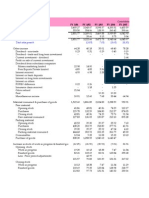

Date of Report Tuesday, April 29, 2008 SRF Limited - Quick & Dirty Analysis Analyst Dhananjayan J Contact

Date of Report Tuesday, April 29, 2008 SRF Limited - Quick & Dirty Analysis Analyst Dhananjayan J Contact

You might also like

- Comparative Income Statements and Balance Sheets For Merck ($ Millions) FollowDocument6 pagesComparative Income Statements and Balance Sheets For Merck ($ Millions) FollowIman naufalNo ratings yet

- 17020841116Document13 pages17020841116Khushboo RajNo ratings yet

- Macrs Depreciation: New Smart Phone Calculation AnalysisDocument4 pagesMacrs Depreciation: New Smart Phone Calculation AnalysisErro Jaya Rosady100% (1)

- Directors of Federal Reserve Bank of New York (1914-2014)Document47 pagesDirectors of Federal Reserve Bank of New York (1914-2014)William Litynski100% (1)

- Lease ContractDocument2 pagesLease ContractAngie NaveraNo ratings yet

- Financial Analysis of P & GDocument25 pagesFinancial Analysis of P & Ghitesh_mahajan_3No ratings yet

- Hgs Q4 & Full Year Fy2018 Financials & Fact Sheet: Hinduja Global Solutions LimitedDocument6 pagesHgs Q4 & Full Year Fy2018 Financials & Fact Sheet: Hinduja Global Solutions LimitedChirag LaxmanNo ratings yet

- Gail (India)Document93 pagesGail (India)Ashley KamalasanNo ratings yet

- WA2Document3 pagesWA2Ahmed HassaanNo ratings yet

- Horizontal & Vertical Analysis of Maruti Suzuki India LTDDocument17 pagesHorizontal & Vertical Analysis of Maruti Suzuki India LTDBerkshire Hathway coldNo ratings yet

- DCF Valuation ExerciseDocument18 pagesDCF Valuation ExerciseAkram MohiddinNo ratings yet

- Profitability Ratio 2Document18 pagesProfitability Ratio 2Wynphap podiotanNo ratings yet

- Result Update Presentation - Q2 FY18: NOVEMBER 09, 2017Document11 pagesResult Update Presentation - Q2 FY18: NOVEMBER 09, 2017Mohit PariharNo ratings yet

- WSP OpModelPrepDocument22 pagesWSP OpModelPreplewisbjunkNo ratings yet

- A2.1 Roe 1Document14 pagesA2.1 Roe 1monemNo ratings yet

- TVS Motor Company: CMP: INR549 TP: INR548Document12 pagesTVS Motor Company: CMP: INR549 TP: INR548anujonwebNo ratings yet

- Financial Ratios Activity Answer KeyDocument8 pagesFinancial Ratios Activity Answer KeyMarienell YuNo ratings yet

- CHB Jun19 PDFDocument14 pagesCHB Jun19 PDFSajeetha MadhavanNo ratings yet

- Financial Modeling - Module I - Workbook 09.28.09Document38 pagesFinancial Modeling - Module I - Workbook 09.28.09rabiaasimNo ratings yet

- Learn2Invest Session 10 - Asian Paints ValuationsDocument8 pagesLearn2Invest Session 10 - Asian Paints ValuationsMadhur BathejaNo ratings yet

- CLA KPI BOD MayDocument248 pagesCLA KPI BOD MaySiluman UlarNo ratings yet

- Chapter 2 - Financial StatementsDocument23 pagesChapter 2 - Financial StatementsErone Edward CatolinNo ratings yet

- Sothin and SonsDocument16 pagesSothin and SonsDicksonNo ratings yet

- Illustration For Financial Analysis Using RatioDocument2 pagesIllustration For Financial Analysis Using RatioamahaktNo ratings yet

- Balkrishna Industries LTD: Investor Presentation February 2020Document30 pagesBalkrishna Industries LTD: Investor Presentation February 2020PIBM MBA-FINANCENo ratings yet

- Reshma Chauhan - PGFC1927 (BOCA)Document9 pagesReshma Chauhan - PGFC1927 (BOCA)Surbhî GuptaNo ratings yet

