TAX Year Assignment

TAX Year Assignment

You might also like

- Chapter 10-Financial Reporting in Public SectorDocument22 pagesChapter 10-Financial Reporting in Public SectorRifky Kesuma100% (2)

- Corporate Financial Reporting - Government AccountingDocument21 pagesCorporate Financial Reporting - Government AccountingAAKASH TOMARNo ratings yet

- Sub Topic 1Document8 pagesSub Topic 1Marie TaylaranNo ratings yet

- OrganizedDocument72 pagesOrganizedhamidsayyed2002No ratings yet

- Government Accounting & Financial ReportingDocument37 pagesGovernment Accounting & Financial ReportingSony AxleNo ratings yet

- Assignment # 1: Submitted FromDocument15 pagesAssignment # 1: Submitted FromAbdullah AliNo ratings yet

- ACC709 Lecture 5Document38 pagesACC709 Lecture 5dt7813369No ratings yet

- Government Accounting SystemDocument46 pagesGovernment Accounting SystemMeshack NyekelelaNo ratings yet

- TOPIC 1 Fundamentals of AccountingDocument10 pagesTOPIC 1 Fundamentals of AccountingAnastasia MelnicovaNo ratings yet

- Chapter 1 Ethiopian Govt AcctingDocument22 pagesChapter 1 Ethiopian Govt Acctingwube100% (1)

- Functions of FBR / Revenue DivisionDocument7 pagesFunctions of FBR / Revenue DivisionWajahat GhafoorNo ratings yet

- ChapterDocument6 pagesChaptermaheshNo ratings yet

- ChapterDocument101 pagesChapterkamath16002No ratings yet

- Chapter 5 & 6Document8 pagesChapter 5 & 6HisyamNo ratings yet

- PTX - AssignmentDocument15 pagesPTX - AssignmentNUR ALEEYA MAISARAH BINTI MOHD NASIR (AS)No ratings yet

- 5acc224 Week One Introduction To Public Sector Accounting 2223Document33 pages5acc224 Week One Introduction To Public Sector Accounting 2223umuriegenevieveNo ratings yet

- Tax FinalDocument16 pagesTax FinalAnany UpadhyayNo ratings yet

- Rohith BcomDocument13 pagesRohith BcomubbapallyrudhiraNo ratings yet

- Direct Tax NotesDocument4 pagesDirect Tax Notesashutoshbhatra98No ratings yet

- Nadiavietta - 120110180071 - Research Methodology Chapter I - IiDocument10 pagesNadiavietta - 120110180071 - Research Methodology Chapter I - IiRasqi ArfakhsyadzNo ratings yet

- 01 Chapter 1 The Development of The Accounting ProfessionDocument3 pages01 Chapter 1 The Development of The Accounting Professionsoyoung kimNo ratings yet

- 270MEF-EN-Prakas On TaxAuditDocument9 pages270MEF-EN-Prakas On TaxAuditchannat zaboroskiNo ratings yet

- BAB II - Inggris Revisi 000001Document18 pagesBAB II - Inggris Revisi 000001Lydia KirbyNo ratings yet

- Income TaxDocument195 pagesIncome TaxAleti NithishNo ratings yet

- Income Tax DepartmentDocument88 pagesIncome Tax DepartmentkajalNo ratings yet

- Chapter One: Introduction To Federal Government of Ethiopia Accounting and Financial ManagementDocument61 pagesChapter One: Introduction To Federal Government of Ethiopia Accounting and Financial ManagementGirma100% (4)

- Functions of Budget:: Economic FunctionDocument10 pagesFunctions of Budget:: Economic FunctionAli BaigNo ratings yet

- Article About Provisional TaxDocument6 pagesArticle About Provisional Taxduanedejager01No ratings yet

- Présentation Des Comptes Consolidés Selon Le Plan Comptable - Chapitre 01 - Le Cadre Théorique Des États Financiers Et de La Consolidation 2Document14 pagesPrésentation Des Comptes Consolidés Selon Le Plan Comptable - Chapitre 01 - Le Cadre Théorique Des États Financiers Et de La Consolidation 2IK storeNo ratings yet

- Public Sector AccountingDocument15 pagesPublic Sector AccountingerutujirogoodluckNo ratings yet

- Operational Framework of Accrual Basis of Accounting in Governments in IndiaDocument19 pagesOperational Framework of Accrual Basis of Accounting in Governments in Indiasas examNo ratings yet

