Download as pdf or txt

You might also like

- Climbers Scale BP HeadquartersDocument69 pagesClimbers Scale BP HeadquartersProtect Florida's BeachesNo ratings yet

- Upstream Services Market Overview 2008 2012Document33 pagesUpstream Services Market Overview 2008 2012Rudy Azwa ShafryNo ratings yet

- Petroleum in IndiaDocument70 pagesPetroleum in IndiaasthapriyamvadaNo ratings yet

- U.S. Biodiesel Industry Update: J. Alan Weber Biodiesel Congress Novotel Center Norte September 1, 2009 Sao Paulo, BrazilDocument40 pagesU.S. Biodiesel Industry Update: J. Alan Weber Biodiesel Congress Novotel Center Norte September 1, 2009 Sao Paulo, Brazilapi-19735310No ratings yet

- EOR-chapter 1 (Ver 1) (5051307)Document181 pagesEOR-chapter 1 (Ver 1) (5051307)KoushikNo ratings yet

- Huft Products Analysis Asian Markets A PR 05Document140 pagesHuft Products Analysis Asian Markets A PR 05bdrepublicadominicana2020No ratings yet

- International Energy Prices and Latin America LPG MarketsDocument39 pagesInternational Energy Prices and Latin America LPG Marketsbirna_01No ratings yet

- Energy: A Global Scan From Bangladesh Perspective: Mohammad TamimDocument59 pagesEnergy: A Global Scan From Bangladesh Perspective: Mohammad TamimRashidul Islam MasumNo ratings yet

- As G Kuala LumpurDocument23 pagesAs G Kuala LumpurYawanda Andhika PutraNo ratings yet

- February 26: Reading Tanker Tea LeavesDocument1 pageFebruary 26: Reading Tanker Tea LeavesSandesh GhandatNo ratings yet

- PRES FlinthillsDocument12 pagesPRES Flinthills김도연No ratings yet

- Presentation Indianoilcorporationlimitedppt 141111050857 Conversion Gate02 1593763349 389572Document20 pagesPresentation Indianoilcorporationlimitedppt 141111050857 Conversion Gate02 1593763349 389572Harsh yadavNo ratings yet

- Biofuels Market Outlook Slide ShowDocument39 pagesBiofuels Market Outlook Slide ShowSAMYAK PANDEYNo ratings yet

- The Petroleum Engineering ProfessionDocument41 pagesThe Petroleum Engineering ProfessionFabian ArizaNo ratings yet

- Barauni Refinary PresentationDocument20 pagesBarauni Refinary PresentationraviakashmurtyNo ratings yet

- Biofuels From Farm To FuelDocument55 pagesBiofuels From Farm To FueljsbautinNo ratings yet

- Maximizing Utilization of Light Tight Oils Economics and Technology SolutionsDocument26 pagesMaximizing Utilization of Light Tight Oils Economics and Technology SolutionsM Scott GreenNo ratings yet

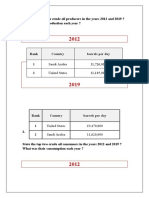

- State The Top Two Crude Oil Producers in The Years 2012 and 2019 ? What Was Their Production Each Year ?Document6 pagesState The Top Two Crude Oil Producers in The Years 2012 and 2019 ? What Was Their Production Each Year ?laoy aolNo ratings yet

- CCK Shareholder Presentation 4 28 22Document12 pagesCCK Shareholder Presentation 4 28 22Ridoy RiNo ratings yet

- 7 Colin Shelley Facts Global EnergyDocument13 pages7 Colin Shelley Facts Global EnergyIan RidzuanNo ratings yet

- Refining 2021: Who Will Be in The Game?Document13 pagesRefining 2021: Who Will Be in The Game?AgungNo ratings yet

- 3175 CokingcoalmarketsDocument10 pages3175 Cokingcoalmarketscdsswaption1979No ratings yet