- Financial Analysis: Nestle India Ltd. ACC LTDDocument20 pagesFinancial Analysis: Nestle India Ltd. ACC LTDrahil0786No ratings yet

- Whirlpool Financial AnalysisDocument5 pagesWhirlpool Financial AnalysisuddhavkulkarniNo ratings yet

- Company AssignmentDocument3 pagesCompany Assignmentrajeshparida9624No ratings yet

- Semen Indonesia Persero TBK PT: at A GlanceDocument3 pagesSemen Indonesia Persero TBK PT: at A GlanceRendy SentosaNo ratings yet

- Result Update Presentation - Q1 FY18: AUGUST 10, 2017Document10 pagesResult Update Presentation - Q1 FY18: AUGUST 10, 2017Mohit PariharNo ratings yet

- Ratio Analysis Summary Particulars Mar '17 Mar '18 Mar '19 Revenue Growth Profitability RatiosDocument10 pagesRatio Analysis Summary Particulars Mar '17 Mar '18 Mar '19 Revenue Growth Profitability RatiosKAVYA GUPTANo ratings yet

- I. Financial AssumptionsDocument14 pagesI. Financial AssumptionsJaera shopaholicNo ratings yet

- What Do We Achive? Interpretation: Other PointsDocument3 pagesWhat Do We Achive? Interpretation: Other PointsDibyaranjan SahooNo ratings yet

- Abrar Engro Excel SheetDocument4 pagesAbrar Engro Excel SheetManahil FayyazNo ratings yet

- Total Revenue: Income StatementDocument4 pagesTotal Revenue: Income Statementmonica asifNo ratings yet

- Vivimed Model VFDocument19 pagesVivimed Model VFShaileshAgrawalNo ratings yet

- Ashok Leyland: CMP: INR115 TP: INR134 (+17%)Document10 pagesAshok Leyland: CMP: INR115 TP: INR134 (+17%)Jitendra GaglaniNo ratings yet

- FM Assignment UcDocument4 pagesFM Assignment UcabhishelNo ratings yet

- Cortez Exam in Business FinanceDocument4 pagesCortez Exam in Business FinanceFranchesca CortezNo ratings yet

- Fixed Assets: Case 25.1: Patel Computers System AssetsDocument2 pagesFixed Assets: Case 25.1: Patel Computers System AssetsMukul KadyanNo ratings yet

- Accounts AssignmentDocument17 pagesAccounts AssignmentApoorvNo ratings yet

- Gita AgricultureDocument20 pagesGita AgriculturemrigendrarimalNo ratings yet

- Bank Performance Analysis - Anushka Gupta (Kotak Mahindra Bank)Document13 pagesBank Performance Analysis - Anushka Gupta (Kotak Mahindra Bank)Surbhî GuptaNo ratings yet

- FinancialsDocument10 pagesFinancialstimothyNo ratings yet

- Spread SheetDocument2 pagesSpread SheetDwi PermanaNo ratings yet

- Lbo W DCF Model SampleDocument33 pagesLbo W DCF Model Samplejulita rachmadewiNo ratings yet

- HDFC Bank Annual ReportDocument1 pageHDFC Bank Annual ReportlovenotafeelingNo ratings yet

- FinShiksha Maruti Suzuki UnsolvedDocument12 pagesFinShiksha Maruti Suzuki UnsolvedGANESH JAINNo ratings yet

- Alembic Angel 020810Document12 pagesAlembic Angel 020810giridesh3No ratings yet

- 11.bergerac SystemsDocument12 pages11.bergerac SystemsAviralNo ratings yet

- Mett International Pty LTD Financial Forecast 3 Year SummaryDocument134 pagesMett International Pty LTD Financial Forecast 3 Year SummaryJamilexNo ratings yet

- DCFValuation JKTyre1Document195 pagesDCFValuation JKTyre1Chulbul PandeyNo ratings yet

- Kotak Mahindra Bank Ltd. Performance Analysis For The Period 2016-2020Document15 pagesKotak Mahindra Bank Ltd. Performance Analysis For The Period 2016-2020Surbhî GuptaNo ratings yet

