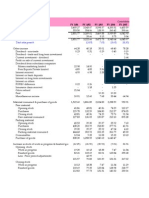

Arkema Industry Research 11th May 06-Dhj

Arkema Industry Research 11th May 06-Dhj

You might also like

- Silicone Chemistry For Fabric CareDocument8 pagesSilicone Chemistry For Fabric CareHrishikesh Dhawadshikar100% (2)

- Technical Information 1279 - Successful Use of AEROSIL® Fumed Silica in Liquid SystemsDocument12 pagesTechnical Information 1279 - Successful Use of AEROSIL® Fumed Silica in Liquid SystemsDavid RuizNo ratings yet

- 2015 Data BookDocument15 pages2015 Data BookMahathir Nur MuhammadNo ratings yet

- NeoCryl B-725 MsdsDocument3 pagesNeoCryl B-725 MsdsLeandro EsvizaNo ratings yet

- Skoog - Solucionário Capítulo 20Document21 pagesSkoog - Solucionário Capítulo 20Thais Dos SantosNo ratings yet

- ClosingTheGap AnticorrosionCoatings BasfDocument15 pagesClosingTheGap AnticorrosionCoatings Basfnsastoquep100% (1)

- Arkema - Polymer Selection Guide For Liquid ResinsDocument28 pagesArkema - Polymer Selection Guide For Liquid ResinsYoNo ratings yet

- 100 Solid Pu CoatingsDocument14 pages100 Solid Pu CoatingsSds Mani SNo ratings yet

- BASF Colourant 2005Document27 pagesBASF Colourant 2005mimjun50% (2)

- BASF Formulation Additives Product Catalog NorthAmerica PDFDocument64 pagesBASF Formulation Additives Product Catalog NorthAmerica PDFm_shahbaghiNo ratings yet

- Residual MDI in FoamDocument8 pagesResidual MDI in FoambehowardNo ratings yet

- Brand+Chimassorb Brochure Coatings+That+Stay+Looking+Good+BASF+Performance+Additives EnglishDocument32 pagesBrand+Chimassorb Brochure Coatings+That+Stay+Looking+Good+BASF+Performance+Additives EnglishvuphamMENo ratings yet

- BASF - Technical Data BrochureDocument12 pagesBASF - Technical Data BrochureJulia RodriguezNo ratings yet

- PCI June 2010Document76 pagesPCI June 2010Azouz Bouchaib100% (1)

- Arlamol LST DS-295-5 PDFDocument12 pagesArlamol LST DS-295-5 PDFsimmiNo ratings yet

- Acrylic Binders For Water-Borne Industrial CoatingsDocument12 pagesAcrylic Binders For Water-Borne Industrial CoatingsLong An DoNo ratings yet

- Rupa FlexiPOLYDocument1 pageRupa FlexiPOLYSaravvanan RajendranNo ratings yet

- Dai-El: High Performance FluoroelastomersDocument16 pagesDai-El: High Performance FluoroelastomersAtham MuhajirNo ratings yet

- Use of Hydrophobic AerosilDocument48 pagesUse of Hydrophobic AerosilHelene Di marcantonioNo ratings yet

- Acronal EDGE 4247 Premium Performance For Exterior Paint and Primer in OneDocument8 pagesAcronal EDGE 4247 Premium Performance For Exterior Paint and Primer in OneLong An DoNo ratings yet

- Acrylic and Acrylic Styrene Copolymer Dispersions by VincentzDocument3 pagesAcrylic and Acrylic Styrene Copolymer Dispersions by VincentzSetyoko AdjieNo ratings yet

- Weberfix PU - DatasheetDocument7 pagesWeberfix PU - DatasheetAnonymous PkvM83sNo ratings yet

- PigmentsDocument6 pagesPigmentsAbhinav TayadeNo ratings yet

- Shell SolDocument2 pagesShell Solpetrofacumar100% (1)

- Atomic Force Microscope (AFM) : Block Copolymer Polymer BlendDocument71 pagesAtomic Force Microscope (AFM) : Block Copolymer Polymer Blendsvo svoNo ratings yet

- Processing Aid: AdditivesDocument7 pagesProcessing Aid: AdditivestadyNo ratings yet

- PaintDocument11 pagesPaintMyo Win TheinNo ratings yet

- (Deligny P., Tuck N.) Resins For Surface Coatings. PDFDocument161 pages(Deligny P., Tuck N.) Resins For Surface Coatings. PDFAlfonso Dominguez GonzalezNo ratings yet

