materials: Study Text Practice & Revision KitDocument4 pagesBPP Publishing ACCA 2017 Studying Materials: Study Text Practice & Revision KitYasir AliNo ratings yet

- Role of AISDocument20 pagesRole of AISFaraz Ahmed QuddusiNo ratings yet

- Junior Philippine Institute of Accountants: Cagayan State University ChapterDocument9 pagesJunior Philippine Institute of Accountants: Cagayan State University ChapterYatots Kulet EslabonNo ratings yet

- Módulo 31: Hiperinflación: Fundación IFRS: Material de Formación Sobre La NIIFDocument45 pagesMódulo 31: Hiperinflación: Fundación IFRS: Material de Formación Sobre La NIIFAnna ReyesNo ratings yet

- Accounting For Managers - FinalDocument21 pagesAccounting For Managers - FinalAnuj SharmaNo ratings yet

- Auditing in A Computerized EnvironmentDocument15 pagesAuditing in A Computerized EnvironmentSed Reyes100% (1)

- ACC Chapter 8 QuestionsDocument12 pagesACC Chapter 8 Questionsmasud.mily06No ratings yet