Download as pdf or txt

You might also like

- Insurance Commission Exam ReviewerDocument5 pagesInsurance Commission Exam ReviewerApolinar Alvarez Jr.98% (40)

- Mobile Recharge Receipt FormatDocument9 pagesMobile Recharge Receipt FormatBSACET.tejNo ratings yet

- Brochure - Digital Transformation in InsuranceDocument8 pagesBrochure - Digital Transformation in Insurancewahyu sinawangNo ratings yet

- Bancassurance: Isha Chugh Assistant Professor Gargi College University of DelhiDocument29 pagesBancassurance: Isha Chugh Assistant Professor Gargi College University of Delhipallavi mishraNo ratings yet

- Consumer Protection Framework No.1-2017/BSDDocument37 pagesConsumer Protection Framework No.1-2017/BSDLucky MurindaNo ratings yet

- Bank PolicyDocument8 pagesBank PolicyJatinderPalNo ratings yet

- Hiver Savings AccountDocument6 pagesHiver Savings AccountAntony StarkNo ratings yet

- fg21 1Document57 pagesfg21 1Olivia Mihaela AlmasanNo ratings yet

- Customer Rights PolicyDocument8 pagesCustomer Rights PolicySiddhaa LNo ratings yet

- Faqs On Fair Treatment of Financial Consumers: Paragraph and Requirement AnswerDocument13 pagesFaqs On Fair Treatment of Financial Consumers: Paragraph and Requirement Answerfazh lpsvNo ratings yet

- Cir 01 Annexure IIIDocument8 pagesCir 01 Annexure IIIabidkilyaniNo ratings yet

- 2013 Adapt To UDAAPDocument6 pages2013 Adapt To UDAAPedpaalaNo ratings yet

- Customer Rights Policy 2023 24 Website Upload 01042023Document9 pagesCustomer Rights Policy 2023 24 Website Upload 01042023Sahil AroraNo ratings yet

- AML CFT Guidelines RiskBasedApproach PDFDocument11 pagesAML CFT Guidelines RiskBasedApproach PDFAijaz Ali MughalNo ratings yet

- New policy Amended CCM policy FinalDec-15_2023 1 1Document40 pagesNew policy Amended CCM policy FinalDec-15_2023 1 1selamNo ratings yet

- Is of The Finance Banking Sector From An Ethical PerspectiveDocument21 pagesIs of The Finance Banking Sector From An Ethical PerspectiveSuresh KodithuwakkuNo ratings yet

- Circular On (A) Benefit Illustration and (B) Other Market Conduct AspectsDocument23 pagesCircular On (A) Benefit Illustration and (B) Other Market Conduct AspectsRoshan PednekarNo ratings yet

- Faqs On Repayment Assistance 3.0: No. AnswerDocument4 pagesFaqs On Repayment Assistance 3.0: No. AnswerOmar MuhdNo ratings yet

- COMMENTARY - Stanford University PDFDocument2 pagesCOMMENTARY - Stanford University PDFa452102No ratings yet

- Grievance Redressal PolicyDocument12 pagesGrievance Redressal Policypriyanshusingh.inboxNo ratings yet

- Risk MGT - Third PPDocument55 pagesRisk MGT - Third PPmithilesh tabhaneNo ratings yet

- RBB-Preferred Relationship ManagerDocument3 pagesRBB-Preferred Relationship Managersunny.sunny0121No ratings yet

- Suggested Solutions Chapter 6, 7 and 8Document5 pagesSuggested Solutions Chapter 6, 7 and 8Loo Bee YeokNo ratings yet

- 2022 06 Reading Deck Customer Outcomes Based Approach Consumer Protection PDFDocument43 pages2022 06 Reading Deck Customer Outcomes Based Approach Consumer Protection PDFBereket GetachewNo ratings yet

- Grievance Redressal PolicyDocument11 pagesGrievance Redressal PolicyrechlootseriesNo ratings yet

- Operational Support Client Forum PDFDocument129 pagesOperational Support Client Forum PDFASDFGHTNo ratings yet

