Download as pdf or txt

You might also like

- Olympus Mju-1 Parts ListDocument8 pagesOlympus Mju-1 Parts ListMalaNo ratings yet

- Sydney Basin Visual Pilot GuideDocument0 pagesSydney Basin Visual Pilot Guidephilridley2No ratings yet

- The Gebusi - Chapter 3Document14 pagesThe Gebusi - Chapter 3Bob Jiggins67% (3)

- Vat Exempt SalesDocument4 pagesVat Exempt SalesEmma Mariz GarciaNo ratings yet

- 424a 2016Document5 pages424a 2016IrsyadnurJ.MargiantoNo ratings yet

- Green and Yellow Classic English Literature Timeline Period InfographicsDocument4 pagesGreen and Yellow Classic English Literature Timeline Period InfographicsMary Mia CenizaNo ratings yet

- Output VatDocument9 pagesOutput Vatyatot carbonelNo ratings yet

- (Reviewer) TaxDocument13 pages(Reviewer) TaxchxrlttxNo ratings yet

- Business Taxation VATDocument4 pagesBusiness Taxation VATMeejhay Leigh BarnedoNo ratings yet

- Vat Exempt TransactionDocument7 pagesVat Exempt TransactionFatima Zaida JahaniNo ratings yet

- Tax.2905 Vat.Document20 pagesTax.2905 Vat.Rodge GabayoyoNo ratings yet

- VAT ExemptionsDocument2 pagesVAT ExemptionsReena MaNo ratings yet

- Vat NotesDocument11 pagesVat NotesStephen CabalteraNo ratings yet

- vat exemptionDocument2 pagesvat exemptiontmiss5461No ratings yet

- VAT Exempt TransactionsDocument10 pagesVAT Exempt TransactionsAce Hulsey TevesNo ratings yet

- To Print TaxDocument13 pagesTo Print TaxVee SyNo ratings yet

- Module 1.1 - VAT Review Notes and ExercisesDocument19 pagesModule 1.1 - VAT Review Notes and ExercisesJann Exequiel FranciscoNo ratings yet

- Accountancy Review Center (ARC) of The Philippines Inc.: Student HandoutsDocument14 pagesAccountancy Review Center (ARC) of The Philippines Inc.: Student HandoutsdasdsadsadasdasdNo ratings yet

- 04 Vat Exempt TransactionsDocument4 pages04 Vat Exempt TransactionsJaneLayugCabacunganNo ratings yet

- A. Nature and Characteristics of VATDocument4 pagesA. Nature and Characteristics of VATKIAN AGEASNo ratings yet

- Vat Exempt Transactions: Page 3 of 6Document4 pagesVat Exempt Transactions: Page 3 of 6Lei Anne GatdulaNo ratings yet

- VAT Exempt VATZeroDocument26 pagesVAT Exempt VATZeroJohn RellonNo ratings yet

- 6 VatDocument159 pages6 VatClaire diane CraveNo ratings yet

- TAX-302 (VAT-Exempt Transactions) PDFDocument5 pagesTAX-302 (VAT-Exempt Transactions) PDFclara san miguelNo ratings yet

- Introduction To Business Taxation, Exclusions and Other Percentage TaxDocument20 pagesIntroduction To Business Taxation, Exclusions and Other Percentage TaxDharel GannabanNo ratings yet

- Added: ValueDocument49 pagesAdded: ValueFearl Hazel Languido BerongesNo ratings yet

- Section 109 Should Be Read in Relation To Section 116Document5 pagesSection 109 Should Be Read in Relation To Section 116Stephanie LopezNo ratings yet

- TAX 302 VAT Exempt Transactions 1Document6 pagesTAX 302 VAT Exempt Transactions 1Jeen JeenNo ratings yet

- Services Importation Sale Other TransactionsDocument4 pagesServices Importation Sale Other TransactionsKaye Alyssa EnriquezNo ratings yet

- Tax 30222Document5 pagesTax 30222Ronariza BondocNo ratings yet

- Sec. 109 VAT Exempt TransactionsDocument2 pagesSec. 109 VAT Exempt TransactionsDis Cat100% (1)

- TAX-302 (VAT-Exempt Transactions)Document7 pagesTAX-302 (VAT-Exempt Transactions)Edith DalidaNo ratings yet

