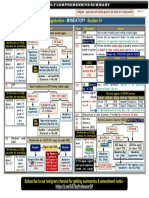

Topic 9 - Registration Under GST

Topic 9 - Registration Under GST

You might also like

- Bir Form 1905 New VersionDocument4 pagesBir Form 1905 New Versionchato law office100% (1)

- Domicile CertificateDocument7 pagesDomicile Certificatesyed.jerjees.haider100% (1)

- Terpin V AttDocument69 pagesTerpin V AttAnonymous PpmcLJSj0lNo ratings yet

- GST NotesDocument156 pagesGST NotesNishthaNo ratings yet

- Registration: GlimpsesDocument12 pagesRegistration: GlimpsesAdventure TimeNo ratings yet

- GST Law in Brief and Chart 2021Document18 pagesGST Law in Brief and Chart 2021sukumar basuNo ratings yet

- DP Classes CA Final IDT May 2021 Module 3Document235 pagesDP Classes CA Final IDT May 2021 Module 3Sathwika DevarapalliNo ratings yet

- Chapter 9 - RegistrationDocument20 pagesChapter 9 - Registrationcloudhunter910No ratings yet

- RegistrationDocument14 pagesRegistrationArnav AggarwalNo ratings yet

- Registration Under GSTDocument36 pagesRegistration Under GSTHarshit JhaNo ratings yet

- Section - 24 GST REGDocument1 pageSection - 24 GST REGraj pandeyNo ratings yet

- REGISTRATION SummaryDocument11 pagesREGISTRATION Summarymufaiz darNo ratings yet

- 411 Flow Chart GST 1 GST NotesDocument24 pages411 Flow Chart GST 1 GST Noteskaranprajapatu9737No ratings yet

- Future Value TablesDocument123 pagesFuture Value TablesShankar ReddyNo ratings yet

- Idt 5Document5 pagesIdt 5manan agrawalNo ratings yet

- Book 2Document34 pagesBook 2Kritika JainNo ratings yet

- Registration in GST NovDocument8 pagesRegistration in GST Novvinod.sale1No ratings yet

- Registration Under GST Law NewDocument3 pagesRegistration Under GST Law NewSunilNo ratings yet

- Input Tax Credi-WPS OfficeDocument9 pagesInput Tax Credi-WPS Officeanamaikaprince369No ratings yet

- Valuable Consideration: Made SupplyDocument22 pagesValuable Consideration: Made SupplyJaihindNo ratings yet

- Levy and Collection of TaxDocument22 pagesLevy and Collection of Tax7013 Arpit DubeyNo ratings yet

- Registration of CGSTDocument3 pagesRegistration of CGSTambikaagarwal1934No ratings yet

- GST Year End Checklist FY 2022-23-NynDocument4 pagesGST Year End Checklist FY 2022-23-NynCA Rajendra Prasad ANo ratings yet

- Standardised PPT On GST: Indirect Taxes Committee The Institute of Chartered Accountants of IndiaDocument31 pagesStandardised PPT On GST: Indirect Taxes Committee The Institute of Chartered Accountants of IndiaFreudestein UditNo ratings yet

- Goods & Service Tax (GST) Is A Huge Reform For Indirect Taxation in IndiaDocument49 pagesGoods & Service Tax (GST) Is A Huge Reform For Indirect Taxation in IndiaGauharNo ratings yet

- GST SummaryDocument72 pagesGST SummaryRishi CharanNo ratings yet

- GST-Divyastra-Ch-8-Registration-R-2Document12 pagesGST-Divyastra-Ch-8-Registration-R-2djvishaljainNo ratings yet

- S. No. Questions / Tweets Received Replies: Tweet FaqsDocument9 pagesS. No. Questions / Tweets Received Replies: Tweet FaqsM MangalNo ratings yet

- GST ChecklistDocument19 pagesGST ChecklistAakash BamniyaNo ratings yet

- Indirect TaxDocument14 pagesIndirect TaxAzulfa Sultan.No ratings yet

- GST Under Reverse Charge On Goods Transport Agency (GTA)Document2 pagesGST Under Reverse Charge On Goods Transport Agency (GTA)Deepak NimmojiNo ratings yet

- Satish Pradhan Dnyanasadhana College: Department of BMS Sample MCQ Questions Subject: Indirect TaxDocument5 pagesSatish Pradhan Dnyanasadhana College: Department of BMS Sample MCQ Questions Subject: Indirect TaxSallu SaleemNo ratings yet