- Video Idea WorksheetDocument3 pagesVideo Idea WorksheetNeach GaoilNo ratings yet

- Customer Acceptance, Customer Care PolicyDocument7 pagesCustomer Acceptance, Customer Care PolicySiddhaa LNo ratings yet

- Product Disclosure RequirementsDocument10 pagesProduct Disclosure RequirementsSyed Abbas Haider ZaidiNo ratings yet

- Insurance Industry Trends Solutions EbookDocument12 pagesInsurance Industry Trends Solutions Ebookscientist xyzNo ratings yet

- Addendum To AePS Fraud Liability Guideline Feb 2022Document10 pagesAddendum To AePS Fraud Liability Guideline Feb 2022Abhishek MasterNo ratings yet

- GT Concise Banca Committee ReportDocument8 pagesGT Concise Banca Committee ReportgirishtiwaskarNo ratings yet

- Consumer AwarenessDocument5 pagesConsumer AwarenessMohit AlamNo ratings yet

- GD - Assignment 2 LatestDocument29 pagesGD - Assignment 2 LatestNurFazalina AkbarNo ratings yet

- Senrnal Prurptras: BanokoDocument12 pagesSenrnal Prurptras: BanokoAte MilesNo ratings yet

- DAO No. 02-08Document8 pagesDAO No. 02-08Boss NikNo ratings yet

- Audit-Report-Sena KaylanDocument50 pagesAudit-Report-Sena KaylanSohag AMLNo ratings yet

- Aowa Electronic Philippines Inc. v. DTI G.R. No. 189655 April 13 2011, Case DigestDocument5 pagesAowa Electronic Philippines Inc. v. DTI G.R. No. 189655 April 13 2011, Case DigestMak Francisco100% (2)

- Innoviti-Fullerton Case StudyDocument4 pagesInnoviti-Fullerton Case StudyraghavachantiNo ratings yet

- Rev1 19MIS0230 Dhinagar & TeamDocument7 pagesRev1 19MIS0230 Dhinagar & TeamSunil RaghuNo ratings yet

- Grievance_Redressal_PolicyDocument15 pagesGrievance_Redressal_Policydipeshjadhav2003No ratings yet

- Customer Compensation PolicyDocument15 pagesCustomer Compensation Policykokilavani5013No ratings yet

- Valoracion de ClientesDocument8 pagesValoracion de ClientesGabriela GonzálezNo ratings yet

- GD - Assignment 2Document24 pagesGD - Assignment 2NurFazalina AkbarNo ratings yet

- Business Banking Working Capital (RM-BBWC)Document3 pagesBusiness Banking Working Capital (RM-BBWC)anshita bangaNo ratings yet

- Policy For Protection of Interests of Policyholders New 2022Document12 pagesPolicy For Protection of Interests of Policyholders New 2022Neeraj ChauhannNo ratings yet

- MC 2022 25 CooperativesDocument79 pagesMC 2022 25 CooperativesRonnell Vic Cañeda YuNo ratings yet

- FNSFMB403 - Assessment 3Document9 pagesFNSFMB403 - Assessment 3husain081No ratings yet

- Standards of Lending Practice July 16Document12 pagesStandards of Lending Practice July 16nuwany2kNo ratings yet

- Customer Rights Policy For The Year 2020-2021: Strategic Planning & Development Wing Head Office, 112, JC Road, BengaluruDocument9 pagesCustomer Rights Policy For The Year 2020-2021: Strategic Planning & Development Wing Head Office, 112, JC Road, BengaluruAshmi JainNo ratings yet

- 4.2 - Needs and Expectation With Risk AnalysisDocument3 pages4.2 - Needs and Expectation With Risk AnalysisSafety Dept50% (2)

- NT Life FrameworkDocument15 pagesNT Life FrameworkSu Meo HuiNo ratings yet

- Embedded Finance Who Will Lead The Next Payments RevolutionDocument6 pagesEmbedded Finance Who Will Lead The Next Payments RevolutionSushma KazaNo ratings yet

