Download as pdf or txt

You might also like

- Notice of Assessment - Year Ended 30 June 2023: !H!ÎÈ/, g4 Î!Ef6ÄDocument4 pagesNotice of Assessment - Year Ended 30 June 2023: !H!ÎÈ/, g4 Î!Ef6Äjoshiepow3llNo ratings yet

- Australian Payslip Generator TemplateDocument1 pageAustralian Payslip Generator TemplateFarzinNo ratings yet

- Natalee Lang - Tax Notice of Assessment For 20202021Document2 pagesNatalee Lang - Tax Notice of Assessment For 20202021MWA Films100% (1)

- Your Centrelink Statement For Disability Support Pension: Reference: 204 552 505CDocument3 pagesYour Centrelink Statement For Disability Support Pension: Reference: 204 552 505CChellii McgrailNo ratings yet

- Notice of Assessment - Year Ended 30 June 2023: Miss Sheralie L Shadforth 8 Clabon ST Hillcrest QLD 4118Document2 pagesNotice of Assessment - Year Ended 30 June 2023: Miss Sheralie L Shadforth 8 Clabon ST Hillcrest QLD 4118shadforth1977No ratings yet

- Notice of Assessment - Year Ended 30 June 2023: Miss Hina Khan Unit 24 29 Nicholls Tce Woodville West Sa 5011Document2 pagesNotice of Assessment - Year Ended 30 June 2023: Miss Hina Khan Unit 24 29 Nicholls Tce Woodville West Sa 5011hina khanNo ratings yet

- Noa 2022Document2 pagesNoa 2022ragprasathNo ratings yet

- Notice of Assessment - Year Ended 30 June 2020: Ms Elaine S Ross 64 Corrofin ST Ferny Grove QLD 4055Document2 pagesNotice of Assessment - Year Ended 30 June 2020: Ms Elaine S Ross 64 Corrofin ST Ferny Grove QLD 4055Vaccine ScamNo ratings yet

- StatementDocument62 pagesStatementisaac ellisNo ratings yet

- Early Release Superannuation Approval 7115569398585Document1 pageEarly Release Superannuation Approval 7115569398585DanielWildSheepZaninNo ratings yet

- Notice of Assessment - Year Ended 30 June 2022Document2 pagesNotice of Assessment - Year Ended 30 June 2022G100% (1)

- Your Centrelink Statement For Parenting Payment: Reference: 207 828 705JDocument3 pagesYour Centrelink Statement For Parenting Payment: Reference: 207 828 705JLupe VakaNo ratings yet

- Child Care Subsidy (0028112904)Document9 pagesChild Care Subsidy (0028112904)ammar naeemNo ratings yet

- Centrelink PaygDocument1 pageCentrelink PaygChandra BhattNo ratings yet

- Income Statement: Llillliltll) Ilililtil)Document1 pageIncome Statement: Llillliltll) Ilililtil)Indy EfuNo ratings yet

- 26082021-PAYG Payment Summary-G Khajarian (CLAIM-00464429)Document1 page26082021-PAYG Payment Summary-G Khajarian (CLAIM-00464429)Garo KhatcherianNo ratings yet

- Business Activity Statement: Summary of AmountsDocument2 pagesBusiness Activity Statement: Summary of AmountsSimona StratulatNo ratings yet

- Chorinho Pacoqui o Du SilvaDocument9 pagesChorinho Pacoqui o Du SilvaAlejo GarciaNo ratings yet

- PAYG Payment Summary Individual Non-Business: Ai Thi Hoai Nguyen 1/3 Mary ST North Melbourne Vic 3051Document1 pagePAYG Payment Summary Individual Non-Business: Ai Thi Hoai Nguyen 1/3 Mary ST North Melbourne Vic 3051hungdahoangNo ratings yet

- Medicare Enrolment Form (MS004) PDFDocument13 pagesMedicare Enrolment Form (MS004) PDFDanielWildSheepZaninNo ratings yet

- Your Centrelink Statement For Youth Allowance: Reference: 280 993 398VDocument3 pagesYour Centrelink Statement For Youth Allowance: Reference: 280 993 398Vbob0% (1)

- Wage Easy ATO Payment Summaries (2018 Jun 28)Document1 pageWage Easy ATO Payment Summaries (2018 Jun 28)Haillander Lopes viannaNo ratings yet

- CV Daniel PDFDocument3 pagesCV Daniel PDFDanielWildSheepZaninNo ratings yet

- Allotment LetterDocument4 pagesAllotment LetteranjumNo ratings yet

- PDF Payment Summary 2022 - 2023Document1 pagePDF Payment Summary 2022 - 2023Ashley RouxNo ratings yet

- SR Notice of Assessment 2015Document1 pageSR Notice of Assessment 2015Ded MarozNo ratings yet

- Prefill 2019Document2 pagesPrefill 2019Usama AshfaqNo ratings yet

- Income Tax Account Statement of Account: MR Brock W Johnson 177 Barrabool RD Highton Vic 3216Document2 pagesIncome Tax Account Statement of Account: MR Brock W Johnson 177 Barrabool RD Highton Vic 3216Annie LamNo ratings yet