- A1.2 Roic TreeDocument9 pagesA1.2 Roic Treesara_AlQuwaifliNo ratings yet

- Horizontal AnalysisDocument1 pageHorizontal Analysiswill burrNo ratings yet

- Financial RatiosDocument7 pagesFinancial RatiosJan TruongNo ratings yet

- MODEL - Investment AnalysisDocument6 pagesMODEL - Investment AnalysisAndrei Cătălin UngureanuNo ratings yet

- Equity Valuation: Models from Leading Investment BanksFrom EverandEquity Valuation: Models from Leading Investment BanksJan ViebigNo ratings yet

- Indian Insider Buyings June 19, 2008-DhananDocument2 pagesIndian Insider Buyings June 19, 2008-Dhananapi-3702531No ratings yet

- GilletteDocument14 pagesGilletteapi-3702531No ratings yet

- Dabur IndiaDocument43 pagesDabur Indiaapi-3702531No ratings yet

- Colgate AR March 2005Document72 pagesColgate AR March 2005ashusingh0141No ratings yet

- Fem CareDocument16 pagesFem Careapi-3702531No ratings yet

- ColgateDocument32 pagesColgateapi-3702531No ratings yet

- DUBARINDIAAR200708Document164 pagesDUBARINDIAAR200708Santosh KumarNo ratings yet

- India - Insider Buying 25th July 2008Document2 pagesIndia - Insider Buying 25th July 2008api-3702531No ratings yet

- ColgateDocument32 pagesColgateapi-3702531No ratings yet

- BSE Special Situations 17th June 2008Document2 pagesBSE Special Situations 17th June 2008api-3702531No ratings yet

- BSE Special Situations 16th June 2008Document4 pagesBSE Special Situations 16th June 2008api-3702531No ratings yet

- BSE Special Situations 18th June 2008Document1 pageBSE Special Situations 18th June 2008api-3702531No ratings yet

- Indian Insider Buyings June 17, 2008-DhananDocument2 pagesIndian Insider Buyings June 17, 2008-Dhananapi-3702531No ratings yet

- Indian Insider Buyings June 13, 2008-DhananDocument2 pagesIndian Insider Buyings June 13, 2008-Dhananapi-3702531No ratings yet

- Indian Insider Buyings June 12, 2008-DhananDocument2 pagesIndian Insider Buyings June 12, 2008-Dhananapi-3702531No ratings yet

- IAPMDocument4 pagesIAPMapi-3699305No ratings yet

- Your Money or Your Life Book ReviewDocument5 pagesYour Money or Your Life Book ReviewSaurabhkumar SinghNo ratings yet

- Test Business and FinanceDocument1 pageTest Business and FinanceKarem Yessenia OCHOCHOQUE SÁNCHEZNo ratings yet

- Hull OFOD10e MultipleChoice Questions Only Ch22Document4 pagesHull OFOD10e MultipleChoice Questions Only Ch22Kevin Molly KamrathNo ratings yet

- Project Selection Process: A) SWOT AnalysisDocument6 pagesProject Selection Process: A) SWOT AnalysisIrtiza MalikNo ratings yet

- Cash Credit Proposal For Bank FinanceDocument15 pagesCash Credit Proposal For Bank Financeajaya thakurNo ratings yet

- A. Bank Rate PolicyDocument4 pagesA. Bank Rate PolicySIMRAN SHOKEENNo ratings yet

- Architect Agreement Contract 2 PDFDocument5 pagesArchitect Agreement Contract 2 PDFS Lakhte Haider ZaidiNo ratings yet

- Course Handout MBA 306 FIN FSIDocument3 pagesCourse Handout MBA 306 FIN FSIAsma KhanNo ratings yet

- Bia Africa - Commercial Offer 2022 SMS - Feb 2023 - Eur - 230406 - 100334Document12 pagesBia Africa - Commercial Offer 2022 SMS - Feb 2023 - Eur - 230406 - 100334Kouakou Affran Rania maryliseNo ratings yet

- Law Juridical RelationDocument3 pagesLaw Juridical RelationAida StanNo ratings yet

- Sap Fi ReportsDocument41 pagesSap Fi Reportssushilo_2100% (1)

- Current and Savings Account User Manual 1 PDFDocument772 pagesCurrent and Savings Account User Manual 1 PDFthandayuthapani sundarNo ratings yet

