Download as xls, pdf, or txt

You might also like

- Fin 6060: Financial Decision MakingDocument9 pagesFin 6060: Financial Decision MakingDEE0% (1)

- Aniket Kulkarni Finance Black Book PDFDocument75 pagesAniket Kulkarni Finance Black Book PDFAniket KulkarniNo ratings yet

- Saaral Information DeckDocument23 pagesSaaral Information DeckVignesh KrishnamoorthyNo ratings yet

- Conventions Used in The Cost Benefit Analysis (CBA) ToolkitDocument4 pagesConventions Used in The Cost Benefit Analysis (CBA) ToolkitnarupatilNo ratings yet

- Common Batch Job FailuresDocument6 pagesCommon Batch Job FailuresSiji SurendranNo ratings yet

- Supply Chain Innovation ForumDocument25 pagesSupply Chain Innovation ForumNational Press Foundation100% (1)

- Ats Vendor Selection Matrix 1Document9 pagesAts Vendor Selection Matrix 1api-319631843No ratings yet

- Essay QuestionsDocument16 pagesEssay Questionssheldon100% (1)

- Appendix F: Accounting For PartnershipsDocument17 pagesAppendix F: Accounting For PartnershipsDerian Wijaya100% (1)

- TESCO Financial AnalysisDocument18 pagesTESCO Financial AnalysisFadekemi Fdk100% (1)

- Control: The Management Control Environment: Changes From The Eleventh EditionDocument22 pagesControl: The Management Control Environment: Changes From The Eleventh EditionRobin Shephard Hogue100% (1)

- Final Paper20 Revised Business ValuationDocument698 pagesFinal Paper20 Revised Business ValuationSukumar100% (5)

- Women Welfare Organisation Poonch (Wwop) Inhanceing Women Accesses To Justis Month Wise Detail of Approved BudgetDocument6 pagesWomen Welfare Organisation Poonch (Wwop) Inhanceing Women Accesses To Justis Month Wise Detail of Approved BudgetZohair AliNo ratings yet

- Attrition Analysis TemplateDocument11 pagesAttrition Analysis TemplateSatyen ChaturvediNo ratings yet

- Item Name Rate Detail Homepage MakeoverDocument3 pagesItem Name Rate Detail Homepage MakeoverkrishnanandvermaNo ratings yet

- Cloudforms Technical PresentationDocument86 pagesCloudforms Technical PresentationpintomaticNo ratings yet

- Business Intelligence Architect Developer Analyst in New York City Resume Ilin StarDocument3 pagesBusiness Intelligence Architect Developer Analyst in New York City Resume Ilin StarIlinStarNo ratings yet

- Revenue Forecast: Free Platform In-App $$ Paid PlatformDocument7 pagesRevenue Forecast: Free Platform In-App $$ Paid PlatformAmit SheoranNo ratings yet

- IP-guard Presentation SlidesDocument30 pagesIP-guard Presentation SlidesRendy AldoNo ratings yet

- MVA Implementing A Data Warehouse With SQL Jump Start Mod 1 FinalDocument37 pagesMVA Implementing A Data Warehouse With SQL Jump Start Mod 1 FinalKeerthan ManjunathNo ratings yet

- Excel Dashboard in MinutesDocument14 pagesExcel Dashboard in MinutesTawfiq4444No ratings yet

- Delivery Manager: The Main Responsibilities of The Post AreDocument4 pagesDelivery Manager: The Main Responsibilities of The Post AreSaravanan MuniandiNo ratings yet

- Eyerise Technologies Web Development Services Package HostingDocument36 pagesEyerise Technologies Web Development Services Package HostingMohsin KhanNo ratings yet

- 2014 Marketing Planning Tool ExampleDocument1 page2014 Marketing Planning Tool ExamplePedroNo ratings yet

- Business Analytics and Data Warehouse Evaluation - Information BuildersDocument10 pagesBusiness Analytics and Data Warehouse Evaluation - Information BuildersSeth FordNo ratings yet

- Client Continuance Evaluation ToolDocument3 pagesClient Continuance Evaluation ToolchenlyNo ratings yet

- Boutique Retail EyeConDocument33 pagesBoutique Retail EyeConHassan SiddiquiNo ratings yet

- Ecom CRM EvaluationDocument31 pagesEcom CRM EvaluationGurucharan K SNo ratings yet

- Proposal For Abhibus Clone Script DODDocument8 pagesProposal For Abhibus Clone Script DODEngida online travel CompanyNo ratings yet

