Download as pdf or txt

You might also like

- Elasticity of Demand ADocument4 pagesElasticity of Demand AAzlan Psp67% (3)

- The Impact of The Monetary and Fiscal Policy in VietnamDocument46 pagesThe Impact of The Monetary and Fiscal Policy in VietnamNhi DươngNo ratings yet

- Amazon Strategic AnalysisDocument44 pagesAmazon Strategic AnalysisBradley Paynter83% (6)

- Merton Truck CompanyDocument16 pagesMerton Truck CompanyAmeeno Pradeep PaulNo ratings yet

- Us Integrated Steel Mills Case StudyDocument7 pagesUs Integrated Steel Mills Case StudyraymundsagumNo ratings yet

- Leverages - SecL (1)Document7 pagesLeverages - SecL (1)Lucifer vazNo ratings yet

- Manajemen Keuangan Kelompok 4Document13 pagesManajemen Keuangan Kelompok 4rasyaraji rachmadiNo ratings yet

- Leverage: Analysis (Analysis Dan Implikasi Pengungkit)Document28 pagesLeverage: Analysis (Analysis Dan Implikasi Pengungkit)arigiofaniNo ratings yet

- 05 BEP and LeverageDocument30 pages05 BEP and LeverageAyushNo ratings yet

- Quiz 6 NotesDocument14 pagesQuiz 6 NotesEmily SNo ratings yet

- Inancing Ecisions Everages: Learning OutcomesDocument35 pagesInancing Ecisions Everages: Learning OutcomesBhai LangurNo ratings yet

- Leverages MaterialDocument15 pagesLeverages MaterialsreevardhanNo ratings yet

- Inancing Ecisions Everages: Analysis of LeverageDocument8 pagesInancing Ecisions Everages: Analysis of LeverageParth BindalNo ratings yet

- Everage: Sales (S) 90,000 90,000 3000 Units at Rs. 30/-Per Unit 15 Per Unit 45,000 45,000Document20 pagesEverage: Sales (S) 90,000 90,000 3000 Units at Rs. 30/-Per Unit 15 Per Unit 45,000 45,000anon_67206536260% (5)

- (8b) Analysis of Leverages (Cir. 9.3.2017)Document44 pages(8b) Analysis of Leverages (Cir. 9.3.2017)Sarvar PathanNo ratings yet

- FM - Analysis of Leverages (Cir. 26.3.2020)Document55 pagesFM - Analysis of Leverages (Cir. 26.3.2020)Owais KadiriNo ratings yet

- LeveragesDocument12 pagesLeveragesjoshipragati123No ratings yet

- LeverageDocument23 pagesLeverageHanuman PrasadNo ratings yet

- LeverageDocument20 pagesLeveragekapish1mittal100% (1)

- Hid - Chapter IV Capital Structure PolicyDocument18 pagesHid - Chapter IV Capital Structure PolicyTsi AwekeNo ratings yet

- LeverageDocument7 pagesLeverageKomal ThakurNo ratings yet

- Capital StructureDocument32 pagesCapital Structurestd30000No ratings yet

- Ch15 Capital Structure and Leverage-1Document44 pagesCh15 Capital Structure and Leverage-1Fizza AwanNo ratings yet

- Leverage: Definition 1Document11 pagesLeverage: Definition 1diptishahNo ratings yet

- LEVERAGESDocument96 pagesLEVERAGESNaman LadhaNo ratings yet

- Chapter 4 Capital Structure PolicyDocument17 pagesChapter 4 Capital Structure PolicyAndualem ZenebeNo ratings yet

- LeveragesDocument50 pagesLeveragesPrem KishanNo ratings yet

- Brought To YouDocument35 pagesBrought To YouJoseph Mejia LaosNo ratings yet

- MBA Advance Financial Management - ASYNCHRONUS ACTIVITYDocument9 pagesMBA Advance Financial Management - ASYNCHRONUS ACTIVITYDaniella LampteyNo ratings yet

- LEVERAGEDocument19 pagesLEVERAGEraka1010100% (10)

