Download as pdf or txt

You might also like

- Goldman Sachs Sees Reliance Industries at 3,400 Returns InflectionDocument35 pagesGoldman Sachs Sees Reliance Industries at 3,400 Returns Inflectionmanitjainm21No ratings yet

- ACC 111 Examination For StudentsDocument10 pagesACC 111 Examination For StudentsNeil Vincent Boco100% (4)

- Behavioral Drivers of Brand Equity - Head and ShouldersDocument18 pagesBehavioral Drivers of Brand Equity - Head and ShouldersNihal GoudNo ratings yet

- ACC 3rd QuizDocument12 pagesACC 3rd QuizJazzy Mercado55% (11)

- Solicitation Letter For Fiesta 2014Document1 pageSolicitation Letter For Fiesta 2014MJ Villamor Aquillo91% (32)

- Practice 5 - Accounting For Merchandising - Theories and Problem SolvingDocument7 pagesPractice 5 - Accounting For Merchandising - Theories and Problem SolvingAeron RamirexNo ratings yet

- Accounting FirstDocument24 pagesAccounting Firstmagdy kamelNo ratings yet

- Accounting For Merchandising OperationsDocument7 pagesAccounting For Merchandising OperationsRakibul HasanNo ratings yet

- JULLIE CARMELLE H. CHATTO - APE 1 - Final Exam AnswersDocument5 pagesJULLIE CARMELLE H. CHATTO - APE 1 - Final Exam AnswersJULLIE CARMELLE H. CHATTONo ratings yet

- BASICDocument3 pagesBASICReynie RamosNo ratings yet

- This Study Resource Was: InventoriesDocument3 pagesThis Study Resource Was: InventoriesKim TanNo ratings yet

- 8 ACCT 1A&B MerchandisingDocument13 pages8 ACCT 1A&B MerchandisingShannon MojicaNo ratings yet

- FDNACCT Review Exam-AnsKey-SetADocument7 pagesFDNACCT Review Exam-AnsKey-SetAChyle Sagun100% (1)

- Merchandising QuizDocument1 pageMerchandising Quizjade0% (1)

- ACCT 1A&B: Fundamentals of Accounting BCSVDocument14 pagesACCT 1A&B: Fundamentals of Accounting BCSVDanicaZhayneValdezNo ratings yet

- ACCT 1A&B: Fundamentals of Accounting BCSV Fundamentals of Accounting Part I Accounting For Merchandising BusinessDocument14 pagesACCT 1A&B: Fundamentals of Accounting BCSV Fundamentals of Accounting Part I Accounting For Merchandising BusinessRyan CapiliNo ratings yet

- Chap 5Document19 pagesChap 5Tran Pham Quoc ThuyNo ratings yet

- Accounting Review Materials: Debited When Petty Cash Fund Proves Out ShortDocument7 pagesAccounting Review Materials: Debited When Petty Cash Fund Proves Out ShortJude SantosNo ratings yet

- Tutorial 3 Due DateDocument6 pagesTutorial 3 Due DateFatin Nur Aina Mohd Radzi0% (1)

- PMBA - Quiz # 6 - SolutionDocument4 pagesPMBA - Quiz # 6 - SolutionAli Shaharyar ShigriNo ratings yet

- Financial Accounting Study Guide Ch5 AnswersDocument7 pagesFinancial Accounting Study Guide Ch5 AnswersSummerNo ratings yet

- Test SamplesDocument18 pagesTest SamplesDen NgNo ratings yet

- Basic Accounting ReviewerDocument4 pagesBasic Accounting ReviewerRyan Dizon100% (1)

- 1E Financial (Sat - 16-3-2024) - Final Ch.1Document11 pages1E Financial (Sat - 16-3-2024) - Final Ch.1ahmedNo ratings yet

- 2022 Fabm 2nd Quarterly ExamDocument4 pages2022 Fabm 2nd Quarterly Examarmelle louiseNo ratings yet

- Inventories - Theories - Please AnswerDocument7 pagesInventories - Theories - Please AnswerAbbygailNo ratings yet

- Basic Acctg MCQDocument8 pagesBasic Acctg MCQJohn AceNo ratings yet

- 1 - Page Dr. Magdy KamelDocument10 pages1 - Page Dr. Magdy Kamelmagdy kamelNo ratings yet

- Accountancy, Business and Management Name: - ScoreDocument3 pagesAccountancy, Business and Management Name: - ScoreHLeigh Nietes-GabutanNo ratings yet

- Basic MathDocument6 pagesBasic MathWarda MamasalagatNo ratings yet

- Chapter 8 Valuation of Inventories MCQ UnansweredDocument7 pagesChapter 8 Valuation of Inventories MCQ UnansweredMa Teresa B. CerezoNo ratings yet

