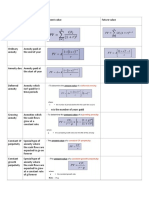

55 Comparison of Accounting Assumptions

55 Comparison of Accounting Assumptions

You might also like

- Gallagher & Mohan - DCF - Modeling - Example - DealDocument12 pagesGallagher & Mohan - DCF - Modeling - Example - Dealbrin dizelleNo ratings yet

- CPA Review Notes 2019 - FAR (Financial Accounting and Reporting)From EverandCPA Review Notes 2019 - FAR (Financial Accounting and Reporting)Rating: 3.5 out of 5 stars3.5/5 (17)

- LIIIDocument6 pagesLIIIcpiercecfaNo ratings yet

- Traditional Method of Investment Valuation For BeginnersDocument6 pagesTraditional Method of Investment Valuation For BeginnersSithick Mohamed100% (2)

- Capitalization: Capital Vs Operating LeaseDocument2 pagesCapitalization: Capital Vs Operating Leasejohnsmith12312312312No ratings yet

- Financial Accounting Ratio Anaylsis FormulasDocument2 pagesFinancial Accounting Ratio Anaylsis Formulasbasit111100% (1)

- Finance PDFDocument136 pagesFinance PDFjariyarasheedNo ratings yet

- Leasing: An OverviewDocument18 pagesLeasing: An OverviewNeha GoyalNo ratings yet

- Ca Final SFM Capital Budgeting Summary (Old Course)Document21 pagesCa Final SFM Capital Budgeting Summary (Old Course)swati mishraNo ratings yet

- ACCA FR Concept CapsuleDocument8 pagesACCA FR Concept CapsulehasharawanNo ratings yet

- Key Soal Chp. 2Document8 pagesKey Soal Chp. 2Yousania SimbiakNo ratings yet

- Fam - 1Document20 pagesFam - 1shahidNo ratings yet

- CORP Finance II Exam NotesDocument12 pagesCORP Finance II Exam NotesTeddie MowerNo ratings yet

- Notes For L4Document11 pagesNotes For L4yuyin.gohyyNo ratings yet

- Chapter 5 - Asset Investment Decisions and Capital RationingDocument31 pagesChapter 5 - Asset Investment Decisions and Capital RationingInga ȚîgaiNo ratings yet

- MF 3 Cost of CapitalDocument48 pagesMF 3 Cost of CapitalKashika BansalNo ratings yet

- AFAR - QuickyDocument27 pagesAFAR - QuickywktxlsrkfNo ratings yet

- Asset Investment Decisions and Capital Rationing: Margarita KouloumbriDocument31 pagesAsset Investment Decisions and Capital Rationing: Margarita KouloumbriInga ȚîgaiNo ratings yet

- Kasus PPAK 1 (Kel 1) Jawaban AgusDocument6 pagesKasus PPAK 1 (Kel 1) Jawaban AgusagusriantoNo ratings yet

- Bholu Baba Jamshedpur If Any Query Mail To (91) 9431757848 Why Fear When I Am Here.......Document9 pagesBholu Baba Jamshedpur If Any Query Mail To (91) 9431757848 Why Fear When I Am Here.......Chirag MalhotraNo ratings yet

- Introduction To Financial Reporting: Assets Liabilities + Owner's EquityDocument7 pagesIntroduction To Financial Reporting: Assets Liabilities + Owner's EquityKothari InvestmentsNo ratings yet

- 4222 CH 20 Slides From PDFDocument17 pages4222 CH 20 Slides From PDFAn NaNo ratings yet

- Afar Notes by DR Ferrer Summary Bs AccountancyDocument22 pagesAfar Notes by DR Ferrer Summary Bs AccountancyAnne Echavez Pasco100% (2)

- Management - 5Document10 pagesManagement - 5mohini.hr07No ratings yet

- Quantitative MethodsDocument35 pagesQuantitative Methodsphindocha30No ratings yet