- Surface Water PFAS StrategyDocument38 pagesSurface Water PFAS StrategyBea ParrillaaNo ratings yet

- Deh 488 MSDS enDocument17 pagesDeh 488 MSDS enALİ ÖRSNo ratings yet

- Chap12 PDFDocument44 pagesChap12 PDFYassine OuakkiNo ratings yet

- Coatings and Inks Additive: Selection GuideDocument16 pagesCoatings and Inks Additive: Selection GuideherryNo ratings yet

- TDS 7728-6028Document2 pagesTDS 7728-6028Md. S H Maruf100% (1)

- AaaDocument8 pagesAaaAPEX SONNo ratings yet

- InTech-Unsaturated Polyester Resin For Specialty ApplicationsDocument2 pagesInTech-Unsaturated Polyester Resin For Specialty ApplicationsRAZA MEHDINo ratings yet

- Additives Solutions For FlooringDocument2 pagesAdditives Solutions For FlooringVictor CastrejonNo ratings yet

- NEI Anticorrosion Paints & Coatings BrochureDocument3 pagesNEI Anticorrosion Paints & Coatings Brochurefallen010% (1)

- Omyacarb 1TDocument1 pageOmyacarb 1TArifin HNNo ratings yet

- Primal CM 219 EF TDS PDFDocument7 pagesPrimal CM 219 EF TDS PDFAPEX SONNo ratings yet

- TDS RD 108Document2 pagesTDS RD 108APEX SONNo ratings yet

- Global Adhesives and Sealants MarketDocument2 pagesGlobal Adhesives and Sealants MarketMahesh ChaudhariNo ratings yet

- Solvent CementDocument7 pagesSolvent CementsnehaalbhalavatNo ratings yet

- 2020-Clariant Brochure High Performance Waxes For The Plastics Industry EN FinalDocument32 pages2020-Clariant Brochure High Performance Waxes For The Plastics Industry EN Finaljaviera1983No ratings yet

- Wivacryl As 50: Styrene Acrylic Paint BinderDocument7 pagesWivacryl As 50: Styrene Acrylic Paint Bindermahesh.nakNo ratings yet

- Marketing Plan AkimDocument10 pagesMarketing Plan AkimqpwoeirituyNo ratings yet

- Lamistar F 121 Geranium TWDocument9 pagesLamistar F 121 Geranium TWsilabanNo ratings yet

- CW September 2019 PDFDocument106 pagesCW September 2019 PDFLee EyannNo ratings yet

- Dicdry Ns-5210a - Ha-520b New TDSDocument2 pagesDicdry Ns-5210a - Ha-520b New TDSMohitNo ratings yet

- Lubrhophos LB-400Document14 pagesLubrhophos LB-400Gilberto GrespanNo ratings yet

- Anti-Graffiti Coating PresentationDocument22 pagesAnti-Graffiti Coating PresentationZenZen F CzoraNo ratings yet

- Safety Data Sheet: Dimethylaminopropylamine (DMAPA)Document7 pagesSafety Data Sheet: Dimethylaminopropylamine (DMAPA)harris fikrenNo ratings yet

- Polyester Based Hybrid Organic CoatingsDocument206 pagesPolyester Based Hybrid Organic CoatingsUsama AwadNo ratings yet

- Exolit AP 422Document3 pagesExolit AP 422محمد عزتNo ratings yet

- Tyzor PDFDocument11 pagesTyzor PDFDhruv SevakNo ratings yet

- Metal Carboxylates For Coatings - Driers / Siccatives: Carboxylate Acid TypesDocument10 pagesMetal Carboxylates For Coatings - Driers / Siccatives: Carboxylate Acid TypesRICHARD ODINDONo ratings yet

- Guide Formulation Sealant of 6530Document1 pageGuide Formulation Sealant of 6530ForeverNo ratings yet

- A Perspective Approach To Sustainable Routes For Non-IsocyanateDocument30 pagesA Perspective Approach To Sustainable Routes For Non-IsocyanateThaís FernandaNo ratings yet

- Manual Acrylite Injection Molding BrochureDocument36 pagesManual Acrylite Injection Molding BrochureJuan Miguel Calzada100% (1)