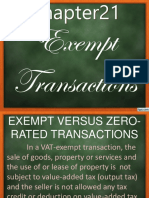

- Chapter21 1Document13 pagesChapter21 1Rachel Pepito BaladjayNo ratings yet

- Bus Tax Chap 2Document11 pagesBus Tax Chap 2David LijaucoNo ratings yet

- 12 Value Added Taxes 1Document91 pages12 Value Added Taxes 1Vince ManahanNo ratings yet

- VAT-Exempt TransactionsDocument38 pagesVAT-Exempt TransactionsAkemiNo ratings yet

- Exempt Sale of Goods Properties and Services NotesDocument2 pagesExempt Sale of Goods Properties and Services NotesSelene DimlaNo ratings yet

- Vat HandoutsDocument7 pagesVat HandoutsjulsNo ratings yet

- MODULE 2 Value Added TaxDocument21 pagesMODULE 2 Value Added TaxLenson NatividadNo ratings yet

- Taxation TableDocument35 pagesTaxation TablePRINCESS MAGPATOCNo ratings yet

- Chapter 4Document3 pagesChapter 4Marinelle DiazNo ratings yet

- VatDocument7 pagesVatCharla SuanNo ratings yet

- Value-Added-Tax-Business-Taxation WordDocument32 pagesValue-Added-Tax-Business-Taxation WordAlex Buzarang SubradoNo ratings yet

- VALUE ADDED TAX ModuleDocument12 pagesVALUE ADDED TAX ModuleAngela VecinoNo ratings yet

- Tax 302 - Vat-Exempt TransactionsDocument6 pagesTax 302 - Vat-Exempt TransactionsiBEAYNo ratings yet

- Bsa2105 FS2021 Vat Da22412Document7 pagesBsa2105 FS2021 Vat Da22412ela kikayNo ratings yet

- Chapter 5.0 Value Added Tax Percentage TaxesDocument14 pagesChapter 5.0 Value Added Tax Percentage TaxesDerick Ocampo Fulgencio0% (1)

- B. Introduction To VAT FinalDocument102 pagesB. Introduction To VAT FinalNatalie SerranoNo ratings yet

- Value Added Tax NotesDocument6 pagesValue Added Tax NotesPatrickHidalgoNo ratings yet

- TAXATION 2 Chapter 9 Exempt SalesDocument5 pagesTAXATION 2 Chapter 9 Exempt SalesKim Cristian MaañoNo ratings yet

- Vat Exempt SalesDocument8 pagesVat Exempt SalesGelai AtienzaNo ratings yet

- VAT Group 3Document39 pagesVAT Group 3Andrea GranilNo ratings yet

- VatDocument13 pagesVatJohn Derek GarreroNo ratings yet

- Tax Consequences: No Output Tax Allowed and Seller IsDocument12 pagesTax Consequences: No Output Tax Allowed and Seller IsXerez SingsonNo ratings yet

- Value Added Tax: A. Business TaxesDocument3 pagesValue Added Tax: A. Business TaxesNerish PlazaNo ratings yet

- Lesson 9Document22 pagesLesson 9Iris Lavigne RojoNo ratings yet

- VATDocument12 pagesVATIngrid VerasNo ratings yet

- 4 VAT ExemptionsDocument28 pages4 VAT ExemptionsMobile LegendsNo ratings yet

- VAT Exempt Transactions and ServicesDocument19 pagesVAT Exempt Transactions and ServicesJane Ibale CarbonquilloNo ratings yet

- LawDocument43 pagesLawMARIANo ratings yet

- Ch02 Value-Added TaxDocument22 pagesCh02 Value-Added TaxRenelyn FiloteoNo ratings yet

- CHAPTER 1 Part 2Document3 pagesCHAPTER 1 Part 2Marinelle DiazNo ratings yet

- A Treatise on Indian Transfer Pricing Regulations - Part II: A Treatise on Indian Transfer Pricing Regulations, #2From EverandA Treatise on Indian Transfer Pricing Regulations - Part II: A Treatise on Indian Transfer Pricing Regulations, #2No ratings yet

- Lesson 2 AasiDocument1 pageLesson 2 Aasidin matanguihanNo ratings yet

- STCM 04 Ge CVPDocument2 pagesSTCM 04 Ge CVPdin matanguihanNo ratings yet

- Lesson 5 BtaxDocument6 pagesLesson 5 Btaxdin matanguihanNo ratings yet

- STCM 03AbsorptionandVariableCostingDocument5 pagesSTCM 03AbsorptionandVariableCostingdin matanguihanNo ratings yet