- Leverage AnalysisDocument22 pagesLeverage AnalysisSiddharthNo ratings yet

- 3 - Topic3 Financial and Operating Leveraging-EditedDocument44 pages3 - Topic3 Financial and Operating Leveraging-EditedCOCONUTNo ratings yet

- Leverage Unit-4 Part - IIDocument34 pagesLeverage Unit-4 Part - IIAstha ParmanandkaNo ratings yet

- CH.6 Financial Structure & The Uses of LeverageDocument16 pagesCH.6 Financial Structure & The Uses of LeverageMark KaiserNo ratings yet

- ST-1 (Analysis of Recessionary Cash Flows) ADocument4 pagesST-1 (Analysis of Recessionary Cash Flows) AGA ZinNo ratings yet

- LeverageDocument16 pagesLeverageanshuldceNo ratings yet

- Report of Finanacial LeverageDocument6 pagesReport of Finanacial LeverageCherryThai PhamNo ratings yet

- Chapter 15 - Analysis and Impact of LeverageDocument38 pagesChapter 15 - Analysis and Impact of LeveragepranavNo ratings yet

- Financial Mgt. Capital Structure M.Com. Sem-II - Sukumar PalDocument19 pagesFinancial Mgt. Capital Structure M.Com. Sem-II - Sukumar PalalokNo ratings yet

- Fm-Ii CH-1-2Document81 pagesFm-Ii CH-1-2gadisadaraje4No ratings yet

- Unit 3 LeveragesDocument25 pagesUnit 3 LeveragesKhushi DNo ratings yet

- LeverageDocument8 pagesLeverageKalam SikderNo ratings yet

- 02 Financing Decisions - Leverages - Practice SheetDocument22 pages02 Financing Decisions - Leverages - Practice SheetPatrick LoboNo ratings yet

- LeverageDocument14 pagesLeverageSurya ElvinoNo ratings yet

- CH 01 Basic Concepts R04 NotesDocument14 pagesCH 01 Basic Concepts R04 NoteschandreshNo ratings yet

- Operating and Financial LeverageDocument31 pagesOperating and Financial LeveragebharatNo ratings yet

- Week 5 - Risk Analysis and LeverageDocument20 pagesWeek 5 - Risk Analysis and LeveragePollsNo ratings yet

- Practice MC Questions CH 16Document3 pagesPractice MC Questions CH 16business docNo ratings yet

- LeverageDocument6 pagesLeverageAhsane RNo ratings yet

- Finance For Managers-Module 4B-LeveragesDocument27 pagesFinance For Managers-Module 4B-LeveragesChayaGandhiNo ratings yet

- Leverage: Leverage Is That Portion of The Fixed Costs Which Represents A Risk To The Firm. TypesDocument17 pagesLeverage: Leverage Is That Portion of The Fixed Costs Which Represents A Risk To The Firm. Typessameer0725No ratings yet

- Marginal Costing Technique: Break-Even AnalysisDocument9 pagesMarginal Costing Technique: Break-Even AnalysisAadarshNo ratings yet

- Dol DFL DTLDocument30 pagesDol DFL DTLZiya M MursalzadeNo ratings yet

- Capital Structure TheoriesDocument12 pagesCapital Structure Theoriesganesh gowthamNo ratings yet

- Section CDocument3 pagesSection Cshaik safiyaNo ratings yet

- LeverageDocument6 pagesLeverageutkarsh.khera98No ratings yet

- Leverage AnalysisDocument29 pagesLeverage AnalysisFALAK OBERAINo ratings yet

- CH 5Document21 pagesCH 5gebremedhnNo ratings yet

- Optimal Financing MixDocument4 pagesOptimal Financing MixSana SarfarazNo ratings yet

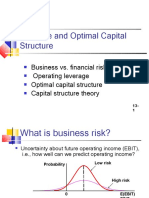

- Leverage and Optimal Capital StructureDocument42 pagesLeverage and Optimal Capital StructureInvisible CionNo ratings yet

- 4 The Firm's Capital Structure and Degree of LeverageDocument9 pages4 The Firm's Capital Structure and Degree of LeverageMariel GarraNo ratings yet

