Download as pdf or txt

You might also like

- Review PetitionDocument19 pagesReview PetitionshwetaNo ratings yet

- 1984 SCC Online Kar 369: (1985) 2 SLR 273 Karnataka High CourtDocument5 pages1984 SCC Online Kar 369: (1985) 2 SLR 273 Karnataka High Courtvijaykumar devanahally srinivasmurthyNo ratings yet

- WA6586-12-28-02-2014 Balanoor TeaDocument68 pagesWA6586-12-28-02-2014 Balanoor Tearajashekhar asNo ratings yet

- Kerala High Court Judgement On Islamic BankingDocument33 pagesKerala High Court Judgement On Islamic BankingSulekha BhattacherjeeNo ratings yet

- SC JudgementDocument23 pagesSC JudgementsreeramaNo ratings yet

- Appsc BacklogDocument53 pagesAppsc BacklogSakroth BanothNo ratings yet

- WP15872 19 08 07 2019Document30 pagesWP15872 19 08 07 2019Varun KannanNo ratings yet

- WWW - Livelaw.In: in The Supreme Court of India Civil Appellate JurisdictionDocument23 pagesWWW - Livelaw.In: in The Supreme Court of India Civil Appellate JurisdictionANUPAM SHIVAMNo ratings yet

- PDF Upload-135749 PDFDocument27 pagesPDF Upload-135749 PDFdrchillpillNo ratings yet

- 147Document22 pages147Alahari Sunil NaiduNo ratings yet

- Moot Court Petitioner FinalDocument24 pagesMoot Court Petitioner FinalIndhuja100% (1)

- Govind Kumar Srivastava v. UOI Annexure P7Document4 pagesGovind Kumar Srivastava v. UOI Annexure P7sidhinathsengarNo ratings yet

- CAT Chandigarh Verdict For Reservation in Promotion PDFDocument9 pagesCAT Chandigarh Verdict For Reservation in Promotion PDFman_i_acNo ratings yet

- Gazettes 1690984228162Document32 pagesGazettes 1690984228162Director APNo ratings yet

- Various Cases Relating To Age Relaxation ConcessionDocument48 pagesVarious Cases Relating To Age Relaxation ConcessionapaarmathurNo ratings yet

- Various Cases Relating To Age Relaxation/ Concession: Back To Index PageDocument48 pagesVarious Cases Relating To Age Relaxation/ Concession: Back To Index PageNasir AhmadNo ratings yet

- B'emmanuel Cashew Industries Vs Chi Commodities Handlers Inc On 29 April, 2011'Document11 pagesB'emmanuel Cashew Industries Vs Chi Commodities Handlers Inc On 29 April, 2011'AKHIL H KRISHNANNo ratings yet

- Display PDFDocument10 pagesDisplay PDFLatest Laws TeamNo ratings yet

- WP204935 18 11 08 2023Document10 pagesWP204935 18 11 08 2023Abhinandan S MNo ratings yet

- Sabc Heads of Argument - 30 May 2016Document31 pagesSabc Heads of Argument - 30 May 2016CityPressNo ratings yet

- CLAT PetitionDocument56 pagesCLAT PetitionlegallyindiaNo ratings yet

- Indian Law Report - Allahabad Series - Dec2009Document100 pagesIndian Law Report - Allahabad Series - Dec2009PrasadNo ratings yet

- Reportable: Signature Not VerifiedDocument35 pagesReportable: Signature Not VerifiedpsrpsrNo ratings yet

- Rajasthan Rajya Vidyut Prasaran Nigam Limited: A State Government UndertakingDocument12 pagesRajasthan Rajya Vidyut Prasaran Nigam Limited: A State Government UndertakingVikas JainNo ratings yet

- Madras High Court WP 25124 of 2005Document6 pagesMadras High Court WP 25124 of 2005Disability Rights AllianceNo ratings yet

- Labour Law Memo FinalDocument15 pagesLabour Law Memo FinalAmitKumarNo ratings yet

- Aftab Adil Versus State of JaharkhandDocument3 pagesAftab Adil Versus State of JaharkhandwarpedzoozooNo ratings yet

- Sarla Verma V Uoi SummaryDocument6 pagesSarla Verma V Uoi SummarysankhlabharatNo ratings yet

- Final Orders222012Document13 pagesFinal Orders222012praveenNo ratings yet

- J 2018 SCC OnLine Bom 12441 Nanbanamo Gmailcom 20230428 165159 1 2Document2 pagesJ 2018 SCC OnLine Bom 12441 Nanbanamo Gmailcom 20230428 165159 1 2Balaji KannanNo ratings yet

