Download as pdf or txt

You might also like

- Ebook POD Eng VersionDocument24 pagesEbook POD Eng VersionNhitodocuNo ratings yet

- City Logistics: Network Modelling Intelligent Transport SystemsDocument258 pagesCity Logistics: Network Modelling Intelligent Transport SystemsĐặng LinhNo ratings yet

- Presentacion Final International FinanceDocument37 pagesPresentacion Final International FinanceJilfredy Gonzalez VisbalNo ratings yet

- How Covid-19 Has-And Has Not-Affected Global Ad Spending: Emarketer'S Updated Full-Year 2020 Ad Spending ForecastDocument3 pagesHow Covid-19 Has-And Has Not-Affected Global Ad Spending: Emarketer'S Updated Full-Year 2020 Ad Spending ForecastDavid H. HorowitzNo ratings yet

- Covid-19 Effect On BusinessDocument3 pagesCovid-19 Effect On BusinessOWAISNo ratings yet

- AOF Case Competition Round 2 Xiaomi MADocument38 pagesAOF Case Competition Round 2 Xiaomi MALương TrầnNo ratings yet

- Noble Media Newsletter 4Q 2020-1Document24 pagesNoble Media Newsletter 4Q 2020-1Joe BidenoNo ratings yet

- Impact of Covid-19 Pandemic On International MarketingDocument8 pagesImpact of Covid-19 Pandemic On International Marketingramya penmatsaNo ratings yet

- Changes in Employment Post CovidDocument4 pagesChanges in Employment Post CovidR TNo ratings yet

- S1 International BusinessDocument4 pagesS1 International Businessyojan huaytaNo ratings yet

- Business ImpactDocument25 pagesBusiness ImpactDeepanshu DimriNo ratings yet

- Marketing Management - Summer-21 - Mid Term AssignmentDocument7 pagesMarketing Management - Summer-21 - Mid Term AssignmentAbdullah Al MuttakiNo ratings yet

- QUESTION 1: Read The Above Article and Explain What Are The Global Conflicting Trade Signals?Document7 pagesQUESTION 1: Read The Above Article and Explain What Are The Global Conflicting Trade Signals?mzhouryNo ratings yet

- A. Survive, Revive and Growth Strategies Adopted by EmamiDocument9 pagesA. Survive, Revive and Growth Strategies Adopted by EmamiShivani DuttNo ratings yet

- MGI Urban World3 ES Oct2013Document28 pagesMGI Urban World3 ES Oct2013valladaoNo ratings yet

- Impact of Covid 19 On Marketing Strategy and ExpenditureDocument9 pagesImpact of Covid 19 On Marketing Strategy and ExpenditureNaveen RajputNo ratings yet

- Your Strategy in The New Global LandscapeDocument6 pagesYour Strategy in The New Global LandscapeSourabh DuttaNo ratings yet

- MGI Urban World 3 Executive Summary Oct 2013Document28 pagesMGI Urban World 3 Executive Summary Oct 2013Hou RasmeyNo ratings yet

- PWC Outlook22Document28 pagesPWC Outlook22Karthik RamanujamNo ratings yet

- State of The UAE Retail Economy - Q1 - 2021 - FINALDocument32 pagesState of The UAE Retail Economy - Q1 - 2021 - FINALFarhaan MutturNo ratings yet

- Extended Essay Final Leonardo ProcaccianteDocument23 pagesExtended Essay Final Leonardo ProcacciantethedevelopersinboxNo ratings yet

- Unit 5Document14 pagesUnit 5sayli kudalkarNo ratings yet

- MKT 5915Document8 pagesMKT 5915Fawad H. KhanNo ratings yet

- 2020 Manufacturing Industry OutlookDocument10 pages2020 Manufacturing Industry OutlookDavid SchumakherNo ratings yet

- A Company of Asos PLC: Group NDocument11 pagesA Company of Asos PLC: Group NRamil AliyevNo ratings yet

- CNBC Catalyst The Road AheadDocument28 pagesCNBC Catalyst The Road AheadromanNo ratings yet

- Chapter 1 Draft-Brosas, Cabug-Os, CayacoDocument20 pagesChapter 1 Draft-Brosas, Cabug-Os, CayacoAdrheyni Kyle Cabug-osNo ratings yet

- Crunchbase - Industry - Forecast - Report 2020Document17 pagesCrunchbase - Industry - Forecast - Report 2020Fatima MaldonadoNo ratings yet

- MBA 600 Final Assinment Last 2Document6 pagesMBA 600 Final Assinment Last 2Abu Sadat Md.SayemNo ratings yet

- Global Market of Advertising IndustryDocument5 pagesGlobal Market of Advertising IndustryVandan SapariaNo ratings yet