- My SBR NOTEDocument21 pagesMy SBR NOTEMD.RIDWANUR RAHMANNo ratings yet

- 4.3 Bond InvestmentsDocument18 pages4.3 Bond Investmentsakshaygangarde143No ratings yet

- Cost of CapitalDocument75 pagesCost of CapitalManisha SanghviNo ratings yet

- Quiz Preparation Notes JTDocument2 pagesQuiz Preparation Notes JTxhayyyzNo ratings yet

- Fundamentals of Corporate Finance Canadian 2Nd Edition Berk Solutions Manual Full Chapter PDFDocument41 pagesFundamentals of Corporate Finance Canadian 2Nd Edition Berk Solutions Manual Full Chapter PDFRussellFischerqxcj100% (12)

- Rev151 - Topic 3-Investment MethodDocument24 pagesRev151 - Topic 3-Investment Methodkhaihafiz14No ratings yet

- Cost of CapitalDocument13 pagesCost of Capitalஇலக்கியச்செல்வி உமாபதிNo ratings yet

- 2.2. Ind AS 7Document25 pages2.2. Ind AS 7Ajay JangirNo ratings yet

- Session 6 - Depreciation - HandoutDocument33 pagesSession 6 - Depreciation - HandoutJohn DoeNo ratings yet

- Module2 EconDocument45 pagesModule2 EconandreslloydralfNo ratings yet

- Topic 2. Discounting: Future ValueDocument13 pagesTopic 2. Discounting: Future ValueАндрей ДымовNo ratings yet

- Finance Reviewer: Time-Value of MoneyDocument1 pageFinance Reviewer: Time-Value of MoneyAngela ChuaNo ratings yet

- Sale and Leaseback: The Benefits of SLB Transactions Are As FollowsDocument6 pagesSale and Leaseback: The Benefits of SLB Transactions Are As FollowsJoan BartolomeNo ratings yet

- CHAPTER 7 Bonds and Their ValuationDocument43 pagesCHAPTER 7 Bonds and Their ValuationAhsan100% (2)

- Expressed As A Percentage of The Value of Revenue or Sales.: Balance Sheet: Reports What The Organization Owns and OwesDocument3 pagesExpressed As A Percentage of The Value of Revenue or Sales.: Balance Sheet: Reports What The Organization Owns and OwesDGNo ratings yet

- Chapter 7 Cashflow ApproachDocument21 pagesChapter 7 Cashflow ApproachINTAN NURLIANA ISMAILNo ratings yet

- Solution Manual For Financial Accounting Libby Libby Short 8th EditionDocument41 pagesSolution Manual For Financial Accounting Libby Libby Short 8th EditionKennethOrrmsqi100% (47)

- Ch#4 Accounting For Non Current AssetsDocument7 pagesCh#4 Accounting For Non Current Assetseaglerealestate31No ratings yet

- Revision MidtermDocument12 pagesRevision MidtermKim NgânNo ratings yet

- Management of Working CapitalDocument12 pagesManagement of Working CapitalViraj DhamdhereNo ratings yet

- Economics Simple InterestDocument8 pagesEconomics Simple InterestbabadapbadapNo ratings yet

- MFD Summary 2Document26 pagesMFD Summary 2h9rkbdhx57No ratings yet

- Discount RateDocument9 pagesDiscount RateNguyễn PhúcNo ratings yet

- ch09 Cost of CapitalDocument46 pagesch09 Cost of Capital蘇則翰No ratings yet

- BEC CPA Formulas November 2015 Becker CPA Review PDFDocument20 pagesBEC CPA Formulas November 2015 Becker CPA Review PDFsasyedaNo ratings yet

- Finance T3 2017 - w9Document45 pagesFinance T3 2017 - w9aabubNo ratings yet

- Unit 4Document22 pagesUnit 4SAI GANESH M S 2127321No ratings yet

- Fnce 100 Final Cheat SheetDocument3 pagesFnce 100 Final Cheat Sheethung TranNo ratings yet