- 501-Direct Tax Laws and AccountsDocument19 pages501-Direct Tax Laws and Accountssuyash bajpaiNo ratings yet

- Historical Overview of Ethiopian Government Accounting SystemDocument20 pagesHistorical Overview of Ethiopian Government Accounting Systemnegamedhane58100% (3)

- An Overview of National Budget in BangladeshDocument4 pagesAn Overview of National Budget in BangladeshAnikaNo ratings yet

- Nature of Government AccountingDocument16 pagesNature of Government AccountingLJ AggabaoNo ratings yet

- In Elec111 - Government Accounting & Budgeting Padm 107 - Public Accounting & Budgeting)Document36 pagesIn Elec111 - Government Accounting & Budgeting Padm 107 - Public Accounting & Budgeting)Erika MonisNo ratings yet

- Financial StatementDocument7 pagesFinancial StatementEunice SorianoNo ratings yet

- Allan and CharlesDocument6 pagesAllan and CharlesNkuuwe EdmundNo ratings yet

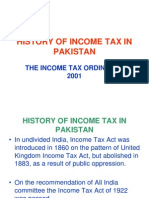

- History of Income Tax in PakistanDocument37 pagesHistory of Income Tax in PakistanSoNaa BalochNo ratings yet

- New Government Accounting System (NGAS) in The PhilippinesDocument24 pagesNew Government Accounting System (NGAS) in The PhilippinesJingRellin100% (1)

- Difference Between Accounting and AuditDocument5 pagesDifference Between Accounting and AuditsrpvickyNo ratings yet

- Financial Accounting and Reporting: Consolidated FundDocument42 pagesFinancial Accounting and Reporting: Consolidated FundHAFIZAH BINTI MAT NAWINo ratings yet

- DTP Full NotesDocument114 pagesDTP Full NotesCHAITHRANo ratings yet

- Audit Report in Case of Non Statutionry and Non Profit OrgDocument5 pagesAudit Report in Case of Non Statutionry and Non Profit OrgVIJAY PAREEKNo ratings yet

- Reporting by Financial Situations and Annual Accounting Reports To Entities in RomaniaDocument10 pagesReporting by Financial Situations and Annual Accounting Reports To Entities in Romaniamoscu danielNo ratings yet

- TaxDocument15 pagesTaxAnuja GuptaNo ratings yet

- Mawlana Bhashani Science and Technology UniversityDocument20 pagesMawlana Bhashani Science and Technology UniversitySabbir Ahmed100% (1)

- Tax Law NotesDocument16 pagesTax Law NotesGauri BansalNo ratings yet

- Hrishad - Income TaxDocument9 pagesHrishad - Income Taxkhayyum0% (1)

- Financial Accounting and Reporting 01Document9 pagesFinancial Accounting and Reporting 01Nuah SilvestreNo ratings yet

- Neha Kushwaha ProjectDocument66 pagesNeha Kushwaha Projectbuccspan2022No ratings yet

- DC Tacn Ki IiDocument6 pagesDC Tacn Ki IiHà Phương TrầnNo ratings yet

- Audit Procedure in IndiaDocument29 pagesAudit Procedure in IndiaPendem Vamsi KrishnaNo ratings yet

- Accounting System in SpainDocument5 pagesAccounting System in SpainHailee HayesNo ratings yet

- Leac 203Document27 pagesLeac 203Ias Aspirant AbhiNo ratings yet

- Government AccountingDocument32 pagesGovernment AccountingPratik GoyalNo ratings yet

- Chapter 1 Nature and Scope of NGASDocument26 pagesChapter 1 Nature and Scope of NGASRia BagoNo ratings yet

- Income Tax Planning in India 1Document76 pagesIncome Tax Planning in India 1Mallika t0% (1)

- Acca F 8 L7Document16 pagesAcca F 8 L7Fahmi AbdullaNo ratings yet

- "The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"From Everand"The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"No ratings yet

- Finger Print ExpertDocument29 pagesFinger Print Expertumaima aliNo ratings yet

- Human RightsDocument10 pagesHuman Rightsumaima aliNo ratings yet

- Assignment TopicDocument8 pagesAssignment Topicumaima aliNo ratings yet

- Plaint BankingDocument6 pagesPlaint Bankingumaima ali100% (1)

- AHRP IBLG Chapter IIIDocument3 pagesAHRP IBLG Chapter IIIjsbw4ky26fNo ratings yet

