Advanced Taxation Paper 3.3 Dec 2023

Advanced Taxation Paper 3.3 Dec 2023

You might also like

- Hammer Group SeptDec 2023Document5 pagesHammer Group SeptDec 2023Adilah AzamNo ratings yet

- Solution Manual For Analysis For Financial Management 12th EditionDocument6 pagesSolution Manual For Analysis For Financial Management 12th EditionMatthew Karaffa100% (38)

- Earthware Case 3-1 To 3-5Document10 pagesEarthware Case 3-1 To 3-5Stephanie Slaughter80% (5)

- Case Study On Gainesboro Machine Tools CorporationDocument13 pagesCase Study On Gainesboro Machine Tools Corporationemehmehmeh86% (7)

- Garage Kipkurui PatrickDocument37 pagesGarage Kipkurui PatrickCarol Soi86% (7)

- Case Interviews IntroductionsDocument6 pagesCase Interviews IntroductionsArjjun ChanderNo ratings yet

- GIS SubstationDocument13 pagesGIS SubstationDakshay BhardwajNo ratings yet

- Summative Test-FABM2 2018-19Document3 pagesSummative Test-FABM2 2018-19Raul Soriano Cabanting0% (1)

- Advanced Taxation 3.3 August 2022Document26 pagesAdvanced Taxation 3.3 August 2022Obed AsamoahNo ratings yet

- Advanced Taxation May 2021Document20 pagesAdvanced Taxation May 2021akpanyapNo ratings yet

- Financial Management Paper 2.4 July 2023Document18 pagesFinancial Management Paper 2.4 July 2023johny SahaNo ratings yet

- Tax Avoidance MeasuresDocument7 pagesTax Avoidance MeasuresOWUSU BOATENGNo ratings yet

- Course Materials TaxationDocument21 pagesCourse Materials TaxationObed AsamoahNo ratings yet

- PT April 2022Document15 pagesPT April 2022Kipson Drizo MuksNo ratings yet

- Adv Tax April 2022Document27 pagesAdv Tax April 2022Kwabena Obeng-FosuNo ratings yet

- May 2020 Professional Examinations Advanced Audit & Assurance (Paper 3.2) Chief Examiner'S Report, Questions and Marking SchemeDocument20 pagesMay 2020 Professional Examinations Advanced Audit & Assurance (Paper 3.2) Chief Examiner'S Report, Questions and Marking SchemeVonnieNo ratings yet

- May 2021 Professional Examination Financial Reporting (Paper 2.1) Chief Examiner'S Report, Questions and Marking SchemeDocument27 pagesMay 2021 Professional Examination Financial Reporting (Paper 2.1) Chief Examiner'S Report, Questions and Marking SchemeThomas nyade100% (1)

- Advanced TaxationDocument21 pagesAdvanced TaxationEMMANUEL ADJEINo ratings yet

- Taxation South Africa (TX Zaf) June 2022 Examiner's ReportDocument9 pagesTaxation South Africa (TX Zaf) June 2022 Examiner's ReportwaseNo ratings yet

- ADVANCED TAXATION PAPER 3.3nov 2023Document22 pagesADVANCED TAXATION PAPER 3.3nov 2023batuchemNo ratings yet

- Sun Home Appliances Private - R - 25082020Document7 pagesSun Home Appliances Private - R - 25082020DarshanNo ratings yet

- Q3'21 Earnings Call PresentationDocument24 pagesQ3'21 Earnings Call Presentationsl7789No ratings yet

- Caf 2 Tax Autumn 2022Document4 pagesCaf 2 Tax Autumn 2022M AHMAD MAQBOOLNo ratings yet

- International TaxationDocument9 pagesInternational TaxationOWUSU BOATENGNo ratings yet

- Analysis For Financial Management 11Th Edition Higgins Solutions Manual Full Chapter PDFDocument36 pagesAnalysis For Financial Management 11Th Edition Higgins Solutions Manual Full Chapter PDFmarcia.tays151100% (22)

- Practice Final With SolutionsDocument8 pagesPractice Final With SolutionsSammy MosesNo ratings yet

- Principles of TaxationDocument17 pagesPrinciples of TaxationEMMANUEL ADJEINo ratings yet

- Advanced Level Accounting 600102 Examiners Report November 2022Document3 pagesAdvanced Level Accounting 600102 Examiners Report November 2022jayapriscilla1No ratings yet