- FM CH - ViDocument34 pagesFM CH - ViGizaw BelayNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Beyond Earnings: Applying the HOLT CFROI and Economic Profit FrameworkFrom EverandBeyond Earnings: Applying the HOLT CFROI and Economic Profit FrameworkNo ratings yet

- Unit 10Document20 pagesUnit 10sheetal gudseNo ratings yet

- Unit 7Document12 pagesUnit 7sheetal gudseNo ratings yet

- Unit 5Document25 pagesUnit 5sheetal gudseNo ratings yet

- Unit 6Document9 pagesUnit 6sheetal gudseNo ratings yet

- Unit 2Document16 pagesUnit 2sheetal gudseNo ratings yet

- BUS3310Document83 pagesBUS3310valero506No ratings yet

- Economics QuestionsDocument6 pagesEconomics Questionsdoggogood9No ratings yet

- Balance of Payments - NotesDocument6 pagesBalance of Payments - NotesJay-an CastillonNo ratings yet

- Aspects of Land Valuation: AUP 3161 (3 Credit Hours) Lecture 1: Introduction To Land ValuationDocument14 pagesAspects of Land Valuation: AUP 3161 (3 Credit Hours) Lecture 1: Introduction To Land ValuationNasrul HanisNo ratings yet

- Chapter 2 - Theory - 6Document32 pagesChapter 2 - Theory - 6Diptish RamtekeNo ratings yet

- Chapter 1: A Simple Market ModelDocument8 pagesChapter 1: A Simple Market ModelblillahNo ratings yet

- 14 - Presentation On Commodity TradingDocument15 pages14 - Presentation On Commodity TradingvijayxkumarNo ratings yet

- Session - 048Document9 pagesSession - 048Abcdef GhNo ratings yet

- Southeast Asia Thriving in The Shadow of GiantsDocument38 pagesSoutheast Asia Thriving in The Shadow of GiantsDDNo ratings yet

- Eco 362 Module 5Document33 pagesEco 362 Module 5ayantayo TolulopeNo ratings yet

- JKT PVT LTDDocument8 pagesJKT PVT LTDSathiya YorathNo ratings yet

- CRM in Service IndustryDocument21 pagesCRM in Service IndustryKarishma VijayNo ratings yet

- (Erik S. Reinert, Francesca L. Viano) Thorstein VeDocument392 pages(Erik S. Reinert, Francesca L. Viano) Thorstein VeUdurunNo ratings yet

- RES Essay Competition 2014 Judges Report & Winning EssaysDocument38 pagesRES Essay Competition 2014 Judges Report & Winning EssaysAxelNo ratings yet

- Case Acron PharmaDocument23 pagesCase Acron PharmanishanthNo ratings yet

- Determinants of Beta: FormallyDocument13 pagesDeterminants of Beta: FormallyvinagoyaNo ratings yet

- 7Document12 pages7JaeDukAndrewSeo100% (1)

- Chap14 Stabilization PolicyDocument38 pagesChap14 Stabilization PolicyKharisma ArtaNo ratings yet

- Marketing Plan - MMDocument11 pagesMarketing Plan - MMAmbiga Ambi BigaNo ratings yet

- HR Management in International Airports in TransitionDocument7 pagesHR Management in International Airports in TransitionrkbaaiNo ratings yet

- Chapter 6 Common Stock FundamentalsDocument6 pagesChapter 6 Common Stock FundamentalsbibekNo ratings yet

- The Pedagogy of The Open Society - Knowledge and The Governance of Higher EducationDocument141 pagesThe Pedagogy of The Open Society - Knowledge and The Governance of Higher EducationYawnathan LinNo ratings yet

- EC1101E: Introduction To Economic AnalysisDocument79 pagesEC1101E: Introduction To Economic AnalysisdineshNo ratings yet

- Scps FinanceDocument19 pagesScps FinanceIsaac BernsteinNo ratings yet

- Payout RatioDocument2 pagesPayout Ratiosunil.sNo ratings yet