- Final Exam - TemplateDocument7 pagesFinal Exam - TemplateKristine Esplana ToraldeNo ratings yet

- UntitledDocument9 pagesUntitledĐăng Nguyễn HảiNo ratings yet

- Forum ACC WM - Sesi 3 (REV)Document9 pagesForum ACC WM - Sesi 3 (REV)Windy Martaputri100% (2)

- Quiz 3 - Intacc 2Document8 pagesQuiz 3 - Intacc 2Eleina SwiftNo ratings yet

- Acctg1 MidtermDocument6 pagesAcctg1 MidtermKevin Elrey Arce50% (4)

- FABM2 First Grading Study GuideDocument3 pagesFABM2 First Grading Study GuideGwyneth BundaNo ratings yet

- Chapter Test - Expenditure CycleDocument4 pagesChapter Test - Expenditure CycleFaith Reyna TanNo ratings yet

- Accounting Concept and Principle QuizDocument2 pagesAccounting Concept and Principle QuizkristelNo ratings yet

- Tutorial 3 Merchandising-1Document5 pagesTutorial 3 Merchandising-1minzheNo ratings yet

- 3 - Activities For ULO 7, 8, 9, 10 & 11Document8 pages3 - Activities For ULO 7, 8, 9, 10 & 11RJ 1No ratings yet

- Far Set2Document5 pagesFar Set2bea kullinNo ratings yet

- Merchandising - Review Materials (Theories)Document69 pagesMerchandising - Review Materials (Theories)julsNo ratings yet

- This Study Resource Was: Theory of AccountsDocument6 pagesThis Study Resource Was: Theory of AccountsNah Hamza100% (1)

- Chapter 1 Introduction To AccountingDocument4 pagesChapter 1 Introduction To AccountingErica mae BodosoNo ratings yet

- Evaluation MULTIPLE CHOICE. Write The Letter of The Correct Answer Beside The Item NumberDocument2 pagesEvaluation MULTIPLE CHOICE. Write The Letter of The Correct Answer Beside The Item NumberKaren CubalitNo ratings yet

- Chapter 5 Inventories Exercises Answer Guide Summer AY2122 PDFDocument10 pagesChapter 5 Inventories Exercises Answer Guide Summer AY2122 PDFwavyastroNo ratings yet

- Ust Jpia Inventories Reviewer Ca51010 PDFDocument10 pagesUst Jpia Inventories Reviewer Ca51010 PDFLlyana paula SuyuNo ratings yet

- Theory NotesDocument7 pagesTheory NotesThe Xplorer In Me CooksNo ratings yet

- AC 1 2 Final Exam 1Document7 pagesAC 1 2 Final Exam 1christine anglaNo ratings yet

- Final Exam AC 1 2 Answer KeyDocument7 pagesFinal Exam AC 1 2 Answer KeyBill VilladolidNo ratings yet

- Principles of AccountingDocument12 pagesPrinciples of AccountingEliza Mae SumangilNo ratings yet

- Accounting Theory and Analysis Chart 16 Test BankDocument14 pagesAccounting Theory and Analysis Chart 16 Test BankSonny MaciasNo ratings yet

- IGCSE Grade 9th & 10thDocument6 pagesIGCSE Grade 9th & 10thThe Xplorer In Me CooksNo ratings yet

- Quiz No. 4 - InventoriesDocument8 pagesQuiz No. 4 - Inventoriesremalyn rigorNo ratings yet

- Practice Material - Transaction CyclesDocument9 pagesPractice Material - Transaction CyclesElin SaldañaNo ratings yet

- Excel Professional Services, Inc.: Discussion QuestionsDocument5 pagesExcel Professional Services, Inc.: Discussion QuestionskæsiiiNo ratings yet

- Ap 501Document7 pagesAp 501Christine Jane AbangNo ratings yet

- Basic AcctgDocument7 pagesBasic AcctglysaNo ratings yet

- Jamb Principles-Of-Accounts Past Question 1994 - 2004Document38 pagesJamb Principles-Of-Accounts Past Question 1994 - 2004Chukwudinma IkechukwuNo ratings yet

- Ex. 2Document4 pagesEx. 2TinNo ratings yet

- Principle I COC Exam 2Document9 pagesPrinciple I COC Exam 2natinaelbahiru74No ratings yet

- Quizzer - Completing The Accounting CycleDocument10 pagesQuizzer - Completing The Accounting CyclePrincess Kaye PitogoNo ratings yet

- Quizzer ManufacturingDocument2 pagesQuizzer ManufacturingPrincess Kaye PitogoNo ratings yet

