Download as pdf or txt

You might also like

- Monetary Policy ReviewDocument4 pagesMonetary Policy ReviewVishal KanojiaNo ratings yet

- Monetary Policy StatementDocument3 pagesMonetary Policy Statementvipulpandey005No ratings yet

- RBI Monetary Policy Statement - Must Read For The Class Now and TodayDocument4 pagesRBI Monetary Policy Statement - Must Read For The Class Now and TodayAnanya SharmaNo ratings yet

- RBI MPC StatementDocument3 pagesRBI MPC StatementLAKHAN TRIVEDINo ratings yet

- Governor's StatementDocument11 pagesGovernor's Statementvipulpandey005No ratings yet

- PR1043MP0Document15 pagesPR1043MP0Shivam SisodiaNo ratings yet

- RBI Governor Statement 1702090413Document9 pagesRBI Governor Statement 1702090413Jyotiraditya JadhavNo ratings yet

- PR452GOVERNORSTATEMENTJUN20296Document15 pagesPR452GOVERNORSTATEMENTJUN20296ysurjeet148No ratings yet

- Reserve Bank of India - Press ReleasesDocument4 pagesReserve Bank of India - Press ReleasesSarthak AroraNo ratings yet

- Governor's Statement - August 6, 2020: TH TH TH THDocument13 pagesGovernor's Statement - August 6, 2020: TH TH TH THThe QuintNo ratings yet

- Group 7 Current IssuesDocument15 pagesGroup 7 Current IssuesMench FranciscoNo ratings yet

- Critical Analysis GROUP-2Document6 pagesCritical Analysis GROUP-2Angelo MagtibayNo ratings yet

- BSP Monetary Policy February 2023Document2 pagesBSP Monetary Policy February 2023Durdle DurdlerNo ratings yet

- RBIBULLETINDECEMBERF7A5Document228 pagesRBIBULLETINDECEMBERF7A5investly.vruddhiNo ratings yet

- GDP Reports 2023 Till June 2023Document15 pagesGDP Reports 2023 Till June 2023Kranti TejanNo ratings yet

- Monthly Economic Review July 2023 - 1Document26 pagesMonthly Economic Review July 2023 - 1H SNo ratings yet

- Central Bank-Monetary Policy ReviewDocument6 pagesCentral Bank-Monetary Policy ReviewAda DeranaNo ratings yet

- Bandhan Debt-Market-Monthly-Outlook-Nov-2023Document3 pagesBandhan Debt-Market-Monthly-Outlook-Nov-2023Shivani NirmalNo ratings yet

- Pak Eco Monetary Policy of Pakistan SBP DataDocument44 pagesPak Eco Monetary Policy of Pakistan SBP Datarn29rww28fNo ratings yet

- SAPM CCA 1Document17 pagesSAPM CCA 1sandeshNo ratings yet

- MCIRFEBRUARY1311Document4 pagesMCIRFEBRUARY1311rohangundpatil096No ratings yet

- First Quarter Review of Monetary Policy 2012-13 Press Statement by Dr. D. SubbaraoDocument5 pagesFirst Quarter Review of Monetary Policy 2012-13 Press Statement by Dr. D. SubbaraoUttam AuddyNo ratings yet

- Monetary Policy Statement - Bank Negara Malaysia+.Document2 pagesMonetary Policy Statement - Bank Negara Malaysia+.sk tanNo ratings yet

- Untitled Document - Edited - 2024-06-09T202151.521Document4 pagesUntitled Document - Edited - 2024-06-09T202151.521kimberlyarileyNo ratings yet

- EconomyDocument4 pagesEconomypremidbi2008No ratings yet

- Summary of Macro Models and Chain of EventsDocument7 pagesSummary of Macro Models and Chain of EventsMzwandile Honono KanohiyaNo ratings yet

- 05 May Magazine 2023Document20 pages05 May Magazine 2023Majid AliNo ratings yet

- 1ASSESSMENTANDPROSPECTSDocument13 pages1ASSESSMENTANDPROSPECTSSkand UpadhyayNo ratings yet

- 0RBIBULLETIN2D1CE48Document200 pages0RBIBULLETIN2D1CE48sp78gxmfkrNo ratings yet

- Economic Survey 2023 Q44 ODocument136 pagesEconomic Survey 2023 Q44 Orambo kunjumonNo ratings yet

- Economic Survey 2022-23 GistDocument17 pagesEconomic Survey 2022-23 GistAMIT BHARDWAZNo ratings yet

- MonetaryPolicySummary February2024Document2 pagesMonetaryPolicySummary February2024Kier TabzNo ratings yet

- Third Bi-Monthly Monetary Policy Statement, 2019-20 Resolution of The Monetary Policy Committee (MPC) Reserve Bank of IndiaDocument5 pagesThird Bi-Monthly Monetary Policy Statement, 2019-20 Resolution of The Monetary Policy Committee (MPC) Reserve Bank of IndiaVineet ChoudharyNo ratings yet