- Sagar Sapkota Full Application PDFDocument14 pagesSagar Sapkota Full Application PDFAnnie LamNo ratings yet

- PAYG Payment Summary - Individual Non-Business: Fook Ngo 139 Railway Avenue Laverton VIC 3028Document1 pagePAYG Payment Summary - Individual Non-Business: Fook Ngo 139 Railway Avenue Laverton VIC 3028Fook NgoNo ratings yet

- Nat14869 01.2006Document1 pageNat14869 01.2006stive007No ratings yet

- Income and Asset Statement (Financial Planner) - G324503937Document2 pagesIncome and Asset Statement (Financial Planner) - G324503937Adam BookerNo ratings yet

- PAYG Payment Summary - Individual Non-Business: Matthew Burn 1933b/702 Harris Street Ultimo NSW 2007Document1 pagePAYG Payment Summary - Individual Non-Business: Matthew Burn 1933b/702 Harris Street Ultimo NSW 2007Anonymous JytY5quhSgNo ratings yet

- Income Tax Account Statement of Account: MR Daniel Zanin 25 Bulgoon CR Ocean Shores NSW 2483Document2 pagesIncome Tax Account Statement of Account: MR Daniel Zanin 25 Bulgoon CR Ocean Shores NSW 2483DanielWildSheepZaninNo ratings yet

- Print - Australian Taxation OfficeDocument2 pagesPrint - Australian Taxation OfficeThi MaiNo ratings yet

- Important Information - M269602760Document2 pagesImportant Information - M269602760jason masciNo ratings yet

- PAYG Payment Summary - Individual Non-Business: Muhammad Danish 22/324 Woodstock Avenue Mount Druitt NSW 2770Document1 pagePAYG Payment Summary - Individual Non-Business: Muhammad Danish 22/324 Woodstock Avenue Mount Druitt NSW 2770Danish MuhammadNo ratings yet

- Manpreet Kaur USQ Application FormDocument5 pagesManpreet Kaur USQ Application FormGagandeep KaurNo ratings yet

- The Property Investors Alliance: Electricity Gas Phone Internet Pay TV InsuranceDocument4 pagesThe Property Investors Alliance: Electricity Gas Phone Internet Pay TV InsuranceRaza RNo ratings yet

- Your Statement: Smart AccessDocument16 pagesYour Statement: Smart AccessDanielWildSheepZaninNo ratings yet

- Application 97586 PDFDocument3 pagesApplication 97586 PDFAnnie LamNo ratings yet

- Modp 2303en F MergedDocument17 pagesModp 2303en F MergedAliyana SmolderhalderNo ratings yet

- HR Manager Digital Technology & Innovation 1 Charles ST, Level 3A ParramattaDocument3 pagesHR Manager Digital Technology & Innovation 1 Charles ST, Level 3A ParramattaKiran PNo ratings yet

- NRAS Tenancy Managers - Australian Government Department Families, Housing, Community Services and Indigenous AffairsDocument12 pagesNRAS Tenancy Managers - Australian Government Department Families, Housing, Community Services and Indigenous Affairsbackch9011No ratings yet

- Centrelink StatementDocument3 pagesCentrelink StatementAdam Di GiuseppeNo ratings yet

- Pay Slip 20200814Document1 pagePay Slip 20200814Mohammed JunaidNo ratings yet

- Overpayment M249802319Document2 pagesOverpayment M249802319Simon ChownNo ratings yet

- Congratulations On A Great Choice!: Paying Your PremiumDocument5 pagesCongratulations On A Great Choice!: Paying Your Premiummark georgeNo ratings yet

- Oscf PDFDocument9 pagesOscf PDFAnnie LamNo ratings yet

- Barry 2003 ITRDocument6 pagesBarry 2003 ITRGreg O'MearaNo ratings yet

- 0131xxxxxxxx8984 - 2022 12 09Document12 pages0131xxxxxxxx8984 - 2022 12 09pitnew618No ratings yet

- PAYG Payment Summary - Individual Non-BusinessDocument1 pagePAYG Payment Summary - Individual Non-BusinessShubham SurekaNo ratings yet

- Parenting Payment - P240503786Document2 pagesParenting Payment - P240503786Izzy BaeNo ratings yet

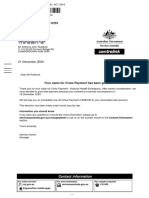

- Grant For Crisis Payment S303833612Document2 pagesGrant For Crisis Payment S303833612anthony rudduck100% (1)

- ANZ BankDocument6 pagesANZ BankВлад АнгелNo ratings yet

- About Sanda Islam Your Family Assistance: Reference: 605 730 292XDocument3 pagesAbout Sanda Islam Your Family Assistance: Reference: 605 730 292XAriful RussellNo ratings yet

- Emergency Recovery Payment Grant A199480158Document2 pagesEmergency Recovery Payment Grant A199480158HenhamNo ratings yet