- Project Profile Rice MillDocument1 pageProject Profile Rice Millhoquetradeintl100% (2)

- Safari - Aug 9, 2019 at 7:11 AM PDFDocument1 pageSafari - Aug 9, 2019 at 7:11 AM PDFMikaela SamonteNo ratings yet

- Economic ReformsDocument77 pagesEconomic Reformssayooj tvNo ratings yet

- Parcor Recit ReviewerDocument7 pagesParcor Recit ReviewerNathaly Nicolle CapuchinoNo ratings yet

- Managing Bank CapitalDocument24 pagesManaging Bank CapitalHenry So E DiarkoNo ratings yet

- Introduction To Financial ManagementDocument31 pagesIntroduction To Financial ManagementzewdieNo ratings yet

- 29 - Liabilities - TheoryDocument5 pages29 - Liabilities - Theoryjaymark canayaNo ratings yet

- Zoomlion Annual ReportDocument192 pagesZoomlion Annual ReportHung Wen GoNo ratings yet

- Financial Management Final Assignment Section 4 Group 9Document8 pagesFinancial Management Final Assignment Section 4 Group 9saksham.dm253064No ratings yet

- MSE604 Ch. 4 - Time Value of MoneyDocument44 pagesMSE604 Ch. 4 - Time Value of MoneyRizqi Fadhlillah100% (1)

- AE 315 FM Sum2021 Week 3 Capital Budgeting Quiz Anserki B FOR DISTRIBDocument7 pagesAE 315 FM Sum2021 Week 3 Capital Budgeting Quiz Anserki B FOR DISTRIBArly Kurt TorresNo ratings yet

- Practice Questions For BAAC 550 Question 1 Property, Plant and Equipment (15 Marks, 15 Minutes)Document19 pagesPractice Questions For BAAC 550 Question 1 Property, Plant and Equipment (15 Marks, 15 Minutes)Jasmine HuangNo ratings yet

- Transport Case Study by URCDocument125 pagesTransport Case Study by URCahmedkadiwalNo ratings yet

- Ramnath & Co: Interpretation of Beneficial ProvisionsDocument6 pagesRamnath & Co: Interpretation of Beneficial ProvisionsVaidehi KolheNo ratings yet

- Petroleraa ZuataDocument9 pagesPetroleraa ZuataArka MitraNo ratings yet

Download as xls, pdf, or txt

You might also like

- Comparative Income Statements and Balance Sheets For Merck ($ Millions) FollowDocument6 pagesComparative Income Statements and Balance Sheets For Merck ($ Millions) FollowIman naufalNo ratings yet

- 17020841116Document13 pages17020841116Khushboo RajNo ratings yet

- Macrs Depreciation: New Smart Phone Calculation AnalysisDocument4 pagesMacrs Depreciation: New Smart Phone Calculation AnalysisErro Jaya Rosady100% (1)

- Directors of Federal Reserve Bank of New York (1914-2014)Document47 pagesDirectors of Federal Reserve Bank of New York (1914-2014)William Litynski100% (1)

- Lease ContractDocument2 pagesLease ContractAngie NaveraNo ratings yet

- Financial Analysis of P & GDocument25 pagesFinancial Analysis of P & Ghitesh_mahajan_3No ratings yet

- Hgs Q4 & Full Year Fy2018 Financials & Fact Sheet: Hinduja Global Solutions LimitedDocument6 pagesHgs Q4 & Full Year Fy2018 Financials & Fact Sheet: Hinduja Global Solutions LimitedChirag LaxmanNo ratings yet

- Gail (India)Document93 pagesGail (India)Ashley KamalasanNo ratings yet

- WA2Document3 pagesWA2Ahmed HassaanNo ratings yet

- Horizontal & Vertical Analysis of Maruti Suzuki India LTDDocument17 pagesHorizontal & Vertical Analysis of Maruti Suzuki India LTDBerkshire Hathway coldNo ratings yet

- DCF Valuation ExerciseDocument18 pagesDCF Valuation ExerciseAkram MohiddinNo ratings yet

- Profitability Ratio 2Document18 pagesProfitability Ratio 2Wynphap podiotanNo ratings yet

- Result Update Presentation - Q2 FY18: NOVEMBER 09, 2017Document11 pagesResult Update Presentation - Q2 FY18: NOVEMBER 09, 2017Mohit PariharNo ratings yet