- First Bi-Monthly Monetary Policy Statement, 2014-15Document8 pagesFirst Bi-Monthly Monetary Policy Statement, 2014-15FirstpostNo ratings yet

- India Monetary Policy Review 17 June 2013Document3 pagesIndia Monetary Policy Review 17 June 2013Jhunjhunwalas Digital Finance & Business Info LibraryNo ratings yet

- Financial Stability Report June 2023Document10 pagesFinancial Stability Report June 2023asdfNo ratings yet

- RBI Q3 Monetory PolicyDocument9 pagesRBI Q3 Monetory Policydeepakambulkar8166No ratings yet

- RBI Policy Review: Turning Hawkish: Normalization of Policy Corridor and Introduction of SDFDocument5 pagesRBI Policy Review: Turning Hawkish: Normalization of Policy Corridor and Introduction of SDFswapnaNo ratings yet

- EconomicsDocument21 pagesEconomicsvedha's preparationNo ratings yet

- Invesco Factsheet June 2022Document56 pagesInvesco Factsheet June 2022ADARSH GUPTANo ratings yet

- Fiscal PolicyDocument14 pagesFiscal PolicySOUMYA DEEP CHATTERJEENo ratings yet

- Mba 324 Diokno On The Economic Growth of The CountryDocument3 pagesMba 324 Diokno On The Economic Growth of The CountryMark Joseph SoreNo ratings yet

- Macro Economics and Business Environment Assignment: Submitted To: Dr. C.S. AdhikariDocument8 pagesMacro Economics and Business Environment Assignment: Submitted To: Dr. C.S. Adhikarigaurav880No ratings yet

- Economic Review 2023Document31 pagesEconomic Review 202317044 AZMAIN IKTIDER AKASHNo ratings yet

- Monthly Economic Review January 2024 - 0Document30 pagesMonthly Economic Review January 2024 - 0guru prasadNo ratings yet

- Ed - 11-08-2023Document1 pageEd - 11-08-2023Avinash Chandra RanaNo ratings yet

- South African Reserve Bank: MPC Statement 21 May 2020Document6 pagesSouth African Reserve Bank: MPC Statement 21 May 2020BusinessTechNo ratings yet

- Macro 3 AssignmentDocument16 pagesMacro 3 AssignmentHarshit RathoreNo ratings yet

- Monetary Policy ReviewDocument3 pagesMonetary Policy ReviewNikhil DambalNo ratings yet

- Assingment On Monetory Policy DecisionDocument4 pagesAssingment On Monetory Policy DecisionDebargha SenguptaNo ratings yet

- C38 Mopocb DumaicosDocument14 pagesC38 Mopocb DumaicosapellidojemimaNo ratings yet

- Macro Perspectives: Group Chief EconomistDocument3 pagesMacro Perspectives: Group Chief EconomistAbhishek SaxenaNo ratings yet

- Monthly Report May 2024Document11 pagesMonthly Report May 2024jahanzaib yasinNo ratings yet

- MPC Press Release January 2024Document7 pagesMPC Press Release January 2024smxj4zxq5hNo ratings yet

- RBI BulletinDocument118 pagesRBI Bulletintheresa.painter100% (1)

- March 2021Document15 pagesMarch 2021RajugupatiNo ratings yet

- Crux of Economic Survey 2023Document8 pagesCrux of Economic Survey 2023Raja S100% (1)

- Bangladesh Quarterly Economic Update: September 2014From EverandBangladesh Quarterly Economic Update: September 2014No ratings yet

- 5 6132145634242725799Document96 pages5 6132145634242725799TheMoneyMitraNo ratings yet

- Bloomberg Markets - Aug Sept 2022Document84 pagesBloomberg Markets - Aug Sept 2022TheMoneyMitraNo ratings yet

- Business Today, 15 May 2022Document96 pagesBusiness Today, 15 May 2022TheMoneyMitraNo ratings yet

- ET-Wealth 19-09Document24 pagesET-Wealth 19-09TheMoneyMitraNo ratings yet

- Earnings Presentation For Q1 FY 2023-24Document12 pagesEarnings Presentation For Q1 FY 2023-24TheMoneyMitraNo ratings yet

- ET-Wealth May 2-8, 2022Document24 pagesET-Wealth May 2-8, 2022TheMoneyMitraNo ratings yet

- Bill AckmanDocument729 pagesBill AckmanTheMoneyMitraNo ratings yet

- FHSK 111Document6 pagesFHSK 111TheMoneyMitraNo ratings yet

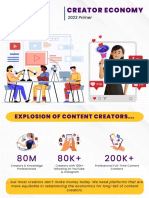

- Creator Economy Primer 2023Document10 pagesCreator Economy Primer 2023TheMoneyMitraNo ratings yet