- Bajrang Lal Sharma SCCDocument15 pagesBajrang Lal Sharma SCCdevanshi jainNo ratings yet

- Kar HC TP SoftbrandsDocument80 pagesKar HC TP SoftbrandsGVKNo ratings yet

- 8th Semester SyllabusDocument22 pages8th Semester SyllabusrohelarupaliNo ratings yet

- Constitutional Law II.Document3 pagesConstitutional Law II.Chenna ReddyNo ratings yet

- APPSC JUNIOR ACCOUNTANTS CATEGORY IV RECRUITMENT Notification 22092012Document17 pagesAPPSC JUNIOR ACCOUNTANTS CATEGORY IV RECRUITMENT Notification 22092012SAN1258No ratings yet

- Case 01karnataka State Medical V Astra Zeneca PharmaDocument36 pagesCase 01karnataka State Medical V Astra Zeneca PharmaBrahm KumarNo ratings yet

- WP 28278 2019 FinalOrder 24-Jan-2020 PDFDocument8 pagesWP 28278 2019 FinalOrder 24-Jan-2020 PDFSahil DhamijaNo ratings yet

- Ajay Hasia and Ors Vs Khalid Mujib Sehravardi and s800498COM634569Document18 pagesAjay Hasia and Ors Vs Khalid Mujib Sehravardi and s800498COM634569Bhumika GuptaNo ratings yet

- Supreme Court of India: Examination ItDocument10 pagesSupreme Court of India: Examination ItAtul krishnaNo ratings yet

- Vishal N Kalsaria Vs Bank of India and OrsDocument20 pagesVishal N Kalsaria Vs Bank of India and OrsSaumya badigineniNo ratings yet

- WP44850 17 15 12 2020Document24 pagesWP44850 17 15 12 2020Ravi Prakash MNo ratings yet

- Senior Lecturer Eee in Govt PolytechnicsDocument7 pagesSenior Lecturer Eee in Govt PolytechnicsNarasimha SastryNo ratings yet

- J 2019 SCC OnLine Mad 31016 2019 78 PTC 274 Sakshamanand Nusrlranchiacin 20240530 015418 1 4Document4 pagesJ 2019 SCC OnLine Mad 31016 2019 78 PTC 274 Sakshamanand Nusrlranchiacin 20240530 015418 1 4Anand SakshamNo ratings yet

- WWW Apspsc Gov inDocument20 pagesWWW Apspsc Gov indeva_g123No ratings yet

- Moot JH Pet Team - ODocument16 pagesMoot JH Pet Team - OMohammed ShahnawazNo ratings yet

- Final Memo of Civil CaseDocument17 pagesFinal Memo of Civil CaseYuvraj NangiaNo ratings yet

- Adjudication Order in Respect of Waverley Investments Ltd.Document8 pagesAdjudication Order in Respect of Waverley Investments Ltd.Shyam SunderNo ratings yet

- WP 30 of 2019 Silajit JudgmentDocument17 pagesWP 30 of 2019 Silajit Judgmentthemis sikkimNo ratings yet

- Reserve Bank of India Bombay Vs CT Dighe and Ors 2s810329COM886675Document9 pagesReserve Bank of India Bombay Vs CT Dighe and Ors 2s810329COM886675hariom bajpaiNo ratings yet

- 1 MergedDocument67 pages1 MergedShivam MishraNo ratings yet

- 1 MergedDocument122 pages1 MergedShivam MishraNo ratings yet

- Ritu Raag Kaur v. Union of India, 2015 SCC OnLine P&H 15782Document2 pagesRitu Raag Kaur v. Union of India, 2015 SCC OnLine P&H 15782utsavsinghofficeNo ratings yet

- Respondents/Respondents 1 To 3/3Rd 5Th & 6Th PetitionersDocument42 pagesRespondents/Respondents 1 To 3/3Rd 5Th & 6Th PetitionersSheethal KakkattilNo ratings yet

- Recruitment Drive To The Post of Junior Assistant (Fire Services)Document4 pagesRecruitment Drive To The Post of Junior Assistant (Fire Services)Aien AmerNo ratings yet

- Punjab IGP Removal Writ - FINAL DRAFTDocument31 pagesPunjab IGP Removal Writ - FINAL DRAFTUsama KhawarNo ratings yet