- Social Advertising Strategic Outlook 2012-2013 Finland, 2012Document4 pagesSocial Advertising Strategic Outlook 2012-2013 Finland, 2012HnyB InsightsNo ratings yet

- Understanding and Leading Changes in Target Corp and MWG Corp - Assignment 1Document26 pagesUnderstanding and Leading Changes in Target Corp and MWG Corp - Assignment 1Dang Le Minh Anh (FGW DN)No ratings yet

- 2012 JulyDocument8 pages2012 Julyjen8948No ratings yet

- Accenture B-School Challenge - Comms & Media Case StudyDocument2 pagesAccenture B-School Challenge - Comms & Media Case StudyNakul VyasNo ratings yet

- Emerging Issues On Trends in Consumption, Productio N and MarketsDocument13 pagesEmerging Issues On Trends in Consumption, Productio N and MarketsWanderlust 7654No ratings yet

- Digital Health Investments SampleDocument7 pagesDigital Health Investments SampleRoberto CarrizosaNo ratings yet

- Okuma Paylaşim-107Document6 pagesOkuma Paylaşim-107faithme googleNo ratings yet

- Wachtell, Lipton, Rosen & KatzDocument13 pagesWachtell, Lipton, Rosen & KatzFooyNo ratings yet

- Impact of Covid-19 On Firms' PerformanceDocument2 pagesImpact of Covid-19 On Firms' PerformanceNguyễn Thuỳ LinhNo ratings yet

- Ass 4 TorionDocument2 pagesAss 4 TorionJeric TorionNo ratings yet

- Social Advertising Strategic Outlook 2012-2013 Canada, 2012Document4 pagesSocial Advertising Strategic Outlook 2012-2013 Canada, 2012HnyB InsightsNo ratings yet

- CompendiumDocument5 pagesCompendiumParimal GosaviNo ratings yet

- The Luxury IndustryDocument8 pagesThe Luxury IndustryShreeyaNo ratings yet

- Covid-19 Crisis and International BusinessDocument13 pagesCovid-19 Crisis and International BusinessStanley PonrajNo ratings yet

- The Outbreak of The COVIDDocument6 pagesThe Outbreak of The COVIDkeithNo ratings yet

- Effect of the Covid Pandemic on Current Economic Trends : Career, Money Management and Investment StrategiesFrom EverandEffect of the Covid Pandemic on Current Economic Trends : Career, Money Management and Investment StrategiesNo ratings yet

- Social Advertising Strategic Outlook 2012-2013 France, 2012Document4 pagesSocial Advertising Strategic Outlook 2012-2013 France, 2012HnyB InsightsNo ratings yet

- Ford ReportDocument8 pagesFord ReportGio RobakidzeNo ratings yet

- The Rise of BPO Industry and Its Effects To The 2021 Philippine EconomyDocument8 pagesThe Rise of BPO Industry and Its Effects To The 2021 Philippine EconomyLean Dale IgosNo ratings yet

- Group ZA - Case Study #1Document12 pagesGroup ZA - Case Study #1penar38488No ratings yet

- Industry 4.0: Volume Lii July 2020Document8 pagesIndustry 4.0: Volume Lii July 2020Andy HuffNo ratings yet

- Entertainment and Media Outlook Perspectives 2020 2024Document28 pagesEntertainment and Media Outlook Perspectives 2020 2024Nairit Mondal100% (1)

- Nauman AssignmentDocument8 pagesNauman Assignmentsalar AHMEDNo ratings yet

- BusinessDocument8 pagesBusinessShubhaNo ratings yet

- Fashion Ecommerce 2021Document41 pagesFashion Ecommerce 2021Nguyễn MyNo ratings yet

- NPC International, Inc. Research AnlysisDocument7 pagesNPC International, Inc. Research Anlysisacademicwriter peterNo ratings yet

- Ten Global Business Challenges in 2024Document4 pagesTen Global Business Challenges in 2024Nikolettochka GaidulyanNo ratings yet

- POWER RANKING: The 10 Best Industries in 2020 For Entrepreneurs To Start Million-Dollar Businesses Despite The PandemicDocument6 pagesPOWER RANKING: The 10 Best Industries in 2020 For Entrepreneurs To Start Million-Dollar Businesses Despite The PandemicTung NgoNo ratings yet

- Social Advertising Strategic Outlook 2012-2013 Germany, 2012Document4 pagesSocial Advertising Strategic Outlook 2012-2013 Germany, 2012HnyB InsightsNo ratings yet

- The Contemporary World EssayDocument3 pagesThe Contemporary World EssayMarcus ZunigaNo ratings yet

- Covid-19 Impact - Consumers Move More Towards Digital - The Hindu BusinessLineDocument13 pagesCovid-19 Impact - Consumers Move More Towards Digital - The Hindu BusinessLineSamiha MjahedNo ratings yet

