Download as pdf or txt

You might also like

- Schaum's Outline of Principles of Accounting I, Fifth EditionFrom EverandSchaum's Outline of Principles of Accounting I, Fifth EditionRating: 5 out of 5 stars5/5 (3)

- MAS-14 FS Analaysis With EFN (Letran)Document6 pagesMAS-14 FS Analaysis With EFN (Letran)Gio PacayraNo ratings yet

- Uk3 2011 Jun ADocument7 pagesUk3 2011 Jun AApple ChinNo ratings yet

- Uk3 2010 Jun ADocument7 pagesUk3 2010 Jun AApple ChinNo ratings yet

- Uk3 2009 Dec ADocument6 pagesUk3 2009 Dec AApple ChinNo ratings yet

- Int3 2010 Jun ADocument7 pagesInt3 2010 Jun AMARYNo ratings yet

- Acca Int3-2009-Dec-ADocument6 pagesAcca Int3-2009-Dec-AApple ChinNo ratings yet

- T31int 2010 Dec AnsDocument6 pagesT31int 2010 Dec AnsApple ChinNo ratings yet

- AAT AVBK AnswersDocument3 pagesAAT AVBK AnswersShailendra KelaniNo ratings yet

- Ans 03 06Document8 pagesAns 03 06samnan123No ratings yet

- 4 2008 Dec ADocument5 pages4 2008 Dec ALai Hui Ing100% (1)

- T4 June 07 AnsDocument6 pagesT4 June 07 AnssmhgilaniNo ratings yet

- F6UK 2014 Dec ADocument9 pagesF6UK 2014 Dec ALatoya JohnsonNo ratings yet

- Spreadsheet Chapter 04 SampleDocument25 pagesSpreadsheet Chapter 04 SampleDiệp Diệu ĐồngNo ratings yet

- 高顿财经ACCA acca.gaodun.cn: Advanced Performance ManagementDocument13 pages高顿财经ACCA acca.gaodun.cn: Advanced Performance ManagementIskandar BudionoNo ratings yet

- Acca Ma and Fma Management Accounting September 2018 To August 2019Document12 pagesAcca Ma and Fma Management Accounting September 2018 To August 20191 N Aaron AgarwalNo ratings yet

- Review2 Ch01 ADocument1 pageReview2 Ch01 AMayy ElleNo ratings yet

- Accounting Question For PreperationDocument8 pagesAccounting Question For PreperationPiyam RazaNo ratings yet

- Spreadsheet - Chapter - 04 - Sample 1Document25 pagesSpreadsheet - Chapter - 04 - Sample 1Diệp Diệu ĐồngNo ratings yet

- Preparing Financial Statements: (UK Stream)Document15 pagesPreparing Financial Statements: (UK Stream)LincolnYNo ratings yet

- Chapter 2 - Control AccountsDocument9 pagesChapter 2 - Control Accountsmelody shayanwakoNo ratings yet

- Cash Flow Projection YEAR2Document2 pagesCash Flow Projection YEAR2Ditiro KgotlaNo ratings yet

- TXUK 2019 MarJun ADocument11 pagesTXUK 2019 MarJun AmdNo ratings yet

- Irc Kit JJ20Document35 pagesIrc Kit JJ20Amir ArifNo ratings yet

- Liabilities and Fund BalancesDocument4 pagesLiabilities and Fund Balancesjohn_allison5873No ratings yet

- AFAR1 Partnership Formation SolutionDocument3 pagesAFAR1 Partnership Formation SolutionVenti AlexisNo ratings yet

- The Colony Towers Financial STMTSDocument8 pagesThe Colony Towers Financial STMTSRikki ThompsonNo ratings yet

- Answers To Questions For Chapter 9 Measuring Relevant Costs and Revenues For Decision-MakingDocument7 pagesAnswers To Questions For Chapter 9 Measuring Relevant Costs and Revenues For Decision-MakingElizabeth Del RosarioNo ratings yet

