Download as pdf or txt

You might also like

- Rexroth Analog Positioning ModeDocument12 pagesRexroth Analog Positioning ModehfvlNo ratings yet

- Laboratory Quality/Management: A Workbook with an Eye on AccreditationFrom EverandLaboratory Quality/Management: A Workbook with an Eye on AccreditationRating: 5 out of 5 stars5/5 (1)

- NQA Business Profile 2019Document38 pagesNQA Business Profile 2019denny simamoraNo ratings yet

- IATF Auditor Guide PDFDocument32 pagesIATF Auditor Guide PDFJosé Carlos GarBad100% (4)

- PB 9104-1 enDocument49 pagesPB 9104-1 enVenkatesan KattappanNo ratings yet

- Automotive Process Approach Audit For IATF 16949 - 2016Document4 pagesAutomotive Process Approach Audit For IATF 16949 - 2016isolongNo ratings yet

- Intro - ISO 19011 - v4 - r2 - ENG - 11 - Audit Closing MeetingDocument7 pagesIntro - ISO 19011 - v4 - r2 - ENG - 11 - Audit Closing MeetingHamza HamNo ratings yet

- Maruti Suzuki Final ProjectDocument63 pagesMaruti Suzuki Final ProjectMilind Singanjude75% (4)

- Webinar ISODocument54 pagesWebinar ISOMF100% (1)

- Aim FPL Aidc Ip03Document4 pagesAim FPL Aidc Ip03Ahmad YaseenNo ratings yet

- Ch1 2016CISADocument139 pagesCh1 2016CISADavid sangaNo ratings yet

- Opening Meeting Presentation (VFeb 2023)Document19 pagesOpening Meeting Presentation (VFeb 2023)mritun007No ratings yet

- NQA Webinar ISO 9001 Back To Basics Internal Auditing 20-01-2023Document54 pagesNQA Webinar ISO 9001 Back To Basics Internal Auditing 20-01-2023Yousef BukhariNo ratings yet

- Johnstone 9e Auditing 1Document98 pagesJohnstone 9e Auditing 1didiNo ratings yet

- VDA 6.3 Management: R. Dan ReidDocument61 pagesVDA 6.3 Management: R. Dan ReidAlpha Excellence consultingNo ratings yet

- Tqm-I - 09 - Iso 9000Document15 pagesTqm-I - 09 - Iso 9000Saransh GoelNo ratings yet

- Dr. P. K. ChaudharyDocument41 pagesDr. P. K. ChaudharyKM DIMPI SINGHNo ratings yet

- Awareness and Internal Auditor TRG IATF 16949 August 22Document95 pagesAwareness and Internal Auditor TRG IATF 16949 August 22Atul SURVE100% (1)

- Nathan & Nathan Consultants Pvt. Ltd. NNCPL/PPT/011Document95 pagesNathan & Nathan Consultants Pvt. Ltd. NNCPL/PPT/011Naveen RajhaNo ratings yet

- 0 - GA - General Assembly Presentation - Reqs Team - IAQG Atlanta - May 2019 R2Document31 pages0 - GA - General Assembly Presentation - Reqs Team - IAQG Atlanta - May 2019 R2Mani Rathinam RajamaniNo ratings yet

- Iso Qualified Company Standard Procedure BUSINESS Process MapDocument13 pagesIso Qualified Company Standard Procedure BUSINESS Process MapJohn P. BandoquilloNo ratings yet

- IAQG SCMH-3.1.2-Managing-Product-and-Process-Variation-in-Support-of-9103-Overview-Rev-C-Dated-21OCT2022Document37 pagesIAQG SCMH-3.1.2-Managing-Product-and-Process-Variation-in-Support-of-9103-Overview-Rev-C-Dated-21OCT2022LiherNo ratings yet

- SCMH 3.1.3 Managing Product and Process Variation in Support of 9103 Rev B Dated 27SEP2018Document102 pagesSCMH 3.1.3 Managing Product and Process Variation in Support of 9103 Rev B Dated 27SEP2018Vinod SaleNo ratings yet

- The Certified Government Auditing Professional® (CGAP®) Exam - Preparatory CourseDocument4 pagesThe Certified Government Auditing Professional® (CGAP®) Exam - Preparatory CourseJames Stallins Jr.No ratings yet

- PRI & Nadcap Overview: Updated 15-May 2014 For ASTM E-01Document35 pagesPRI & Nadcap Overview: Updated 15-May 2014 For ASTM E-01amirkhakzad498No ratings yet

- PB 9104-1 en PDFDocument49 pagesPB 9104-1 en PDFjferreiraNo ratings yet

- Mo1Da1Se1 Introduction Version PrintReadyDocument41 pagesMo1Da1Se1 Introduction Version PrintReadyCristian Eduardo Ariel ROJASNo ratings yet

- Quality Management SystemsDocument38 pagesQuality Management SystemsSrishKumarNo ratings yet