- World Energy Outlook 2019: Dr. Fatih Birol, IEA Executive Director Oslo, 26 NovemberDocument14 pagesWorld Energy Outlook 2019: Dr. Fatih Birol, IEA Executive Director Oslo, 26 NovemberET163018 Khaled ArjuNo ratings yet

- Joe BennecheDocument28 pagesJoe BennecheAsad AliNo ratings yet

- Major Upcoming Upstream Projects NigeriaDocument1 pageMajor Upcoming Upstream Projects NigeriaZvonko BosnjakNo ratings yet

- Small-Scale Biodiesel ProductionDocument61 pagesSmall-Scale Biodiesel Productionsourabh1486No ratings yet

- Excise Policy 2010-11 PDFDocument13 pagesExcise Policy 2010-11 PDFSoumya TrivediNo ratings yet

- BIMBSec Corp Day - 2022 OG OutlookDocument9 pagesBIMBSec Corp Day - 2022 OG Outlookmuhammad ihsanNo ratings yet

- IEA, Oil Market Trends To 2028Document15 pagesIEA, Oil Market Trends To 2028Ananth KrishnanNo ratings yet

- JPM Oil 2030 - Long Term Incentive Oil PriceDocument54 pagesJPM Oil 2030 - Long Term Incentive Oil PriceНикита МузафаровNo ratings yet

- LNG Trends & Outlook Post Covid-19: Thursday, 11th June 2020Document25 pagesLNG Trends & Outlook Post Covid-19: Thursday, 11th June 2020Andrew XuguomingNo ratings yet

- Warade Revised Export Procedure and Documentation V6Document38 pagesWarade Revised Export Procedure and Documentation V6Omkar RanadeNo ratings yet

- Ox 3Document2 pagesOx 3Görkem ErcanNo ratings yet

- Insights Reg PlantationsDocument69 pagesInsights Reg PlantationsNasya YenitaNo ratings yet

- Insights Reg PlantationsDocument69 pagesInsights Reg PlantationsNasya YenitaNo ratings yet

- mcs2023 PotashDocument2 pagesmcs2023 PotashSolaris VeritatisNo ratings yet

- Ethanol Process FundamentalsDocument86 pagesEthanol Process FundamentalsEric NelsonNo ratings yet

- SIMULACION CME GROUP - Grupo 5 Exposiscion Hoy PorDocument21 pagesSIMULACION CME GROUP - Grupo 5 Exposiscion Hoy PoredwardNo ratings yet

- VN report-P3W1Document24 pagesVN report-P3W1Isabelle FreitasNo ratings yet

- Jam & MarmaladeDocument29 pagesJam & Marmaladeyenealem AbebeNo ratings yet

- Oil Benchmarks NY MayDocument41 pagesOil Benchmarks NY Maymbw000012378No ratings yet

- DR Mohamad Fadhil Hasan - 240306 - 170524Document23 pagesDR Mohamad Fadhil Hasan - 240306 - 170524wanikmalwakeelhasbunallahNo ratings yet

- IMO 2020 RepsolDocument29 pagesIMO 2020 RepsoledgarmerchanNo ratings yet

- Mcs2020 PotashDocument2 pagesMcs2020 PotashSolaris VeritatisNo ratings yet

- Douglas Westwood - Global Subsea Market Outlook - Kian Zi Chew PDFDocument31 pagesDouglas Westwood - Global Subsea Market Outlook - Kian Zi Chew PDFmulyadiNo ratings yet

- 2022 US Ethanol Trade Statistics Summary - RFADocument10 pages2022 US Ethanol Trade Statistics Summary - RFAcLiP FLIXNo ratings yet

- Study Id10750 Global Oil Industry and Market Statista DossierDocument44 pagesStudy Id10750 Global Oil Industry and Market Statista Dossiernivedha asokanNo ratings yet