- Consultancy Project DetailsDocument516 pagesConsultancy Project DetailsIlayaraja BoopathyNo ratings yet

- Data Labeling CompanyDocument11 pagesData Labeling CompanylearningspiralaiNo ratings yet

- AL Musbah Historical Data Analysis 20170519Document27 pagesAL Musbah Historical Data Analysis 20170519Ethan WilliamNo ratings yet

- Project Budget WBSDocument4 pagesProject Budget WBSRajcapeNo ratings yet

- Transformation Description Examples of When Transformation Would Be UsedDocument7 pagesTransformation Description Examples of When Transformation Would Be UsedSubrahmanyam SudiNo ratings yet

- Proposed Solutions: Peterson vs. Weber vs. Kelleher vs. AndersonDocument1 pageProposed Solutions: Peterson vs. Weber vs. Kelleher vs. AndersonNikhil JeswaniNo ratings yet

- Corporate CapabilitiesDocument31 pagesCorporate CapabilitieselyssaraeNo ratings yet

- Process Assessment Worksheet - PurchasingDocument1 pageProcess Assessment Worksheet - PurchasingDaniel BordenNo ratings yet

- PEF - Nick Sharma - IHS Markit - Panel 1Document13 pagesPEF - Nick Sharma - IHS Markit - Panel 1Nina KonitatNo ratings yet

- Flat - File.jewelry 2015 MPDocument5,104 pagesFlat - File.jewelry 2015 MPAurora Garcia Dela CruzNo ratings yet

- Voqeoit Technogies IntroductionDocument4 pagesVoqeoit Technogies Introductionmanjula puttaswamaiahNo ratings yet

- Digital MarketingDocument5 pagesDigital MarketingMRUNMAYI DESHPANDENo ratings yet

- Demand Estimation & P&LDocument2 pagesDemand Estimation & P&LAdnan MushtaqNo ratings yet

- Adwords Training ManualDocument73 pagesAdwords Training ManualKannan S100% (1)

- Solar Photovoltaic Design, Engineering & Budgeting Services: 1. Energy Generation SimulationDocument2 pagesSolar Photovoltaic Design, Engineering & Budgeting Services: 1. Energy Generation SimulationNirat PatelNo ratings yet

- Project Process FlowDocument42 pagesProject Process FlowMamtaNo ratings yet

- Manager Director Business Excellence in Philadelphia PA Resume Michael WeeksDocument3 pagesManager Director Business Excellence in Philadelphia PA Resume Michael WeeksMichaelWeeksNo ratings yet

- Accenture Mining Brochure PDFDocument12 pagesAccenture Mining Brochure PDFAdan Ceballos MiovichNo ratings yet

- Pyramid Big Data TestingDocument3 pagesPyramid Big Data Testingutagore58100% (1)

- WBS TEMPLATE - Parry SugarsDocument20 pagesWBS TEMPLATE - Parry SugarsPranaya ReddyNo ratings yet

- Odisha State Urban Water Supply Policy-2013Document11 pagesOdisha State Urban Water Supply Policy-2013Janaki MohapatraNo ratings yet

- Sales PlanDocument26 pagesSales Plansaurabh323612No ratings yet

- You Exec - Pricing Strategies Part 2 FreeDocument8 pagesYou Exec - Pricing Strategies Part 2 FreeAta JaafatNo ratings yet

- A Cloud For Doing GoodDocument118 pagesA Cloud For Doing GoodBela VillamilNo ratings yet

- BrochureDocument4 pagesBrochureI J'sNo ratings yet

- Using Analytics To Enhance A Food Retailer's Shelf-SpaceDocument22 pagesUsing Analytics To Enhance A Food Retailer's Shelf-SpaceJanaNo ratings yet

- What Is I-O?: Consultant: Leadership Development and Assessment About The OrganizationDocument3 pagesWhat Is I-O?: Consultant: Leadership Development and Assessment About The OrganizationklatifdgNo ratings yet

- Azure Solution ArchitectDocument2 pagesAzure Solution ArchitectAnil ReddyNo ratings yet

- Excel FormulasDocument206 pagesExcel FormulasEricka GeliNo ratings yet

- Implementing The Account and Financial Dimensions Framework AX2012Document43 pagesImplementing The Account and Financial Dimensions Framework AX2012Sky Boon Kok LeongNo ratings yet

- Digital DiaryDocument369 pagesDigital DiaryPartho BoraNo ratings yet

- Data MiningDocument22 pagesData MiningTanmay DeyNo ratings yet

- I Will Do 5 Hours Perfect Web Research and Data Entry WorkDocument4 pagesI Will Do 5 Hours Perfect Web Research and Data Entry WorkSamreen AwanNo ratings yet