- Principle of TaxationDocument6 pagesPrinciple of TaxationKhurram ShahzadNo ratings yet

- Press Release Arman Q3FY21Document5 pagesPress Release Arman Q3FY21Forall PainNo ratings yet

- Accounts Receivable and Inventory ManagementDocument53 pagesAccounts Receivable and Inventory ManagementFerriza AbanNo ratings yet

- Mergers and AcquisitionsDocument4 pagesMergers and AcquisitionsOWUSU BOATENGNo ratings yet

- Tutorial 2 Questions (Chapter 1)Document3 pagesTutorial 2 Questions (Chapter 1)jiayiwang0221No ratings yet

- Examiner Comments-Summer 2012Document4 pagesExaminer Comments-Summer 2012Mahendar BhojwaniNo ratings yet

- Financial Management Papernov 2023Document21 pagesFinancial Management Papernov 2023batuchemNo ratings yet

- Earnings Conference Call: Q4 Fiscal Year 2021Document25 pagesEarnings Conference Call: Q4 Fiscal Year 2021sl7789No ratings yet

- Group 4 Assignement, Financial and Management Accounting-1Document10 pagesGroup 4 Assignement, Financial and Management Accounting-10pointsNo ratings yet

- GP FINNANCEDocument12 pagesGP FINNANCEMuhammad Aiezaqul Haikal bin ZainuriNo ratings yet

- Earnings Conference Call: Q2 Fiscal Year 2021Document24 pagesEarnings Conference Call: Q2 Fiscal Year 2021sl7789No ratings yet

- Advanced Audit AssuranceDocument24 pagesAdvanced Audit AssuranceEMMANUEL ADJEINo ratings yet

- AF208 Testbank CompiledDocument100 pagesAF208 Testbank Compileds11186706No ratings yet

- Airvision India Private Limited - R - 25082020Document7 pagesAirvision India Private Limited - R - 25082020DarshanNo ratings yet

- Cadbury Nigeria PLC 2005Document29 pagesCadbury Nigeria PLC 2005Ada TeachesNo ratings yet

- Financial Reporting Paper 2.1 Dec 2023Document28 pagesFinancial Reporting Paper 2.1 Dec 2023Oni SegunNo ratings yet

- Ratio Analysis: Mari Perolum Company LimitiedDocument5 pagesRatio Analysis: Mari Perolum Company LimitiedNuman AhmedNo ratings yet

- Assessment 2 2Document6 pagesAssessment 2 2Thảo NguyễnNo ratings yet

- Important - Read This First: Family NameDocument6 pagesImportant - Read This First: Family NameArthur MendesNo ratings yet

- Balance Sheet InterpretationDocument3 pagesBalance Sheet InterpretationAkanksha KadamNo ratings yet

- November 2016 Professional Examinations Financial Management (Paper 2.4) Chief Examiner'S Report, Questions & Marking SchemeDocument18 pagesNovember 2016 Professional Examinations Financial Management (Paper 2.4) Chief Examiner'S Report, Questions & Marking SchemeSrikrishna DharNo ratings yet

- Medical Presentation - Q2FY23Document26 pagesMedical Presentation - Q2FY23Kdp03No ratings yet

- MGT Capstone 1 - 4Document3 pagesMGT Capstone 1 - 4Shakeel SajjadNo ratings yet

- 2022 ND - FM Suggested AnswerDocument10 pages2022 ND - FM Suggested Answermiradvance studyNo ratings yet

- FM MJ20 Detailed CommentaryDocument4 pagesFM MJ20 Detailed CommentaryleylaNo ratings yet

- CF Final ReportDocument11 pagesCF Final Reporteshmalsheikh703No ratings yet

- Greenlight Capital Re Press Release 2020 Q3 FINALDocument8 pagesGreenlight Capital Re Press Release 2020 Q3 FINALJoey KlenderNo ratings yet

- Popular, Inc. Conference Call PresentationDocument24 pagesPopular, Inc. Conference Call PresentationRubén E. Morales RiveraNo ratings yet

- PRINCIPLES OF TAXATION PAPER 2.6nov 2023Document22 pagesPRINCIPLES OF TAXATION PAPER 2.6nov 2023Obed AsamoahNo ratings yet