- 12+Valuation+of+stock+and+bonds - โหมดความเข้ากันได้Document14 pages12+Valuation+of+stock+and+bonds - โหมดความเข้ากันได้NATCHA TANAPANJAPORNNo ratings yet

- Ch07 BondsDocument44 pagesCh07 BondsRaazia GulNo ratings yet

- Cost of CapitalDocument39 pagesCost of CapitalGeethika NayanaprabhaNo ratings yet

- Investment AppraisalDocument3 pagesInvestment AppraisalDawar Hussain (WT)No ratings yet

- Intro To Oil & Gas IssuesDocument16 pagesIntro To Oil & Gas Issuesjeff.oneal23No ratings yet

- Applied Corporate Finance. What is a Company worth?From EverandApplied Corporate Finance. What is a Company worth?Rating: 3 out of 5 stars3/5 (2)

- 1.1 4 - Discounting Risky Cash FlowsDocument40 pages1.1 4 - Discounting Risky Cash Flowsmanoranjan838241No ratings yet

- Cost Benefit AnalysisDocument1 pageCost Benefit Analysismanoranjan838241No ratings yet

- Basel Norms IIDocument3 pagesBasel Norms IImanoranjan838241No ratings yet

- Formation of CompaniesDocument7 pagesFormation of Companiesmanoranjan838241No ratings yet

- MemorandumDocument11 pagesMemorandummanoranjan838241No ratings yet

- Memorandum of Artcles For AGM To Be Held On 23rd Novemver 2005Document45 pagesMemorandum of Artcles For AGM To Be Held On 23rd Novemver 2005manoranjan838241No ratings yet

- 3 BepDocument1 page3 Bepmanoranjan838241No ratings yet

- Break Even AnalysisDocument12 pagesBreak Even Analysismanoranjan838241No ratings yet

- A Break Even Analysis Is A MethodDocument2 pagesA Break Even Analysis Is A Methodmanoranjan838241No ratings yet

- Indiancompaniesact 1956Document18 pagesIndiancompaniesact 1956manoranjan838241No ratings yet

- Article 202Document14 pagesArticle 202manoranjan838241No ratings yet

- v28n3 3Document6 pagesv28n3 3manoranjan838241No ratings yet

- Cost - Benefit Training Handouts 9-02Document8 pagesCost - Benefit Training Handouts 9-02manoranjan838241No ratings yet

- Feasibility AnalysisDocument4 pagesFeasibility Analysismanoranjan838241No ratings yet

- DP 200906Document18 pagesDP 200906manoranjan838241No ratings yet

- Cost and Benefit AnalysisDocument1 pageCost and Benefit Analysismanoranjan838241No ratings yet

- Bonds IIIDocument2 pagesBonds IIImanoranjan838241No ratings yet

- BackyardTrends CBAIRRDocument2 pagesBackyardTrends CBAIRRmanoranjan838241No ratings yet

- Beta N GrowthDocument18 pagesBeta N Growthmanoranjan838241No ratings yet

- Bond ValuationDocument4 pagesBond Valuationmanoranjan838241No ratings yet

- Calculation of Stock BetaDocument2 pagesCalculation of Stock Betamanoranjan838241No ratings yet

- Business Valuation ModelDocument1 pageBusiness Valuation Modelmanoranjan838241No ratings yet

- FJMOMI en Brochure 1Document32 pagesFJMOMI en Brochure 1manoranjan838241No ratings yet

- Accounting For Employee Stock Option Plans: After Studying This Chapter, You Will Be Able ToDocument41 pagesAccounting For Employee Stock Option Plans: After Studying This Chapter, You Will Be Able ToSandeep As SandeepNo ratings yet

- IASB Project ForSMEDocument27 pagesIASB Project ForSMEAlexandre ValcazaraNo ratings yet

- Hindustan Construction CompanyDocument18 pagesHindustan Construction CompanySudipta BoseNo ratings yet