- In The Income Tax Appellate Tribunal "B" Bench, Ahmedabad Before Shri Pradip Kumar Kedia, Accountant Member & Shri Mahavir Prasad, Judicial MemebrDocument47 pagesIn The Income Tax Appellate Tribunal "B" Bench, Ahmedabad Before Shri Pradip Kumar Kedia, Accountant Member & Shri Mahavir Prasad, Judicial MemebrshantXNo ratings yet

- In The High Court of Delhi at New DelhiDocument10 pagesIn The High Court of Delhi at New DelhiSudhir KumarNo ratings yet

- Avoiding Workplace Discrimination: A Guide for Employers and EmployeesFrom EverandAvoiding Workplace Discrimination: A Guide for Employers and EmployeesNo ratings yet

- Bombay High Court Judgement Dated 11062012Document30 pagesBombay High Court Judgement Dated 11062012Manish MishraNo ratings yet

- New Gorakhpur Final - 1-Layout1Document1 pageNew Gorakhpur Final - 1-Layout1Manish MishraNo ratings yet

- Orissa High Court Judgement Dated 31012012Document10 pagesOrissa High Court Judgement Dated 31012012Manish MishraNo ratings yet

- Confirming Landuse ChartDocument8 pagesConfirming Landuse ChartManish MishraNo ratings yet

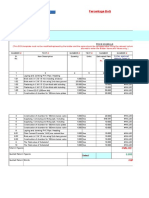

- V3 BOQ Percentage Template 4decimalDocument6 pagesV3 BOQ Percentage Template 4decimalManish MishraNo ratings yet

- Modenity TraditionDocument33 pagesModenity TraditionDrAman GurnayNo ratings yet

- Linguistic Code of NationDocument1 pageLinguistic Code of NationManish MishraNo ratings yet

- CivilDAR 2019 Vol 1Document2 pagesCivilDAR 2019 Vol 1Manish MishraNo ratings yet

- DWG SectionDocument1 pageDWG SectionManish MishraNo ratings yet

- Note: - (I) Attempt All Questions. (Ii) Each Question Carries Equal Marks. Note: - (I) Attempt All Questions. (Ii) Each Question Carries Equal MarksDocument1 pageNote: - (I) Attempt All Questions. (Ii) Each Question Carries Equal Marks. Note: - (I) Attempt All Questions. (Ii) Each Question Carries Equal MarksManish MishraNo ratings yet

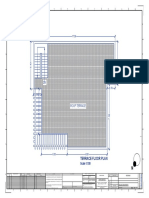

- Terrace Floor Plan: Scale 1:100Document1 pageTerrace Floor Plan: Scale 1:100Manish MishraNo ratings yet

- Building Economics Complete NotesDocument20 pagesBuilding Economics Complete NotesManish MishraNo ratings yet

- Drinking Water Drinking WaterDocument1 pageDrinking Water Drinking WaterManish MishraNo ratings yet

- CPWD Handbook Office BuildingDocument91 pagesCPWD Handbook Office Buildingexecutive engineer1No ratings yet

- ARB Student HandbookDocument35 pagesARB Student HandbookManish MishraNo ratings yet

- AREA APRX. 3000 M : SITE LAYOUT PLAN (Not To Scale)Document1 pageAREA APRX. 3000 M : SITE LAYOUT PLAN (Not To Scale)Manish MishraNo ratings yet

- Transforming Contemporary Architecture Education in India With Ancient Indian Learning System of GurukulDocument7 pagesTransforming Contemporary Architecture Education in India With Ancient Indian Learning System of GurukulManish Mishra0% (1)

- Prospectus 2013Document30 pagesProspectus 2013Manish MishraNo ratings yet

- Housing BriefDocument6 pagesHousing BriefManish MishraNo ratings yet

- L. ASIAN TERMINALS, INC. (ATI) v. PADOSON STAINLESS STEEL CORPDocument21 pagesL. ASIAN TERMINALS, INC. (ATI) v. PADOSON STAINLESS STEEL CORPKaloi GarciaNo ratings yet

- Reas Bank Study Notes 22 01 19 EnglishDocument11 pagesReas Bank Study Notes 22 01 19 EnglishVivek Earnest nathNo ratings yet

- Rodillas Vs SandiganbayanDocument4 pagesRodillas Vs SandiganbayanJasielle Leigh UlangkayaNo ratings yet