- 2018 01 22 - Presentation - Transforming TT Natural Gas - Energy Conference 2018 - Pres Mark LoquanDocument20 pages2018 01 22 - Presentation - Transforming TT Natural Gas - Energy Conference 2018 - Pres Mark LoquanrubenpeNo ratings yet

- Mcs2022 PotashDocument2 pagesMcs2022 PotashSolaris VeritatisNo ratings yet

- UOP FCC Bitumen Processing Case StudyDocument22 pagesUOP FCC Bitumen Processing Case Studysaleh4060No ratings yet

- 2018 ICIS Africa Presentation PDFDocument17 pages2018 ICIS Africa Presentation PDFSanogo YayaNo ratings yet

- FGE-WOMR - Products Imbalances & Pressure Points, 29 June 2023Document69 pagesFGE-WOMR - Products Imbalances & Pressure Points, 29 June 2023boanzhu2001No ratings yet

- Simulacion Cme Group - Grupo 5 Exposiscion HoyDocument21 pagesSimulacion Cme Group - Grupo 5 Exposiscion HoyedwardNo ratings yet

- VC Fund Tear SheetDocument1 pageVC Fund Tear SheetVik LNo ratings yet

- Raw Materials Outlook For India: - A ReviewDocument99 pagesRaw Materials Outlook For India: - A Reviewminingnova1No ratings yet

- 2023 06 23 5 Years Forward GIBSONDocument8 pages2023 06 23 5 Years Forward GIBSONMai PhamNo ratings yet

- Education LoanDocument13 pagesEducation LoanSahilNo ratings yet

- Silicon Carbide Solid & Grains & Powders & Flour Abrasives World Summary: Market Sector Values & Financials by CountryFrom EverandSilicon Carbide Solid & Grains & Powders & Flour Abrasives World Summary: Market Sector Values & Financials by CountryNo ratings yet

- Reforms, Opportunities, and Challenges for State-Owned EnterprisesFrom EverandReforms, Opportunities, and Challenges for State-Owned EnterprisesNo ratings yet

- Imperial Power and Regional Trade: The Caribbean Basin InitiativeFrom EverandImperial Power and Regional Trade: The Caribbean Basin InitiativeNo ratings yet

- J-1996 Alternative Fuels PDFDocument1 pageJ-1996 Alternative Fuels PDFSarthak GuptaNo ratings yet

- Task 39 Implementation Agendas Report 2019 2021 UpdateDocument312 pagesTask 39 Implementation Agendas Report 2019 2021 UpdateTalha MohsinNo ratings yet

- Development of Enzymes For Biomass Degradation and Other Bioenergy Activities at NovozymesDocument13 pagesDevelopment of Enzymes For Biomass Degradation and Other Bioenergy Activities at NovozymesDuy NguyễnNo ratings yet

- Biomass Energy: Mubashir Imdad 02-134191-118 BS (CS) - 1BDocument4 pagesBiomass Energy: Mubashir Imdad 02-134191-118 BS (CS) - 1BMubashir ImdadNo ratings yet

- Oilgae Comprehensive Report On Algae FuelsDocument68 pagesOilgae Comprehensive Report On Algae Fuelsoilgae0% (1)

- Analysis of Biomass and Biofuels As Source of Energy: K. Vaideesh Subbaraj Shivendra Upadhyay M. VishwanathDocument50 pagesAnalysis of Biomass and Biofuels As Source of Energy: K. Vaideesh Subbaraj Shivendra Upadhyay M. VishwanathDicky SmartNo ratings yet

- GTL Technology Small Scale - by V.wanDocument11 pagesGTL Technology Small Scale - by V.wanDebye101No ratings yet

- Biomass Gasifica+On The Piracicaba Biosyngas Project: September 17, 2012 Dr. Fernando LandgrafDocument34 pagesBiomass Gasifica+On The Piracicaba Biosyngas Project: September 17, 2012 Dr. Fernando LandgrafAna lisbeth Galindo NogueraNo ratings yet