- IDT Saar CA Final CH 8 Input Tax Credit by CA Mahesh Gour Handwritten NotesDocument27 pagesIDT Saar CA Final CH 8 Input Tax Credit by CA Mahesh Gour Handwritten NotesRonita DuttaNo ratings yet

- Sales Tax Last Hour SummaryDocument5 pagesSales Tax Last Hour SummaryboundaryblastsNo ratings yet

- Itc GSTDocument22 pagesItc GST311812922nishanthininkNo ratings yet

- Tax Law AssingmentDocument14 pagesTax Law AssingmentLov AnanadNo ratings yet

- Tweet Faqs: S. No. Questions / Tweets Received RepliesDocument9 pagesTweet Faqs: S. No. Questions / Tweets Received RepliesSumeet MehtaNo ratings yet

- GST Registration – A Detailed Analysis - Taxguru - inDocument6 pagesGST Registration – A Detailed Analysis - Taxguru - indivyanshi guptaNo ratings yet

- EKM ICAI Material 287181Document66 pagesEKM ICAI Material 287181DIYA MALNo ratings yet

- Income Tax Threshold Limits 2021Document24 pagesIncome Tax Threshold Limits 2021Harty RobertNo ratings yet

- GST Registration PPT Ver6 28042017Document46 pagesGST Registration PPT Ver6 28042017Sonal AggarwalNo ratings yet

- GST Presentation MsmeDocument114 pagesGST Presentation MsmeViky AkNo ratings yet

- VAT Theory Question Answer by Subash NepalDocument13 pagesVAT Theory Question Answer by Subash Nepalssah4155No ratings yet

- GST Remark Related FileDocument14 pagesGST Remark Related FileAnonymous ikQZphNo ratings yet

- GST Registration (Sec 22)Document5 pagesGST Registration (Sec 22)Shubakar ReddyNo ratings yet

- Input Tax Credit: Cma Bibhudatta SarangiDocument3 pagesInput Tax Credit: Cma Bibhudatta SarangihanumanthaiahgowdaNo ratings yet

- GST Presentation 15032019Document113 pagesGST Presentation 15032019Viky AkNo ratings yet

- GST at A GlanceDocument10 pagesGST at A Glancestr690No ratings yet

- Tax Provisions For Input Tax Credit - Job Work, EcommerceDocument6 pagesTax Provisions For Input Tax Credit - Job Work, Ecommercemayankmehul12No ratings yet

- Presentation ON: Goods and Service Tax: Applicability, Itc and ReturnsDocument31 pagesPresentation ON: Goods and Service Tax: Applicability, Itc and ReturnsSonal AggarwalNo ratings yet

- GST Unit VDocument29 pagesGST Unit VMani Maran123No ratings yet

- Session 3 & 4 - Input Tax Credit and Cross Utilisation of Taxes FinalDocument42 pagesSession 3 & 4 - Input Tax Credit and Cross Utilisation of Taxes FinalaskNo ratings yet

- 2020 Bustax - VAT - Part1 - Handouts PDFDocument13 pages2020 Bustax - VAT - Part1 - Handouts PDFMila MercadoNo ratings yet

- Reverse Charge MechanismDocument3 pagesReverse Charge MechanismARJUNNo ratings yet

- 6.input Tax CreditDocument24 pages6.input Tax CreditBhuvaneswari karuturiNo ratings yet

- CA Ashish Chaudhary 1Document30 pagesCA Ashish Chaudhary 1sonapakhi nandyNo ratings yet

- Section: A MCQ 20X1 20 Marks: A. B. C. DDocument12 pagesSection: A MCQ 20X1 20 Marks: A. B. C. DSarath KumarNo ratings yet

- GST Overview Rachana 1Document31 pagesGST Overview Rachana 1Path A Way AheadNo ratings yet

- GST Itc DetailDocument8 pagesGST Itc DetailAnonymous ikQZphNo ratings yet

- Cross Border B2C (Business To Consumer) Services Provided in Taxable Territory Cross Border B2B (Business To Business) Services OidarDocument16 pagesCross Border B2C (Business To Consumer) Services Provided in Taxable Territory Cross Border B2B (Business To Business) Services OidarSushant SaxenaNo ratings yet

- Amendment Final N2020 BGSirDocument30 pagesAmendment Final N2020 BGSirAfnan KhanNo ratings yet