- Greenfield Corporation Case Study Part ADocument11 pagesGreenfield Corporation Case Study Part AJay WainwrightNo ratings yet

- 208-Test-Bank-2nd-Edth s1 2019Document96 pages208-Test-Bank-2nd-Edth s1 2019MilanNo ratings yet

- Financial Management Source 1Document13 pagesFinancial Management Source 1John Llucastre CortezNo ratings yet

- CreditAccess Grameen - Investor Presentation - Q4 - FY 2021 22Document54 pagesCreditAccess Grameen - Investor Presentation - Q4 - FY 2021 22Haidir AuliaNo ratings yet

- J.K. Lasser's Small Business Taxes 2012: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2012: Your Complete Guide to a Better Bottom LineNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific: 2020 EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: 2020 EditionNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionNo ratings yet

- Book-Responsibility Actg-SolMan PDFDocument18 pagesBook-Responsibility Actg-SolMan PDFLordson RamosNo ratings yet

- Basic Accounting-RatiosDocument22 pagesBasic Accounting-RatiosSala SahariNo ratings yet

- The Economic Feasibility of An Ultra-Low Cost AirlineDocument1 pageThe Economic Feasibility of An Ultra-Low Cost AirlineTshep SekNo ratings yet

- Hospital ManagementDocument12 pagesHospital Managementvalene_elleNo ratings yet

- Ken Hackel: Slowing Economic Growth Means Greater Focus On Economic ProfitDocument4 pagesKen Hackel: Slowing Economic Growth Means Greater Focus On Economic ProfitbogatishankarNo ratings yet

- Nirlaba JawabDocument7 pagesNirlaba JawabVerel HaikalNo ratings yet

- Soal SapDocument14 pagesSoal SapWenny HuNo ratings yet

- INVESTMENT MANAGEMENT-lakatan and CondoDocument22 pagesINVESTMENT MANAGEMENT-lakatan and CondoJewelyn C. Espares-CioconNo ratings yet

- Basic Concepts (1-33)Document33 pagesBasic Concepts (1-33)Akash LandgeNo ratings yet

- Accounting StandardDocument14 pagesAccounting StandardridhiNo ratings yet

- Hansen AISE IM Ch10Document55 pagesHansen AISE IM Ch10indahNo ratings yet

- An Introduction To Insurance AccountingDocument86 pagesAn Introduction To Insurance AccountingTricia PrincipeNo ratings yet

- Crisil Rating Using RatiosDocument17 pagesCrisil Rating Using RatiossushmaNo ratings yet

- SB 44 - LacsonDocument25 pagesSB 44 - LacsonMark Lester Lee AureNo ratings yet

- F2 - Financial ManagementDocument20 pagesF2 - Financial ManagementRobert MunyaradziNo ratings yet

- The Revenue CycleDocument68 pagesThe Revenue CycleKino Marinay100% (1)

- Chapter 3 Financial Statement Taxes and CashflowDocument33 pagesChapter 3 Financial Statement Taxes and CashflowlovejkbsNo ratings yet

- Informasi Keuangan Pro Forma Tidak Diaudit 31 Desember 2021 Dan 30 November 2022Document8 pagesInformasi Keuangan Pro Forma Tidak Diaudit 31 Desember 2021 Dan 30 November 2022KhresnaNo ratings yet

- BHL FY19 Annual ReportDocument94 pagesBHL FY19 Annual ReportFoysal NobinNo ratings yet

- Pepsi Annual ReportDocument118 pagesPepsi Annual Reportcurtnie bernardoNo ratings yet

- TXROM 2019 Dec QDocument17 pagesTXROM 2019 Dec QKAH MENG KAMNo ratings yet

- Lecture 1 - Accounting in The Czech RepublicDocument12 pagesLecture 1 - Accounting in The Czech RepublicUmar SulemanNo ratings yet

- Accounting Rule Changes Increase Apple ComputerDocument2 pagesAccounting Rule Changes Increase Apple ComputerDesiree Chambers0% (1)

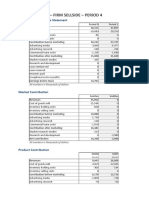

- Financial Report - Firm Sellside - Period 4: Company Profit & Loss StatementDocument73 pagesFinancial Report - Firm Sellside - Period 4: Company Profit & Loss StatementNancy suri100% (1)