- WSP OpModelPrepDocument22 pagesWSP OpModelPreplewisbjunkNo ratings yet

- A2.1 Roe 1Document14 pagesA2.1 Roe 1monemNo ratings yet

- TVS Motor Company: CMP: INR549 TP: INR548Document12 pagesTVS Motor Company: CMP: INR549 TP: INR548anujonwebNo ratings yet

- Financial Ratios Activity Answer KeyDocument8 pagesFinancial Ratios Activity Answer KeyMarienell YuNo ratings yet

- CHB Jun19 PDFDocument14 pagesCHB Jun19 PDFSajeetha MadhavanNo ratings yet

- Financial Modeling - Module I - Workbook 09.28.09Document38 pagesFinancial Modeling - Module I - Workbook 09.28.09rabiaasimNo ratings yet

- Learn2Invest Session 10 - Asian Paints ValuationsDocument8 pagesLearn2Invest Session 10 - Asian Paints ValuationsMadhur BathejaNo ratings yet

- CLA KPI BOD MayDocument248 pagesCLA KPI BOD MaySiluman UlarNo ratings yet

- Chapter 2 - Financial StatementsDocument23 pagesChapter 2 - Financial StatementsErone Edward CatolinNo ratings yet

- Sothin and SonsDocument16 pagesSothin and SonsDicksonNo ratings yet

- Illustration For Financial Analysis Using RatioDocument2 pagesIllustration For Financial Analysis Using RatioamahaktNo ratings yet

- Balkrishna Industries LTD: Investor Presentation February 2020Document30 pagesBalkrishna Industries LTD: Investor Presentation February 2020PIBM MBA-FINANCENo ratings yet

- Reshma Chauhan - PGFC1927 (BOCA)Document9 pagesReshma Chauhan - PGFC1927 (BOCA)Surbhî GuptaNo ratings yet

- Financial Analysis: Nestle India Ltd. ACC LTDDocument20 pagesFinancial Analysis: Nestle India Ltd. ACC LTDrahil0786No ratings yet

- Whirlpool Financial AnalysisDocument5 pagesWhirlpool Financial AnalysisuddhavkulkarniNo ratings yet

- Company AssignmentDocument3 pagesCompany Assignmentrajeshparida9624No ratings yet

- Semen Indonesia Persero TBK PT: at A GlanceDocument3 pagesSemen Indonesia Persero TBK PT: at A GlanceRendy SentosaNo ratings yet

- Result Update Presentation - Q1 FY18: AUGUST 10, 2017Document10 pagesResult Update Presentation - Q1 FY18: AUGUST 10, 2017Mohit PariharNo ratings yet

- Ratio Analysis Summary Particulars Mar '17 Mar '18 Mar '19 Revenue Growth Profitability RatiosDocument10 pagesRatio Analysis Summary Particulars Mar '17 Mar '18 Mar '19 Revenue Growth Profitability RatiosKAVYA GUPTANo ratings yet

- I. Financial AssumptionsDocument14 pagesI. Financial AssumptionsJaera shopaholicNo ratings yet

- What Do We Achive? Interpretation: Other PointsDocument3 pagesWhat Do We Achive? Interpretation: Other PointsDibyaranjan SahooNo ratings yet

- Abrar Engro Excel SheetDocument4 pagesAbrar Engro Excel SheetManahil FayyazNo ratings yet

- Total Revenue: Income StatementDocument4 pagesTotal Revenue: Income Statementmonica asifNo ratings yet

- Vivimed Model VFDocument19 pagesVivimed Model VFShaileshAgrawalNo ratings yet

- Ashok Leyland: CMP: INR115 TP: INR134 (+17%)Document10 pagesAshok Leyland: CMP: INR115 TP: INR134 (+17%)Jitendra GaglaniNo ratings yet

- FM Assignment UcDocument4 pagesFM Assignment UcabhishelNo ratings yet

- Cortez Exam in Business FinanceDocument4 pagesCortez Exam in Business FinanceFranchesca CortezNo ratings yet

- Fixed Assets: Case 25.1: Patel Computers System AssetsDocument2 pagesFixed Assets: Case 25.1: Patel Computers System AssetsMukul KadyanNo ratings yet