- The Iron Oxides: Structure, Properties, Reactions, Occurrences and UsesFrom EverandThe Iron Oxides: Structure, Properties, Reactions, Occurrences and UsesRating: 5 out of 5 stars5/5 (1)

- Self-Cleaning Materials and Surfaces: A Nanotechnology ApproachFrom EverandSelf-Cleaning Materials and Surfaces: A Nanotechnology ApproachWalid A. DaoudRating: 5 out of 5 stars5/5 (1)

- Indian Insider Buyings June 19, 2008-DhananDocument2 pagesIndian Insider Buyings June 19, 2008-Dhananapi-3702531No ratings yet

- Fem CareDocument16 pagesFem Careapi-3702531No ratings yet

- GilletteDocument14 pagesGilletteapi-3702531No ratings yet

- ColgateDocument32 pagesColgateapi-3702531No ratings yet

- Dabur IndiaDocument43 pagesDabur Indiaapi-3702531No ratings yet

- DUBARINDIAAR200708Document164 pagesDUBARINDIAAR200708Santosh KumarNo ratings yet

- BSE Special Situations 17th June 2008Document2 pagesBSE Special Situations 17th June 2008api-3702531No ratings yet

- ColgateDocument32 pagesColgateapi-3702531No ratings yet

- Colgate AR March 2005Document72 pagesColgate AR March 2005ashusingh0141No ratings yet

- India - Insider Buying 25th July 2008Document2 pagesIndia - Insider Buying 25th July 2008api-3702531No ratings yet

- Indian Insider Buyings June 17, 2008-DhananDocument2 pagesIndian Insider Buyings June 17, 2008-Dhananapi-3702531No ratings yet

- BSE Special Situations 18th June 2008Document1 pageBSE Special Situations 18th June 2008api-3702531No ratings yet

- BSE Special Situations 16th June 2008Document4 pagesBSE Special Situations 16th June 2008api-3702531No ratings yet

- Indian Insider Buyings June 13, 2008-DhananDocument2 pagesIndian Insider Buyings June 13, 2008-Dhananapi-3702531No ratings yet

- Indian Insider Buyings June 12, 2008-DhananDocument2 pagesIndian Insider Buyings June 12, 2008-Dhananapi-3702531No ratings yet

- Equilibrium Practice Test 1Document17 pagesEquilibrium Practice Test 1Carlos HfNo ratings yet

- Project Report On Integrated Unit On Fat Powder & Soya Sauce Powder, Amino Acid From (Protein Source) Plant Growth Promoters, Fruit and Vegetable Powder Like Tomato Powder, Pineapple Powder Etc.Document9 pagesProject Report On Integrated Unit On Fat Powder & Soya Sauce Powder, Amino Acid From (Protein Source) Plant Growth Promoters, Fruit and Vegetable Powder Like Tomato Powder, Pineapple Powder Etc.EIRI Board of Consultants and PublishersNo ratings yet

- A2 Level Chemistry 5.3 Transition Metals Assessed Homework: Answer All Questions Max 114 MarksDocument17 pagesA2 Level Chemistry 5.3 Transition Metals Assessed Homework: Answer All Questions Max 114 Markskingman14No ratings yet

- The Link Between Vitamin B12 and Methylmercury - A ReviewDocument5 pagesThe Link Between Vitamin B12 and Methylmercury - A ReviewOstensibleNo ratings yet

- Galata Fomrez Product GuideDocument1 pageGalata Fomrez Product Guideparijat patelNo ratings yet

- Corrosion FundamentalsDocument113 pagesCorrosion FundamentalsahmadhatakeNo ratings yet

- Organic Chemistry ReviewerDocument22 pagesOrganic Chemistry ReviewerKaren Kate LozadaNo ratings yet

- 1716 ch05Document103 pages1716 ch05parisliuhotmail.comNo ratings yet

- Uranium in North East India Atomic Minerals Division India Economic GeologyDocument4 pagesUranium in North East India Atomic Minerals Division India Economic GeologyS.Alec KnowleNo ratings yet

- Types of Reactions Guided Tutorial Spring 2015Document41 pagesTypes of Reactions Guided Tutorial Spring 2015Stefanie CorcoranNo ratings yet

- Cambridge IGCSE: Co-Ordinated Sciences 0654/42Document32 pagesCambridge IGCSE: Co-Ordinated Sciences 0654/42cpi52477No ratings yet