- BiofuelsDocument18 pagesBiofuelsAbdulsalam AbdulrahmanNo ratings yet

- Answer: Ethanol (Which Is Also Called Ethyl Alcohol or Grain Alcohol, and Abbreviated AsDocument1 pageAnswer: Ethanol (Which Is Also Called Ethyl Alcohol or Grain Alcohol, and Abbreviated Assankarsuper83No ratings yet

- Work-Order UpdateDocument75 pagesWork-Order UpdateOPARA JOSIAHNo ratings yet

- Poster Presentation Script DocumentDocument11 pagesPoster Presentation Script DocumentK.D. PatelNo ratings yet

- An Introduction To BioenergyDocument2 pagesAn Introduction To BioenergysteffenpreusserNo ratings yet

- Hydrogen: The Future Fuel: Veena.V.Parthan BL - EN.P2TSE17015Document21 pagesHydrogen: The Future Fuel: Veena.V.Parthan BL - EN.P2TSE17015Veena ParthanNo ratings yet

- Hydrogen Production and DeliveryDocument2 pagesHydrogen Production and DeliveryAnkitPatel90No ratings yet

- Biomass Resources in PakistanDocument14 pagesBiomass Resources in PakistanAmmar MohsinNo ratings yet

- BB Alternative ProcessDocument85 pagesBB Alternative ProcessMira SyafanurillahNo ratings yet

- Uhde Biomass and Coal Gasification: Fluidized Bed Entrained FlowDocument24 pagesUhde Biomass and Coal Gasification: Fluidized Bed Entrained Flowanshuman432No ratings yet

- Hydrogen Production Through Biomass Gasification in Supercritical Water: A Review From Exergy AspectDocument10 pagesHydrogen Production Through Biomass Gasification in Supercritical Water: A Review From Exergy Aspectalaa haithamNo ratings yet

- Biofuels and The Indian ScenarioDocument41 pagesBiofuels and The Indian ScenariomileyjonesNo ratings yet

- H 2 o 2Document3 pagesH 2 o 2Muzammal hoque mollahNo ratings yet

- Nila Kimia Xi IpaDocument52 pagesNila Kimia Xi IpamrizkyrameshNo ratings yet

- Lesson 1 - Introduction To BioenergyDocument12 pagesLesson 1 - Introduction To Bioenergymiss ujjanNo ratings yet

- BIOMASS: Optimal Choice For Perfect FutureDocument12 pagesBIOMASS: Optimal Choice For Perfect Futuredanea haitham abd alrahmanNo ratings yet

- Gasifikasi Biomassa Serbuk Gergaji Kayu Mahoni (Swietenia Mahagoni) Untuk Menghasilkan Bahan Bakar Gas Sebagai Sumber Energi TerbarukanDocument6 pagesGasifikasi Biomassa Serbuk Gergaji Kayu Mahoni (Swietenia Mahagoni) Untuk Menghasilkan Bahan Bakar Gas Sebagai Sumber Energi TerbarukanIndah OktavianiNo ratings yet

- GTLDocument21 pagesGTLSahil BhainsoraNo ratings yet

- Biofuels: by Group 7 - MAY 07, 2018 Mamba, Rhea Manaligod, Laica Maquera Kricel-Mae Maruquin, ElhaDocument37 pagesBiofuels: by Group 7 - MAY 07, 2018 Mamba, Rhea Manaligod, Laica Maquera Kricel-Mae Maruquin, ElhaKricel MaqueraNo ratings yet

- Bio Ethanol DBGDocument30 pagesBio Ethanol DBGGhulam RabbaniNo ratings yet

- Term Paper On Hydrogen Fuel A New HopeDocument15 pagesTerm Paper On Hydrogen Fuel A New Hopeprashant_cool_4uNo ratings yet

- Ammonia Revamp Webinar For DownloadDocument37 pagesAmmonia Revamp Webinar For Downloadtatoo1No ratings yet