- Accounts AssignmentDocument17 pagesAccounts AssignmentApoorvNo ratings yet

- Gita AgricultureDocument20 pagesGita AgriculturemrigendrarimalNo ratings yet

- Bank Performance Analysis - Anushka Gupta (Kotak Mahindra Bank)Document13 pagesBank Performance Analysis - Anushka Gupta (Kotak Mahindra Bank)Surbhî GuptaNo ratings yet

- FinancialsDocument10 pagesFinancialstimothyNo ratings yet

- Spread SheetDocument2 pagesSpread SheetDwi PermanaNo ratings yet

- Lbo W DCF Model SampleDocument33 pagesLbo W DCF Model Samplejulita rachmadewiNo ratings yet

- HDFC Bank Annual ReportDocument1 pageHDFC Bank Annual ReportlovenotafeelingNo ratings yet

- FinShiksha Maruti Suzuki UnsolvedDocument12 pagesFinShiksha Maruti Suzuki UnsolvedGANESH JAINNo ratings yet

- Alembic Angel 020810Document12 pagesAlembic Angel 020810giridesh3No ratings yet

- 11.bergerac SystemsDocument12 pages11.bergerac SystemsAviralNo ratings yet

- Mett International Pty LTD Financial Forecast 3 Year SummaryDocument134 pagesMett International Pty LTD Financial Forecast 3 Year SummaryJamilexNo ratings yet

- DCFValuation JKTyre1Document195 pagesDCFValuation JKTyre1Chulbul PandeyNo ratings yet

- Kotak Mahindra Bank Ltd. Performance Analysis For The Period 2016-2020Document15 pagesKotak Mahindra Bank Ltd. Performance Analysis For The Period 2016-2020Surbhî GuptaNo ratings yet

- A1.2 Roic TreeDocument9 pagesA1.2 Roic Treesara_AlQuwaifliNo ratings yet

- Horizontal AnalysisDocument1 pageHorizontal Analysiswill burrNo ratings yet

- Financial RatiosDocument7 pagesFinancial RatiosJan TruongNo ratings yet

- MODEL - Investment AnalysisDocument6 pagesMODEL - Investment AnalysisAndrei Cătălin UngureanuNo ratings yet

- Equity Valuation: Models from Leading Investment BanksFrom EverandEquity Valuation: Models from Leading Investment BanksJan ViebigNo ratings yet

- Indian Insider Buyings June 19, 2008-DhananDocument2 pagesIndian Insider Buyings June 19, 2008-Dhananapi-3702531No ratings yet

- GilletteDocument14 pagesGilletteapi-3702531No ratings yet

- Dabur IndiaDocument43 pagesDabur Indiaapi-3702531No ratings yet

- Colgate AR March 2005Document72 pagesColgate AR March 2005ashusingh0141No ratings yet

- Fem CareDocument16 pagesFem Careapi-3702531No ratings yet

- ColgateDocument32 pagesColgateapi-3702531No ratings yet

- DUBARINDIAAR200708Document164 pagesDUBARINDIAAR200708Santosh KumarNo ratings yet

- India - Insider Buying 25th July 2008Document2 pagesIndia - Insider Buying 25th July 2008api-3702531No ratings yet

- ColgateDocument32 pagesColgateapi-3702531No ratings yet

- BSE Special Situations 17th June 2008Document2 pagesBSE Special Situations 17th June 2008api-3702531No ratings yet

- BSE Special Situations 16th June 2008Document4 pagesBSE Special Situations 16th June 2008api-3702531No ratings yet

- BSE Special Situations 18th June 2008Document1 pageBSE Special Situations 18th June 2008api-3702531No ratings yet

- Indian Insider Buyings June 17, 2008-DhananDocument2 pagesIndian Insider Buyings June 17, 2008-Dhananapi-3702531No ratings yet

- Indian Insider Buyings June 13, 2008-DhananDocument2 pagesIndian Insider Buyings June 13, 2008-Dhananapi-3702531No ratings yet

- Indian Insider Buyings June 12, 2008-DhananDocument2 pagesIndian Insider Buyings June 12, 2008-Dhananapi-3702531No ratings yet