- Sir Humphry DavyDocument2 pagesSir Humphry DavyClaudine VelascoNo ratings yet

- SeraFastN HWDocument5 pagesSeraFastN HWArbab SkunderNo ratings yet

- Pseudohalogen and Imterhalogen CompoundsDocument9 pagesPseudohalogen and Imterhalogen CompoundsSavita ChemistryNo ratings yet

- NSEJS Previous Year Question PaperDocument16 pagesNSEJS Previous Year Question PaperUS CREATIONSNo ratings yet

- Reebol WBDocument2 pagesReebol WBVenkata RaoNo ratings yet

- Nuclear Magnetic Resonance Spectros PDFDocument310 pagesNuclear Magnetic Resonance Spectros PDFValemtinoNo ratings yet

- MSDS Baterias Sonnenschein A 600Document6 pagesMSDS Baterias Sonnenschein A 600Kingefrain Yusuke AmamiyaNo ratings yet

- Immediate Bonding Properties of Universal Adhesives To DentineDocument8 pagesImmediate Bonding Properties of Universal Adhesives To DentineDanis Diba Sabatillah YaminNo ratings yet

- Synthesis of DibenzalacetoneDocument8 pagesSynthesis of DibenzalacetoneHoai VanNo ratings yet

- Types and Classification of LipidsDocument9 pagesTypes and Classification of LipidsEdin AbolenciaNo ratings yet

- Liu 2013Document10 pagesLiu 2013Saad LHNo ratings yet

- Module 3 Instrumental Methods and NanomaterialsDocument23 pagesModule 3 Instrumental Methods and Nanomaterialsandru media workNo ratings yet

- Chemguide - Answers: H-1 NMR: Low ResolutionDocument2 pagesChemguide - Answers: H-1 NMR: Low ResolutionKhondokar TarakkyNo ratings yet

- Solution NotesDocument10 pagesSolution NotesM AroNo ratings yet

- Molecular Orbital Theory of Octahedral ComplexesDocument9 pagesMolecular Orbital Theory of Octahedral Complexesmarinogv100% (1)

- C Colours-Merged PDFDocument90 pagesC Colours-Merged PDFvinodhiniNo ratings yet

- PRACTICE MCQ HYDROCARBONS - 11ScADocument7 pagesPRACTICE MCQ HYDROCARBONS - 11ScAArda Rahmaini100% (1)

Download as doc, pdf, or txt

You might also like

- Silicone Chemistry For Fabric CareDocument8 pagesSilicone Chemistry For Fabric CareHrishikesh Dhawadshikar100% (2)

- Technical Information 1279 - Successful Use of AEROSIL® Fumed Silica in Liquid SystemsDocument12 pagesTechnical Information 1279 - Successful Use of AEROSIL® Fumed Silica in Liquid SystemsDavid RuizNo ratings yet

- 2015 Data BookDocument15 pages2015 Data BookMahathir Nur MuhammadNo ratings yet

- NeoCryl B-725 MsdsDocument3 pagesNeoCryl B-725 MsdsLeandro EsvizaNo ratings yet

- Skoog - Solucionário Capítulo 20Document21 pagesSkoog - Solucionário Capítulo 20Thais Dos SantosNo ratings yet

- ClosingTheGap AnticorrosionCoatings BasfDocument15 pagesClosingTheGap AnticorrosionCoatings Basfnsastoquep100% (1)

- Arkema - Polymer Selection Guide For Liquid ResinsDocument28 pagesArkema - Polymer Selection Guide For Liquid ResinsYoNo ratings yet

- 100 Solid Pu CoatingsDocument14 pages100 Solid Pu CoatingsSds Mani SNo ratings yet

- BASF Colourant 2005Document27 pagesBASF Colourant 2005mimjun50% (2)

- BASF Formulation Additives Product Catalog NorthAmerica PDFDocument64 pagesBASF Formulation Additives Product Catalog NorthAmerica PDFm_shahbaghiNo ratings yet

- Residual MDI in FoamDocument8 pagesResidual MDI in FoambehowardNo ratings yet

- Brand+Chimassorb Brochure Coatings+That+Stay+Looking+Good+BASF+Performance+Additives EnglishDocument32 pagesBrand+Chimassorb Brochure Coatings+That+Stay+Looking+Good+BASF+Performance+Additives EnglishvuphamMENo ratings yet

- BASF - Technical Data BrochureDocument12 pagesBASF - Technical Data BrochureJulia RodriguezNo ratings yet