- API Spec Q1 (10th Edition) Awareness by Decky Antony KiftaDocument81 pagesAPI Spec Q1 (10th Edition) Awareness by Decky Antony Kiftadecky antonyNo ratings yet

- Practical TOGAF 9 Sample Soln 2014Q2Document35 pagesPractical TOGAF 9 Sample Soln 2014Q2HPot PotTechNo ratings yet

- Structural Integrity ManagementDocument22 pagesStructural Integrity Managementonnly1964100% (1)

- Iso TS 16949Document35 pagesIso TS 16949dyogasara2No ratings yet

- CSI Blackbelt in SEATA - Internal Audit Master Class (Malaysia), Featuring Mr. TOMMY SEAHDocument4 pagesCSI Blackbelt in SEATA - Internal Audit Master Class (Malaysia), Featuring Mr. TOMMY SEAHCFE International Consultancy GroupNo ratings yet

- Lecture - 6Document17 pagesLecture - 6Sheikh Muneeb Ul HaqNo ratings yet

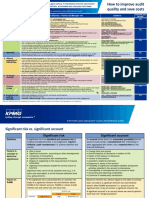

- How To Improve Audit Quality and Save CostsDocument2 pagesHow To Improve Audit Quality and Save CostsSalauddin Kader ACCANo ratings yet

- IAQG 9120:2009 Revision Overview: Prepared by IAQG 9120 TeamDocument24 pagesIAQG 9120:2009 Revision Overview: Prepared by IAQG 9120 TeamYogita NarangNo ratings yet

- F8-06 DocumentationDocument20 pagesF8-06 DocumentationReever RiverNo ratings yet

- Audit PlanningDocument17 pagesAudit PlanningMathew P. VargheseNo ratings yet

- Pushkar Narsikar ResumeDocument2 pagesPushkar Narsikar ResumenarsikarNo ratings yet

- Unit 5Document34 pagesUnit 5MECH HODNo ratings yet

- Sundar GDocument2 pagesSundar GRazvan GheorghiesNo ratings yet

- Engineering Job CV FormatDocument3 pagesEngineering Job CV FormatOjolowo OlamideNo ratings yet

- Moving To CMMI Level 4 (SW/SE/IPPD) : CMMI User Conference Denver, Colorado November 2003 Sarah Bengzon, Associate PartnerDocument17 pagesMoving To CMMI Level 4 (SW/SE/IPPD) : CMMI User Conference Denver, Colorado November 2003 Sarah Bengzon, Associate Partnerfire_mNo ratings yet

- Mid Term ItsmDocument11 pagesMid Term ItsmRohan TawarNo ratings yet

- RICI - ISO 14001 EMS Lead AuditorDocument8 pagesRICI - ISO 14001 EMS Lead AuditorUsamah Al-HussainiNo ratings yet

- 3-DPA Awareness ProgramDocument27 pages3-DPA Awareness ProgramVishal MaliNo ratings yet

- Ramya Pabbisetti: Consultant, OAS - UHG - IIM IndoreDocument2 pagesRamya Pabbisetti: Consultant, OAS - UHG - IIM IndoreJyotirmoy GhoshNo ratings yet

- Prospectus: Title: Sponsor: Initiative LeadDocument3 pagesProspectus: Title: Sponsor: Initiative LeadtadiganeshNo ratings yet

- NERC CIP - Version - 5 - Revisions - Technical - Conferences-Posted - Version - January - 2014Document61 pagesNERC CIP - Version - 5 - Revisions - Technical - Conferences-Posted - Version - January - 2014paladin777No ratings yet

- Insurance Case Study TestingDocument18 pagesInsurance Case Study Testingpaddy_workNo ratings yet

- BPI 2019 Week 4-Define MeasureDocument20 pagesBPI 2019 Week 4-Define MeasureELVIRA ABIDINNo ratings yet

- Overview of Working Papers in RAMDocument21 pagesOverview of Working Papers in RAMIsha PopNo ratings yet

- Internal Audit Checklist Q1 - ISO 2015Document29 pagesInternal Audit Checklist Q1 - ISO 2015ayşe çavdar100% (1)

- AdvaMed CFQ Slides PUBLICDocument13 pagesAdvaMed CFQ Slides PUBLICluisrayvcNo ratings yet

- 6 - Kimberly Todd - QA and QCDocument18 pages6 - Kimberly Todd - QA and QCFizz FirdausNo ratings yet

- Intern Presentation SiemensDocument17 pagesIntern Presentation Siemensapi-336689769No ratings yet

- IDENTCO Value Assessment For Labels: IVAL StagesDocument2 pagesIDENTCO Value Assessment For Labels: IVAL StagesJorge Navarro BeckerNo ratings yet

- Quality Management SystemsDocument49 pagesQuality Management SystemsShanmugavalli VijaiNo ratings yet