- Financial Statement Analysis FormulasDocument10 pagesFinancial Statement Analysis FormulasKarl LuzungNo ratings yet

Download as pdf or txt

You might also like

- Hammer Group SeptDec 2023Document5 pagesHammer Group SeptDec 2023Adilah AzamNo ratings yet

- Solution Manual For Analysis For Financial Management 12th EditionDocument6 pagesSolution Manual For Analysis For Financial Management 12th EditionMatthew Karaffa100% (38)

- Earthware Case 3-1 To 3-5Document10 pagesEarthware Case 3-1 To 3-5Stephanie Slaughter80% (5)

- Case Study On Gainesboro Machine Tools CorporationDocument13 pagesCase Study On Gainesboro Machine Tools Corporationemehmehmeh86% (7)

- Garage Kipkurui PatrickDocument37 pagesGarage Kipkurui PatrickCarol Soi86% (7)

- Case Interviews IntroductionsDocument6 pagesCase Interviews IntroductionsArjjun ChanderNo ratings yet

- GIS SubstationDocument13 pagesGIS SubstationDakshay BhardwajNo ratings yet

- Summative Test-FABM2 2018-19Document3 pagesSummative Test-FABM2 2018-19Raul Soriano Cabanting0% (1)

- Advanced Taxation 3.3 August 2022Document26 pagesAdvanced Taxation 3.3 August 2022Obed AsamoahNo ratings yet

- Advanced Taxation May 2021Document20 pagesAdvanced Taxation May 2021akpanyapNo ratings yet

- Financial Management Paper 2.4 July 2023Document18 pagesFinancial Management Paper 2.4 July 2023johny SahaNo ratings yet

- Tax Avoidance MeasuresDocument7 pagesTax Avoidance MeasuresOWUSU BOATENGNo ratings yet

- Course Materials TaxationDocument21 pagesCourse Materials TaxationObed AsamoahNo ratings yet

- PT April 2022Document15 pagesPT April 2022Kipson Drizo MuksNo ratings yet

- Adv Tax April 2022Document27 pagesAdv Tax April 2022Kwabena Obeng-FosuNo ratings yet

- May 2020 Professional Examinations Advanced Audit & Assurance (Paper 3.2) Chief Examiner'S Report, Questions and Marking SchemeDocument20 pagesMay 2020 Professional Examinations Advanced Audit & Assurance (Paper 3.2) Chief Examiner'S Report, Questions and Marking SchemeVonnieNo ratings yet

- May 2021 Professional Examination Financial Reporting (Paper 2.1) Chief Examiner'S Report, Questions and Marking SchemeDocument27 pagesMay 2021 Professional Examination Financial Reporting (Paper 2.1) Chief Examiner'S Report, Questions and Marking SchemeThomas nyade100% (1)

- Advanced TaxationDocument21 pagesAdvanced TaxationEMMANUEL ADJEINo ratings yet

- Taxation South Africa (TX Zaf) June 2022 Examiner's ReportDocument9 pagesTaxation South Africa (TX Zaf) June 2022 Examiner's ReportwaseNo ratings yet

- ADVANCED TAXATION PAPER 3.3nov 2023Document22 pagesADVANCED TAXATION PAPER 3.3nov 2023batuchemNo ratings yet

- Sun Home Appliances Private - R - 25082020Document7 pagesSun Home Appliances Private - R - 25082020DarshanNo ratings yet

- Q3'21 Earnings Call PresentationDocument24 pagesQ3'21 Earnings Call Presentationsl7789No ratings yet

- Caf 2 Tax Autumn 2022Document4 pagesCaf 2 Tax Autumn 2022M AHMAD MAQBOOLNo ratings yet

- International TaxationDocument9 pagesInternational TaxationOWUSU BOATENGNo ratings yet

- Analysis For Financial Management 11Th Edition Higgins Solutions Manual Full Chapter PDFDocument36 pagesAnalysis For Financial Management 11Th Edition Higgins Solutions Manual Full Chapter PDFmarcia.tays151100% (22)

- Practice Final With SolutionsDocument8 pagesPractice Final With SolutionsSammy MosesNo ratings yet

- Principles of TaxationDocument17 pagesPrinciples of TaxationEMMANUEL ADJEINo ratings yet

- Advanced Level Accounting 600102 Examiners Report November 2022Document3 pagesAdvanced Level Accounting 600102 Examiners Report November 2022jayapriscilla1No ratings yet