- VAT HandoutDocument34 pagesVAT HandoutAira Mae MendozaNo ratings yet

- Contract CostingDocument7 pagesContract CostingMehul GuptaNo ratings yet

- Budgetary ControlDocument10 pagesBudgetary ControlMehul GuptaNo ratings yet

- Ca Inter (GST Only) Ca Vijender AggarwalDocument1 pageCa Inter (GST Only) Ca Vijender AggarwalMehul GuptaNo ratings yet

- Assets.: (Vi) Due To Lack of Information, Depreciation Has Not Been Provided On FixedDocument6 pagesAssets.: (Vi) Due To Lack of Information, Depreciation Has Not Been Provided On FixedMehul Gupta100% (1)

- Products & Services - ValuepitchDocument17 pagesProducts & Services - Valuepitchtiger SNo ratings yet

- Mini Mein Deutschheft 2018Document29 pagesMini Mein Deutschheft 2018nizam petaNo ratings yet

- Registration Certificate Government of MaharashtraDocument4 pagesRegistration Certificate Government of MaharashtraSujal RajNo ratings yet

- New Request Form DeathDocument2 pagesNew Request Form Deathzanderhero30No ratings yet

- CS Form No. 6, Revised 2020 (Application For Leave) - UPVDocument2 pagesCS Form No. 6, Revised 2020 (Application For Leave) - UPVEmaylyn Villegas100% (1)

- Petition To Annul Contract of LeaseDocument4 pagesPetition To Annul Contract of LeaseJulie SaliliNo ratings yet

- Summary of Section 800Document21 pagesSummary of Section 800Alicia Jewel HolgadoNo ratings yet

- Annexure B - KYC Change Address IndividualDocument2 pagesAnnexure B - KYC Change Address IndividualVinay Kumar0% (1)

- Indian Air Force: Air Force Common Admission Test Admit Card - Afcat 02/2020 (Afcat & Ekt)Document6 pagesIndian Air Force: Air Force Common Admission Test Admit Card - Afcat 02/2020 (Afcat & Ekt)Ahmad RehanNo ratings yet

- Army Public Schools: Candidate's Signature (In Front of Invigilator at The Exam Center)Document1 pageArmy Public Schools: Candidate's Signature (In Front of Invigilator at The Exam Center)Shah AasifNo ratings yet

- MARRIAGE AND CIVIL PARTNERSHIP CEREMONY GUIDANCE NOTES GibraltarDocument17 pagesMARRIAGE AND CIVIL PARTNERSHIP CEREMONY GUIDANCE NOTES GibraltarVladGrigoreNo ratings yet

- Skillful Student Book Answer KeyDocument14 pagesSkillful Student Book Answer KeyThắm Lê ThịNo ratings yet

- Guide OndatoDocument9 pagesGuide OndatoDucks TeeNo ratings yet

- Abstract On BiometricsDocument9 pagesAbstract On BiometricsBleu Oiseau100% (1)

- NOAA Intro To Security AwarenessDocument15 pagesNOAA Intro To Security AwarenessShinosuke ShinjanNo ratings yet

- PCSP Sales Service Training MAY 15 - PCSPDocument33 pagesPCSP Sales Service Training MAY 15 - PCSPmilea vladNo ratings yet

- Podanur PDFDocument60 pagesPodanur PDFabhijithNo ratings yet

- Schema 2017Document57 pagesSchema 2017Sreenath NairNo ratings yet

- R E M Ind Er S:: UHC v.1 January 2020Document2 pagesR E M Ind Er S:: UHC v.1 January 2020Melody Frac ZapateroNo ratings yet

- Republic of The Philippines Metro Manila Twelfth Congress Third Regular SessionDocument13 pagesRepublic of The Philippines Metro Manila Twelfth Congress Third Regular SessionRoland CepedaNo ratings yet

- 2017 BuletinDocument17 pages2017 BuletinzolalkkNo ratings yet

- Open Membership Form - 1.0Document1 pageOpen Membership Form - 1.0vijayindia87100% (8)

- IRR of SIRVDocument11 pagesIRR of SIRVRickmon Albert AlcantaraNo ratings yet

- ICON Student Registration FormDocument4 pagesICON Student Registration FormGeorgios BarkasNo ratings yet

- ABirla Common Appln FormDocument92 pagesABirla Common Appln FormJason Kenneth D’SilvaNo ratings yet

- MFT Written Exam HandbookDocument17 pagesMFT Written Exam HandbookSA_VialNo ratings yet

- WWW - Pica.gov - JM Wp-Content Uploads 2014 06 Jamaica-Passport-Application-Compressed PDFDocument6 pagesWWW - Pica.gov - JM Wp-Content Uploads 2014 06 Jamaica-Passport-Application-Compressed PDFlorna_thomas3348No ratings yet