- Lesson 4 BtaxDocument4 pagesLesson 4 Btaxdin matanguihanNo ratings yet

- Atomic Model Comparison SheetDocument2 pagesAtomic Model Comparison SheetEamon BarkhordarianNo ratings yet

- E-12 Rudder Angle System Sperry RAI PDFDocument116 pagesE-12 Rudder Angle System Sperry RAI PDFAlexandra DuduNo ratings yet

- Throw Training ProgramDocument3 pagesThrow Training ProgramSir Manny100% (1)

- Kitchen SAfety Power Point ComDocument38 pagesKitchen SAfety Power Point CombibubhaskarNo ratings yet

- Ayurvedic Herb - EKSHUDocument4 pagesAyurvedic Herb - EKSHUSanjay PisharodiNo ratings yet

- BWSC - Cylinder Liner Monitoring System - 10 0110Document4 pagesBWSC - Cylinder Liner Monitoring System - 10 0110shankar ganesh vadivelNo ratings yet

- 2013 ASA Guidelines Difficult AirwayDocument20 pages2013 ASA Guidelines Difficult AirwayStacey WoodsNo ratings yet

- Pidari Lounge Menu 2021Document21 pagesPidari Lounge Menu 2021Akta SektiawanNo ratings yet

- THE BANAO BODONG ASSOCIATION (BBA) SMALL SCALE GOLD MINING IN GA-ANG MINES TALALANG, BALBALAN KALINGA CAR, PHILIPPINES by ROYCE LINGBAWANDocument22 pagesTHE BANAO BODONG ASSOCIATION (BBA) SMALL SCALE GOLD MINING IN GA-ANG MINES TALALANG, BALBALAN KALINGA CAR, PHILIPPINES by ROYCE LINGBAWANpopsky100% (1)

- Mikyas. 2020. Positive Science or Interpretive UnderstandingDocument16 pagesMikyas. 2020. Positive Science or Interpretive UnderstandingMikyas AberaNo ratings yet

- KasaysayanDocument12 pagesKasaysayanJoed RodriguezNo ratings yet

- Annual Barangay Youth Investment Plan (Abyip)Document5 pagesAnnual Barangay Youth Investment Plan (Abyip)Rhyss Malinao BurandayNo ratings yet

- Carbon Footprint ClubDocument25 pagesCarbon Footprint ClubRaviNo ratings yet

- Alfonso Lopez CardiovascularDocument15 pagesAlfonso Lopez Cardiovascularjaniceli0207100% (1)

- Visual-Vestibular Interaction and Treatment of Dizziness: A Case ReportDocument5 pagesVisual-Vestibular Interaction and Treatment of Dizziness: A Case ReportsoumenNo ratings yet

- Stress Analyses Around Holes in Composite Laminates Using Boundary Element MethodDocument10 pagesStress Analyses Around Holes in Composite Laminates Using Boundary Element MethodpdhurveyNo ratings yet

- Nitriding & Nitrocarburising: Mikael Fällström Bodycote AGI NEEDocument51 pagesNitriding & Nitrocarburising: Mikael Fällström Bodycote AGI NEEPushparaj Vignesh100% (1)

- ESE 2022 CE Questions With Detailed SolutionsDocument44 pagesESE 2022 CE Questions With Detailed SolutionsamirNo ratings yet

- Quiz 2 PDFDocument7 pagesQuiz 2 PDFRuth Montebon0% (1)

- Electrostatic Work, Potential Energy, and Potential Electrostatic WorkDocument22 pagesElectrostatic Work, Potential Energy, and Potential Electrostatic WorkwonuNo ratings yet

- United States Patent (10) Patent No.: US 9,024.815 B2Document13 pagesUnited States Patent (10) Patent No.: US 9,024.815 B2Daniela ScobarNo ratings yet

- A Wanderer in Holland by Lucas, E. V. (Edward Verrall), 1868-1938Document251 pagesA Wanderer in Holland by Lucas, E. V. (Edward Verrall), 1868-1938Gutenberg.orgNo ratings yet

- FASE II - Tema 7Document27 pagesFASE II - Tema 7Angela MelgarNo ratings yet

- Home AutoDocument9 pagesHome AutoAlokNo ratings yet

- HBM RTN Datasheet UsaDocument4 pagesHBM RTN Datasheet UsaAntony Stip Flores TorresNo ratings yet

- All India Aakash Test Series For NEET - 2021 TEST - 6 (Code-C)Document32 pagesAll India Aakash Test Series For NEET - 2021 TEST - 6 (Code-C)Kavyatharsheni S XI-B 46No ratings yet