- p7sgp 2011 Dec QDocument10 pagesp7sgp 2011 Dec QamNo ratings yet

- 2019 FBS 200 Exam Solution FINALDocument11 pages2019 FBS 200 Exam Solution FINALger pingNo ratings yet

- MT2 Ch02Document24 pagesMT2 Ch02api-3725162No ratings yet

- Working Capital (ST15)Document2 pagesWorking Capital (ST15)John SamonteNo ratings yet

- T-aacountsDocument8 pagesT-aacountssattharit2No ratings yet

- 2-3mwi 2004 Dec ADocument13 pages2-3mwi 2004 Dec Aanga100% (1)

- MQP ANS 01 NDocument13 pagesMQP ANS 01 NAVINASH ROYNo ratings yet

- Problem 12-10 SolutionDocument9 pagesProblem 12-10 SolutionKELLY DANGNo ratings yet

- Intacc Cash Flow SolutionDocument3 pagesIntacc Cash Flow SolutionMila MercadoNo ratings yet

- 10-Department Sol. For M23Document1 page10-Department Sol. For M23rs3594024No ratings yet

- Acca Paper F3 Financial Accounting (International Stream) Question Day - Final Mock ExaminationDocument8 pagesAcca Paper F3 Financial Accounting (International Stream) Question Day - Final Mock ExaminationuzshahNo ratings yet

- This Study Resource Was: Guerrero / German Siy / de Jesus / Lim / FerrerDocument5 pagesThis Study Resource Was: Guerrero / German Siy / de Jesus / Lim / FerrerKyla Dane P. PradoNo ratings yet

- Chapter 7 SolutionsDocument8 pagesChapter 7 SolutionsAustin LeeNo ratings yet

- 2006 - Dec - Ans CAT T3Document7 pages2006 - Dec - Ans CAT T3asad19No ratings yet

- Finance ReportsDocument2 pagesFinance ReportsCristian MiunsipNo ratings yet

- Ans m2 PaperDocument6 pagesAns m2 Paperbigab31327No ratings yet

- Lecture 3 - Practice AnswerDocument11 pagesLecture 3 - Practice AnswerBhunesh KumarNo ratings yet

- Philippine Politics and Governance DLPDocument6 pagesPhilippine Politics and Governance DLPDMarrie Abao Boniao-LabadanNo ratings yet

- TXUK 2019 SepDec - ADocument10 pagesTXUK 2019 SepDec - AmdNo ratings yet

- MFA Test 1 SolutionDocument4 pagesMFA Test 1 SolutionMuhammad ImranNo ratings yet

- 4 2005 Jun ADocument7 pages4 2005 Jun Aapi-19836745No ratings yet

- F7 SolutionsDocument15 pagesF7 Solutionsnoor ul anum100% (1)

- CPA 1 - Financial Acconting Sep 2022Document10 pagesCPA 1 - Financial Acconting Sep 2022Asaba GloriaNo ratings yet

- June 2009 Fa4a1Document9 pagesJune 2009 Fa4a1ksakala58No ratings yet

- 2015 Jun Ans-7Document1 page2015 Jun Ans-7何健珩No ratings yet

- 2009 S3 Ase2007Document15 pages2009 S3 Ase2007May CcmNo ratings yet

- Acc Vol 1 Chap 4 SolDocument78 pagesAcc Vol 1 Chap 4 Solkhushichandak07No ratings yet

- AnswersDocument8 pagesAnswersNirmal ShresthaNo ratings yet

- 2023 - 2024 - Class - Xii - Accountancy - First Pre Board - Set - C - MSDocument11 pages2023 - 2024 - Class - Xii - Accountancy - First Pre Board - Set - C - MScommerce12onlineclassesNo ratings yet

- Basu Deb SharmaDocument1 pageBasu Deb SharmaBasudev SharmaNo ratings yet

- Equity Valuation: Models from Leading Investment BanksFrom EverandEquity Valuation: Models from Leading Investment BanksJan ViebigNo ratings yet