- PT Indocement Tunggal Prakarsa Tbk. and SubsidiariesDocument64 pagesPT Indocement Tunggal Prakarsa Tbk. and SubsidiariesJonathan OngNo ratings yet

- Binder - BARC CD SA Bank Forecasting ValuationDocument184 pagesBinder - BARC CD SA Bank Forecasting ValuationMarcus HowardNo ratings yet

- 0.80 Points: AwardDocument21 pages0.80 Points: AwardhirevNo ratings yet

- Ey Transitioning To New Leasing Standard Ind As 116 PDFDocument44 pagesEy Transitioning To New Leasing Standard Ind As 116 PDFGere TassewNo ratings yet

- Theories (IIA and PPE)Document6 pagesTheories (IIA and PPE)LDB Ashley Jeremiah Magsino - ABMNo ratings yet

- Leather GoodsDocument27 pagesLeather GoodsThomas M100% (1)

- DAIBB Lending - 2 - 0Document8 pagesDAIBB Lending - 2 - 0ashraf294No ratings yet

- Annual Report PindoDeli 2010 PDFDocument157 pagesAnnual Report PindoDeli 2010 PDFImago graphix100% (1)

- Financial Statement Analysis of Vinamilk: Fabrikam ResidencesDocument21 pagesFinancial Statement Analysis of Vinamilk: Fabrikam ResidencesThanh TrầnNo ratings yet

- Acct1501 Tutorial Questions Solutions Week3Document3 pagesAcct1501 Tutorial Questions Solutions Week3chunkityik100% (1)

- Partnership Dissolution Lecture NotesDocument7 pagesPartnership Dissolution Lecture NotesGene Marie PotencianoNo ratings yet

- Audrina AP2 QT21.2Document32 pagesAudrina AP2 QT21.2nguyenphamnhungoc51No ratings yet

- S 5.8-5.13 Limited CompaniesDocument11 pagesS 5.8-5.13 Limited CompaniesIlovejjcNo ratings yet

- Ar 2010 PDFDocument234 pagesAr 2010 PDFLala RifaNo ratings yet

- Analysis of Asian Paints Financial StatementsDocument12 pagesAnalysis of Asian Paints Financial StatementsSahil SondhiNo ratings yet

- Rezultate Financiare AppleDocument3 pagesRezultate Financiare AppleClaudiuNo ratings yet

- Measuring and Managing Brand LoyaltyDocument19 pagesMeasuring and Managing Brand LoyaltyPratibha SinghNo ratings yet

- RWJ Chapter 3 Financial Statements Analysis and Financial ModelsDocument34 pagesRWJ Chapter 3 Financial Statements Analysis and Financial ModelsAshekin MahadiNo ratings yet

- ØHPK14/C 67/1/1: Series SET 1Document24 pagesØHPK14/C 67/1/1: Series SET 1Ethan GomesNo ratings yet

- Financial PlanDocument16 pagesFinancial PlanSenpai Kun0% (1)

- CB Annual Report 2012 FINALDocument76 pagesCB Annual Report 2012 FINALcrystalmckenzie941No ratings yet

- Kalpataru Power Transmission LimitedDocument8 pagesKalpataru Power Transmission LimitedjayNo ratings yet

- Financial InstrumentDocument79 pagesFinancial InstrumentÑïkêţ BäûðhåNo ratings yet

- GSPrime Finance IB Fund Accounting Important QuestionsDocument34 pagesGSPrime Finance IB Fund Accounting Important Questionsnaghulk1No ratings yet

- Waterfront Philippines, Inc - Sec Form 17-A - 30june2020Document233 pagesWaterfront Philippines, Inc - Sec Form 17-A - 30june2020backup cmbmpNo ratings yet

- Ch06 Proactive Approach To Detecting FraudDocument26 pagesCh06 Proactive Approach To Detecting Fraud230191No ratings yet