- HO2.The Conceptual FrameworkDocument36 pagesHO2.The Conceptual FrameworkPrincess Kaye PitogoNo ratings yet

- Bfar Act.Document1 pageBfar Act.Princess Kaye PitogoNo ratings yet

- Business Model CanvasDocument12 pagesBusiness Model CanvasSabrine DraouiNo ratings yet

- CG and BOD Governance: Presented By: Anita Khanal Basanta Bhetwal Sushmita PandeyDocument13 pagesCG and BOD Governance: Presented By: Anita Khanal Basanta Bhetwal Sushmita PandeyBasanta BhetwalNo ratings yet

- Chapter 8 - Sample ProblemDocument2 pagesChapter 8 - Sample ProblemMaDine 19No ratings yet

- Behavioral Process in Marketing Channels - IMT GHZDocument29 pagesBehavioral Process in Marketing Channels - IMT GHZGurmeet SinghNo ratings yet

- Purchase Price - An EOI Covers The Purchase Consideration The BuyerDocument3 pagesPurchase Price - An EOI Covers The Purchase Consideration The Buyerankush birlaNo ratings yet

- MiyawwDocument9 pagesMiyawwjessa mae zerdaNo ratings yet

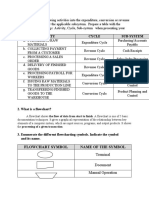

- Activity Cycle Sub-System: Flowchart Symbol Name of The SymbolDocument3 pagesActivity Cycle Sub-System: Flowchart Symbol Name of The SymbolALLIAH CARL MANUELLE PASCASIONo ratings yet

- Edward EnelamahDocument3 pagesEdward EnelamahRajan GuptaNo ratings yet

- Proozy QNADocument3 pagesProozy QNANicholas GoeiNo ratings yet

- Module 4. Activity Based Costing (Questions)Document9 pagesModule 4. Activity Based Costing (Questions)Praneeth KNo ratings yet

- Katarmal Divyaben BlackbookDocument77 pagesKatarmal Divyaben Blackbookritzzzz1309No ratings yet

- Creating A Model Culture of Management Change Key PointsDocument3 pagesCreating A Model Culture of Management Change Key PointsJeaneth Dela Pena CarnicerNo ratings yet

- Digital-Skills-Digital-Marketing Certificate of Achievement Oj838x9 PDFDocument2 pagesDigital-Skills-Digital-Marketing Certificate of Achievement Oj838x9 PDFMd.Taharul IslamNo ratings yet

- Your Name and Identical Card, Address: Resignation Letter From Ria Solution SDN BHD As Ldar InspectorDocument1 pageYour Name and Identical Card, Address: Resignation Letter From Ria Solution SDN BHD As Ldar InspectorMuhammad ZariqNo ratings yet

- Seven ElevenSupplyChainanalysisDocument12 pagesSeven ElevenSupplyChainanalysisHuyền HuyềnNo ratings yet

- HSBC Ivb VC Term Sheet Guide 2024Document67 pagesHSBC Ivb VC Term Sheet Guide 2024Xie NiyunNo ratings yet

- Tutorial CSDocument5 pagesTutorial CSallyaNo ratings yet

- Chap 9: Present ValueDocument4 pagesChap 9: Present ValueDouglas M. DougyNo ratings yet

- 1 Processing Financial Transactions and Extracting InterimDocument62 pages1 Processing Financial Transactions and Extracting InterimZEMENAYENo ratings yet

- Sam (300 Words Individual Reflective Summary)Document5 pagesSam (300 Words Individual Reflective Summary)Rohan Nag ChowdhuryNo ratings yet

- Zinka Logistics Solutions - R-25092020Document8 pagesZinka Logistics Solutions - R-25092020Atiqur Rahman BarbhuiyaNo ratings yet

- Day 9Document22 pagesDay 9Trang NguyễnNo ratings yet

- Module 5 Introduction To Display AdvertisingDocument41 pagesModule 5 Introduction To Display AdvertisingVMPNo ratings yet

- Subledger Accounting Rules Detail Listing ReportDocument9 pagesSubledger Accounting Rules Detail Listing ReportRoberto Velasco CostaNo ratings yet

- CMCF Membership-Application-Form 2023Document5 pagesCMCF Membership-Application-Form 2023Afiq ZulhilmiNo ratings yet

- What Is The Overall Weighted Average Cost of Capital (WACC) ?Document3 pagesWhat Is The Overall Weighted Average Cost of Capital (WACC) ?JIAXUAN WANGNo ratings yet

- Star Export HouseDocument14 pagesStar Export Houseshishir09aug0% (1)