- Principle of TaxationDocument6 pagesPrinciple of TaxationKhurram ShahzadNo ratings yet

- Press Release Arman Q3FY21Document5 pagesPress Release Arman Q3FY21Forall PainNo ratings yet

- Accounts Receivable and Inventory ManagementDocument53 pagesAccounts Receivable and Inventory ManagementFerriza AbanNo ratings yet

- Mergers and AcquisitionsDocument4 pagesMergers and AcquisitionsOWUSU BOATENGNo ratings yet

- Tutorial 2 Questions (Chapter 1)Document3 pagesTutorial 2 Questions (Chapter 1)jiayiwang0221No ratings yet

- Examiner Comments-Summer 2012Document4 pagesExaminer Comments-Summer 2012Mahendar BhojwaniNo ratings yet

- Financial Management Papernov 2023Document21 pagesFinancial Management Papernov 2023batuchemNo ratings yet

- Earnings Conference Call: Q4 Fiscal Year 2021Document25 pagesEarnings Conference Call: Q4 Fiscal Year 2021sl7789No ratings yet

- Group 4 Assignement, Financial and Management Accounting-1Document10 pagesGroup 4 Assignement, Financial and Management Accounting-10pointsNo ratings yet

- GP FINNANCEDocument12 pagesGP FINNANCEMuhammad Aiezaqul Haikal bin ZainuriNo ratings yet

- Earnings Conference Call: Q2 Fiscal Year 2021Document24 pagesEarnings Conference Call: Q2 Fiscal Year 2021sl7789No ratings yet

- Advanced Audit AssuranceDocument24 pagesAdvanced Audit AssuranceEMMANUEL ADJEINo ratings yet

- AF208 Testbank CompiledDocument100 pagesAF208 Testbank Compileds11186706No ratings yet

- Airvision India Private Limited - R - 25082020Document7 pagesAirvision India Private Limited - R - 25082020DarshanNo ratings yet

- Cadbury Nigeria PLC 2005Document29 pagesCadbury Nigeria PLC 2005Ada TeachesNo ratings yet

- Financial Reporting Paper 2.1 Dec 2023Document28 pagesFinancial Reporting Paper 2.1 Dec 2023Oni SegunNo ratings yet

- Ratio Analysis: Mari Perolum Company LimitiedDocument5 pagesRatio Analysis: Mari Perolum Company LimitiedNuman AhmedNo ratings yet

- Assessment 2 2Document6 pagesAssessment 2 2Thảo NguyễnNo ratings yet

- Important - Read This First: Family NameDocument6 pagesImportant - Read This First: Family NameArthur MendesNo ratings yet

- Balance Sheet InterpretationDocument3 pagesBalance Sheet InterpretationAkanksha KadamNo ratings yet

- November 2016 Professional Examinations Financial Management (Paper 2.4) Chief Examiner'S Report, Questions & Marking SchemeDocument18 pagesNovember 2016 Professional Examinations Financial Management (Paper 2.4) Chief Examiner'S Report, Questions & Marking SchemeSrikrishna DharNo ratings yet

- Medical Presentation - Q2FY23Document26 pagesMedical Presentation - Q2FY23Kdp03No ratings yet

- MGT Capstone 1 - 4Document3 pagesMGT Capstone 1 - 4Shakeel SajjadNo ratings yet

- 2022 ND - FM Suggested AnswerDocument10 pages2022 ND - FM Suggested Answermiradvance studyNo ratings yet

- FM MJ20 Detailed CommentaryDocument4 pagesFM MJ20 Detailed CommentaryleylaNo ratings yet

- CF Final ReportDocument11 pagesCF Final Reporteshmalsheikh703No ratings yet

- Greenlight Capital Re Press Release 2020 Q3 FINALDocument8 pagesGreenlight Capital Re Press Release 2020 Q3 FINALJoey KlenderNo ratings yet

- Popular, Inc. Conference Call PresentationDocument24 pagesPopular, Inc. Conference Call PresentationRubén E. Morales RiveraNo ratings yet

- PRINCIPLES OF TAXATION PAPER 2.6nov 2023Document22 pagesPRINCIPLES OF TAXATION PAPER 2.6nov 2023Obed AsamoahNo ratings yet