- PCI June 2010Document76 pagesPCI June 2010Azouz Bouchaib100% (1)

- Arlamol LST DS-295-5 PDFDocument12 pagesArlamol LST DS-295-5 PDFsimmiNo ratings yet

- Acrylic Binders For Water-Borne Industrial CoatingsDocument12 pagesAcrylic Binders For Water-Borne Industrial CoatingsLong An DoNo ratings yet

- Rupa FlexiPOLYDocument1 pageRupa FlexiPOLYSaravvanan RajendranNo ratings yet

- Dai-El: High Performance FluoroelastomersDocument16 pagesDai-El: High Performance FluoroelastomersAtham MuhajirNo ratings yet

- Use of Hydrophobic AerosilDocument48 pagesUse of Hydrophobic AerosilHelene Di marcantonioNo ratings yet

- Acronal EDGE 4247 Premium Performance For Exterior Paint and Primer in OneDocument8 pagesAcronal EDGE 4247 Premium Performance For Exterior Paint and Primer in OneLong An DoNo ratings yet

- Acrylic and Acrylic Styrene Copolymer Dispersions by VincentzDocument3 pagesAcrylic and Acrylic Styrene Copolymer Dispersions by VincentzSetyoko AdjieNo ratings yet

- Weberfix PU - DatasheetDocument7 pagesWeberfix PU - DatasheetAnonymous PkvM83sNo ratings yet

- PigmentsDocument6 pagesPigmentsAbhinav TayadeNo ratings yet

- Shell SolDocument2 pagesShell Solpetrofacumar100% (1)

- Atomic Force Microscope (AFM) : Block Copolymer Polymer BlendDocument71 pagesAtomic Force Microscope (AFM) : Block Copolymer Polymer Blendsvo svoNo ratings yet

- Processing Aid: AdditivesDocument7 pagesProcessing Aid: AdditivestadyNo ratings yet

- PaintDocument11 pagesPaintMyo Win TheinNo ratings yet

- (Deligny P., Tuck N.) Resins For Surface Coatings. PDFDocument161 pages(Deligny P., Tuck N.) Resins For Surface Coatings. PDFAlfonso Dominguez GonzalezNo ratings yet

- Surface Water PFAS StrategyDocument38 pagesSurface Water PFAS StrategyBea ParrillaaNo ratings yet

- Deh 488 MSDS enDocument17 pagesDeh 488 MSDS enALİ ÖRSNo ratings yet

- Chap12 PDFDocument44 pagesChap12 PDFYassine OuakkiNo ratings yet

- Coatings and Inks Additive: Selection GuideDocument16 pagesCoatings and Inks Additive: Selection GuideherryNo ratings yet

- TDS 7728-6028Document2 pagesTDS 7728-6028Md. S H Maruf100% (1)

- AaaDocument8 pagesAaaAPEX SONNo ratings yet

- InTech-Unsaturated Polyester Resin For Specialty ApplicationsDocument2 pagesInTech-Unsaturated Polyester Resin For Specialty ApplicationsRAZA MEHDINo ratings yet

- Additives Solutions For FlooringDocument2 pagesAdditives Solutions For FlooringVictor CastrejonNo ratings yet

- NEI Anticorrosion Paints & Coatings BrochureDocument3 pagesNEI Anticorrosion Paints & Coatings Brochurefallen010% (1)

- Omyacarb 1TDocument1 pageOmyacarb 1TArifin HNNo ratings yet

- Primal CM 219 EF TDS PDFDocument7 pagesPrimal CM 219 EF TDS PDFAPEX SONNo ratings yet

- TDS RD 108Document2 pagesTDS RD 108APEX SONNo ratings yet

- Global Adhesives and Sealants MarketDocument2 pagesGlobal Adhesives and Sealants MarketMahesh ChaudhariNo ratings yet

- Solvent CementDocument7 pagesSolvent CementsnehaalbhalavatNo ratings yet

- 2020-Clariant Brochure High Performance Waxes For The Plastics Industry EN FinalDocument32 pages2020-Clariant Brochure High Performance Waxes For The Plastics Industry EN Finaljaviera1983No ratings yet

- Wivacryl As 50: Styrene Acrylic Paint BinderDocument7 pagesWivacryl As 50: Styrene Acrylic Paint Bindermahesh.nakNo ratings yet