- MRT JAKARTA Annual Report 2013 PDFDocument100 pagesMRT JAKARTA Annual Report 2013 PDFDanu RangkutiNo ratings yet

Download as pdf or txt

You might also like

- Gallagher & Mohan - DCF - Modeling - Example - DealDocument12 pagesGallagher & Mohan - DCF - Modeling - Example - Dealbrin dizelleNo ratings yet

- CPA Review Notes 2019 - FAR (Financial Accounting and Reporting)From EverandCPA Review Notes 2019 - FAR (Financial Accounting and Reporting)Rating: 3.5 out of 5 stars3.5/5 (17)

- LIIIDocument6 pagesLIIIcpiercecfaNo ratings yet

- Traditional Method of Investment Valuation For BeginnersDocument6 pagesTraditional Method of Investment Valuation For BeginnersSithick Mohamed100% (2)

- Capitalization: Capital Vs Operating LeaseDocument2 pagesCapitalization: Capital Vs Operating Leasejohnsmith12312312312No ratings yet

- Financial Accounting Ratio Anaylsis FormulasDocument2 pagesFinancial Accounting Ratio Anaylsis Formulasbasit111100% (1)

- Finance PDFDocument136 pagesFinance PDFjariyarasheedNo ratings yet

- Leasing: An OverviewDocument18 pagesLeasing: An OverviewNeha GoyalNo ratings yet

- Ca Final SFM Capital Budgeting Summary (Old Course)Document21 pagesCa Final SFM Capital Budgeting Summary (Old Course)swati mishraNo ratings yet

- ACCA FR Concept CapsuleDocument8 pagesACCA FR Concept CapsulehasharawanNo ratings yet

- Key Soal Chp. 2Document8 pagesKey Soal Chp. 2Yousania SimbiakNo ratings yet

- Fam - 1Document20 pagesFam - 1shahidNo ratings yet

- CORP Finance II Exam NotesDocument12 pagesCORP Finance II Exam NotesTeddie MowerNo ratings yet

- Notes For L4Document11 pagesNotes For L4yuyin.gohyyNo ratings yet

- Chapter 5 - Asset Investment Decisions and Capital RationingDocument31 pagesChapter 5 - Asset Investment Decisions and Capital RationingInga ȚîgaiNo ratings yet

- MF 3 Cost of CapitalDocument48 pagesMF 3 Cost of CapitalKashika BansalNo ratings yet

- AFAR - QuickyDocument27 pagesAFAR - QuickywktxlsrkfNo ratings yet

- Asset Investment Decisions and Capital Rationing: Margarita KouloumbriDocument31 pagesAsset Investment Decisions and Capital Rationing: Margarita KouloumbriInga ȚîgaiNo ratings yet

- Kasus PPAK 1 (Kel 1) Jawaban AgusDocument6 pagesKasus PPAK 1 (Kel 1) Jawaban AgusagusriantoNo ratings yet

- Bholu Baba Jamshedpur If Any Query Mail To (91) 9431757848 Why Fear When I Am Here.......Document9 pagesBholu Baba Jamshedpur If Any Query Mail To (91) 9431757848 Why Fear When I Am Here.......Chirag MalhotraNo ratings yet

- Introduction To Financial Reporting: Assets Liabilities + Owner's EquityDocument7 pagesIntroduction To Financial Reporting: Assets Liabilities + Owner's EquityKothari InvestmentsNo ratings yet

- 4222 CH 20 Slides From PDFDocument17 pages4222 CH 20 Slides From PDFAn NaNo ratings yet

- Afar Notes by DR Ferrer Summary Bs AccountancyDocument22 pagesAfar Notes by DR Ferrer Summary Bs AccountancyAnne Echavez Pasco100% (2)

- Management - 5Document10 pagesManagement - 5mohini.hr07No ratings yet

- Quantitative MethodsDocument35 pagesQuantitative Methodsphindocha30No ratings yet