- IncentivesDocument25 pagesIncentivesNikko Bait-itNo ratings yet

- Chapter 5. Tax Policy: Policy Framework For Investment User'S ToolkitDocument40 pagesChapter 5. Tax Policy: Policy Framework For Investment User'S ToolkitRediet UtteNo ratings yet

- Project Report For The Institute of Education and Also TradingDocument9 pagesProject Report For The Institute of Education and Also Tradingbhanjasomanath4No ratings yet

- ABM TextDocument6 pagesABM TextPauline TayabanNo ratings yet

- Practical Research 2Document24 pagesPractical Research 2Charlene DimayugaNo ratings yet

- Kassahun Final Thesis 2005 CTA EditedDocument93 pagesKassahun Final Thesis 2005 CTA EditedHannaNo ratings yet

- Taxation IssuesDocument23 pagesTaxation IssuesBianca Jane GaayonNo ratings yet

- Tax Incentives in Developing Countries - A Case Study-Singapore and PhilippinesDocument29 pagesTax Incentives in Developing Countries - A Case Study-Singapore and PhilippinesBhosx KimNo ratings yet

- Chapter Five 5. Investment IncentivesDocument12 pagesChapter Five 5. Investment IncentivesSeid KassawNo ratings yet

- Đầu tư QT - metroDocument66 pagesĐầu tư QT - metroMaiNo ratings yet

- Tax IncentivesDocument43 pagesTax Incentivesmay leeNo ratings yet

- JAO No 1-2019Document6 pagesJAO No 1-2019JoyceTanNo ratings yet

- Tax Competition For Foreign Direct Investment in ASEAN: Is Corporate Income Tax Harmonization The Solution?Document34 pagesTax Competition For Foreign Direct Investment in ASEAN: Is Corporate Income Tax Harmonization The Solution?MUC kediriNo ratings yet

- Chapter 15 Taxincentives Group3Document15 pagesChapter 15 Taxincentives Group3Rhenzo ManayanNo ratings yet

- Tax Incentives For Companies To Invest The Portuguese Case in 2019Document17 pagesTax Incentives For Companies To Invest The Portuguese Case in 2019Global Research and Development ServicesNo ratings yet

- Module 01 CREATE Law Tax IncentivesDocument30 pagesModule 01 CREATE Law Tax IncentivesMitch PacienteNo ratings yet

- ĐTQT ĐỀ CƯƠNG THI CUỐI KỲ 1Document9 pagesĐTQT ĐỀ CƯƠNG THI CUỐI KỲ 1hminlNo ratings yet

- Scopus (Macroeconomic Effects of Corporate Tax Policy)Document22 pagesScopus (Macroeconomic Effects of Corporate Tax Policy)aldapermatasari021No ratings yet

- Tax Incentives G. 07 BsDocument10 pagesTax Incentives G. 07 BsLevenson KadegheNo ratings yet

- Effect of Tax Incentives On The Growth of Smes in Rwanda: A Case Study of Smes in Nyarugenge DistrictDocument9 pagesEffect of Tax Incentives On The Growth of Smes in Rwanda: A Case Study of Smes in Nyarugenge DistrictMusondaNo ratings yet

- Tax 3 ASSIGNMENTDocument23 pagesTax 3 ASSIGNMENTPui YanNo ratings yet

- Package 2: Corporate Recovery and Tax Incentives For Enterprises (CREATE) ActDocument7 pagesPackage 2: Corporate Recovery and Tax Incentives For Enterprises (CREATE) ActGieanne Prudence VenculadoNo ratings yet

- Effect of Tax Incentives On The Growth of SMEs in RwandaDocument10 pagesEffect of Tax Incentives On The Growth of SMEs in RwandaBhosx KimNo ratings yet

- Mkuchajr ProposalDocument9 pagesMkuchajr ProposalinnocentmkuchajrNo ratings yet

- Agbm 102Document11 pagesAgbm 102skimanja0No ratings yet

- Dof-Train With TrabahoDocument56 pagesDof-Train With TrabahoMariver LlorenteNo ratings yet

- Train 2 or Trabaho Bill: (Tax Reform For Attracting Better and High-Quality Opportunities) House Bill No. 8083Document30 pagesTrain 2 or Trabaho Bill: (Tax Reform For Attracting Better and High-Quality Opportunities) House Bill No. 8083Azaria MatiasNo ratings yet

- Firb Advisory Faqs (Firms, Atir, and Abr)Document10 pagesFirb Advisory Faqs (Firms, Atir, and Abr)Asam Marie FernandezNo ratings yet