- Greenfield Corporation Case Study Part ADocument11 pagesGreenfield Corporation Case Study Part AJay WainwrightNo ratings yet

- 208-Test-Bank-2nd-Edth s1 2019Document96 pages208-Test-Bank-2nd-Edth s1 2019MilanNo ratings yet

- Financial Management Source 1Document13 pagesFinancial Management Source 1John Llucastre CortezNo ratings yet

- CreditAccess Grameen - Investor Presentation - Q4 - FY 2021 22Document54 pagesCreditAccess Grameen - Investor Presentation - Q4 - FY 2021 22Haidir AuliaNo ratings yet

- J.K. Lasser's Small Business Taxes 2012: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2012: Your Complete Guide to a Better Bottom LineNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific: 2020 EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: 2020 EditionNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionNo ratings yet

- Book-Responsibility Actg-SolMan PDFDocument18 pagesBook-Responsibility Actg-SolMan PDFLordson RamosNo ratings yet

- Basic Accounting-RatiosDocument22 pagesBasic Accounting-RatiosSala SahariNo ratings yet

- The Economic Feasibility of An Ultra-Low Cost AirlineDocument1 pageThe Economic Feasibility of An Ultra-Low Cost AirlineTshep SekNo ratings yet

- Hospital ManagementDocument12 pagesHospital Managementvalene_elleNo ratings yet

- Ken Hackel: Slowing Economic Growth Means Greater Focus On Economic ProfitDocument4 pagesKen Hackel: Slowing Economic Growth Means Greater Focus On Economic ProfitbogatishankarNo ratings yet

- Nirlaba JawabDocument7 pagesNirlaba JawabVerel HaikalNo ratings yet

- Soal SapDocument14 pagesSoal SapWenny HuNo ratings yet

- INVESTMENT MANAGEMENT-lakatan and CondoDocument22 pagesINVESTMENT MANAGEMENT-lakatan and CondoJewelyn C. Espares-CioconNo ratings yet

- Basic Concepts (1-33)Document33 pagesBasic Concepts (1-33)Akash LandgeNo ratings yet

- Accounting StandardDocument14 pagesAccounting StandardridhiNo ratings yet

- Hansen AISE IM Ch10Document55 pagesHansen AISE IM Ch10indahNo ratings yet

- An Introduction To Insurance AccountingDocument86 pagesAn Introduction To Insurance AccountingTricia PrincipeNo ratings yet

- Crisil Rating Using RatiosDocument17 pagesCrisil Rating Using RatiossushmaNo ratings yet

- SB 44 - LacsonDocument25 pagesSB 44 - LacsonMark Lester Lee AureNo ratings yet

- F2 - Financial ManagementDocument20 pagesF2 - Financial ManagementRobert MunyaradziNo ratings yet

- The Revenue CycleDocument68 pagesThe Revenue CycleKino Marinay100% (1)

- Chapter 3 Financial Statement Taxes and CashflowDocument33 pagesChapter 3 Financial Statement Taxes and CashflowlovejkbsNo ratings yet

- Informasi Keuangan Pro Forma Tidak Diaudit 31 Desember 2021 Dan 30 November 2022Document8 pagesInformasi Keuangan Pro Forma Tidak Diaudit 31 Desember 2021 Dan 30 November 2022KhresnaNo ratings yet

- BHL FY19 Annual ReportDocument94 pagesBHL FY19 Annual ReportFoysal NobinNo ratings yet

- Pepsi Annual ReportDocument118 pagesPepsi Annual Reportcurtnie bernardoNo ratings yet

- TXROM 2019 Dec QDocument17 pagesTXROM 2019 Dec QKAH MENG KAMNo ratings yet

- Lecture 1 - Accounting in The Czech RepublicDocument12 pagesLecture 1 - Accounting in The Czech RepublicUmar SulemanNo ratings yet

- Accounting Rule Changes Increase Apple ComputerDocument2 pagesAccounting Rule Changes Increase Apple ComputerDesiree Chambers0% (1)

- Financial Report - Firm Sellside - Period 4: Company Profit & Loss StatementDocument73 pagesFinancial Report - Firm Sellside - Period 4: Company Profit & Loss StatementNancy suri100% (1)

- Financial Statement Analysis FormulasDocument10 pagesFinancial Statement Analysis FormulasKarl LuzungNo ratings yet