Download as pdf or txt

You might also like

- Bir Form 1905 New VersionDocument4 pagesBir Form 1905 New Versionchato law office100% (1)

- Domicile CertificateDocument7 pagesDomicile Certificatesyed.jerjees.haider100% (1)

- Terpin V AttDocument69 pagesTerpin V AttAnonymous PpmcLJSj0lNo ratings yet

- GST NotesDocument156 pagesGST NotesNishthaNo ratings yet

- Registration: GlimpsesDocument12 pagesRegistration: GlimpsesAdventure TimeNo ratings yet

- GST Law in Brief and Chart 2021Document18 pagesGST Law in Brief and Chart 2021sukumar basuNo ratings yet

- DP Classes CA Final IDT May 2021 Module 3Document235 pagesDP Classes CA Final IDT May 2021 Module 3Sathwika DevarapalliNo ratings yet

- Chapter 9 - RegistrationDocument20 pagesChapter 9 - Registrationcloudhunter910No ratings yet

- RegistrationDocument14 pagesRegistrationArnav AggarwalNo ratings yet

- Registration Under GSTDocument36 pagesRegistration Under GSTHarshit JhaNo ratings yet

- Section - 24 GST REGDocument1 pageSection - 24 GST REGraj pandeyNo ratings yet

- REGISTRATION SummaryDocument11 pagesREGISTRATION Summarymufaiz darNo ratings yet

- 411 Flow Chart GST 1 GST NotesDocument24 pages411 Flow Chart GST 1 GST Noteskaranprajapatu9737No ratings yet

- Future Value TablesDocument123 pagesFuture Value TablesShankar ReddyNo ratings yet

- Idt 5Document5 pagesIdt 5manan agrawalNo ratings yet

- Book 2Document34 pagesBook 2Kritika JainNo ratings yet

- Registration in GST NovDocument8 pagesRegistration in GST Novvinod.sale1No ratings yet

- Registration Under GST Law NewDocument3 pagesRegistration Under GST Law NewSunilNo ratings yet

- Input Tax Credi-WPS OfficeDocument9 pagesInput Tax Credi-WPS Officeanamaikaprince369No ratings yet

- Valuable Consideration: Made SupplyDocument22 pagesValuable Consideration: Made SupplyJaihindNo ratings yet

- Levy and Collection of TaxDocument22 pagesLevy and Collection of Tax7013 Arpit DubeyNo ratings yet

- Registration of CGSTDocument3 pagesRegistration of CGSTambikaagarwal1934No ratings yet

- GST Year End Checklist FY 2022-23-NynDocument4 pagesGST Year End Checklist FY 2022-23-NynCA Rajendra Prasad ANo ratings yet

- Standardised PPT On GST: Indirect Taxes Committee The Institute of Chartered Accountants of IndiaDocument31 pagesStandardised PPT On GST: Indirect Taxes Committee The Institute of Chartered Accountants of IndiaFreudestein UditNo ratings yet

- Goods & Service Tax (GST) Is A Huge Reform For Indirect Taxation in IndiaDocument49 pagesGoods & Service Tax (GST) Is A Huge Reform For Indirect Taxation in IndiaGauharNo ratings yet

- GST SummaryDocument72 pagesGST SummaryRishi CharanNo ratings yet

- GST-Divyastra-Ch-8-Registration-R-2Document12 pagesGST-Divyastra-Ch-8-Registration-R-2djvishaljainNo ratings yet

- S. No. Questions / Tweets Received Replies: Tweet FaqsDocument9 pagesS. No. Questions / Tweets Received Replies: Tweet FaqsM MangalNo ratings yet

- GST ChecklistDocument19 pagesGST ChecklistAakash BamniyaNo ratings yet

- Indirect TaxDocument14 pagesIndirect TaxAzulfa Sultan.No ratings yet

- GST Under Reverse Charge On Goods Transport Agency (GTA)Document2 pagesGST Under Reverse Charge On Goods Transport Agency (GTA)Deepak NimmojiNo ratings yet

- Satish Pradhan Dnyanasadhana College: Department of BMS Sample MCQ Questions Subject: Indirect TaxDocument5 pagesSatish Pradhan Dnyanasadhana College: Department of BMS Sample MCQ Questions Subject: Indirect TaxSallu SaleemNo ratings yet