- GMAT-Session11 CRDocument8 pagesGMAT-Session11 CRhardy.contreras.silveraNo ratings yet

Download as docx, pdf, or txt

You might also like

- Chapter 10-Financial Reporting in Public SectorDocument22 pagesChapter 10-Financial Reporting in Public SectorRifky Kesuma100% (2)

- Corporate Financial Reporting - Government AccountingDocument21 pagesCorporate Financial Reporting - Government AccountingAAKASH TOMARNo ratings yet

- Sub Topic 1Document8 pagesSub Topic 1Marie TaylaranNo ratings yet

- OrganizedDocument72 pagesOrganizedhamidsayyed2002No ratings yet

- Government Accounting & Financial ReportingDocument37 pagesGovernment Accounting & Financial ReportingSony AxleNo ratings yet

- Assignment # 1: Submitted FromDocument15 pagesAssignment # 1: Submitted FromAbdullah AliNo ratings yet

- ACC709 Lecture 5Document38 pagesACC709 Lecture 5dt7813369No ratings yet

- Government Accounting SystemDocument46 pagesGovernment Accounting SystemMeshack NyekelelaNo ratings yet

- TOPIC 1 Fundamentals of AccountingDocument10 pagesTOPIC 1 Fundamentals of AccountingAnastasia MelnicovaNo ratings yet

- Chapter 1 Ethiopian Govt AcctingDocument22 pagesChapter 1 Ethiopian Govt Acctingwube100% (1)

- Functions of FBR / Revenue DivisionDocument7 pagesFunctions of FBR / Revenue DivisionWajahat GhafoorNo ratings yet

- ChapterDocument6 pagesChaptermaheshNo ratings yet

- ChapterDocument101 pagesChapterkamath16002No ratings yet

- Chapter 5 & 6Document8 pagesChapter 5 & 6HisyamNo ratings yet

- PTX - AssignmentDocument15 pagesPTX - AssignmentNUR ALEEYA MAISARAH BINTI MOHD NASIR (AS)No ratings yet

- 5acc224 Week One Introduction To Public Sector Accounting 2223Document33 pages5acc224 Week One Introduction To Public Sector Accounting 2223umuriegenevieveNo ratings yet

- Tax FinalDocument16 pagesTax FinalAnany UpadhyayNo ratings yet

- Rohith BcomDocument13 pagesRohith BcomubbapallyrudhiraNo ratings yet

- Direct Tax NotesDocument4 pagesDirect Tax Notesashutoshbhatra98No ratings yet

- Nadiavietta - 120110180071 - Research Methodology Chapter I - IiDocument10 pagesNadiavietta - 120110180071 - Research Methodology Chapter I - IiRasqi ArfakhsyadzNo ratings yet

- 01 Chapter 1 The Development of The Accounting ProfessionDocument3 pages01 Chapter 1 The Development of The Accounting Professionsoyoung kimNo ratings yet

- 270MEF-EN-Prakas On TaxAuditDocument9 pages270MEF-EN-Prakas On TaxAuditchannat zaboroskiNo ratings yet

- BAB II - Inggris Revisi 000001Document18 pagesBAB II - Inggris Revisi 000001Lydia KirbyNo ratings yet

- Income TaxDocument195 pagesIncome TaxAleti NithishNo ratings yet

- Income Tax DepartmentDocument88 pagesIncome Tax DepartmentkajalNo ratings yet

- Chapter One: Introduction To Federal Government of Ethiopia Accounting and Financial ManagementDocument61 pagesChapter One: Introduction To Federal Government of Ethiopia Accounting and Financial ManagementGirma100% (4)

- Functions of Budget:: Economic FunctionDocument10 pagesFunctions of Budget:: Economic FunctionAli BaigNo ratings yet

- Article About Provisional TaxDocument6 pagesArticle About Provisional Taxduanedejager01No ratings yet

- Présentation Des Comptes Consolidés Selon Le Plan Comptable - Chapitre 01 - Le Cadre Théorique Des États Financiers Et de La Consolidation 2Document14 pagesPrésentation Des Comptes Consolidés Selon Le Plan Comptable - Chapitre 01 - Le Cadre Théorique Des États Financiers Et de La Consolidation 2IK storeNo ratings yet

- Public Sector AccountingDocument15 pagesPublic Sector AccountingerutujirogoodluckNo ratings yet

- Operational Framework of Accrual Basis of Accounting in Governments in IndiaDocument19 pagesOperational Framework of Accrual Basis of Accounting in Governments in Indiasas examNo ratings yet