- My SBR NOTEDocument21 pagesMy SBR NOTEMD.RIDWANUR RAHMANNo ratings yet

- 4.3 Bond InvestmentsDocument18 pages4.3 Bond Investmentsakshaygangarde143No ratings yet

- Cost of CapitalDocument75 pagesCost of CapitalManisha SanghviNo ratings yet

- Quiz Preparation Notes JTDocument2 pagesQuiz Preparation Notes JTxhayyyzNo ratings yet

- Fundamentals of Corporate Finance Canadian 2Nd Edition Berk Solutions Manual Full Chapter PDFDocument41 pagesFundamentals of Corporate Finance Canadian 2Nd Edition Berk Solutions Manual Full Chapter PDFRussellFischerqxcj100% (12)

- Rev151 - Topic 3-Investment MethodDocument24 pagesRev151 - Topic 3-Investment Methodkhaihafiz14No ratings yet

- Cost of CapitalDocument13 pagesCost of Capitalஇலக்கியச்செல்வி உமாபதிNo ratings yet

- 2.2. Ind AS 7Document25 pages2.2. Ind AS 7Ajay JangirNo ratings yet

- Session 6 - Depreciation - HandoutDocument33 pagesSession 6 - Depreciation - HandoutJohn DoeNo ratings yet

- Module2 EconDocument45 pagesModule2 EconandreslloydralfNo ratings yet

- Topic 2. Discounting: Future ValueDocument13 pagesTopic 2. Discounting: Future ValueАндрей ДымовNo ratings yet

- Finance Reviewer: Time-Value of MoneyDocument1 pageFinance Reviewer: Time-Value of MoneyAngela ChuaNo ratings yet

- Sale and Leaseback: The Benefits of SLB Transactions Are As FollowsDocument6 pagesSale and Leaseback: The Benefits of SLB Transactions Are As FollowsJoan BartolomeNo ratings yet

- CHAPTER 7 Bonds and Their ValuationDocument43 pagesCHAPTER 7 Bonds and Their ValuationAhsan100% (2)

- Expressed As A Percentage of The Value of Revenue or Sales.: Balance Sheet: Reports What The Organization Owns and OwesDocument3 pagesExpressed As A Percentage of The Value of Revenue or Sales.: Balance Sheet: Reports What The Organization Owns and OwesDGNo ratings yet

- Chapter 7 Cashflow ApproachDocument21 pagesChapter 7 Cashflow ApproachINTAN NURLIANA ISMAILNo ratings yet

- Solution Manual For Financial Accounting Libby Libby Short 8th EditionDocument41 pagesSolution Manual For Financial Accounting Libby Libby Short 8th EditionKennethOrrmsqi100% (47)

- Ch#4 Accounting For Non Current AssetsDocument7 pagesCh#4 Accounting For Non Current Assetseaglerealestate31No ratings yet

- Revision MidtermDocument12 pagesRevision MidtermKim NgânNo ratings yet

- Management of Working CapitalDocument12 pagesManagement of Working CapitalViraj DhamdhereNo ratings yet

- Economics Simple InterestDocument8 pagesEconomics Simple InterestbabadapbadapNo ratings yet

- MFD Summary 2Document26 pagesMFD Summary 2h9rkbdhx57No ratings yet

- Discount RateDocument9 pagesDiscount RateNguyễn PhúcNo ratings yet

- ch09 Cost of CapitalDocument46 pagesch09 Cost of Capital蘇則翰No ratings yet

- BEC CPA Formulas November 2015 Becker CPA Review PDFDocument20 pagesBEC CPA Formulas November 2015 Becker CPA Review PDFsasyedaNo ratings yet

- Finance T3 2017 - w9Document45 pagesFinance T3 2017 - w9aabubNo ratings yet

- Unit 4Document22 pagesUnit 4SAI GANESH M S 2127321No ratings yet

- Fnce 100 Final Cheat SheetDocument3 pagesFnce 100 Final Cheat Sheethung TranNo ratings yet