- Consumer Behaviour Insurance SectorDocument25 pagesConsumer Behaviour Insurance SectorFaizan ShaikhNo ratings yet

- FNSFMB403 - Assessment 2 - PerformanceDocument3 pagesFNSFMB403 - Assessment 2 - Performancehusain081No ratings yet

- Customer Churn Case StudyDocument19 pagesCustomer Churn Case Studysantoshsadan100% (2)

- Concise Banca Committee ReportDocument8 pagesConcise Banca Committee ReportgirishtiwaskarNo ratings yet

- ITGS Paper 2 HLSL MarkschemeDocument15 pagesITGS Paper 2 HLSL MarkschemeDanielNo ratings yet

- Visa Brokerage StudyDocument10 pagesVisa Brokerage StudymichelleyeahhNo ratings yet

- Us Advisory Pushing The Boundaries of The Banking Regulatory Perimeter February 2023 PDFDocument26 pagesUs Advisory Pushing The Boundaries of The Banking Regulatory Perimeter February 2023 PDFikhan809No ratings yet

- Critical Financial Review: Understanding Corporate Financial InformationFrom EverandCritical Financial Review: Understanding Corporate Financial InformationNo ratings yet

- The Basel Ii "Use Test" - a Retail Credit Approach: Developing and Implementing Effective Retail Credit Risk Strategies Using Basel IiFrom EverandThe Basel Ii "Use Test" - a Retail Credit Approach: Developing and Implementing Effective Retail Credit Risk Strategies Using Basel IiNo ratings yet

- Klay - Eje JDDocument1 pageKlay - Eje JDhafizuddinrazaliNo ratings yet

- Public Islamic Asia Dividend Fund (Piadf)Document6 pagesPublic Islamic Asia Dividend Fund (Piadf)hafizuddinrazaliNo ratings yet

- EagleBurgmann - SPS Level Switch - ENDocument2 pagesEagleBurgmann - SPS Level Switch - ENhafizuddinrazaliNo ratings yet

- EagleBurgmann ZY Cyclone Separators enDocument6 pagesEagleBurgmann ZY Cyclone Separators enhafizuddinrazaliNo ratings yet

- FWD CI First EngBrochureDocument13 pagesFWD CI First EngBrochurehafizuddinrazaliNo ratings yet

- Esaimen Counselling ReflectionDocument4 pagesEsaimen Counselling ReflectionhafizuddinrazaliNo ratings yet

- D@A@U@L Zblc@Lcfru@L D@N@L K@N@ - Yo@ D@A@U@L Zblc@Lcfru@L D@N@L K@N@ - Yo@ Amq@Lc ZBQKMGML@L Nbybl Xmf@Yoml@N Amq@Lc ZBQKMGML@L Nbybl Xmf@Yoml@NDocument1 pageD@A@U@L Zblc@Lcfru@L D@N@L K@N@ - Yo@ D@A@U@L Zblc@Lcfru@L D@N@L K@N@ - Yo@ Amq@Lc ZBQKMGML@L Nbybl Xmf@Yoml@N Amq@Lc ZBQKMGML@L Nbybl Xmf@Yoml@NhafizuddinrazaliNo ratings yet

- Katalog Laminate Flooring PDFDocument28 pagesKatalog Laminate Flooring PDFhafizuddinrazaliNo ratings yet

- Azbil SDC25Document2 pagesAzbil SDC25hafizuddinrazaliNo ratings yet

- Stat 240120 174404Document103 pagesStat 240120 174404romeoahmed687No ratings yet

- BTMSB2104618 PT Wasco Enginnering (JGC)Document1 pageBTMSB2104618 PT Wasco Enginnering (JGC)Yoggi Gusfarianto100% (1)

- TPS14-007 Rev1.1 A8 Web-Admin Configuration Manual - FM 2.3.0.207Document91 pagesTPS14-007 Rev1.1 A8 Web-Admin Configuration Manual - FM 2.3.0.207adesedas2009No ratings yet

- 2.3. Affinity MappingDocument1 page2.3. Affinity MappingJansi FathimaNo ratings yet