- 501-Direct Tax Laws and AccountsDocument19 pages501-Direct Tax Laws and Accountssuyash bajpaiNo ratings yet

- Historical Overview of Ethiopian Government Accounting SystemDocument20 pagesHistorical Overview of Ethiopian Government Accounting Systemnegamedhane58100% (3)

- An Overview of National Budget in BangladeshDocument4 pagesAn Overview of National Budget in BangladeshAnikaNo ratings yet

- Nature of Government AccountingDocument16 pagesNature of Government AccountingLJ AggabaoNo ratings yet

- In Elec111 - Government Accounting & Budgeting Padm 107 - Public Accounting & Budgeting)Document36 pagesIn Elec111 - Government Accounting & Budgeting Padm 107 - Public Accounting & Budgeting)Erika MonisNo ratings yet

- Financial StatementDocument7 pagesFinancial StatementEunice SorianoNo ratings yet

- Allan and CharlesDocument6 pagesAllan and CharlesNkuuwe EdmundNo ratings yet

- History of Income Tax in PakistanDocument37 pagesHistory of Income Tax in PakistanSoNaa BalochNo ratings yet

- New Government Accounting System (NGAS) in The PhilippinesDocument24 pagesNew Government Accounting System (NGAS) in The PhilippinesJingRellin100% (1)

- Difference Between Accounting and AuditDocument5 pagesDifference Between Accounting and AuditsrpvickyNo ratings yet

- Financial Accounting and Reporting: Consolidated FundDocument42 pagesFinancial Accounting and Reporting: Consolidated FundHAFIZAH BINTI MAT NAWINo ratings yet

- DTP Full NotesDocument114 pagesDTP Full NotesCHAITHRANo ratings yet

- Audit Report in Case of Non Statutionry and Non Profit OrgDocument5 pagesAudit Report in Case of Non Statutionry and Non Profit OrgVIJAY PAREEKNo ratings yet

- Reporting by Financial Situations and Annual Accounting Reports To Entities in RomaniaDocument10 pagesReporting by Financial Situations and Annual Accounting Reports To Entities in Romaniamoscu danielNo ratings yet

- TaxDocument15 pagesTaxAnuja GuptaNo ratings yet

- Mawlana Bhashani Science and Technology UniversityDocument20 pagesMawlana Bhashani Science and Technology UniversitySabbir Ahmed100% (1)

- Tax Law NotesDocument16 pagesTax Law NotesGauri BansalNo ratings yet

- Hrishad - Income TaxDocument9 pagesHrishad - Income Taxkhayyum0% (1)

- Financial Accounting and Reporting 01Document9 pagesFinancial Accounting and Reporting 01Nuah SilvestreNo ratings yet

- Neha Kushwaha ProjectDocument66 pagesNeha Kushwaha Projectbuccspan2022No ratings yet

- DC Tacn Ki IiDocument6 pagesDC Tacn Ki IiHà Phương TrầnNo ratings yet

- Audit Procedure in IndiaDocument29 pagesAudit Procedure in IndiaPendem Vamsi KrishnaNo ratings yet

- Accounting System in SpainDocument5 pagesAccounting System in SpainHailee HayesNo ratings yet

- Leac 203Document27 pagesLeac 203Ias Aspirant AbhiNo ratings yet

- Government AccountingDocument32 pagesGovernment AccountingPratik GoyalNo ratings yet

- Chapter 1 Nature and Scope of NGASDocument26 pagesChapter 1 Nature and Scope of NGASRia BagoNo ratings yet

- Income Tax Planning in India 1Document76 pagesIncome Tax Planning in India 1Mallika t0% (1)

- Acca F 8 L7Document16 pagesAcca F 8 L7Fahmi AbdullaNo ratings yet

- "The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"From Everand"The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"No ratings yet

- Finger Print ExpertDocument29 pagesFinger Print Expertumaima aliNo ratings yet

- Human RightsDocument10 pagesHuman Rightsumaima aliNo ratings yet

- Assignment TopicDocument8 pagesAssignment Topicumaima aliNo ratings yet

- Plaint BankingDocument6 pagesPlaint Bankingumaima ali100% (1)

- AHRP IBLG Chapter IIIDocument3 pagesAHRP IBLG Chapter IIIjsbw4ky26fNo ratings yet

- IncentivesDocument25 pagesIncentivesNikko Bait-itNo ratings yet

- Chapter 5. Tax Policy: Policy Framework For Investment User'S ToolkitDocument40 pagesChapter 5. Tax Policy: Policy Framework For Investment User'S ToolkitRediet UtteNo ratings yet