- Tat ATO 2022Document3 pagesTat ATO 2022Tate chanNo ratings yet

- VEVO Visa Details Check - Munna BaruaDocument3 pagesVEVO Visa Details Check - Munna Baruaakkashhussain005No ratings yet

- Notice of Amended Assessment - Year Ended 30 June 2022: !msîzdçuy/ Î!Iu - ÄDocument4 pagesNotice of Amended Assessment - Year Ended 30 June 2022: !msîzdçuy/ Î!Iu - Äellas-dadNo ratings yet

- Notice of Amended Assessment - Year Ended 30 June 2023Document4 pagesNotice of Amended Assessment - Year Ended 30 June 2023carmenzhou2001No ratings yet

- E-Auctions - MSTC Limited-TATA POWER HALDIADocument7 pagesE-Auctions - MSTC Limited-TATA POWER HALDIAmannakauNo ratings yet

- Agent/ Intermediary Name and Code:POLICYBAZAAR INSURANCE BROKERS PRIVATE LIMITED BRC0000434Document5 pagesAgent/ Intermediary Name and Code:POLICYBAZAAR INSURANCE BROKERS PRIVATE LIMITED BRC0000434hiteshmohakar15No ratings yet

- LAPD-IT-G17 - Basic Guide To Tax Deductible Donations - External GuideDocument17 pagesLAPD-IT-G17 - Basic Guide To Tax Deductible Donations - External GuidePheletso RigdwayNo ratings yet

- GlobalizationDocument4 pagesGlobalizationMark MorongeNo ratings yet

- Exercises 4 Financial Planning BudgetingDocument2 pagesExercises 4 Financial Planning BudgetingKyle PereiraNo ratings yet

- Acc 5 Course OutlineDocument7 pagesAcc 5 Course OutlineArvin Glen BeltranNo ratings yet

- Adjusted Present Value Method of Project AppraisalDocument7 pagesAdjusted Present Value Method of Project AppraisalAhmed RazaNo ratings yet

- Abuse of Incorporation of Company To Commit FraudDocument6 pagesAbuse of Incorporation of Company To Commit FraudPriyanka TaktawalaNo ratings yet

- Combine Tax Module 2020 - For BIRDocument2,701 pagesCombine Tax Module 2020 - For BIRDave Banay Yabo, LPTNo ratings yet

- 01 Republic Vs CA, 258 SCRA 712Document6 pages01 Republic Vs CA, 258 SCRA 712Louiegie Thomas San JuanNo ratings yet

- Statement 4597116Document1 pageStatement 4597116Thalia Pajares ArangurenNo ratings yet

- Income Taxation Reviewer PDFDocument65 pagesIncome Taxation Reviewer PDFPaulo Joshua Abasolo BetacheNo ratings yet

- Cambridge History of Latin America 04, 1870-1930Document681 pagesCambridge History of Latin America 04, 1870-1930beatrizp85100% (3)

- Test BankDocument33 pagesTest BankThelma T. DancelNo ratings yet

- Pas 14 Segment ReportingDocument3 pagesPas 14 Segment ReportingrandyNo ratings yet

- Regulation and DevelopmentDocument293 pagesRegulation and DevelopmentG LzNo ratings yet

- DT 0108a Employer Annual Tax Deduction Schedule v1 2Document1 pageDT 0108a Employer Annual Tax Deduction Schedule v1 2joseph borketeyNo ratings yet

- PAC vs. Lim (G. R. No. 119775 - October 24, 2003)Document5 pagesPAC vs. Lim (G. R. No. 119775 - October 24, 2003)Lecdiee Nhojiezz Tacissea SalnackyiNo ratings yet

- Awara Study Russia Economy 09.12.2014Document67 pagesAwara Study Russia Economy 09.12.2014Мирослав ВујицаNo ratings yet

- Tender Document JSSDocument58 pagesTender Document JSSSunilkumar CeNo ratings yet

- AnswersDocument5 pagesAnswersrasangana arampathNo ratings yet

- HERON - D 2 2 - Annex 5 GreeceDocument25 pagesHERON - D 2 2 - Annex 5 GreeceMoldoveanu BogdanNo ratings yet

- S S T P S Wyoming: NtroductionDocument4 pagesS S T P S Wyoming: NtroductionManoj GNo ratings yet

- ch-07 Dividend and DDTDocument57 pagesch-07 Dividend and DDTdean.socNo ratings yet

- Islamabad Capital Territory (Tax On Services) Ordinance, 2001Document12 pagesIslamabad Capital Territory (Tax On Services) Ordinance, 2001Bilal KhanNo ratings yet

- 4.3 Solution To Income From Salary - Class Work & Home Assignment QuestionsDocument39 pages4.3 Solution To Income From Salary - Class Work & Home Assignment QuestionsKASHISH GUPTANo ratings yet

- A Project ProposalDocument8 pagesA Project ProposalPasang TamangNo ratings yet

- Daily Express 2011.01.05Document80 pagesDaily Express 2011.01.05Michał MatuszewskiNo ratings yet

- India Price List 2017-18 PDFDocument100 pagesIndia Price List 2017-18 PDF10605114No ratings yet