- Group Term Insurance FormDocument1 pageGroup Term Insurance FormkumarNo ratings yet

- Work Enablers - Mobile Phone Policy - Reliance Retail: Details Job Grade Cost of Handset (RS)Document1 pageWork Enablers - Mobile Phone Policy - Reliance Retail: Details Job Grade Cost of Handset (RS)Manish SinghNo ratings yet

- Notification of The Bank of Thailand No. Sornorsor. 95/2551 Re: Regulation On Minimum Capital Requirement For Operational RiskDocument24 pagesNotification of The Bank of Thailand No. Sornorsor. 95/2551 Re: Regulation On Minimum Capital Requirement For Operational Riskmi nguyenNo ratings yet

- Ploughman AgroDocument2 pagesPloughman AgroSubin chhatriaNo ratings yet

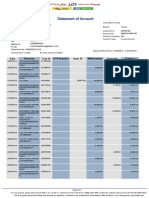

- Statement of Account: Date Tran Id Remarks UTR Number Instr. ID Withdrawals Deposits BalanceDocument8 pagesStatement of Account: Date Tran Id Remarks UTR Number Instr. ID Withdrawals Deposits Balancedinesh namdeoNo ratings yet

- BDO ATM-Debit-Card-FormDocument1 pageBDO ATM-Debit-Card-Formmunic14No ratings yet

- Annual Reports and Account Jan 2023Document260 pagesAnnual Reports and Account Jan 2023Bilal AhmedNo ratings yet

- Inmarsat ServiceDocument28 pagesInmarsat ServiceAntonis IsidorouNo ratings yet

- Medical Reimbursement Claim Form For Outdoor Treatment: Attach Prescription, Vouchers)Document2 pagesMedical Reimbursement Claim Form For Outdoor Treatment: Attach Prescription, Vouchers)balajiNo ratings yet

- HbbabrauditDocument278 pagesHbbabrauditpadmanabha14No ratings yet

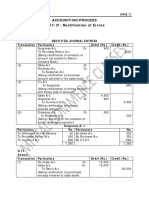

- CA Foundation Accounting SolutionsDocument117 pagesCA Foundation Accounting SolutionsAkash AjayNo ratings yet

- Hannah Cornman, BSDocument2 pagesHannah Cornman, BSapi-322065835No ratings yet

- Final Black BookDocument27 pagesFinal Black Bookruanonlineservices2023No ratings yet

- Hindustan Electronic Limited-Case StudyDocument27 pagesHindustan Electronic Limited-Case StudyMayank KothariNo ratings yet

- Prosanjit CVDocument2 pagesProsanjit CVMd. Nazmus SakibNo ratings yet

- Airbnb Travel Receipt, Confirmation Code HMAB5TZXYKDocument2 pagesAirbnb Travel Receipt, Confirmation Code HMAB5TZXYKAirbnb USNo ratings yet

- Branch srx300 GsDocument65 pagesBranch srx300 GsYoyow S. W.No ratings yet

- PDF DocumentDocument4 pagesPDF DocumentShubham SharmaNo ratings yet

- Information Security: Security Tools Presented By: Dr. F. N MusauDocument23 pagesInformation Security: Security Tools Presented By: Dr. F. N Musausteng5050No ratings yet

- Munhumutapa School of Commerce Name Student Number Course Title & Code Lecturer Task DateDocument5 pagesMunhumutapa School of Commerce Name Student Number Course Title & Code Lecturer Task DateNeoline Chipo DzirutsvaNo ratings yet

- Due Date Telephone Number Amount Payable: GstinDocument4 pagesDue Date Telephone Number Amount Payable: GstinivadjcourtNo ratings yet

- Comparison of Two BanksDocument49 pagesComparison of Two BanksAarti50% (2)

- DCN Manual 2019Document74 pagesDCN Manual 2019Suhani SrivastavaNo ratings yet

- F8 (AA) Kit - Que 81 Prancer ConstructionDocument2 pagesF8 (AA) Kit - Que 81 Prancer ConstructionChrisNo ratings yet