- Project Report For The Institute of Education and Also TradingDocument9 pagesProject Report For The Institute of Education and Also Tradingbhanjasomanath4No ratings yet

- ABM TextDocument6 pagesABM TextPauline TayabanNo ratings yet

- Practical Research 2Document24 pagesPractical Research 2Charlene DimayugaNo ratings yet

- Kassahun Final Thesis 2005 CTA EditedDocument93 pagesKassahun Final Thesis 2005 CTA EditedHannaNo ratings yet

- Taxation IssuesDocument23 pagesTaxation IssuesBianca Jane GaayonNo ratings yet

- Tax Incentives in Developing Countries - A Case Study-Singapore and PhilippinesDocument29 pagesTax Incentives in Developing Countries - A Case Study-Singapore and PhilippinesBhosx KimNo ratings yet

- Chapter Five 5. Investment IncentivesDocument12 pagesChapter Five 5. Investment IncentivesSeid KassawNo ratings yet

- Đầu tư QT - metroDocument66 pagesĐầu tư QT - metroMaiNo ratings yet

- Tax IncentivesDocument43 pagesTax Incentivesmay leeNo ratings yet

- JAO No 1-2019Document6 pagesJAO No 1-2019JoyceTanNo ratings yet

- Tax Competition For Foreign Direct Investment in ASEAN: Is Corporate Income Tax Harmonization The Solution?Document34 pagesTax Competition For Foreign Direct Investment in ASEAN: Is Corporate Income Tax Harmonization The Solution?MUC kediriNo ratings yet

- Chapter 15 Taxincentives Group3Document15 pagesChapter 15 Taxincentives Group3Rhenzo ManayanNo ratings yet

- Tax Incentives For Companies To Invest The Portuguese Case in 2019Document17 pagesTax Incentives For Companies To Invest The Portuguese Case in 2019Global Research and Development ServicesNo ratings yet

- Module 01 CREATE Law Tax IncentivesDocument30 pagesModule 01 CREATE Law Tax IncentivesMitch PacienteNo ratings yet

- ĐTQT ĐỀ CƯƠNG THI CUỐI KỲ 1Document9 pagesĐTQT ĐỀ CƯƠNG THI CUỐI KỲ 1hminlNo ratings yet

- Scopus (Macroeconomic Effects of Corporate Tax Policy)Document22 pagesScopus (Macroeconomic Effects of Corporate Tax Policy)aldapermatasari021No ratings yet

- Tax Incentives G. 07 BsDocument10 pagesTax Incentives G. 07 BsLevenson KadegheNo ratings yet

- Effect of Tax Incentives On The Growth of Smes in Rwanda: A Case Study of Smes in Nyarugenge DistrictDocument9 pagesEffect of Tax Incentives On The Growth of Smes in Rwanda: A Case Study of Smes in Nyarugenge DistrictMusondaNo ratings yet

- Tax 3 ASSIGNMENTDocument23 pagesTax 3 ASSIGNMENTPui YanNo ratings yet

- Package 2: Corporate Recovery and Tax Incentives For Enterprises (CREATE) ActDocument7 pagesPackage 2: Corporate Recovery and Tax Incentives For Enterprises (CREATE) ActGieanne Prudence VenculadoNo ratings yet

- Effect of Tax Incentives On The Growth of SMEs in RwandaDocument10 pagesEffect of Tax Incentives On The Growth of SMEs in RwandaBhosx KimNo ratings yet

- Mkuchajr ProposalDocument9 pagesMkuchajr ProposalinnocentmkuchajrNo ratings yet

- Agbm 102Document11 pagesAgbm 102skimanja0No ratings yet

- Dof-Train With TrabahoDocument56 pagesDof-Train With TrabahoMariver LlorenteNo ratings yet

- Train 2 or Trabaho Bill: (Tax Reform For Attracting Better and High-Quality Opportunities) House Bill No. 8083Document30 pagesTrain 2 or Trabaho Bill: (Tax Reform For Attracting Better and High-Quality Opportunities) House Bill No. 8083Azaria MatiasNo ratings yet

- Firb Advisory Faqs (Firms, Atir, and Abr)Document10 pagesFirb Advisory Faqs (Firms, Atir, and Abr)Asam Marie FernandezNo ratings yet

- GMAT-Session11 CRDocument8 pagesGMAT-Session11 CRhardy.contreras.silveraNo ratings yet