- Marketing Plan AkimDocument10 pagesMarketing Plan AkimqpwoeirituyNo ratings yet

- Lamistar F 121 Geranium TWDocument9 pagesLamistar F 121 Geranium TWsilabanNo ratings yet

- CW September 2019 PDFDocument106 pagesCW September 2019 PDFLee EyannNo ratings yet

- Dicdry Ns-5210a - Ha-520b New TDSDocument2 pagesDicdry Ns-5210a - Ha-520b New TDSMohitNo ratings yet

- Lubrhophos LB-400Document14 pagesLubrhophos LB-400Gilberto GrespanNo ratings yet

- Anti-Graffiti Coating PresentationDocument22 pagesAnti-Graffiti Coating PresentationZenZen F CzoraNo ratings yet

- Safety Data Sheet: Dimethylaminopropylamine (DMAPA)Document7 pagesSafety Data Sheet: Dimethylaminopropylamine (DMAPA)harris fikrenNo ratings yet

- Polyester Based Hybrid Organic CoatingsDocument206 pagesPolyester Based Hybrid Organic CoatingsUsama AwadNo ratings yet

- Exolit AP 422Document3 pagesExolit AP 422محمد عزتNo ratings yet

- Tyzor PDFDocument11 pagesTyzor PDFDhruv SevakNo ratings yet

- Metal Carboxylates For Coatings - Driers / Siccatives: Carboxylate Acid TypesDocument10 pagesMetal Carboxylates For Coatings - Driers / Siccatives: Carboxylate Acid TypesRICHARD ODINDONo ratings yet

- Guide Formulation Sealant of 6530Document1 pageGuide Formulation Sealant of 6530ForeverNo ratings yet

- A Perspective Approach To Sustainable Routes For Non-IsocyanateDocument30 pagesA Perspective Approach To Sustainable Routes For Non-IsocyanateThaís FernandaNo ratings yet

- Manual Acrylite Injection Molding BrochureDocument36 pagesManual Acrylite Injection Molding BrochureJuan Miguel Calzada100% (1)

- The Iron Oxides: Structure, Properties, Reactions, Occurrences and UsesFrom EverandThe Iron Oxides: Structure, Properties, Reactions, Occurrences and UsesRating: 5 out of 5 stars5/5 (1)

- Self-Cleaning Materials and Surfaces: A Nanotechnology ApproachFrom EverandSelf-Cleaning Materials and Surfaces: A Nanotechnology ApproachWalid A. DaoudRating: 5 out of 5 stars5/5 (1)

- Indian Insider Buyings June 19, 2008-DhananDocument2 pagesIndian Insider Buyings June 19, 2008-Dhananapi-3702531No ratings yet

- Fem CareDocument16 pagesFem Careapi-3702531No ratings yet

- GilletteDocument14 pagesGilletteapi-3702531No ratings yet

- ColgateDocument32 pagesColgateapi-3702531No ratings yet

- Dabur IndiaDocument43 pagesDabur Indiaapi-3702531No ratings yet

- DUBARINDIAAR200708Document164 pagesDUBARINDIAAR200708Santosh KumarNo ratings yet

- BSE Special Situations 17th June 2008Document2 pagesBSE Special Situations 17th June 2008api-3702531No ratings yet

- ColgateDocument32 pagesColgateapi-3702531No ratings yet

- Colgate AR March 2005Document72 pagesColgate AR March 2005ashusingh0141No ratings yet

- India - Insider Buying 25th July 2008Document2 pagesIndia - Insider Buying 25th July 2008api-3702531No ratings yet

- Indian Insider Buyings June 17, 2008-DhananDocument2 pagesIndian Insider Buyings June 17, 2008-Dhananapi-3702531No ratings yet

- BSE Special Situations 18th June 2008Document1 pageBSE Special Situations 18th June 2008api-3702531No ratings yet

- BSE Special Situations 16th June 2008Document4 pagesBSE Special Situations 16th June 2008api-3702531No ratings yet

- Indian Insider Buyings June 13, 2008-DhananDocument2 pagesIndian Insider Buyings June 13, 2008-Dhananapi-3702531No ratings yet

- Indian Insider Buyings June 12, 2008-DhananDocument2 pagesIndian Insider Buyings June 12, 2008-Dhananapi-3702531No ratings yet

- Equilibrium Practice Test 1Document17 pagesEquilibrium Practice Test 1Carlos HfNo ratings yet