- Audit Checklist 5 Management Commitment & ResponsibilityDocument4 pagesAudit Checklist 5 Management Commitment & ResponsibilityGilbert MendozaNo ratings yet

- RICI - ISO 14001 Internal Audit - Rev 03Document8 pagesRICI - ISO 14001 Internal Audit - Rev 03Usamah Al-HussainiNo ratings yet

- Lac ImsDocument4 pagesLac ImsMelwin DsouzaNo ratings yet

- Is14489 2018Document23 pagesIs14489 2018Gautam ShahNo ratings yet

- ICOP Scheme Transition Roadmap Rev 2 21 2022Document6 pagesICOP Scheme Transition Roadmap Rev 2 21 2022salih yukselNo ratings yet

- 2022-12-07 - SR004 For 9104 Series Transition Rev B v2Document6 pages2022-12-07 - SR004 For 9104 Series Transition Rev B v2salih yukselNo ratings yet

- 400 OASIS NG Feedback Process V6Document52 pages400 OASIS NG Feedback Process V6salih yukselNo ratings yet

- IAFML42016 Issue 8 10052016Document23 pagesIAFML42016 Issue 8 10052016salih yukselNo ratings yet

- (CHIP IC) w25x20cl - A02Document51 pages(CHIP IC) w25x20cl - A02Felipe de san anicetoNo ratings yet

- Quiz 1 Internet ShoppingDocument1 pageQuiz 1 Internet ShoppingEloy RicouzNo ratings yet

- KickStart 19Document2 pagesKickStart 19Venu GopalNo ratings yet

- A GMM Approach For Dealing With Missing DataDocument41 pagesA GMM Approach For Dealing With Missing DataraghidkNo ratings yet

- Ruwanpura Expressway Design ProjectDocument5 pagesRuwanpura Expressway Design ProjectMuhammadh MANo ratings yet

- NOC Video Walls Solutions - 4!10!2021 Rالبريد1Document2 pagesNOC Video Walls Solutions - 4!10!2021 Rالبريد1Sayed HamedNo ratings yet

- Display CAT PDFDocument2 pagesDisplay CAT PDFAndres130No ratings yet

- CA ProjectDocument21 pagesCA Projectkalaswami100% (1)

- Wagner Power Steamer ManualDocument8 pagesWagner Power Steamer ManualagsmarioNo ratings yet

- READMEDocument25 pagesREADMENate ClarkNo ratings yet

- 3 Simpson Wickelgren (2007) Naked Exclusion Efficient Breach and Downstream Competition1Document10 pages3 Simpson Wickelgren (2007) Naked Exclusion Efficient Breach and Downstream Competition1211257No ratings yet

- D H Reid - Organic Compounds of Sulphur, Selenium, and Tellurium Vol 1-Royal Society of Chemistry (1970)Document518 pagesD H Reid - Organic Compounds of Sulphur, Selenium, and Tellurium Vol 1-Royal Society of Chemistry (1970)julianpellegrini860No ratings yet

- Manual de Usuario Motor Fuera de Borda.Document68 pagesManual de Usuario Motor Fuera de Borda.Carlos GallardoNo ratings yet

- Performance Task 1. Piecewise FunctionDocument3 pagesPerformance Task 1. Piecewise FunctionKatherine Jane GeronaNo ratings yet

- Dicionário Assírio SDocument452 pagesDicionário Assírio SAlexandre Luis Dos Santos100% (1)

- 9 Polyethylene Piping SystemDocument4 pages9 Polyethylene Piping SystemPrashant PatilNo ratings yet

- Shipham Special Alloy ValvesDocument62 pagesShipham Special Alloy ValvesYogi173No ratings yet

- BiodiversityR PDFDocument128 pagesBiodiversityR PDFEsteban VegaNo ratings yet

- Topic 6:sustainability & Green EngineeringDocument5 pagesTopic 6:sustainability & Green EngineeringyanNo ratings yet

- ICC Air 2009 CL387 - SrpskiDocument2 pagesICC Air 2009 CL387 - SrpskiZoran DimitrijevicNo ratings yet

- VLANS and Other HardwareDocument20 pagesVLANS and Other HardwareVishal KushwahaNo ratings yet

- Formulas To LearnDocument3 pagesFormulas To LearnHuệ LêNo ratings yet

- Athul AjiDocument5 pagesAthul AjiAsif SNo ratings yet

- Trad Ic Mock ExamDocument15 pagesTrad Ic Mock ExamArvin AltamiaNo ratings yet

- OSINTDocument49 pagesOSINTMARCUS VINICIUSNo ratings yet

- Ace3 Unit8 TestDocument3 pagesAce3 Unit8 Testnatacha100% (3)

- SPP ADC Flightplan UnderstandingDocument25 pagesSPP ADC Flightplan UnderstandingYesid BarraganNo ratings yet

- EPDDocument34 pagesEPDRobin AbrahamNo ratings yet