- Mutual Fund - Monthly Report December 2021: Dhartikumar Sahu +91-22-2217 1770Document54 pagesMutual Fund - Monthly Report December 2021: Dhartikumar Sahu +91-22-2217 1770TheMoneyMitraNo ratings yet

- std.5 - Science Vacation Worksheet - 2023 PDFDocument8 pagesstd.5 - Science Vacation Worksheet - 2023 PDFTheMoneyMitraNo ratings yet

- Bio186 (Final)Document49 pagesBio186 (Final)Neill TeodoroNo ratings yet

- Synechron Corporate Apartments GuidelinesDocument4 pagesSynechron Corporate Apartments GuidelinesSree KrithNo ratings yet

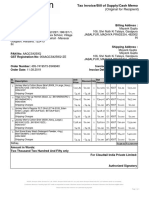

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document2 pagesTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)MAYANK GUPTANo ratings yet

- BG Construction POW.R1V6Document13 pagesBG Construction POW.R1V6Deepum HalloomanNo ratings yet

- Banking SWOT Analysis v2Document29 pagesBanking SWOT Analysis v2Chiraroj AngsumaleeNo ratings yet

- Ammonite WorksheetDocument2 pagesAmmonite WorksheetDerrick Scott FullerNo ratings yet

- TravelDocument18 pagesTravelAnna Marie De JuanNo ratings yet

- Concrete Quality Control PlanDocument5 pagesConcrete Quality Control PlanKripasindhu SamantaNo ratings yet

- IGCSE HISTORY Topic 5 - Who Was To Blame For The Cold WarDocument11 pagesIGCSE HISTORY Topic 5 - Who Was To Blame For The Cold WarAbby IuNo ratings yet

- Critical Analysis of Transgender Persons (Protection of Rights) Act, 2019Document16 pagesCritical Analysis of Transgender Persons (Protection of Rights) Act, 2019Alethea JoelleNo ratings yet

- Syllabus The Contemporary WorldDocument8 pagesSyllabus The Contemporary WorldLenicho MarquezNo ratings yet

- Research in Education HandoutsDocument4 pagesResearch in Education HandoutsJessa Quiño EscarpeNo ratings yet

- Renaissance Period in English LiteratureDocument2 pagesRenaissance Period in English LiteratureAngelNo ratings yet

- DT Ratcfull Sig 55 Sce MetaDocument3 pagesDT Ratcfull Sig 55 Sce MetaPrashant JumanalNo ratings yet

- Pe ReviewerDocument3 pagesPe Reviewerig: vrlcmNo ratings yet

- Pak-India Arms RaceDocument9 pagesPak-India Arms RacesaleembaripatujoNo ratings yet

- Bayle & Rayner (2016) Sociology of A Scandal. The Emergence of FifagateDocument20 pagesBayle & Rayner (2016) Sociology of A Scandal. The Emergence of FifagateRMADVNo ratings yet

- Noida International AirportDocument4 pagesNoida International AirportAvinash SinghNo ratings yet

- Ubud Tour Bali - Cheap Price Day TourDocument9 pagesUbud Tour Bali - Cheap Price Day TourTri RanggaNo ratings yet

- Chapter 6 FeminismDocument20 pagesChapter 6 FeminismatelierimkellerNo ratings yet

- Mahatma Gandhi BiographyDocument5 pagesMahatma Gandhi BiographyGian LuceroNo ratings yet

- Gilgit-Baltistan: Administrative TerritoryDocument12 pagesGilgit-Baltistan: Administrative TerritoryRizwan689No ratings yet

- A Bloody Conflict: Chapter 9 Section 3 US HistoryDocument27 pagesA Bloody Conflict: Chapter 9 Section 3 US HistoryEthan CombsNo ratings yet

- Notes On Cash and Cash EquivalentsDocument5 pagesNotes On Cash and Cash EquivalentsLeonoramarie BernosNo ratings yet

- Novelas Cortas, by Pedro Antonio de AlarconDocument229 pagesNovelas Cortas, by Pedro Antonio de Alarconme meNo ratings yet

- ItikaafDocument3 pagesItikaafmusarhadNo ratings yet

- Deirdre J. Wright, LICSW, ACSW P.O. Box 11302 Washington, DCDocument4 pagesDeirdre J. Wright, LICSW, ACSW P.O. Box 11302 Washington, DCdedeej100% (1)

- Church of EnglandDocument34 pagesChurch of Englandbrian2chrisNo ratings yet

- Magic Quadrant For 5G Network Infrastructure For Communications Service ProvidersDocument19 pagesMagic Quadrant For 5G Network Infrastructure For Communications Service ProvidersRazman Rashid100% (1)

- UTS Ganjil 2019Document2 pagesUTS Ganjil 2019Saepul RahmanNo ratings yet