- Module 3 Analysis of Financial StatementsDocument24 pagesModule 3 Analysis of Financial StatementsErick Mequiso100% (1)

- Score Report - Cibil DashboardDocument57 pagesScore Report - Cibil DashboardkingdemoinNo ratings yet

- Exercise On Bank ReconciliationDocument3 pagesExercise On Bank ReconciliationJoshua OtienoNo ratings yet

- Broadening Tops and BottomsDocument7 pagesBroadening Tops and BottomsURLUCKYNo ratings yet

- Accounting StandardsDocument2 pagesAccounting StandardsAseem1No ratings yet

- Financial AccountingDocument233 pagesFinancial AccountingJyoti ThatheraNo ratings yet

- AP.3501 Audit of InventoriesDocument7 pagesAP.3501 Audit of InventoriesMarinoNo ratings yet

- Valuation Concepts and Methods EssayDocument2 pagesValuation Concepts and Methods EssayChristine MadecNo ratings yet

- Chap012 2Document125 pagesChap012 2Aai NurrNo ratings yet

- Mk1-Performance-Conversions - Co.uk: British Leyland Motor Corporation 1969 Report and AccountsDocument36 pagesMk1-Performance-Conversions - Co.uk: British Leyland Motor Corporation 1969 Report and AccountsKorrolocoNo ratings yet

- Financial Ratio Analysis of Bangladesh Engineering SectorDocument5 pagesFinancial Ratio Analysis of Bangladesh Engineering SectorAhmed NafiuNo ratings yet

- Gopal Limited: (Please Scan This QR Code To View The RHP)Document504 pagesGopal Limited: (Please Scan This QR Code To View The RHP)skyrizz12No ratings yet

- UntitledDocument3,876 pagesUntitledAng'ila JuniorNo ratings yet

- Household Statement W - Summary For December 2023Document12 pagesHousehold Statement W - Summary For December 2023Randy WrightNo ratings yet

- Walter ModelDocument3 pagesWalter ModelSidhesh MittalNo ratings yet

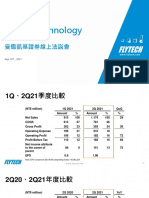

- Flytech TechnologyDocument7 pagesFlytech TechnologyLouis ChenNo ratings yet

- Chapter 11 BKMDocument7 pagesChapter 11 BKMNatalie OngNo ratings yet

- Consolidation by Sir ARM v2Document91 pagesConsolidation by Sir ARM v2Shah ZaibNo ratings yet

- FN2191 Commentary 2022Document27 pagesFN2191 Commentary 2022slimshadyNo ratings yet

- Cash Flow Statement: Performa and ProblemsDocument52 pagesCash Flow Statement: Performa and Problems727822TPMB005 ARAVINTHAN.SNo ratings yet

- Economic Evaluation of Capital Expenditures: Multiple ChoiceDocument14 pagesEconomic Evaluation of Capital Expenditures: Multiple ChoiceGweeenchanaNo ratings yet

- ACC 610 Final Project SubmissionDocument26 pagesACC 610 Final Project SubmissionvincentNo ratings yet

- Chapter 9 - HW SolutionsDocument7 pagesChapter 9 - HW Solutionsa8829060% (1)

- Fabm 1 LeapDocument4 pagesFabm 1 Leapanna paulaNo ratings yet

- RKG Imp Q (CH 1 & 2) DoneDocument3 pagesRKG Imp Q (CH 1 & 2) Donepriyanshi.bansal25No ratings yet

- Retail Financial ModelingDocument43 pagesRetail Financial ModelingtsohNo ratings yet

- Vikas Provisional ComputationDocument6 pagesVikas Provisional ComputationAmit TyagiNo ratings yet

- Funding of AcquisitionsDocument41 pagesFunding of AcquisitionssandipNo ratings yet

- Multiple Choice QuestionsDocument82 pagesMultiple Choice QuestionsJohn Rey EnriquezNo ratings yet