- Project Report On Integrated Unit On Fat Powder & Soya Sauce Powder, Amino Acid From (Protein Source) Plant Growth Promoters, Fruit and Vegetable Powder Like Tomato Powder, Pineapple Powder Etc.Document9 pagesProject Report On Integrated Unit On Fat Powder & Soya Sauce Powder, Amino Acid From (Protein Source) Plant Growth Promoters, Fruit and Vegetable Powder Like Tomato Powder, Pineapple Powder Etc.EIRI Board of Consultants and PublishersNo ratings yet

- A2 Level Chemistry 5.3 Transition Metals Assessed Homework: Answer All Questions Max 114 MarksDocument17 pagesA2 Level Chemistry 5.3 Transition Metals Assessed Homework: Answer All Questions Max 114 Markskingman14No ratings yet

- The Link Between Vitamin B12 and Methylmercury - A ReviewDocument5 pagesThe Link Between Vitamin B12 and Methylmercury - A ReviewOstensibleNo ratings yet

- Galata Fomrez Product GuideDocument1 pageGalata Fomrez Product Guideparijat patelNo ratings yet

- Corrosion FundamentalsDocument113 pagesCorrosion FundamentalsahmadhatakeNo ratings yet

- Organic Chemistry ReviewerDocument22 pagesOrganic Chemistry ReviewerKaren Kate LozadaNo ratings yet

- 1716 ch05Document103 pages1716 ch05parisliuhotmail.comNo ratings yet

- Uranium in North East India Atomic Minerals Division India Economic GeologyDocument4 pagesUranium in North East India Atomic Minerals Division India Economic GeologyS.Alec KnowleNo ratings yet

- Types of Reactions Guided Tutorial Spring 2015Document41 pagesTypes of Reactions Guided Tutorial Spring 2015Stefanie CorcoranNo ratings yet

- Cambridge IGCSE: Co-Ordinated Sciences 0654/42Document32 pagesCambridge IGCSE: Co-Ordinated Sciences 0654/42cpi52477No ratings yet

- Sir Humphry DavyDocument2 pagesSir Humphry DavyClaudine VelascoNo ratings yet

- SeraFastN HWDocument5 pagesSeraFastN HWArbab SkunderNo ratings yet

- Pseudohalogen and Imterhalogen CompoundsDocument9 pagesPseudohalogen and Imterhalogen CompoundsSavita ChemistryNo ratings yet

- NSEJS Previous Year Question PaperDocument16 pagesNSEJS Previous Year Question PaperUS CREATIONSNo ratings yet

- Reebol WBDocument2 pagesReebol WBVenkata RaoNo ratings yet

- Nuclear Magnetic Resonance Spectros PDFDocument310 pagesNuclear Magnetic Resonance Spectros PDFValemtinoNo ratings yet

- MSDS Baterias Sonnenschein A 600Document6 pagesMSDS Baterias Sonnenschein A 600Kingefrain Yusuke AmamiyaNo ratings yet

- Immediate Bonding Properties of Universal Adhesives To DentineDocument8 pagesImmediate Bonding Properties of Universal Adhesives To DentineDanis Diba Sabatillah YaminNo ratings yet

- Synthesis of DibenzalacetoneDocument8 pagesSynthesis of DibenzalacetoneHoai VanNo ratings yet

- Types and Classification of LipidsDocument9 pagesTypes and Classification of LipidsEdin AbolenciaNo ratings yet

- Liu 2013Document10 pagesLiu 2013Saad LHNo ratings yet

- Module 3 Instrumental Methods and NanomaterialsDocument23 pagesModule 3 Instrumental Methods and Nanomaterialsandru media workNo ratings yet

- Chemguide - Answers: H-1 NMR: Low ResolutionDocument2 pagesChemguide - Answers: H-1 NMR: Low ResolutionKhondokar TarakkyNo ratings yet

- Solution NotesDocument10 pagesSolution NotesM AroNo ratings yet

- Molecular Orbital Theory of Octahedral ComplexesDocument9 pagesMolecular Orbital Theory of Octahedral Complexesmarinogv100% (1)

- C Colours-Merged PDFDocument90 pagesC Colours-Merged PDFvinodhiniNo ratings yet

- PRACTICE MCQ HYDROCARBONS - 11ScADocument7 pagesPRACTICE MCQ HYDROCARBONS - 11ScAArda Rahmaini100% (1)