- IAPMDocument4 pagesIAPMapi-3699305No ratings yet

- Your Money or Your Life Book ReviewDocument5 pagesYour Money or Your Life Book ReviewSaurabhkumar SinghNo ratings yet

- Test Business and FinanceDocument1 pageTest Business and FinanceKarem Yessenia OCHOCHOQUE SÁNCHEZNo ratings yet

- Hull OFOD10e MultipleChoice Questions Only Ch22Document4 pagesHull OFOD10e MultipleChoice Questions Only Ch22Kevin Molly KamrathNo ratings yet

- Project Selection Process: A) SWOT AnalysisDocument6 pagesProject Selection Process: A) SWOT AnalysisIrtiza MalikNo ratings yet

- Cash Credit Proposal For Bank FinanceDocument15 pagesCash Credit Proposal For Bank Financeajaya thakurNo ratings yet

- A. Bank Rate PolicyDocument4 pagesA. Bank Rate PolicySIMRAN SHOKEENNo ratings yet

- Architect Agreement Contract 2 PDFDocument5 pagesArchitect Agreement Contract 2 PDFS Lakhte Haider ZaidiNo ratings yet

- Course Handout MBA 306 FIN FSIDocument3 pagesCourse Handout MBA 306 FIN FSIAsma KhanNo ratings yet

- Bia Africa - Commercial Offer 2022 SMS - Feb 2023 - Eur - 230406 - 100334Document12 pagesBia Africa - Commercial Offer 2022 SMS - Feb 2023 - Eur - 230406 - 100334Kouakou Affran Rania maryliseNo ratings yet

- Law Juridical RelationDocument3 pagesLaw Juridical RelationAida StanNo ratings yet

- Sap Fi ReportsDocument41 pagesSap Fi Reportssushilo_2100% (1)

- Current and Savings Account User Manual 1 PDFDocument772 pagesCurrent and Savings Account User Manual 1 PDFthandayuthapani sundarNo ratings yet

- Project Profile Rice MillDocument1 pageProject Profile Rice Millhoquetradeintl100% (2)

- Safari - Aug 9, 2019 at 7:11 AM PDFDocument1 pageSafari - Aug 9, 2019 at 7:11 AM PDFMikaela SamonteNo ratings yet

- Economic ReformsDocument77 pagesEconomic Reformssayooj tvNo ratings yet

- Parcor Recit ReviewerDocument7 pagesParcor Recit ReviewerNathaly Nicolle CapuchinoNo ratings yet

- Managing Bank CapitalDocument24 pagesManaging Bank CapitalHenry So E DiarkoNo ratings yet

- Introduction To Financial ManagementDocument31 pagesIntroduction To Financial ManagementzewdieNo ratings yet

- 29 - Liabilities - TheoryDocument5 pages29 - Liabilities - Theoryjaymark canayaNo ratings yet

- Zoomlion Annual ReportDocument192 pagesZoomlion Annual ReportHung Wen GoNo ratings yet

- Financial Management Final Assignment Section 4 Group 9Document8 pagesFinancial Management Final Assignment Section 4 Group 9saksham.dm253064No ratings yet

- MSE604 Ch. 4 - Time Value of MoneyDocument44 pagesMSE604 Ch. 4 - Time Value of MoneyRizqi Fadhlillah100% (1)

- AE 315 FM Sum2021 Week 3 Capital Budgeting Quiz Anserki B FOR DISTRIBDocument7 pagesAE 315 FM Sum2021 Week 3 Capital Budgeting Quiz Anserki B FOR DISTRIBArly Kurt TorresNo ratings yet

- Practice Questions For BAAC 550 Question 1 Property, Plant and Equipment (15 Marks, 15 Minutes)Document19 pagesPractice Questions For BAAC 550 Question 1 Property, Plant and Equipment (15 Marks, 15 Minutes)Jasmine HuangNo ratings yet

- Transport Case Study by URCDocument125 pagesTransport Case Study by URCahmedkadiwalNo ratings yet

- Ramnath & Co: Interpretation of Beneficial ProvisionsDocument6 pagesRamnath & Co: Interpretation of Beneficial ProvisionsVaidehi KolheNo ratings yet

- Petroleraa ZuataDocument9 pagesPetroleraa ZuataArka MitraNo ratings yet