- 12+Valuation+of+stock+and+bonds - โหมดความเข้ากันได้Document14 pages12+Valuation+of+stock+and+bonds - โหมดความเข้ากันได้NATCHA TANAPANJAPORNNo ratings yet

- Ch07 BondsDocument44 pagesCh07 BondsRaazia GulNo ratings yet

- Cost of CapitalDocument39 pagesCost of CapitalGeethika NayanaprabhaNo ratings yet

- Investment AppraisalDocument3 pagesInvestment AppraisalDawar Hussain (WT)No ratings yet

- Intro To Oil & Gas IssuesDocument16 pagesIntro To Oil & Gas Issuesjeff.oneal23No ratings yet

- Applied Corporate Finance. What is a Company worth?From EverandApplied Corporate Finance. What is a Company worth?Rating: 3 out of 5 stars3/5 (2)

- 1.1 4 - Discounting Risky Cash FlowsDocument40 pages1.1 4 - Discounting Risky Cash Flowsmanoranjan838241No ratings yet

- Cost Benefit AnalysisDocument1 pageCost Benefit Analysismanoranjan838241No ratings yet

- Basel Norms IIDocument3 pagesBasel Norms IImanoranjan838241No ratings yet

- Formation of CompaniesDocument7 pagesFormation of Companiesmanoranjan838241No ratings yet

- MemorandumDocument11 pagesMemorandummanoranjan838241No ratings yet

- Memorandum of Artcles For AGM To Be Held On 23rd Novemver 2005Document45 pagesMemorandum of Artcles For AGM To Be Held On 23rd Novemver 2005manoranjan838241No ratings yet

- 3 BepDocument1 page3 Bepmanoranjan838241No ratings yet

- Break Even AnalysisDocument12 pagesBreak Even Analysismanoranjan838241No ratings yet

- A Break Even Analysis Is A MethodDocument2 pagesA Break Even Analysis Is A Methodmanoranjan838241No ratings yet

- Indiancompaniesact 1956Document18 pagesIndiancompaniesact 1956manoranjan838241No ratings yet

- Article 202Document14 pagesArticle 202manoranjan838241No ratings yet

- v28n3 3Document6 pagesv28n3 3manoranjan838241No ratings yet

- Cost - Benefit Training Handouts 9-02Document8 pagesCost - Benefit Training Handouts 9-02manoranjan838241No ratings yet

- Feasibility AnalysisDocument4 pagesFeasibility Analysismanoranjan838241No ratings yet

- DP 200906Document18 pagesDP 200906manoranjan838241No ratings yet

- Cost and Benefit AnalysisDocument1 pageCost and Benefit Analysismanoranjan838241No ratings yet

- Bonds IIIDocument2 pagesBonds IIImanoranjan838241No ratings yet

- BackyardTrends CBAIRRDocument2 pagesBackyardTrends CBAIRRmanoranjan838241No ratings yet

- Beta N GrowthDocument18 pagesBeta N Growthmanoranjan838241No ratings yet

- Bond ValuationDocument4 pagesBond Valuationmanoranjan838241No ratings yet

- Calculation of Stock BetaDocument2 pagesCalculation of Stock Betamanoranjan838241No ratings yet

- Business Valuation ModelDocument1 pageBusiness Valuation Modelmanoranjan838241No ratings yet

- FJMOMI en Brochure 1Document32 pagesFJMOMI en Brochure 1manoranjan838241No ratings yet

- Accounting For Employee Stock Option Plans: After Studying This Chapter, You Will Be Able ToDocument41 pagesAccounting For Employee Stock Option Plans: After Studying This Chapter, You Will Be Able ToSandeep As SandeepNo ratings yet

- IASB Project ForSMEDocument27 pagesIASB Project ForSMEAlexandre ValcazaraNo ratings yet

- Hindustan Construction CompanyDocument18 pagesHindustan Construction CompanySudipta BoseNo ratings yet