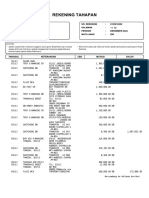

- E Statement 240429103244336704914Document13 pagesE Statement 240429103244336704914deepakjhaNo ratings yet

- ANTIVIRUSDocument5 pagesANTIVIRUSAmardeep SinghNo ratings yet

- Priyanka (CV)Document3 pagesPriyanka (CV)Priyanka AggarwalNo ratings yet

- Cryptography and System SecurityDocument3 pagesCryptography and System SecurityNirishNo ratings yet

- NIFT M.ftech Sample QuestionsDocument7 pagesNIFT M.ftech Sample QuestionsMunnar KeralaNo ratings yet

- A Developer's Guide To Symbian Signed: v1.1 - 20 September 2005Document58 pagesA Developer's Guide To Symbian Signed: v1.1 - 20 September 2005Argien Mesina NaguitNo ratings yet

- Resume - Chitransh JoshiDocument3 pagesResume - Chitransh JoshiTeddy & VarshuNo ratings yet

- Cyber Law and Information SecurityDocument2 pagesCyber Law and Information SecurityDreamtech Press100% (1)

- 14 - Industrial Revolution 4.0Document22 pages14 - Industrial Revolution 4.0mazuraoctavianum1No ratings yet

- E Commerce - AkashDocument17 pagesE Commerce - AkashakashNo ratings yet

- FMCG CEOs - Why Do We Need To Update Now Our Ecommerce Strategy - The Rise of Ecommerce 2.0® - FFA 30102023Document43 pagesFMCG CEOs - Why Do We Need To Update Now Our Ecommerce Strategy - The Rise of Ecommerce 2.0® - FFA 30102023Aravind ANo ratings yet

- Commercial Bank of CeylonDocument12 pagesCommercial Bank of Ceylonpavel4570250% (1)

- AccountManagement ChecklistDocument2 pagesAccountManagement ChecklistDushyant TyagiNo ratings yet

- Some Specific Examples of Brand Marketing StrategyDocument3 pagesSome Specific Examples of Brand Marketing StrategyThanh ThuỳNo ratings yet

- Bitcoin: Done By: Mohammad Ali Abu Shukur 20150269Document10 pagesBitcoin: Done By: Mohammad Ali Abu Shukur 20150269Mohammad Abu-ShukurNo ratings yet

- b2b AssignmentDocument11 pagesb2b AssignmentAyush ChoudharyNo ratings yet

- Eap TLSDocument3 pagesEap TLSscribdbhanuNo ratings yet

- E-Commerce Network Security Based On Big Data in Cloud Computing EnvironmentDocument8 pagesE-Commerce Network Security Based On Big Data in Cloud Computing EnvironmentNisa Nurlitawaty 2102125029No ratings yet

- Amazon Ansoff MatrixDocument2 pagesAmazon Ansoff Matrixlailarashed6100% (1)

- ETSI TR 102 071: Mobile Commerce (M-COMM) Requirements For Payment Methods For Mobile CommerceDocument16 pagesETSI TR 102 071: Mobile Commerce (M-COMM) Requirements For Payment Methods For Mobile CommerceShahzeb AmjadNo ratings yet

- Mis206 010 058Document13 pagesMis206 010 058Tazrian FerdousNo ratings yet

- OpTransactionHistoryTpr03 01 2023Document21 pagesOpTransactionHistoryTpr03 01 2023rajesh lankaNo ratings yet

- Merged - XXXX - HR Payroll Management - Amazon - Deena Wala Sahil SinghDocument75 pagesMerged - XXXX - HR Payroll Management - Amazon - Deena Wala Sahil Singhmahesh 1430No ratings yet

- CH # 17 - Telecommunication NotesDocument6 pagesCH # 17 - Telecommunication Notesfarjad0% (1)

- MM Unit VI Sales PromotionDocument42 pagesMM Unit VI Sales PromotionAbhishek RajNo ratings yet

- Tes DesDocument12 pagesTes DesSarah SarcheNo ratings yet

- Elifas Levi - Masonske Legende: Everything Books Audiobooks Snapshots Articles Sheet Music PodcastsDocument8 pagesElifas Levi - Masonske Legende: Everything Books Audiobooks Snapshots Articles Sheet Music PodcastsTinamou0001No ratings yet

- The Influence of Social Media Marketing Activities On Customer LoyaltyDocument24 pagesThe Influence of Social Media Marketing Activities On Customer LoyaltyFaheemullah HaddadNo ratings yet

- Entrepreneurship & Halal EarningDocument7 pagesEntrepreneurship & Halal EarningAritri AyatNo ratings yet