- The Evolution of Strategy Analysis at P&GDocument22 pagesThe Evolution of Strategy Analysis at P>auhid Rahman JuboNo ratings yet

- MIS Case Study - Digitalization at SiemensDocument6 pagesMIS Case Study - Digitalization at SiemensRumani ChakrabortyNo ratings yet

- Linear Programming On Excel: Problems and SolutionsDocument5 pagesLinear Programming On Excel: Problems and Solutionsacetinkaya92No ratings yet

- Hands-On Lab: Introduction To SQL Azure For Visual Studio 2010 DevelopersDocument58 pagesHands-On Lab: Introduction To SQL Azure For Visual Studio 2010 DevelopersJunXian KeNo ratings yet

- Cba ExampleDocument4 pagesCba Examplelaxave8817No ratings yet

- Investment DecisionsDocument11 pagesInvestment DecisionsNJUGUNA IANNo ratings yet

- 01 Konsep Dasar Manajemen KeuanganDocument35 pages01 Konsep Dasar Manajemen Keuangandulli fitriantoNo ratings yet

- Relevance:: ExampleDocument4 pagesRelevance:: ExampleNicoleMendozaNo ratings yet

- BE1Document4 pagesBE1egaNo ratings yet

- IN Financial Management 1: Leyte CollegesDocument20 pagesIN Financial Management 1: Leyte CollegesJeric LepasanaNo ratings yet

- RFM Corp Annual ReportDocument169 pagesRFM Corp Annual ReportGab RielNo ratings yet

- Corporate FinanceDocument418 pagesCorporate FinanceLusayo Mhango100% (2)

- CHEMALITEDocument1 pageCHEMALITEPurva TamhankarNo ratings yet

- Topic Selection: by Tek Bahadur MadaiDocument24 pagesTopic Selection: by Tek Bahadur Madairesh dhamiNo ratings yet

- ACY4008 - Topic 2 - Financial Reporting and AnalysisDocument42 pagesACY4008 - Topic 2 - Financial Reporting and Analysisjason leeNo ratings yet

- Cambridge O Level: Accounting 7707/22 May/June 2022Document16 pagesCambridge O Level: Accounting 7707/22 May/June 2022Kutwaroo GayetreeNo ratings yet

- FINANCIAL ACCOUNTING AND ANALYSIS AssignmentDocument5 pagesFINANCIAL ACCOUNTING AND ANALYSIS AssignmentnikitaNo ratings yet

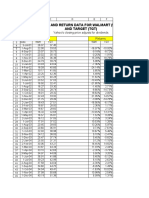

- Price and Return Data For Walmart (WMT) and Target (TGT) : Prices Returns Yahoo's Closing Price Adjusts For DividendsDocument19 pagesPrice and Return Data For Walmart (WMT) and Target (TGT) : Prices Returns Yahoo's Closing Price Adjusts For DividendsSyed Ameer Ali ShahNo ratings yet

- Hostile & Defensive Takeover StrategiesDocument26 pagesHostile & Defensive Takeover StrategiesShobhit Bhatnagar100% (2)

- Financial Statement FY2017 PDFDocument227 pagesFinancial Statement FY2017 PDFNena AnnisyaNo ratings yet

- Reflection#4 - Asset ManagementDocument2 pagesReflection#4 - Asset ManagementnerieroseNo ratings yet

- Financial Statement Analysis of DellDocument14 pagesFinancial Statement Analysis of Dellfizza amjadNo ratings yet

- UBI230110110 Industry CompetitorAnalysis 20180314222113Document8 pagesUBI230110110 Industry CompetitorAnalysis 20180314222113DamTokyoNo ratings yet

- © The Institute of Chartered Accountants of IndiaDocument40 pages© The Institute of Chartered Accountants of Indiaकनक नामदेवNo ratings yet

- Financial Statement and The Reporting Entity.Document8 pagesFinancial Statement and The Reporting Entity.Mikki Miks AkbarNo ratings yet

- Case Study - Sony Vs GoogleDocument3 pagesCase Study - Sony Vs GoogleMariaAngelicaMargenApeNo ratings yet

- How To Trade Like Hedge FundsDocument26 pagesHow To Trade Like Hedge FundsjoshuaofferNo ratings yet

- CorelDRAW Graphics Suite X7Document5 pagesCorelDRAW Graphics Suite X7niker justiniano infantesNo ratings yet