- Good Behavior and The Murderous MayorDocument40 pagesGood Behavior and The Murderous MayorJohn Bailor FajardoNo ratings yet

- Assessment Process and Reglementary PeriodDocument52 pagesAssessment Process and Reglementary PeriodClint Lou Matthew EstapiaNo ratings yet

- Ewton S AWS OF Otion: The Fundamental Laws of Newtonian DynamicsDocument74 pagesEwton S AWS OF Otion: The Fundamental Laws of Newtonian Dynamicsapi-37284110% (1)

- Undang-Undang Jenayah Ii LIA2007 SESI 2018/2019: Nama: Mohd Nazlee Bin ZubairDocument12 pagesUndang-Undang Jenayah Ii LIA2007 SESI 2018/2019: Nama: Mohd Nazlee Bin ZubairCijet ZubairNo ratings yet

- Paat V CA Case DigestDocument2 pagesPaat V CA Case DigestRoldan GanadosNo ratings yet

- Macasiray V PeopleDocument2 pagesMacasiray V PeopleiptrinidadNo ratings yet

- SOLAS Chapter V - Regulation 33Document2 pagesSOLAS Chapter V - Regulation 33Wunna Tint WayNo ratings yet

- PAO Objectives and ThrustsDocument2 pagesPAO Objectives and ThrustsPhoebe BuffayNo ratings yet

- Marine Surveyors Manual Part 2Document66 pagesMarine Surveyors Manual Part 2Javier Garcia Marquez100% (1)

- Topic Iv - Local Taxation and Fiscal MattersDocument48 pagesTopic Iv - Local Taxation and Fiscal MattersJean Ashley Napoles AbarcaNo ratings yet

- Thermal Terms & Conditions of SaleDocument1 pageThermal Terms & Conditions of SalethermaltechnologiesNo ratings yet

- Eastwest Credit Card Application Form: X X X X X XDocument1 pageEastwest Credit Card Application Form: X X X X X XLuigi NavalNo ratings yet

- Electric Forces and Electric Fields: Chapter 18Document57 pagesElectric Forces and Electric Fields: Chapter 18mama helmiNo ratings yet

- Atencio LawsuitDocument20 pagesAtencio LawsuitFusionNewsNo ratings yet

- National Security ProjectDocument10 pagesNational Security ProjectmehulaforeverNo ratings yet

- Fire Accident in RMG Industry in BangladeshDocument14 pagesFire Accident in RMG Industry in BangladeshdevilbondhonNo ratings yet

- United States Court of Appeals, Second Circuit.: No. 527, Docket 84-7698Document10 pagesUnited States Court of Appeals, Second Circuit.: No. 527, Docket 84-7698Scribd Government DocsNo ratings yet

- And Immigration Services Act (Saskatchewan) and The Immigrant and Refugee Protection Act (Canada)Document4 pagesAnd Immigration Services Act (Saskatchewan) and The Immigrant and Refugee Protection Act (Canada)atrinandanNo ratings yet

- Political Parties ReviewerDocument13 pagesPolitical Parties ReviewerMawon Lin TigasNo ratings yet

- BP 220 Economic and Socialized Housing Revised Irr 2008Document76 pagesBP 220 Economic and Socialized Housing Revised Irr 2008jncbrazilNo ratings yet

- Profile Form - Athlete: Pencak Silat Alexius Martin Q. Patano AthleteDocument5 pagesProfile Form - Athlete: Pencak Silat Alexius Martin Q. Patano AthleteReyn UlidanNo ratings yet

- FEMA CAMP LOCATIONS - Via - GPS COORDINATES PDFDocument19 pagesFEMA CAMP LOCATIONS - Via - GPS COORDINATES PDFal mooreNo ratings yet

- Bolastig v. Sandiganbayan, 235 SCRA 103Document5 pagesBolastig v. Sandiganbayan, 235 SCRA 103Karen Patricio LusticaNo ratings yet

- Cabinet Secretaries of Aquino IIIDocument37 pagesCabinet Secretaries of Aquino IIIResshille Ann T. SalleyNo ratings yet

- Unified Application of Building PermitDocument2 pagesUnified Application of Building PermitMark Ian InesNo ratings yet

- Kenya Legal Framework AnalysisDocument19 pagesKenya Legal Framework AnalysisBenedict AnicetNo ratings yet

- SUCCESSION Reserva Troncal DigestsDocument7 pagesSUCCESSION Reserva Troncal DigestsMartin AlfonsoNo ratings yet