- IDT Saar CA Final CH 8 Input Tax Credit by CA Mahesh Gour Handwritten NotesDocument27 pagesIDT Saar CA Final CH 8 Input Tax Credit by CA Mahesh Gour Handwritten NotesRonita DuttaNo ratings yet

- Sales Tax Last Hour SummaryDocument5 pagesSales Tax Last Hour SummaryboundaryblastsNo ratings yet

- Itc GSTDocument22 pagesItc GST311812922nishanthininkNo ratings yet

- Tax Law AssingmentDocument14 pagesTax Law AssingmentLov AnanadNo ratings yet

- Tweet Faqs: S. No. Questions / Tweets Received RepliesDocument9 pagesTweet Faqs: S. No. Questions / Tweets Received RepliesSumeet MehtaNo ratings yet

- GST Registration – A Detailed Analysis - Taxguru - inDocument6 pagesGST Registration – A Detailed Analysis - Taxguru - indivyanshi guptaNo ratings yet

- EKM ICAI Material 287181Document66 pagesEKM ICAI Material 287181DIYA MALNo ratings yet

- Income Tax Threshold Limits 2021Document24 pagesIncome Tax Threshold Limits 2021Harty RobertNo ratings yet

- GST Registration PPT Ver6 28042017Document46 pagesGST Registration PPT Ver6 28042017Sonal AggarwalNo ratings yet

- GST Presentation MsmeDocument114 pagesGST Presentation MsmeViky AkNo ratings yet

- VAT Theory Question Answer by Subash NepalDocument13 pagesVAT Theory Question Answer by Subash Nepalssah4155No ratings yet

- GST Remark Related FileDocument14 pagesGST Remark Related FileAnonymous ikQZphNo ratings yet

- GST Registration (Sec 22)Document5 pagesGST Registration (Sec 22)Shubakar ReddyNo ratings yet

- Input Tax Credit: Cma Bibhudatta SarangiDocument3 pagesInput Tax Credit: Cma Bibhudatta SarangihanumanthaiahgowdaNo ratings yet

- GST Presentation 15032019Document113 pagesGST Presentation 15032019Viky AkNo ratings yet

- GST at A GlanceDocument10 pagesGST at A Glancestr690No ratings yet

- Tax Provisions For Input Tax Credit - Job Work, EcommerceDocument6 pagesTax Provisions For Input Tax Credit - Job Work, Ecommercemayankmehul12No ratings yet

- Presentation ON: Goods and Service Tax: Applicability, Itc and ReturnsDocument31 pagesPresentation ON: Goods and Service Tax: Applicability, Itc and ReturnsSonal AggarwalNo ratings yet

- GST Unit VDocument29 pagesGST Unit VMani Maran123No ratings yet

- Session 3 & 4 - Input Tax Credit and Cross Utilisation of Taxes FinalDocument42 pagesSession 3 & 4 - Input Tax Credit and Cross Utilisation of Taxes FinalaskNo ratings yet

- 2020 Bustax - VAT - Part1 - Handouts PDFDocument13 pages2020 Bustax - VAT - Part1 - Handouts PDFMila MercadoNo ratings yet

- Reverse Charge MechanismDocument3 pagesReverse Charge MechanismARJUNNo ratings yet

- 6.input Tax CreditDocument24 pages6.input Tax CreditBhuvaneswari karuturiNo ratings yet

- CA Ashish Chaudhary 1Document30 pagesCA Ashish Chaudhary 1sonapakhi nandyNo ratings yet

- Section: A MCQ 20X1 20 Marks: A. B. C. DDocument12 pagesSection: A MCQ 20X1 20 Marks: A. B. C. DSarath KumarNo ratings yet

- GST Overview Rachana 1Document31 pagesGST Overview Rachana 1Path A Way AheadNo ratings yet

- GST Itc DetailDocument8 pagesGST Itc DetailAnonymous ikQZphNo ratings yet

- Cross Border B2C (Business To Consumer) Services Provided in Taxable Territory Cross Border B2B (Business To Business) Services OidarDocument16 pagesCross Border B2C (Business To Consumer) Services Provided in Taxable Territory Cross Border B2B (Business To Business) Services OidarSushant SaxenaNo ratings yet

- Amendment Final N2020 BGSirDocument30 pagesAmendment Final N2020 BGSirAfnan KhanNo ratings yet

- VAT HandoutDocument34 pagesVAT HandoutAira Mae MendozaNo ratings yet

- Contract CostingDocument7 pagesContract CostingMehul GuptaNo ratings yet

- Budgetary ControlDocument10 pagesBudgetary ControlMehul GuptaNo ratings yet

- Ca Inter (GST Only) Ca Vijender AggarwalDocument1 pageCa Inter (GST Only) Ca Vijender AggarwalMehul GuptaNo ratings yet