- PT Indocement Tunggal Prakarsa Tbk. and SubsidiariesDocument64 pagesPT Indocement Tunggal Prakarsa Tbk. and SubsidiariesJonathan OngNo ratings yet

- Binder - BARC CD SA Bank Forecasting ValuationDocument184 pagesBinder - BARC CD SA Bank Forecasting ValuationMarcus HowardNo ratings yet

- 0.80 Points: AwardDocument21 pages0.80 Points: AwardhirevNo ratings yet

- Ey Transitioning To New Leasing Standard Ind As 116 PDFDocument44 pagesEy Transitioning To New Leasing Standard Ind As 116 PDFGere TassewNo ratings yet

- Theories (IIA and PPE)Document6 pagesTheories (IIA and PPE)LDB Ashley Jeremiah Magsino - ABMNo ratings yet

- Leather GoodsDocument27 pagesLeather GoodsThomas M100% (1)

- DAIBB Lending - 2 - 0Document8 pagesDAIBB Lending - 2 - 0ashraf294No ratings yet

- Annual Report PindoDeli 2010 PDFDocument157 pagesAnnual Report PindoDeli 2010 PDFImago graphix100% (1)

- Financial Statement Analysis of Vinamilk: Fabrikam ResidencesDocument21 pagesFinancial Statement Analysis of Vinamilk: Fabrikam ResidencesThanh TrầnNo ratings yet

- Acct1501 Tutorial Questions Solutions Week3Document3 pagesAcct1501 Tutorial Questions Solutions Week3chunkityik100% (1)

- Partnership Dissolution Lecture NotesDocument7 pagesPartnership Dissolution Lecture NotesGene Marie PotencianoNo ratings yet

- Audrina AP2 QT21.2Document32 pagesAudrina AP2 QT21.2nguyenphamnhungoc51No ratings yet

- S 5.8-5.13 Limited CompaniesDocument11 pagesS 5.8-5.13 Limited CompaniesIlovejjcNo ratings yet

- Ar 2010 PDFDocument234 pagesAr 2010 PDFLala RifaNo ratings yet

- Analysis of Asian Paints Financial StatementsDocument12 pagesAnalysis of Asian Paints Financial StatementsSahil SondhiNo ratings yet

- Rezultate Financiare AppleDocument3 pagesRezultate Financiare AppleClaudiuNo ratings yet

- Measuring and Managing Brand LoyaltyDocument19 pagesMeasuring and Managing Brand LoyaltyPratibha SinghNo ratings yet

- RWJ Chapter 3 Financial Statements Analysis and Financial ModelsDocument34 pagesRWJ Chapter 3 Financial Statements Analysis and Financial ModelsAshekin MahadiNo ratings yet

- ØHPK14/C 67/1/1: Series SET 1Document24 pagesØHPK14/C 67/1/1: Series SET 1Ethan GomesNo ratings yet

- Financial PlanDocument16 pagesFinancial PlanSenpai Kun0% (1)

- CB Annual Report 2012 FINALDocument76 pagesCB Annual Report 2012 FINALcrystalmckenzie941No ratings yet

- Kalpataru Power Transmission LimitedDocument8 pagesKalpataru Power Transmission LimitedjayNo ratings yet

- Financial InstrumentDocument79 pagesFinancial InstrumentÑïkêţ BäûðhåNo ratings yet

- GSPrime Finance IB Fund Accounting Important QuestionsDocument34 pagesGSPrime Finance IB Fund Accounting Important Questionsnaghulk1No ratings yet

- Waterfront Philippines, Inc - Sec Form 17-A - 30june2020Document233 pagesWaterfront Philippines, Inc - Sec Form 17-A - 30june2020backup cmbmpNo ratings yet

- Ch06 Proactive Approach To Detecting FraudDocument26 pagesCh06 Proactive Approach To Detecting Fraud230191No ratings yet

- MRT JAKARTA Annual Report 2013 PDFDocument100 pagesMRT JAKARTA Annual Report 2013 PDFDanu RangkutiNo ratings yet