- Assets.: (Vi) Due To Lack of Information, Depreciation Has Not Been Provided On FixedDocument6 pagesAssets.: (Vi) Due To Lack of Information, Depreciation Has Not Been Provided On FixedMehul Gupta100% (1)

- Products & Services - ValuepitchDocument17 pagesProducts & Services - Valuepitchtiger SNo ratings yet

- Mini Mein Deutschheft 2018Document29 pagesMini Mein Deutschheft 2018nizam petaNo ratings yet

- Registration Certificate Government of MaharashtraDocument4 pagesRegistration Certificate Government of MaharashtraSujal RajNo ratings yet

- New Request Form DeathDocument2 pagesNew Request Form Deathzanderhero30No ratings yet

- CS Form No. 6, Revised 2020 (Application For Leave) - UPVDocument2 pagesCS Form No. 6, Revised 2020 (Application For Leave) - UPVEmaylyn Villegas100% (1)

- Petition To Annul Contract of LeaseDocument4 pagesPetition To Annul Contract of LeaseJulie SaliliNo ratings yet

- Summary of Section 800Document21 pagesSummary of Section 800Alicia Jewel HolgadoNo ratings yet

- Annexure B - KYC Change Address IndividualDocument2 pagesAnnexure B - KYC Change Address IndividualVinay Kumar0% (1)

- Indian Air Force: Air Force Common Admission Test Admit Card - Afcat 02/2020 (Afcat & Ekt)Document6 pagesIndian Air Force: Air Force Common Admission Test Admit Card - Afcat 02/2020 (Afcat & Ekt)Ahmad RehanNo ratings yet

- Army Public Schools: Candidate's Signature (In Front of Invigilator at The Exam Center)Document1 pageArmy Public Schools: Candidate's Signature (In Front of Invigilator at The Exam Center)Shah AasifNo ratings yet

- MARRIAGE AND CIVIL PARTNERSHIP CEREMONY GUIDANCE NOTES GibraltarDocument17 pagesMARRIAGE AND CIVIL PARTNERSHIP CEREMONY GUIDANCE NOTES GibraltarVladGrigoreNo ratings yet

- Skillful Student Book Answer KeyDocument14 pagesSkillful Student Book Answer KeyThắm Lê ThịNo ratings yet

- Guide OndatoDocument9 pagesGuide OndatoDucks TeeNo ratings yet

- Abstract On BiometricsDocument9 pagesAbstract On BiometricsBleu Oiseau100% (1)

- NOAA Intro To Security AwarenessDocument15 pagesNOAA Intro To Security AwarenessShinosuke ShinjanNo ratings yet

- PCSP Sales Service Training MAY 15 - PCSPDocument33 pagesPCSP Sales Service Training MAY 15 - PCSPmilea vladNo ratings yet

- Podanur PDFDocument60 pagesPodanur PDFabhijithNo ratings yet

- Schema 2017Document57 pagesSchema 2017Sreenath NairNo ratings yet

- R E M Ind Er S:: UHC v.1 January 2020Document2 pagesR E M Ind Er S:: UHC v.1 January 2020Melody Frac ZapateroNo ratings yet

- Republic of The Philippines Metro Manila Twelfth Congress Third Regular SessionDocument13 pagesRepublic of The Philippines Metro Manila Twelfth Congress Third Regular SessionRoland CepedaNo ratings yet

- 2017 BuletinDocument17 pages2017 BuletinzolalkkNo ratings yet

- Open Membership Form - 1.0Document1 pageOpen Membership Form - 1.0vijayindia87100% (8)

- IRR of SIRVDocument11 pagesIRR of SIRVRickmon Albert AlcantaraNo ratings yet

- ICON Student Registration FormDocument4 pagesICON Student Registration FormGeorgios BarkasNo ratings yet

- ABirla Common Appln FormDocument92 pagesABirla Common Appln FormJason Kenneth D’SilvaNo ratings yet

- MFT Written Exam HandbookDocument17 pagesMFT Written Exam HandbookSA_VialNo ratings yet

- WWW - Pica.gov - JM Wp-Content Uploads 2014 06 Jamaica-Passport-Application-Compressed PDFDocument6 pagesWWW - Pica.gov - JM Wp-Content Uploads 2014 06 Jamaica-Passport-Application-Compressed PDFlorna_thomas3348No ratings yet